MAA303 Auditing: Financial Analysis & Risk Assessment - Beautiful Ltd

VerifiedAdded on 2023/04/21

|9

|1572

|102

Case Study

AI Summary

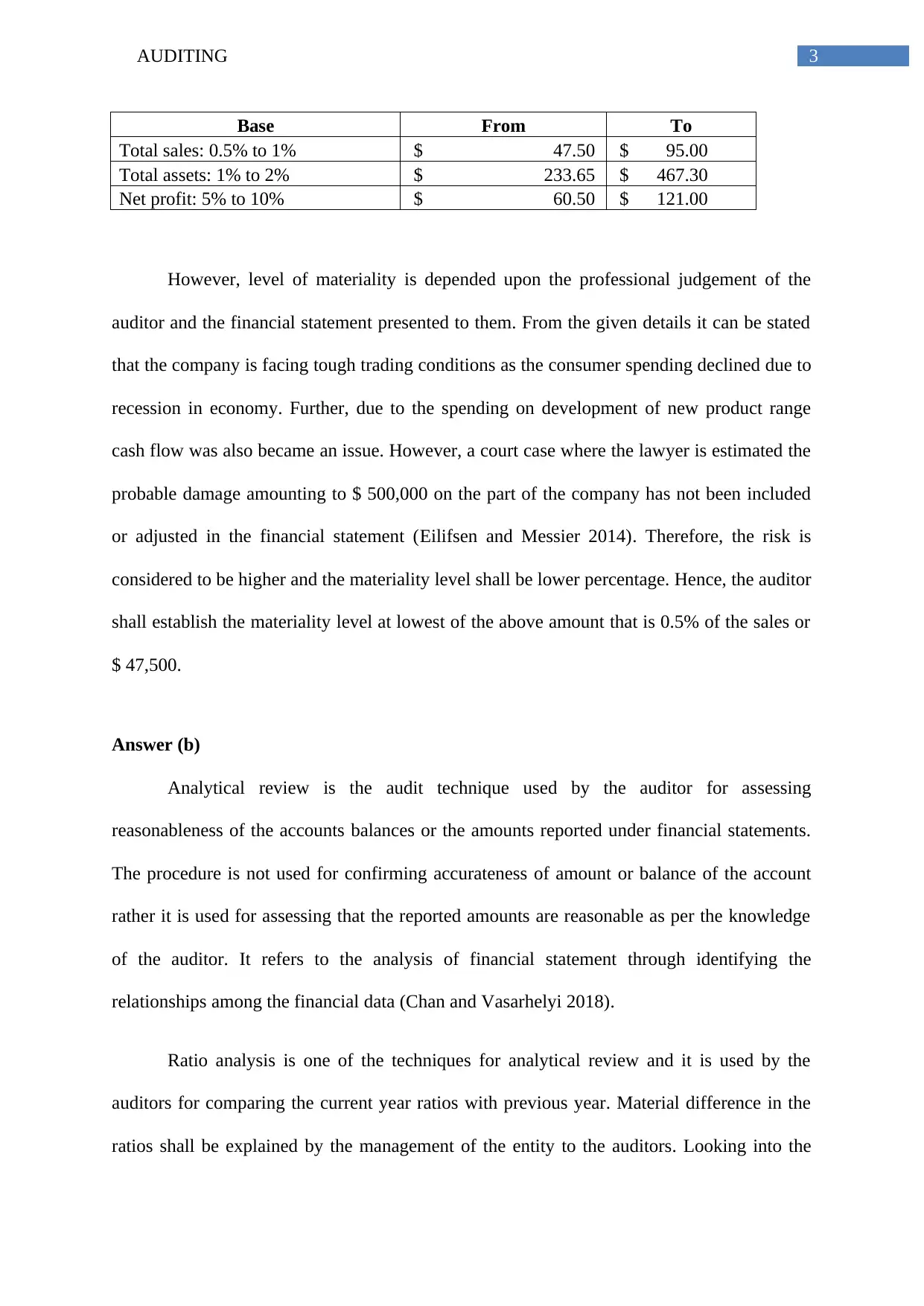

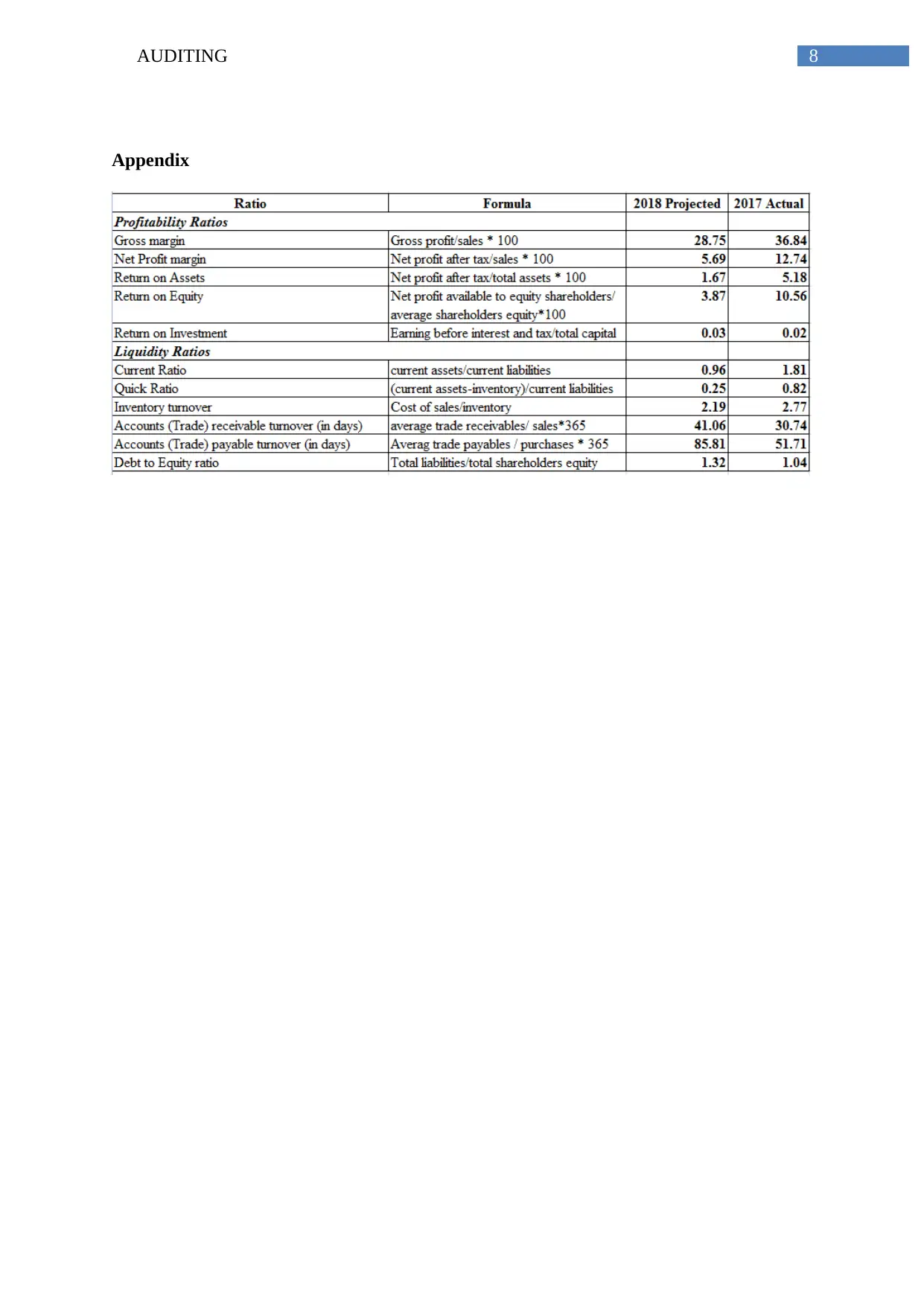

This report analyzes the financial performance of Beautiful Products Ltd, establishing a materiality benchmark based on provided information. It conducts an analytical review to identify control and inherent risks crucial for audit planning. The analysis involves assessing materiality, with a recommendation to set it at 0.5% of sales due to the company's financial struggles and a pending lawsuit. The analytical review reveals a deteriorating liquidity position, increased leverage, and declining profitability, prompting questions for management. Key inherent risks include the unadjusted lawsuit and potential misstatements due to financial difficulties, while control risks are evaluated through transaction documentation. The report concludes that auditors should scrutinize significant changes in financial performance and carefully plan materiality based on sales.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.