Financial Auditing Case Study: Ethical Issues and Independence

VerifiedAdded on 2023/04/20

|5

|1202

|153

Case Study

AI Summary

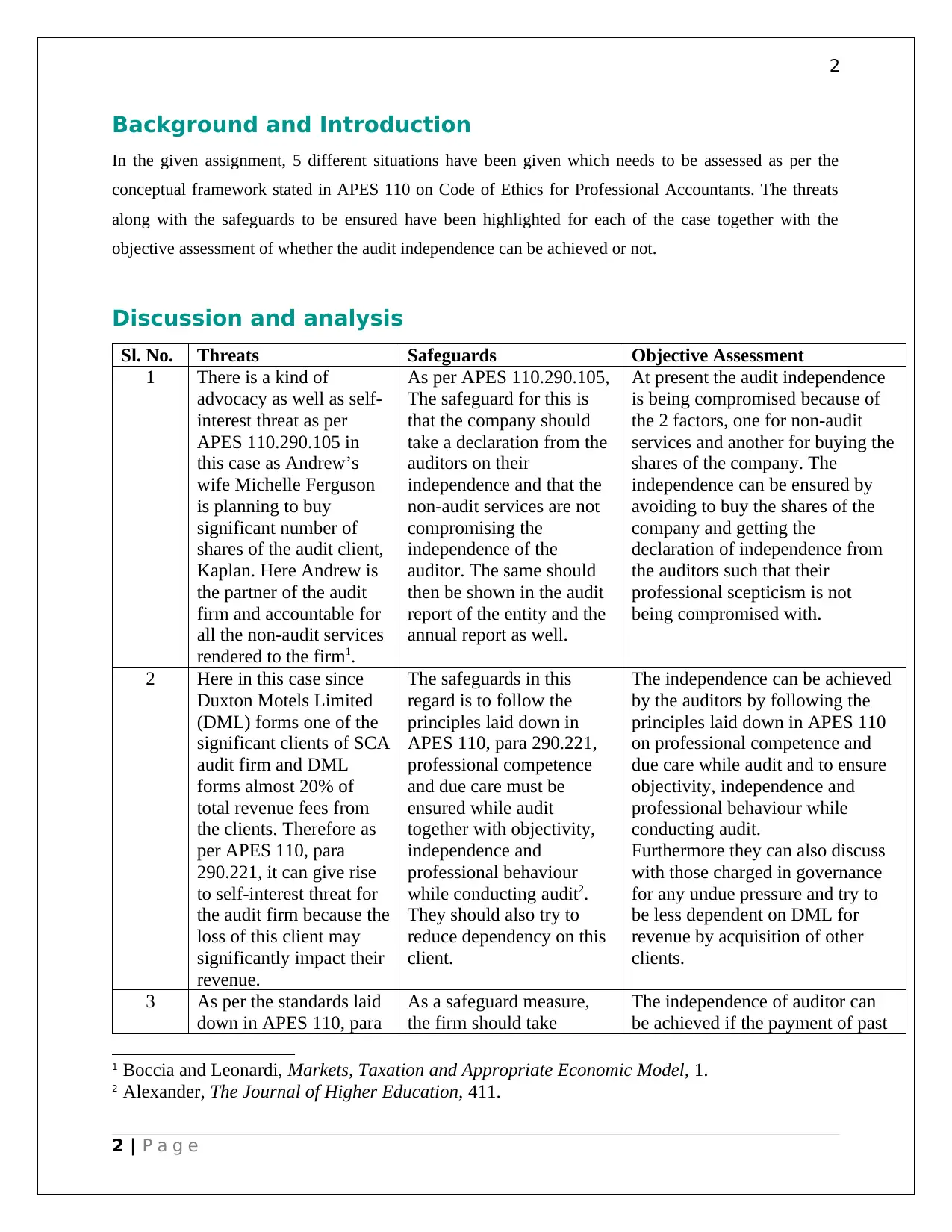

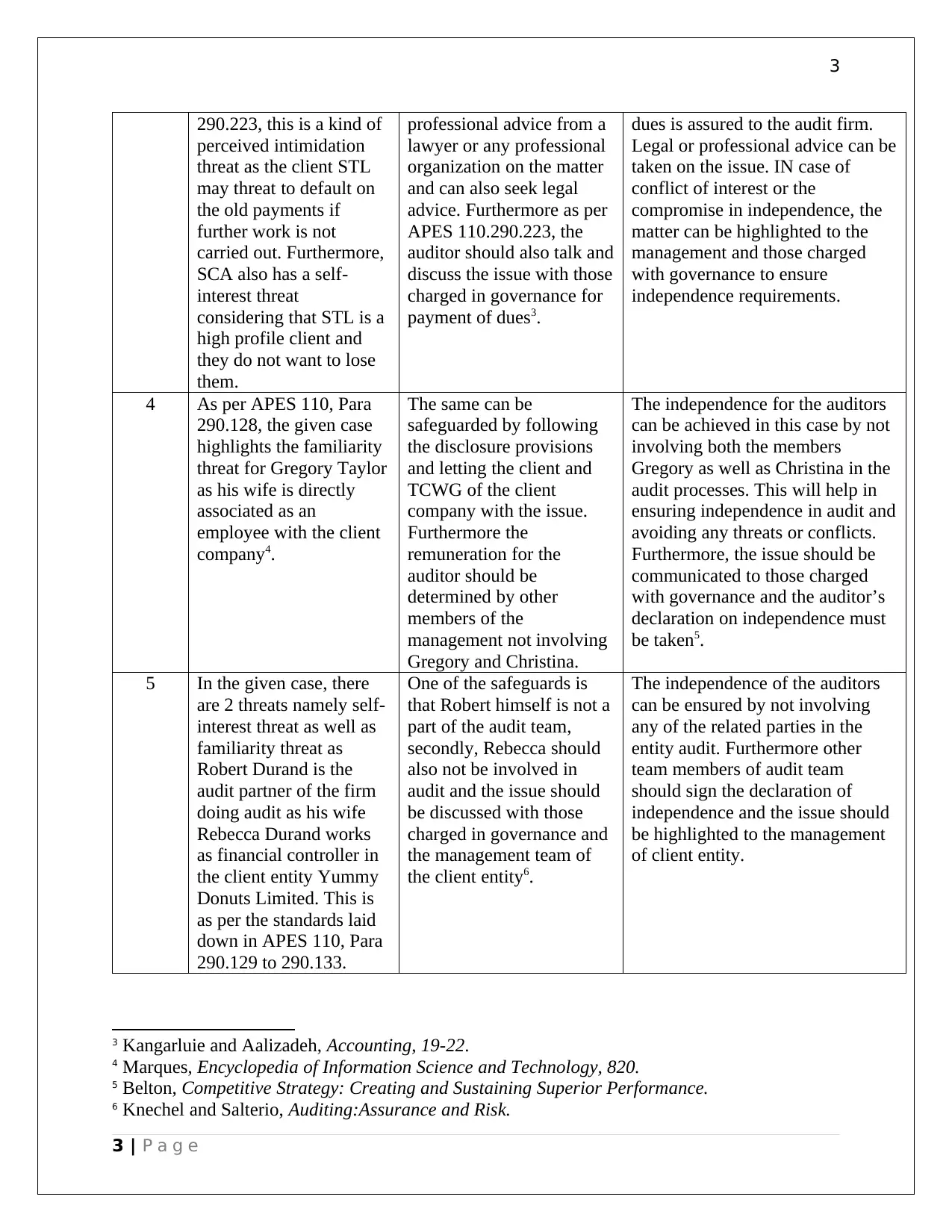

This assignment analyzes five different scenarios related to auditing, assurance, and risk assessment, based on the conceptual framework of APES 110 on the Code of Ethics for Professional Accountants. The analysis identifies threats to auditor independence, such as advocacy, self-interest, intimidation, and familiarity threats, along with the corresponding safeguards to mitigate these threats. Each case provides an objective assessment of whether audit independence can be achieved, considering factors like non-audit services, share ownership, client revenue dependency, and relationships between auditors and client personnel. The assignment emphasizes the importance of professional competence, due care, objectivity, independence, and professional behavior in conducting audits. The solutions suggest safeguards like declarations of independence, reducing client dependency, seeking legal or professional advice, and ensuring that related parties are not involved in the audit process to maintain auditor independence and ethical standards.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.