Auditing Case Study Solution

VerifiedAdded on 2019/11/20

|7

|1838

|148

Homework Assignment

AI Summary

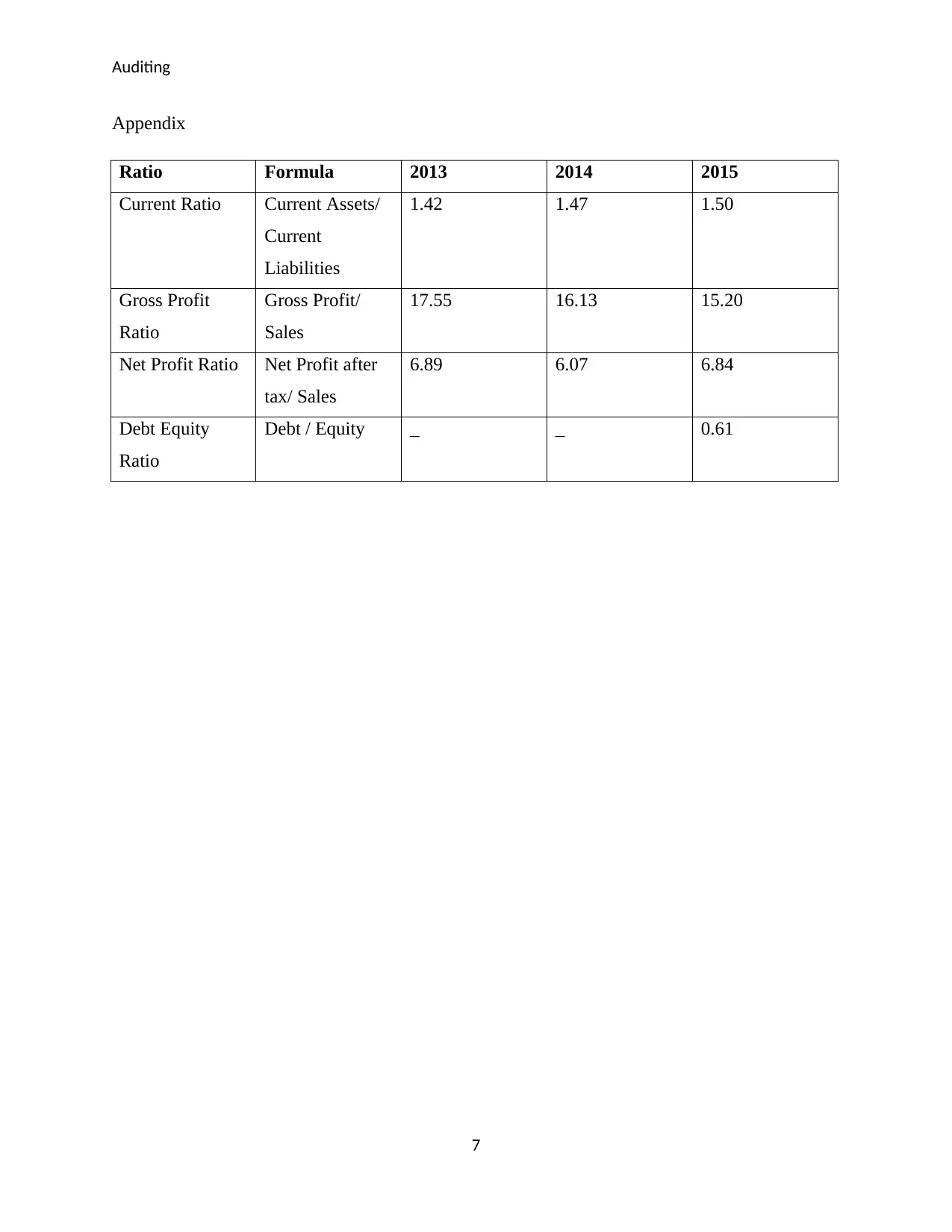

This assignment presents a case study of DIPL Ltd., focusing on auditing its financial records. The solution addresses three key areas: Firstly, it recommends analytical procedures like ratio analysis (comparing current ratios, gross profit ratios, and net profit ratios across three years) and transaction confirmation to assess the company's financial health and detect anomalies. Secondly, it identifies inherent risks, such as the discontinuation of the old IT system and the potential for bias from a financially interested CEO. Thirdly, it discusses potential frauds, including unrecorded transactions and inventory inflation, and their impact on the auditor's assessment. The solution emphasizes the auditor's responsibility to use professional skepticism and not solely rely on management-provided data. References to relevant auditing literature are provided.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.