Research Project: Auditing Changes & Australian Companies - BUS707

VerifiedAdded on 2023/06/11

|9

|871

|356

Project

AI Summary

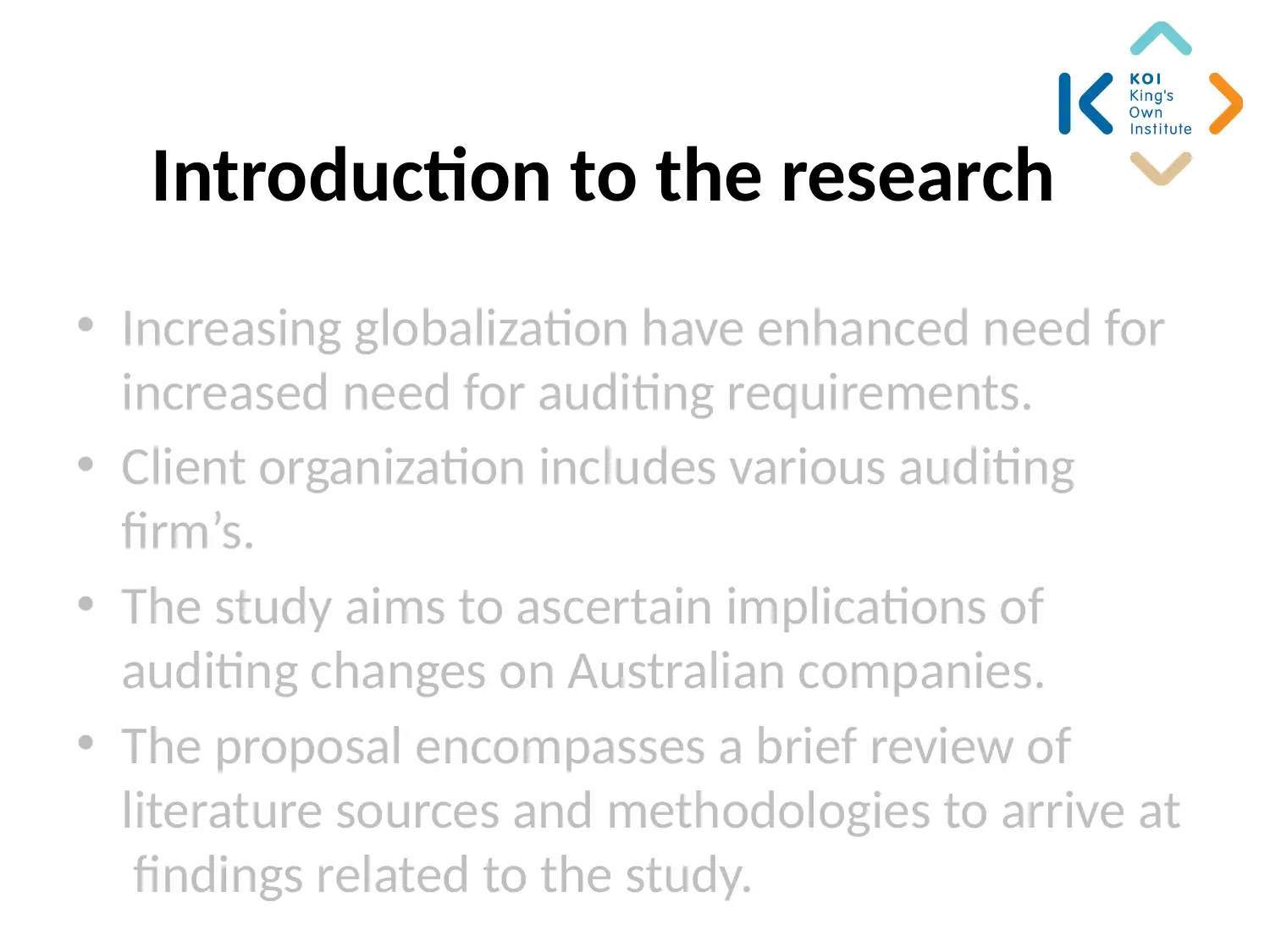

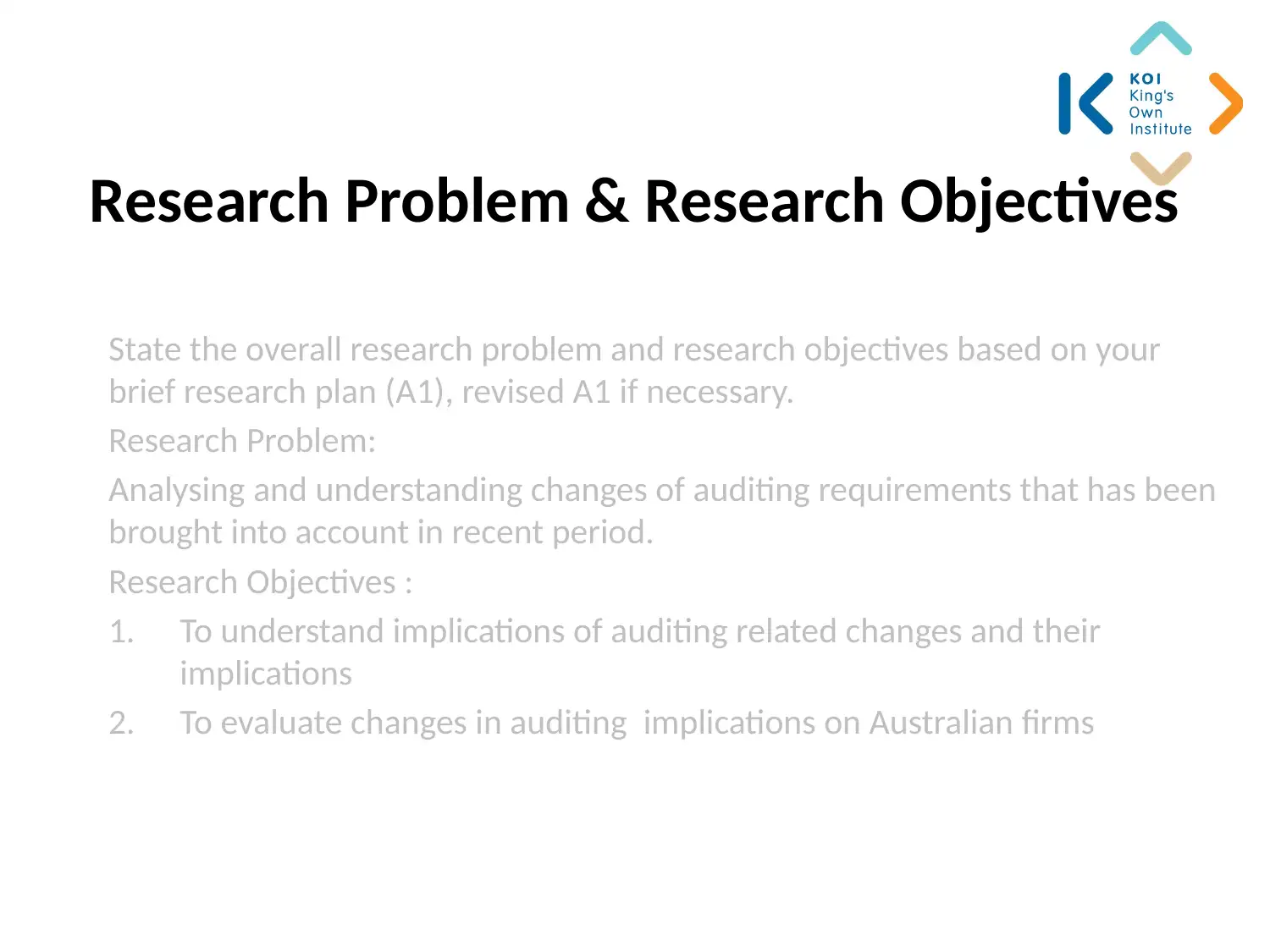

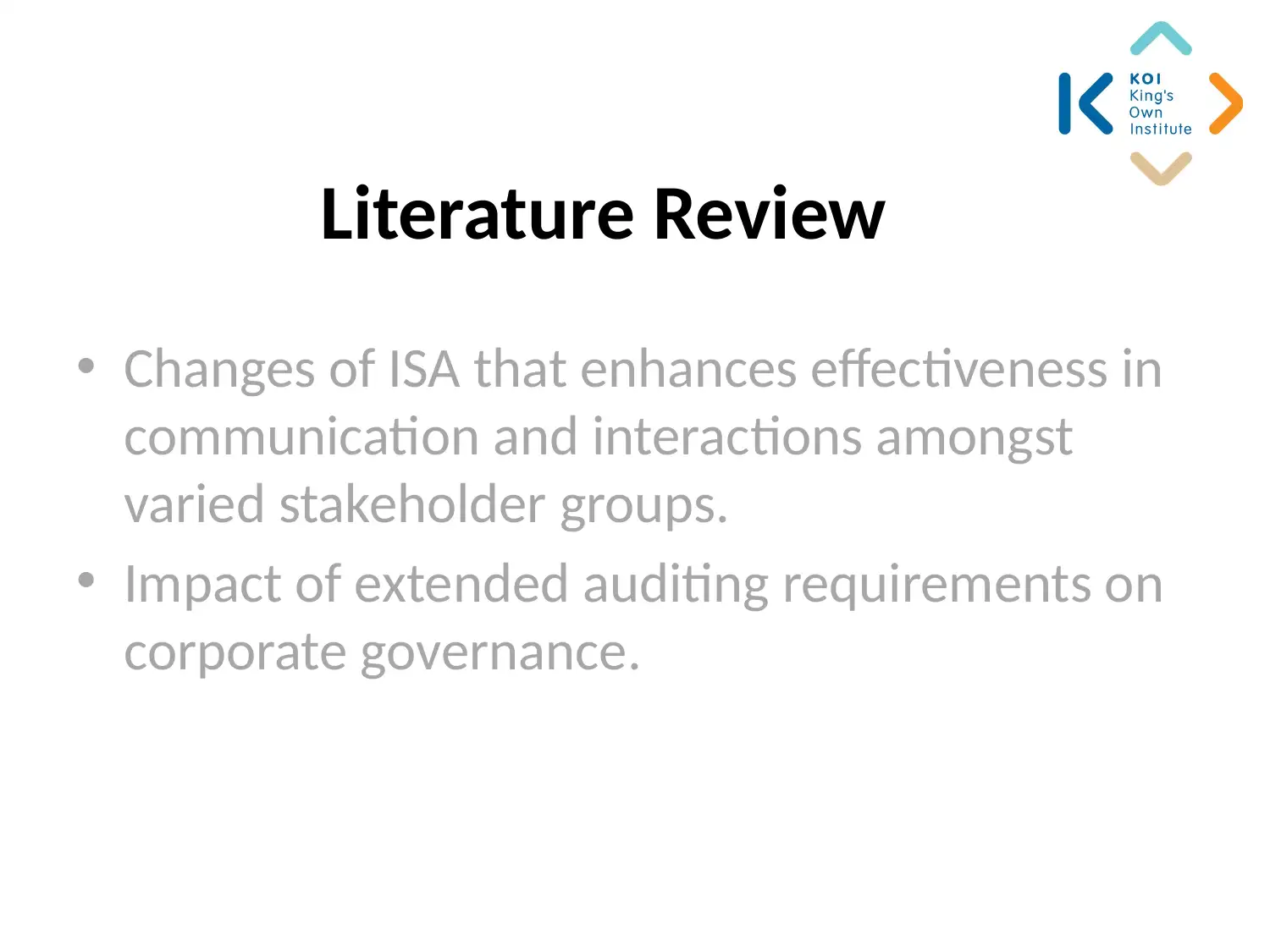

This research project investigates the implications of recent auditing changes on Australian companies. It addresses the increasing need for enhanced auditing requirements due to globalization. The study aims to analyze and understand the changes in auditing requirements, evaluate their impact on Australian firms, and understand the implications of these changes. An exploratory research design with a mixed-methods approach, combining qualitative and quantitative data, is employed. Primary and secondary data will be collected through interviews, observations, surveys, and experiments. The sampling frame includes auditors from various Australian auditing organizations. Data analysis will involve theme-based analysis for qualitative research and statistical analysis for quantitative research, ensuring all ethical concerns are addressed by adhering to strict procedures. The research references a variety of sources discussing changes in ISA, auditor reporting, and audit quality.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.