ACCT20075 Auditing Report: Financial Analysis of Crown Resorts Company

VerifiedAdded on 2022/12/27

|14

|3368

|1

Report

AI Summary

This report analyzes the audit of Crown Resorts, an Australian gaming company. It begins with an introduction to auditing and its importance, followed by an overview of the company. The report is divided into three sections. Section 1 focuses on materiality in the audit, including planning materiality calculations and the review of disclosures. Section 2 provides an analytical review of the company, including liquidity, profitability, efficiency, and leverage ratios. Section 3 analyzes the cash flow statement, discusses the going concern assumption, and analyzes the auditor's report, focusing on key audit matters. The report concludes with a summary of findings and references.

Running head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Introduction................................................................................................................................3

Section 1.....................................................................................................................................3

Materiality in Audit................................................................................................................3

Review of Disclosures............................................................................................................5

Section 2.....................................................................................................................................5

Analytical Review of Company.............................................................................................5

Section 3...................................................................................................................................10

Analysis of Cash Flow Statement........................................................................................10

Going Concern.....................................................................................................................10

Analysis of Auditor Report..................................................................................................11

Key Audit Matter.................................................................................................................11

Conclusion................................................................................................................................11

Reference and Bibliography.....................................................................................................13

AUDITING

Table of Contents

Introduction................................................................................................................................3

Section 1.....................................................................................................................................3

Materiality in Audit................................................................................................................3

Review of Disclosures............................................................................................................5

Section 2.....................................................................................................................................5

Analytical Review of Company.............................................................................................5

Section 3...................................................................................................................................10

Analysis of Cash Flow Statement........................................................................................10

Going Concern.....................................................................................................................10

Analysis of Auditor Report..................................................................................................11

Key Audit Matter.................................................................................................................11

Conclusion................................................................................................................................11

Reference and Bibliography.....................................................................................................13

2

AUDITING

Introduction

Auditor should audit financial statement so it can gain proper information, so this help

the financial user to know various activity in the business. Company has to get its financial

statement audit so this will help them to ensure that the company is able to follow all the rules

in the preparation of financial statement (Coppage & Shastri 2014). Auditor has to ensure that

it able to follow the norms while preparing the financial statement so it have to carry many

different procedure which will help the auditor to know about the company financial

statement and on that basic auditor will able to give its opinion upon the company financial

statement. It have to check the internal control of the company, which help the auditor to

know how the company is able to manage the business risk and able to carry its business

operation easily in the market (DeFond & Zhang 2014). The report deal with a company

name Crown Resort which is an Australian Gaming company and business operation in

Australia. The company is the largest gaming company in the country and its was founded in

31st May 2007. The report is divided into three section as first section show about the

materiality in the business, the second section shows about the analytical procedure in the

company and last section show the analysis of company annual report.

Section 1

Materiality in Audit

This section deal with the materiality and scope of audit that is involve in company

financial report. Each company has to maintain many operation in order to carry its business

activities which lead to overall increase in company error and omission so this will directly

affect the company financial statement (Eilifsen & Messier Jr 2014). It show the materiality

which is involve in the company and how the auditor is able to address the same while

carrying its audit procedures in the company financial statement. Auditor has to give its

AUDITING

Introduction

Auditor should audit financial statement so it can gain proper information, so this help

the financial user to know various activity in the business. Company has to get its financial

statement audit so this will help them to ensure that the company is able to follow all the rules

in the preparation of financial statement (Coppage & Shastri 2014). Auditor has to ensure that

it able to follow the norms while preparing the financial statement so it have to carry many

different procedure which will help the auditor to know about the company financial

statement and on that basic auditor will able to give its opinion upon the company financial

statement. It have to check the internal control of the company, which help the auditor to

know how the company is able to manage the business risk and able to carry its business

operation easily in the market (DeFond & Zhang 2014). The report deal with a company

name Crown Resort which is an Australian Gaming company and business operation in

Australia. The company is the largest gaming company in the country and its was founded in

31st May 2007. The report is divided into three section as first section show about the

materiality in the business, the second section shows about the analytical procedure in the

company and last section show the analysis of company annual report.

Section 1

Materiality in Audit

This section deal with the materiality and scope of audit that is involve in company

financial report. Each company has to maintain many operation in order to carry its business

activities which lead to overall increase in company error and omission so this will directly

affect the company financial statement (Eilifsen & Messier Jr 2014). It show the materiality

which is involve in the company and how the auditor is able to address the same while

carrying its audit procedures in the company financial statement. Auditor has to give its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

opinion upon the company financial statement so to know the proper detail of company

financial statement it have to ascertain the amount of materiality which is involve in the

company business as this will help the auditor to know the amount of risk which the company

is having in their financial statement.

Auditor have to ascertain the amount of materiality in the business at the planning

stage so that it will able to know the procedure which has to be followed in the auditing of

company financial report. The assumption and estimation which the company is able to take

should be disclose properly to the auditor which will help it to know the amount of risk in the

business. It have to calculate the planning materiality which will help them to know about

the company more details and help them to give proper opinion in the company business

(Elder et al., 2013). The planning materiality is calculated while taking into consideration the

total sales, total asset and equity. Auditor usually take the amount which the largest one so

this give them a proper planning materiality so as per the calculation of planning materiality

is concern, the total asset is been taken as base and the calculation is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 8171700

¿ 5 %

¿ $ 408585

The above figure shows the planning materiality which is involve in the business so the

auditor have to carry the audit procedure properly while taking this into consideration so this

will help it to give proper opinion in company financial statement and able to give an

independent opinion on the company business activities.

AUDITING

opinion upon the company financial statement so to know the proper detail of company

financial statement it have to ascertain the amount of materiality which is involve in the

company business as this will help the auditor to know the amount of risk which the company

is having in their financial statement.

Auditor have to ascertain the amount of materiality in the business at the planning

stage so that it will able to know the procedure which has to be followed in the auditing of

company financial report. The assumption and estimation which the company is able to take

should be disclose properly to the auditor which will help it to know the amount of risk in the

business. It have to calculate the planning materiality which will help them to know about

the company more details and help them to give proper opinion in the company business

(Elder et al., 2013). The planning materiality is calculated while taking into consideration the

total sales, total asset and equity. Auditor usually take the amount which the largest one so

this give them a proper planning materiality so as per the calculation of planning materiality

is concern, the total asset is been taken as base and the calculation is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 8171700

¿ 5 %

¿ $ 408585

The above figure shows the planning materiality which is involve in the business so the

auditor have to carry the audit procedure properly while taking this into consideration so this

will help it to give proper opinion in company financial statement and able to give an

independent opinion on the company business activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

Review of Disclosures

Company is having so many business activities and to carry them it have to maintain

many accounting policy so this increase the lack of clarity in concern of financial report so it

is the management duty to show all the related information properly in the annual report

disclosure so that the company financial user is able to ascertain the company performance

easily and take their decision of investment in the company or not (Crownresorts.com.au.

2019). The company ensures that it is complying with the disclosure requirements of the

ASX Listing Rule in their financial report which will help them to provide all the information

properly and effectively in company business (Louwers et al.,2015). Auditor has to check

whether the company is able to provide all the required information properly in their financial

statement or not as this will help it to ascertain the amount of fraud which can be there in

company business. The details of the policy process for the adherence of market information

that could have reputation or issues with material regulatory or involve risk that gets

communicated to the respective Disclosure Officer or be sensitive to the market (Jacoby and

Levy, 2016). The Disclosure Committee and the Board does assessment of the information

whenever required and disclose the material information in the market. They also do a broad

publication of the information to the analysts, investors and media.

Section 2

Analytical Review of Company

Company is having so many items in annual report so this process help the auditor to

ascertain the risk that is associated in company financial statement, the process carry with the

analysis of company financial ratio which will show many aspects of company and able to

provide proper information to auditor so it can carry the process properly in the business.

AUDITING

Review of Disclosures

Company is having so many business activities and to carry them it have to maintain

many accounting policy so this increase the lack of clarity in concern of financial report so it

is the management duty to show all the related information properly in the annual report

disclosure so that the company financial user is able to ascertain the company performance

easily and take their decision of investment in the company or not (Crownresorts.com.au.

2019). The company ensures that it is complying with the disclosure requirements of the

ASX Listing Rule in their financial report which will help them to provide all the information

properly and effectively in company business (Louwers et al.,2015). Auditor has to check

whether the company is able to provide all the required information properly in their financial

statement or not as this will help it to ascertain the amount of fraud which can be there in

company business. The details of the policy process for the adherence of market information

that could have reputation or issues with material regulatory or involve risk that gets

communicated to the respective Disclosure Officer or be sensitive to the market (Jacoby and

Levy, 2016). The Disclosure Committee and the Board does assessment of the information

whenever required and disclose the material information in the market. They also do a broad

publication of the information to the analysts, investors and media.

Section 2

Analytical Review of Company

Company is having so many items in annual report so this process help the auditor to

ascertain the risk that is associated in company financial statement, the process carry with the

analysis of company financial ratio which will show many aspects of company and able to

provide proper information to auditor so it can carry the process properly in the business.

5

AUDITING

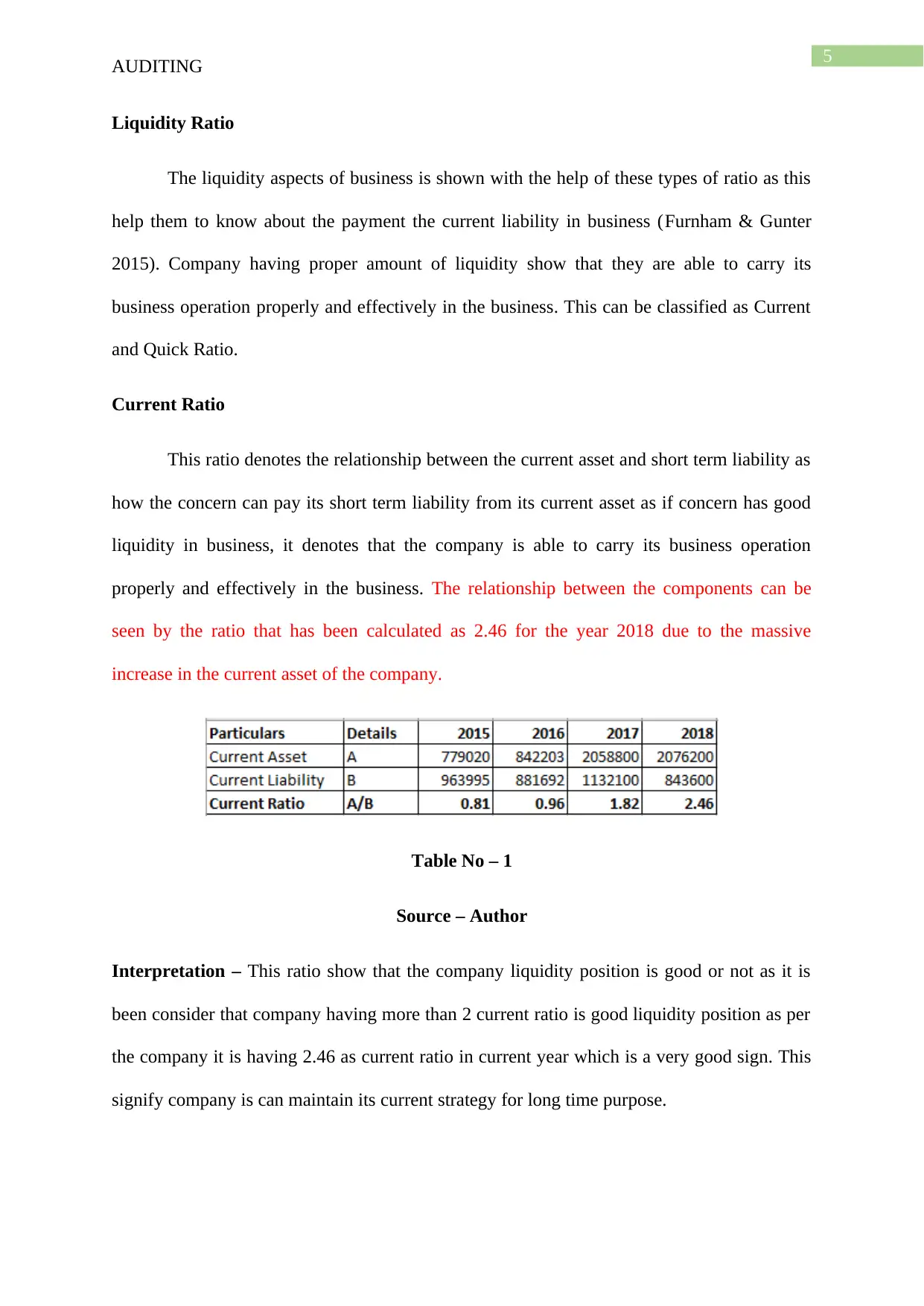

Liquidity Ratio

The liquidity aspects of business is shown with the help of these types of ratio as this

help them to know about the payment the current liability in business (Furnham & Gunter

2015). Company having proper amount of liquidity show that they are able to carry its

business operation properly and effectively in the business. This can be classified as Current

and Quick Ratio.

Current Ratio

This ratio denotes the relationship between the current asset and short term liability as

how the concern can pay its short term liability from its current asset as if concern has good

liquidity in business, it denotes that the company is able to carry its business operation

properly and effectively in the business. The relationship between the components can be

seen by the ratio that has been calculated as 2.46 for the year 2018 due to the massive

increase in the current asset of the company.

Table No – 1

Source – Author

Interpretation – This ratio show that the company liquidity position is good or not as it is

been consider that company having more than 2 current ratio is good liquidity position as per

the company it is having 2.46 as current ratio in current year which is a very good sign. This

signify company is can maintain its current strategy for long time purpose.

AUDITING

Liquidity Ratio

The liquidity aspects of business is shown with the help of these types of ratio as this

help them to know about the payment the current liability in business (Furnham & Gunter

2015). Company having proper amount of liquidity show that they are able to carry its

business operation properly and effectively in the business. This can be classified as Current

and Quick Ratio.

Current Ratio

This ratio denotes the relationship between the current asset and short term liability as

how the concern can pay its short term liability from its current asset as if concern has good

liquidity in business, it denotes that the company is able to carry its business operation

properly and effectively in the business. The relationship between the components can be

seen by the ratio that has been calculated as 2.46 for the year 2018 due to the massive

increase in the current asset of the company.

Table No – 1

Source – Author

Interpretation – This ratio show that the company liquidity position is good or not as it is

been consider that company having more than 2 current ratio is good liquidity position as per

the company it is having 2.46 as current ratio in current year which is a very good sign. This

signify company is can maintain its current strategy for long time purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

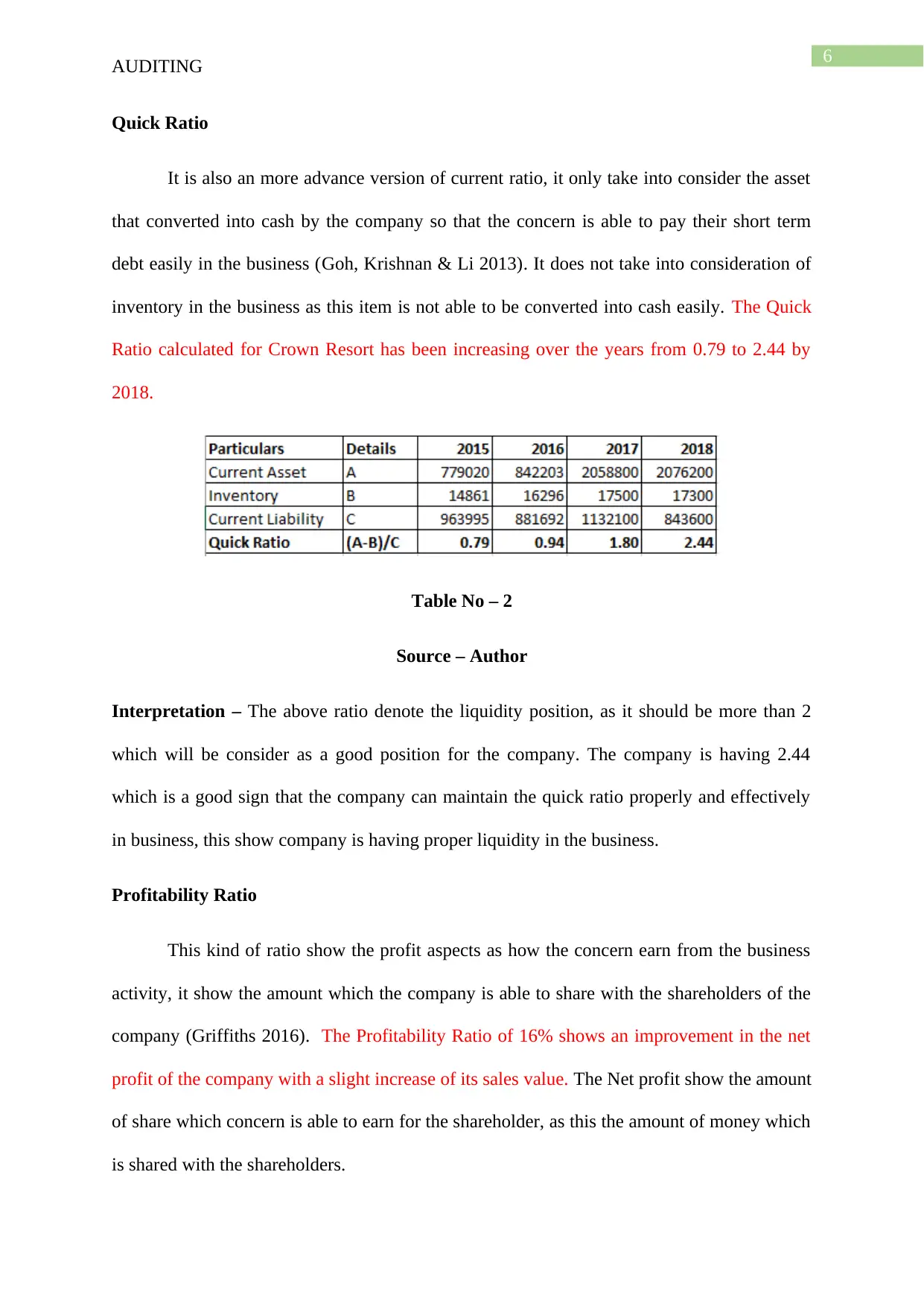

Quick Ratio

It is also an more advance version of current ratio, it only take into consider the asset

that converted into cash by the company so that the concern is able to pay their short term

debt easily in the business (Goh, Krishnan & Li 2013). It does not take into consideration of

inventory in the business as this item is not able to be converted into cash easily. The Quick

Ratio calculated for Crown Resort has been increasing over the years from 0.79 to 2.44 by

2018.

Table No – 2

Source – Author

Interpretation – The above ratio denote the liquidity position, as it should be more than 2

which will be consider as a good position for the company. The company is having 2.44

which is a good sign that the company can maintain the quick ratio properly and effectively

in business, this show company is having proper liquidity in the business.

Profitability Ratio

This kind of ratio show the profit aspects as how the concern earn from the business

activity, it show the amount which the company is able to share with the shareholders of the

company (Griffiths 2016). The Profitability Ratio of 16% shows an improvement in the net

profit of the company with a slight increase of its sales value. The Net profit show the amount

of share which concern is able to earn for the shareholder, as this the amount of money which

is shared with the shareholders.

AUDITING

Quick Ratio

It is also an more advance version of current ratio, it only take into consider the asset

that converted into cash by the company so that the concern is able to pay their short term

debt easily in the business (Goh, Krishnan & Li 2013). It does not take into consideration of

inventory in the business as this item is not able to be converted into cash easily. The Quick

Ratio calculated for Crown Resort has been increasing over the years from 0.79 to 2.44 by

2018.

Table No – 2

Source – Author

Interpretation – The above ratio denote the liquidity position, as it should be more than 2

which will be consider as a good position for the company. The company is having 2.44

which is a good sign that the company can maintain the quick ratio properly and effectively

in business, this show company is having proper liquidity in the business.

Profitability Ratio

This kind of ratio show the profit aspects as how the concern earn from the business

activity, it show the amount which the company is able to share with the shareholders of the

company (Griffiths 2016). The Profitability Ratio of 16% shows an improvement in the net

profit of the company with a slight increase of its sales value. The Net profit show the amount

of share which concern is able to earn for the shareholder, as this the amount of money which

is shared with the shareholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

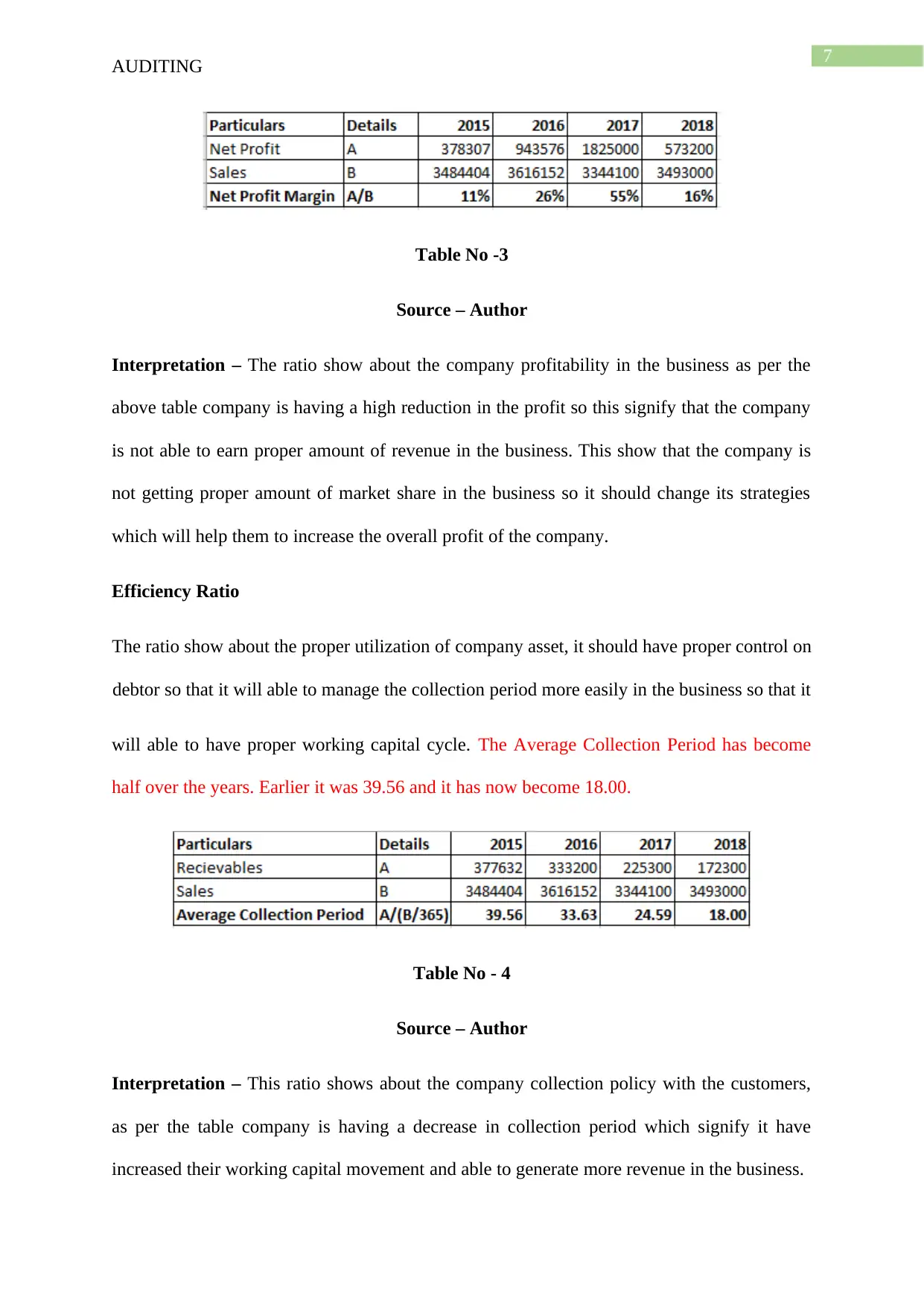

Table No -3

Source – Author

Interpretation – The ratio show about the company profitability in the business as per the

above table company is having a high reduction in the profit so this signify that the company

is not able to earn proper amount of revenue in the business. This show that the company is

not getting proper amount of market share in the business so it should change its strategies

which will help them to increase the overall profit of the company.

Efficiency Ratio

The ratio show about the proper utilization of company asset, it should have proper control on

debtor so that it will able to manage the collection period more easily in the business so that it

will able to have proper working capital cycle. The Average Collection Period has become

half over the years. Earlier it was 39.56 and it has now become 18.00.

Table No - 4

Source – Author

Interpretation – This ratio shows about the company collection policy with the customers,

as per the table company is having a decrease in collection period which signify it have

increased their working capital movement and able to generate more revenue in the business.

AUDITING

Table No -3

Source – Author

Interpretation – The ratio show about the company profitability in the business as per the

above table company is having a high reduction in the profit so this signify that the company

is not able to earn proper amount of revenue in the business. This show that the company is

not getting proper amount of market share in the business so it should change its strategies

which will help them to increase the overall profit of the company.

Efficiency Ratio

The ratio show about the proper utilization of company asset, it should have proper control on

debtor so that it will able to manage the collection period more easily in the business so that it

will able to have proper working capital cycle. The Average Collection Period has become

half over the years. Earlier it was 39.56 and it has now become 18.00.

Table No - 4

Source – Author

Interpretation – This ratio shows about the company collection policy with the customers,

as per the table company is having a decrease in collection period which signify it have

increased their working capital movement and able to generate more revenue in the business.

8

AUDITING

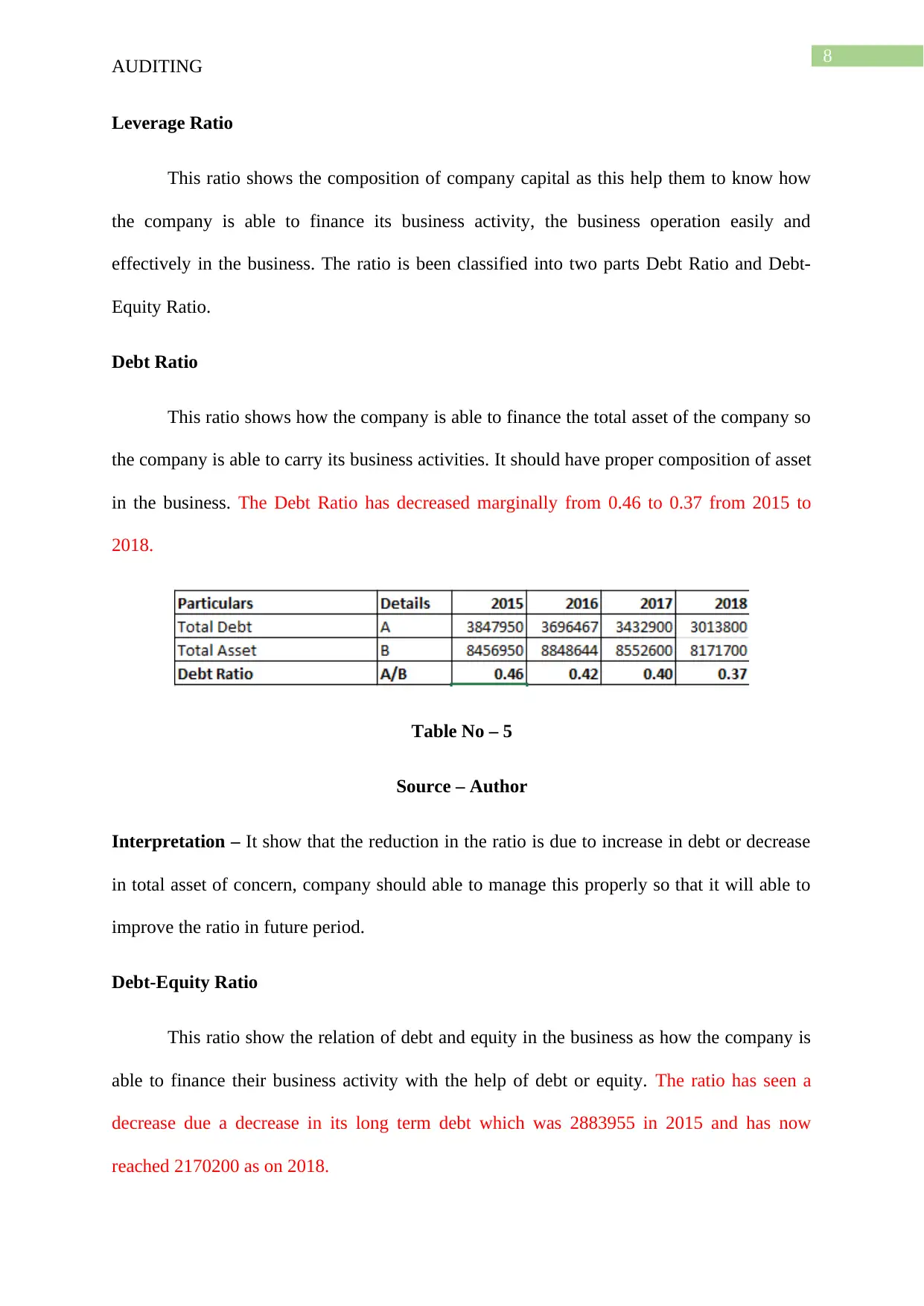

Leverage Ratio

This ratio shows the composition of company capital as this help them to know how

the company is able to finance its business activity, the business operation easily and

effectively in the business. The ratio is been classified into two parts Debt Ratio and Debt-

Equity Ratio.

Debt Ratio

This ratio shows how the company is able to finance the total asset of the company so

the company is able to carry its business activities. It should have proper composition of asset

in the business. The Debt Ratio has decreased marginally from 0.46 to 0.37 from 2015 to

2018.

Table No – 5

Source – Author

Interpretation – It show that the reduction in the ratio is due to increase in debt or decrease

in total asset of concern, company should able to manage this properly so that it will able to

improve the ratio in future period.

Debt-Equity Ratio

This ratio show the relation of debt and equity in the business as how the company is

able to finance their business activity with the help of debt or equity. The ratio has seen a

decrease due a decrease in its long term debt which was 2883955 in 2015 and has now

reached 2170200 as on 2018.

AUDITING

Leverage Ratio

This ratio shows the composition of company capital as this help them to know how

the company is able to finance its business activity, the business operation easily and

effectively in the business. The ratio is been classified into two parts Debt Ratio and Debt-

Equity Ratio.

Debt Ratio

This ratio shows how the company is able to finance the total asset of the company so

the company is able to carry its business activities. It should have proper composition of asset

in the business. The Debt Ratio has decreased marginally from 0.46 to 0.37 from 2015 to

2018.

Table No – 5

Source – Author

Interpretation – It show that the reduction in the ratio is due to increase in debt or decrease

in total asset of concern, company should able to manage this properly so that it will able to

improve the ratio in future period.

Debt-Equity Ratio

This ratio show the relation of debt and equity in the business as how the company is

able to finance their business activity with the help of debt or equity. The ratio has seen a

decrease due a decrease in its long term debt which was 2883955 in 2015 and has now

reached 2170200 as on 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

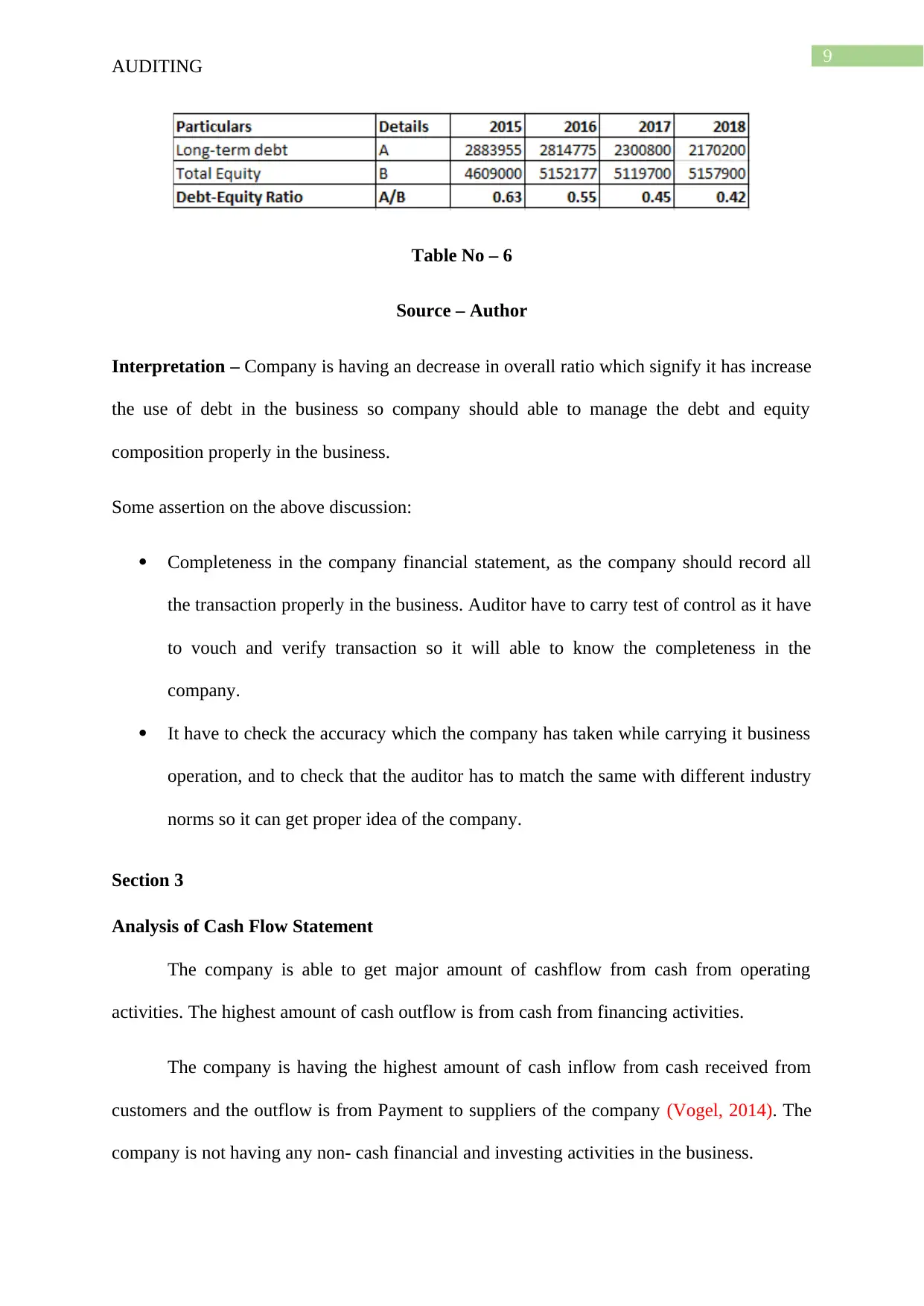

AUDITING

Table No – 6

Source – Author

Interpretation – Company is having an decrease in overall ratio which signify it has increase

the use of debt in the business so company should able to manage the debt and equity

composition properly in the business.

Some assertion on the above discussion:

Completeness in the company financial statement, as the company should record all

the transaction properly in the business. Auditor have to carry test of control as it have

to vouch and verify transaction so it will able to know the completeness in the

company.

It have to check the accuracy which the company has taken while carrying it business

operation, and to check that the auditor has to match the same with different industry

norms so it can get proper idea of the company.

Section 3

Analysis of Cash Flow Statement

The company is able to get major amount of cashflow from cash from operating

activities. The highest amount of cash outflow is from cash from financing activities.

The company is having the highest amount of cash inflow from cash received from

customers and the outflow is from Payment to suppliers of the company (Vogel, 2014). The

company is not having any non- cash financial and investing activities in the business.

AUDITING

Table No – 6

Source – Author

Interpretation – Company is having an decrease in overall ratio which signify it has increase

the use of debt in the business so company should able to manage the debt and equity

composition properly in the business.

Some assertion on the above discussion:

Completeness in the company financial statement, as the company should record all

the transaction properly in the business. Auditor have to carry test of control as it have

to vouch and verify transaction so it will able to know the completeness in the

company.

It have to check the accuracy which the company has taken while carrying it business

operation, and to check that the auditor has to match the same with different industry

norms so it can get proper idea of the company.

Section 3

Analysis of Cash Flow Statement

The company is able to get major amount of cashflow from cash from operating

activities. The highest amount of cash outflow is from cash from financing activities.

The company is having the highest amount of cash inflow from cash received from

customers and the outflow is from Payment to suppliers of the company (Vogel, 2014). The

company is not having any non- cash financial and investing activities in the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

The concern is having positive cash so this signify it able to carry its business

operation properly and effectively in the business so this show company is not having any

problem in the going concern concept as a result the auditor should carry all the audit process

to ascertain the true and fair view in the business (Williams & Dobelman, 2017).

Going Concern

This is the principle which state that the company is able to run for long term so the

investors can able to invest properly in the company as they will able to gain the return on

investment easily in the business, the company is not having any kind of risk which can affect

the principle of going concern in the business (Sundgren & Svanström, 2014).

Some points which can affect the principle of going concern is:

Company is not able to pay the finance cost in the business

It is having decrease in overall profit of the company

There is increase in the sale of company fixed asset

Company is increasing the debt funding in the business

Analysis of Auditor Report

Auditor of the company is Ernst and Young, as per the auditor the company can

maintain all the rules and regulation as per the Corporation Act 2001, the auditor has gave the

company an Unqualified Report which signify concern is not having any misstatement in the

business (Crownresorts.com.au. 2019). The auditor is has given the company unqualified

report as the company is able to maintain all the norms in the preparation of its financial

report and the company is having no materiality in their financial statement.

AUDITING

The concern is having positive cash so this signify it able to carry its business

operation properly and effectively in the business so this show company is not having any

problem in the going concern concept as a result the auditor should carry all the audit process

to ascertain the true and fair view in the business (Williams & Dobelman, 2017).

Going Concern

This is the principle which state that the company is able to run for long term so the

investors can able to invest properly in the company as they will able to gain the return on

investment easily in the business, the company is not having any kind of risk which can affect

the principle of going concern in the business (Sundgren & Svanström, 2014).

Some points which can affect the principle of going concern is:

Company is not able to pay the finance cost in the business

It is having decrease in overall profit of the company

There is increase in the sale of company fixed asset

Company is increasing the debt funding in the business

Analysis of Auditor Report

Auditor of the company is Ernst and Young, as per the auditor the company can

maintain all the rules and regulation as per the Corporation Act 2001, the auditor has gave the

company an Unqualified Report which signify concern is not having any misstatement in the

business (Crownresorts.com.au. 2019). The auditor is has given the company unqualified

report as the company is able to maintain all the norms in the preparation of its financial

report and the company is having no materiality in their financial statement.

11

AUDITING

Key Audit Matter

These are the matter which are shown by the auditor so that the financial user can

know about the risk associated in company business. The key audit matter shown by auditor

is:

The auditor found that the company is not having proper recoverable policy for trade

receivables as it able to get extend the credit term of the company. To check this

auditor had tested the valuation of trade receivables with the customer transaction.

The judgement which the company is able to make in regards of provision of

doubtful debt in the business. Auditor had to evaluate each debtor information so it

can know whether the company is able to take proper amount of judgement in the

business or not.

The impairment of company involves much amount of complexity as it involves the

modelling of different range and judgement which can also affect the future event of

the company. Auditor had to involve the valuation specialists so that it can give

proper valuation with the help of application of different methodology in company

business.

Conclusion

The report conclude about auditing process in business as it conclude about how the

auditor can carry its operation in the company financial activities. It conclude about the

company Crown Resorts Ltd and show the materiality aspects and the financial analysis of

company. Lastly the report conclude about the analysis of cash flow statement and auditor

report of company.

AUDITING

Key Audit Matter

These are the matter which are shown by the auditor so that the financial user can

know about the risk associated in company business. The key audit matter shown by auditor

is:

The auditor found that the company is not having proper recoverable policy for trade

receivables as it able to get extend the credit term of the company. To check this

auditor had tested the valuation of trade receivables with the customer transaction.

The judgement which the company is able to make in regards of provision of

doubtful debt in the business. Auditor had to evaluate each debtor information so it

can know whether the company is able to take proper amount of judgement in the

business or not.

The impairment of company involves much amount of complexity as it involves the

modelling of different range and judgement which can also affect the future event of

the company. Auditor had to involve the valuation specialists so that it can give

proper valuation with the help of application of different methodology in company

business.

Conclusion

The report conclude about auditing process in business as it conclude about how the

auditor can carry its operation in the company financial activities. It conclude about the

company Crown Resorts Ltd and show the materiality aspects and the financial analysis of

company. Lastly the report conclude about the analysis of cash flow statement and auditor

report of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.