Analysis of Analytical Procedures and Risk in DIPL Auditing Case

VerifiedAdded on 2020/03/04

|9

|2763

|51

Homework Assignment

AI Summary

This assignment analyzes the DIPL auditing case, focusing on analytical procedures, risk assessment, and fraud risk factors. The analysis begins with a review of key financial ratios such as the current ratio, return on equity, and debt-to-equity ratio, highlighting potential inconsistencies and areas of concern in the financial statements. It then delves into inherent risks, particularly those related to inventory control and the impact of a new CEO and internal audit firm. Finally, the assignment identifies fraud risk factors associated with the adoption of a new IT system and plant and equipment asset valuation. The analysis emphasizes the need for detailed examination and further audit procedures to address the identified risks and ensure the accuracy of the financial statements. The analysis highlights potential manipulation of financial figures and the importance of thorough investigation to identify and mitigate financial risks.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

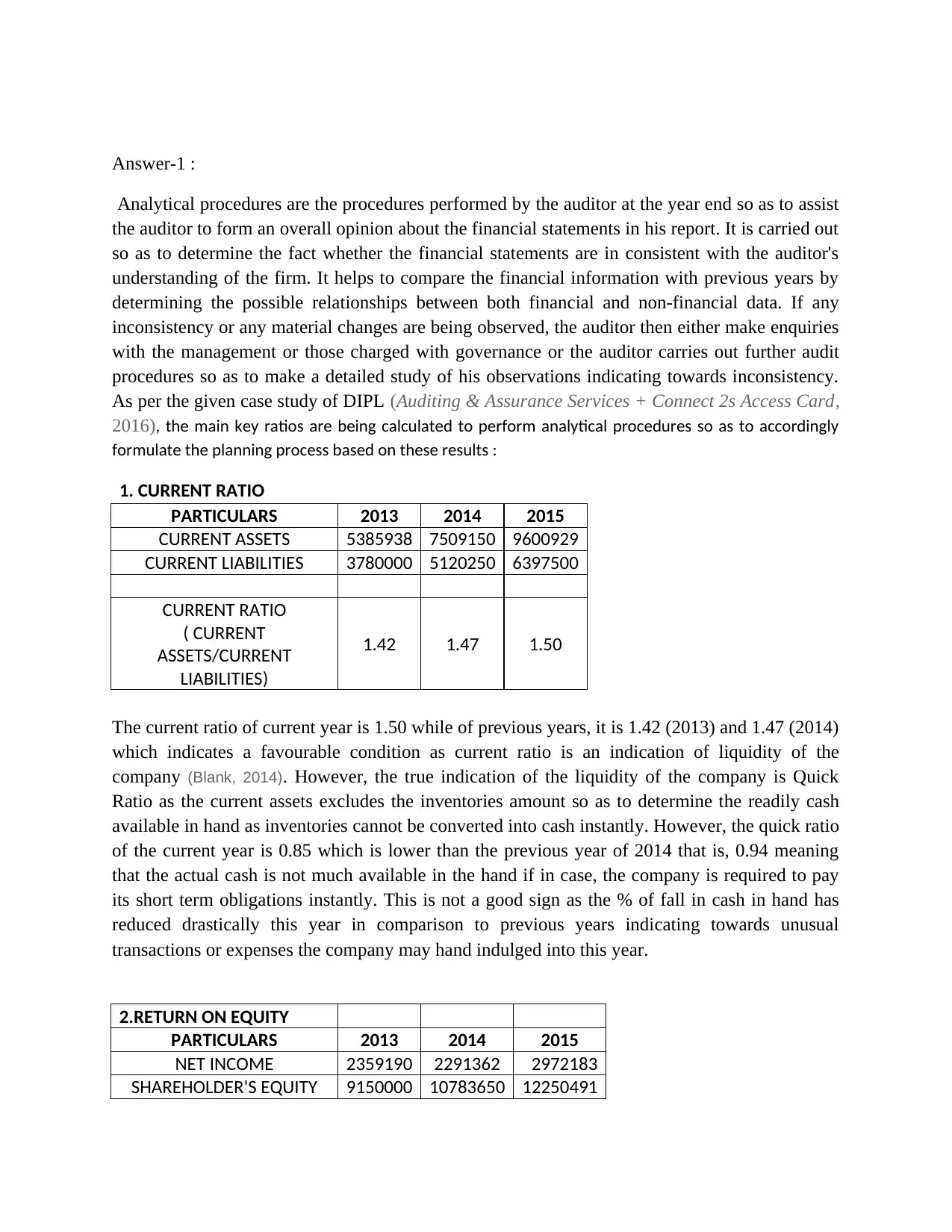

Answer-1 :

Analytical procedures are the procedures performed by the auditor at the year end so as to assist

the auditor to form an overall opinion about the financial statements in his report. It is carried out

so as to determine the fact whether the financial statements are in consistent with the auditor's

understanding of the firm. It helps to compare the financial information with previous years by

determining the possible relationships between both financial and non-financial data. If any

inconsistency or any material changes are being observed, the auditor then either make enquiries

with the management or those charged with governance or the auditor carries out further audit

procedures so as to make a detailed study of his observations indicating towards inconsistency.

As per the given case study of DIPL (Auditing & Assurance Services + Connect 2s Access Card,

2016), the main key ratios are being calculated to perform analytical procedures so as to accordingly

formulate the planning process based on these results :

1. CURRENT RATIO

PARTICULARS 2013 2014 2015

CURRENT ASSETS 5385938 7509150 9600929

CURRENT LIABILITIES 3780000 5120250 6397500

CURRENT RATIO

( CURRENT

ASSETS/CURRENT

LIABILITIES)

1.42 1.47 1.50

The current ratio of current year is 1.50 while of previous years, it is 1.42 (2013) and 1.47 (2014)

which indicates a favourable condition as current ratio is an indication of liquidity of the

company (Blank, 2014). However, the true indication of the liquidity of the company is Quick

Ratio as the current assets excludes the inventories amount so as to determine the readily cash

available in hand as inventories cannot be converted into cash instantly. However, the quick ratio

of the current year is 0.85 which is lower than the previous year of 2014 that is, 0.94 meaning

that the actual cash is not much available in the hand if in case, the company is required to pay

its short term obligations instantly. This is not a good sign as the % of fall in cash in hand has

reduced drastically this year in comparison to previous years indicating towards unusual

transactions or expenses the company may hand indulged into this year.

2.RETURN ON EQUITY

PARTICULARS 2013 2014 2015

NET INCOME 2359190 2291362 2972183

SHAREHOLDER'S EQUITY 9150000 10783650 12250491

Analytical procedures are the procedures performed by the auditor at the year end so as to assist

the auditor to form an overall opinion about the financial statements in his report. It is carried out

so as to determine the fact whether the financial statements are in consistent with the auditor's

understanding of the firm. It helps to compare the financial information with previous years by

determining the possible relationships between both financial and non-financial data. If any

inconsistency or any material changes are being observed, the auditor then either make enquiries

with the management or those charged with governance or the auditor carries out further audit

procedures so as to make a detailed study of his observations indicating towards inconsistency.

As per the given case study of DIPL (Auditing & Assurance Services + Connect 2s Access Card,

2016), the main key ratios are being calculated to perform analytical procedures so as to accordingly

formulate the planning process based on these results :

1. CURRENT RATIO

PARTICULARS 2013 2014 2015

CURRENT ASSETS 5385938 7509150 9600929

CURRENT LIABILITIES 3780000 5120250 6397500

CURRENT RATIO

( CURRENT

ASSETS/CURRENT

LIABILITIES)

1.42 1.47 1.50

The current ratio of current year is 1.50 while of previous years, it is 1.42 (2013) and 1.47 (2014)

which indicates a favourable condition as current ratio is an indication of liquidity of the

company (Blank, 2014). However, the true indication of the liquidity of the company is Quick

Ratio as the current assets excludes the inventories amount so as to determine the readily cash

available in hand as inventories cannot be converted into cash instantly. However, the quick ratio

of the current year is 0.85 which is lower than the previous year of 2014 that is, 0.94 meaning

that the actual cash is not much available in the hand if in case, the company is required to pay

its short term obligations instantly. This is not a good sign as the % of fall in cash in hand has

reduced drastically this year in comparison to previous years indicating towards unusual

transactions or expenses the company may hand indulged into this year.

2.RETURN ON EQUITY

PARTICULARS 2013 2014 2015

NET INCOME 2359190 2291362 2972183

SHAREHOLDER'S EQUITY 9150000 10783650 12250491

RETURN ON EQUITY (NET

INCOME/TOTAL

EQUITY)*100

25.78% 21.25% 24.26%

Coming to Return On Equity % and EPS calculation, the profit before tax in 2015 is Rs. 3059299

but the income tax shows an amount of Rs. 87116, which is just not possible, without any

manipulations. It may be so as to show high net earnings as the EPS for 2013 is Rs. 104.85,for

2014 is Rs. 101.84 but the current year's EPS is Rs. 132 approximately. Such calculation of PAT

(Profit After Tax) needs a justification as the calculation of income tax is too low according to

the operations which may be to show high EPS so as to win the confidence of the investors in the

company. Also, such calculation of net earnings may also be done so as to lift up its return on

equity % from previous years as it reveals the % of return the investors are receiving on their

investment (Boynton & Johnson, 2006).

3. DEBT TO EQUITY RATIO

PARTICULARS 2013 2014 2015

INTEREST-BEARING DEBTS 0 0 7500000

SHAREHOLDER'S EQUITY 9150000 10783650 12250491

DEBT TO EQUITY RATIO

(TOTAL

DEBT/SHAREHOLDER'S

EQUITY)

0.00 0.00 0.61

The debt equity ratio is calculated only for this year, that is, 0.61. The company has an obligation

that it is to maintain a current ratio of at least 1.5 and debt equity should be below 1 otherwise

the loan giver would recall the loan amount. Being under pressure, it can be the case that to show

a high shareholder's equity balance, the company manipulated the books that the income tax

liability came to Rs. 87116 on a profit of Rs. 3059299. Also in comparison to previous year

retained earning balances, there in an unusual increase in the value of the retained earnings

inspite of facing heavy expenditure in this current year such as new It System, takeover of a new

company named as Nuclear Publishing Ltd., purchase of fixed assets in large amount etc. Thus,

such a case requires detailed examination of books (Boynton & Johnson, 2006).

4. INTEREST COVERAGE

RATIO

PARTICULARS 2013 2014 2015

NET EARNINGS 2359190 2291362 2972183

INCOME TAX EXPENSE 1011081 982012 87116

INTEREST EXPENSE 84379 83663 808038

INCOME/TOTAL

EQUITY)*100

25.78% 21.25% 24.26%

Coming to Return On Equity % and EPS calculation, the profit before tax in 2015 is Rs. 3059299

but the income tax shows an amount of Rs. 87116, which is just not possible, without any

manipulations. It may be so as to show high net earnings as the EPS for 2013 is Rs. 104.85,for

2014 is Rs. 101.84 but the current year's EPS is Rs. 132 approximately. Such calculation of PAT

(Profit After Tax) needs a justification as the calculation of income tax is too low according to

the operations which may be to show high EPS so as to win the confidence of the investors in the

company. Also, such calculation of net earnings may also be done so as to lift up its return on

equity % from previous years as it reveals the % of return the investors are receiving on their

investment (Boynton & Johnson, 2006).

3. DEBT TO EQUITY RATIO

PARTICULARS 2013 2014 2015

INTEREST-BEARING DEBTS 0 0 7500000

SHAREHOLDER'S EQUITY 9150000 10783650 12250491

DEBT TO EQUITY RATIO

(TOTAL

DEBT/SHAREHOLDER'S

EQUITY)

0.00 0.00 0.61

The debt equity ratio is calculated only for this year, that is, 0.61. The company has an obligation

that it is to maintain a current ratio of at least 1.5 and debt equity should be below 1 otherwise

the loan giver would recall the loan amount. Being under pressure, it can be the case that to show

a high shareholder's equity balance, the company manipulated the books that the income tax

liability came to Rs. 87116 on a profit of Rs. 3059299. Also in comparison to previous year

retained earning balances, there in an unusual increase in the value of the retained earnings

inspite of facing heavy expenditure in this current year such as new It System, takeover of a new

company named as Nuclear Publishing Ltd., purchase of fixed assets in large amount etc. Thus,

such a case requires detailed examination of books (Boynton & Johnson, 2006).

4. INTEREST COVERAGE

RATIO

PARTICULARS 2013 2014 2015

NET EARNINGS 2359190 2291362 2972183

INCOME TAX EXPENSE 1011081 982012 87116

INTEREST EXPENSE 84379 83663 808038

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

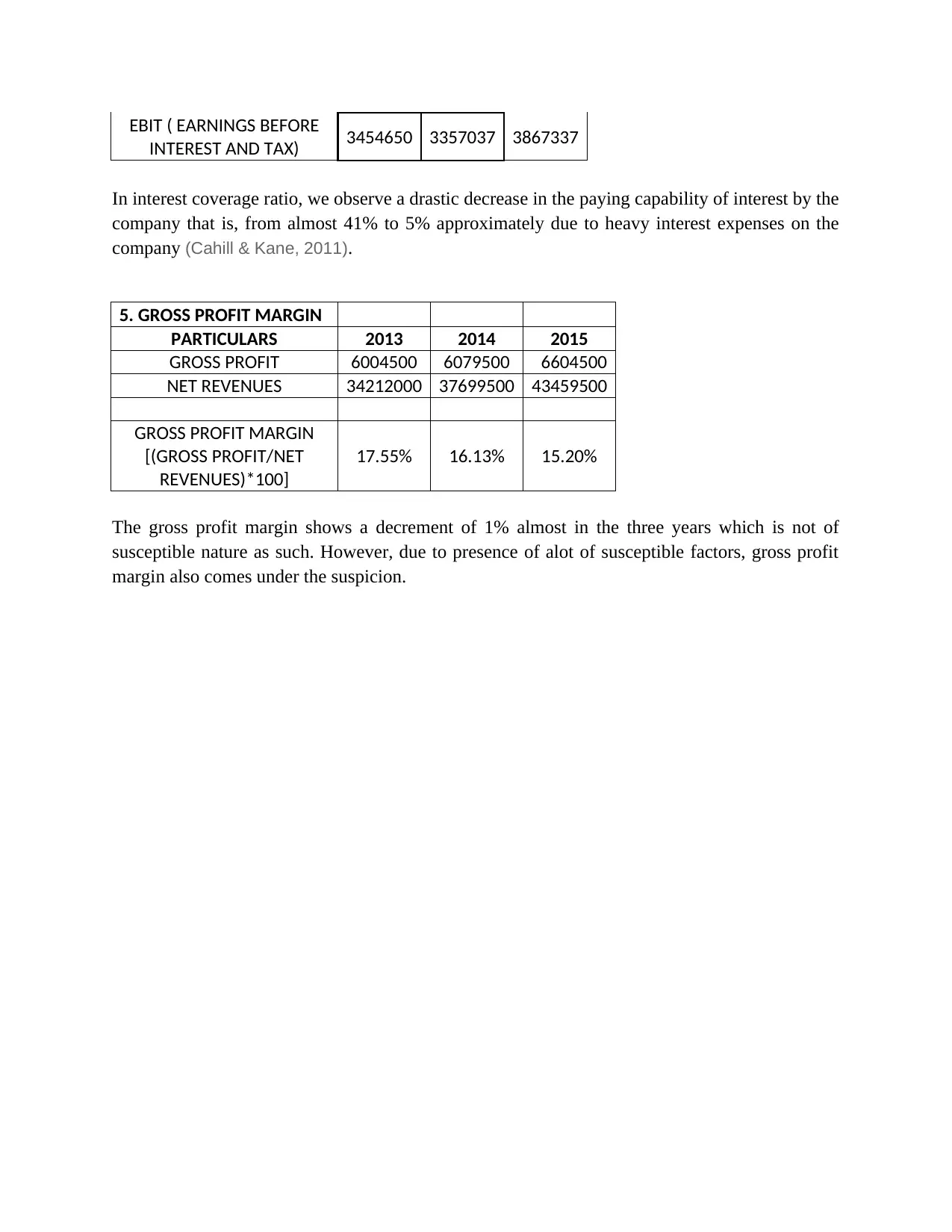

EBIT ( EARNINGS BEFORE

INTEREST AND TAX) 3454650 3357037 3867337

In interest coverage ratio, we observe a drastic decrease in the paying capability of interest by the

company that is, from almost 41% to 5% approximately due to heavy interest expenses on the

company (Cahill & Kane, 2011).

5. GROSS PROFIT MARGIN

PARTICULARS 2013 2014 2015

GROSS PROFIT 6004500 6079500 6604500

NET REVENUES 34212000 37699500 43459500

GROSS PROFIT MARGIN

[(GROSS PROFIT/NET

REVENUES)*100]

17.55% 16.13% 15.20%

The gross profit margin shows a decrement of 1% almost in the three years which is not of

susceptible nature as such. However, due to presence of alot of susceptible factors, gross profit

margin also comes under the suspicion.

INTEREST AND TAX) 3454650 3357037 3867337

In interest coverage ratio, we observe a drastic decrease in the paying capability of interest by the

company that is, from almost 41% to 5% approximately due to heavy interest expenses on the

company (Cahill & Kane, 2011).

5. GROSS PROFIT MARGIN

PARTICULARS 2013 2014 2015

GROSS PROFIT 6004500 6079500 6604500

NET REVENUES 34212000 37699500 43459500

GROSS PROFIT MARGIN

[(GROSS PROFIT/NET

REVENUES)*100]

17.55% 16.13% 15.20%

The gross profit margin shows a decrement of 1% almost in the three years which is not of

susceptible nature as such. However, due to presence of alot of susceptible factors, gross profit

margin also comes under the suspicion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer-2 :

While performing the audit, risk assessment procedures are being used so as to identify the risk

where the material misstatements exist or not. It is an important step as the whole aim of auditing

the financial statements is to find out whether the books are free of misstatements or not.

Inherent risk is one of the major types of audit risk that means the risk arising out of misleading

information or omission in financial statements due to certain reasons but not due to failure of

controls. Inherent risk occurs due to large number of similar transactions, heavy use of sampling,

human intuitions, and disclosure to the misstatements that can be material, or a number of small

misstatements contributing to a material misstatement together. The auditor assess this kind of

risk on the basis of his intuitions & judgments and his understanding of the entity's nature &

operations (Fountain, n.d.).

Considering the present case of Double Ink Printers Ltd. (DIPL), where the books are being

closed on 30th June, following are the two inherent risk factors that arises out of the company's

nature & operations:

Control over Inventory: The inventory of this company basically consists of paper, ink &

binding materials, which are to be specified as materials not of high value. The inventory

when received is kept at the warehouse and the entry is being made by the accounts

payable clerk on the arrival of it specifying the value & quantity in the books. The risk

observed in this case :

(a) The warehouse closes only at the yearend for the last two days which can be susceptible as

inventories are something that can be stolen. The employees can use the raw materials for their

own personal use (Hooks, 2011). A periodic stock counting should take place rather than

conducting it only at the year end as stock taking only at the yearend won't reveal the regularity

or irregularity of stock at the month end. Theft is a very common risk in this case as the items

missing can either be ignored or can be claimed as discrepancies and therefore, the employees

remains on the safe side.

(b) It is nowhere mentioned that when the inventory is being received, there is a physical check

of inventory. Only one in-charge is being appointed who passes the entry on the arrival.

However, it is a susceptible point because it may happen the person responsible may record the

entry of less inventory in his books rather than what is being actually received and the balance he

sells it personally to the outside parties and enjoys the entire earning without actually paying for

any cost of production (Knechel, Salterio & Ballou, 2017).

While performing the audit, risk assessment procedures are being used so as to identify the risk

where the material misstatements exist or not. It is an important step as the whole aim of auditing

the financial statements is to find out whether the books are free of misstatements or not.

Inherent risk is one of the major types of audit risk that means the risk arising out of misleading

information or omission in financial statements due to certain reasons but not due to failure of

controls. Inherent risk occurs due to large number of similar transactions, heavy use of sampling,

human intuitions, and disclosure to the misstatements that can be material, or a number of small

misstatements contributing to a material misstatement together. The auditor assess this kind of

risk on the basis of his intuitions & judgments and his understanding of the entity's nature &

operations (Fountain, n.d.).

Considering the present case of Double Ink Printers Ltd. (DIPL), where the books are being

closed on 30th June, following are the two inherent risk factors that arises out of the company's

nature & operations:

Control over Inventory: The inventory of this company basically consists of paper, ink &

binding materials, which are to be specified as materials not of high value. The inventory

when received is kept at the warehouse and the entry is being made by the accounts

payable clerk on the arrival of it specifying the value & quantity in the books. The risk

observed in this case :

(a) The warehouse closes only at the yearend for the last two days which can be susceptible as

inventories are something that can be stolen. The employees can use the raw materials for their

own personal use (Hooks, 2011). A periodic stock counting should take place rather than

conducting it only at the year end as stock taking only at the yearend won't reveal the regularity

or irregularity of stock at the month end. Theft is a very common risk in this case as the items

missing can either be ignored or can be claimed as discrepancies and therefore, the employees

remains on the safe side.

(b) It is nowhere mentioned that when the inventory is being received, there is a physical check

of inventory. Only one in-charge is being appointed who passes the entry on the arrival.

However, it is a susceptible point because it may happen the person responsible may record the

entry of less inventory in his books rather than what is being actually received and the balance he

sells it personally to the outside parties and enjoys the entire earning without actually paying for

any cost of production (Knechel, Salterio & Ballou, 2017).

Appointment of New CEO & a new internal audit firm in January, 2015 : The Company

appointed a new CEO in almost in the mid of the financial year without mentioning much

reasons and explanations. The previous CEO was semi-retired but wasn't on the verge of

being replaced. Enquiries are to be made so as to analyze the true reasons of such a step

either by having a word with previous CEO or the other members of the company. Also,

the board now formed an internal audit department that indicates that previously it had no

such internal audit procedures. This is susceptible in a way as it indicates a pressure over

the company or maybe some problems in the operations of the company or maybe the

level of misappropriations are increasing which the company is not being able to identify

but is only facing the consequences. All these can together create a pressure on the firm

that made it to form an entire separate audit department so as to rectify the areas prone to

errors or frauds (Louwers, Blay, Sinason, Strawser & Thibodeau, n.d.).

appointed a new CEO in almost in the mid of the financial year without mentioning much

reasons and explanations. The previous CEO was semi-retired but wasn't on the verge of

being replaced. Enquiries are to be made so as to analyze the true reasons of such a step

either by having a word with previous CEO or the other members of the company. Also,

the board now formed an internal audit department that indicates that previously it had no

such internal audit procedures. This is susceptible in a way as it indicates a pressure over

the company or maybe some problems in the operations of the company or maybe the

level of misappropriations are increasing which the company is not being able to identify

but is only facing the consequences. All these can together create a pressure on the firm

that made it to form an entire separate audit department so as to rectify the areas prone to

errors or frauds (Louwers, Blay, Sinason, Strawser & Thibodeau, n.d.).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer-3 :

Fraud is an act done intentionally by one or more individuals among the management itself be it

the employees or third parties or the top level management, so as to enjoy an illegal advantage.

Fraud risk factors are the factors that indicate a pressure or an incentive that can result in

committing fraud. Fraud risk factors can be generally classified into three conditions that usually

exists where a fraud occurs - Incentives, Opportunities and Attitudes/Rationalizations.

Based on the given case study, the two key fraud risk factor that DIPL is susceptible to are as

follow:

Adoption of New IT System : The board under extreme pressure invested in the new IT

system so as to automate the entire accounting processes. It created a heavy pressure on

the IT department to install the system in the June, 2015 itself when the company is

supposed to close its books. The IT manager claimed that sudden change of the entire

system of recording accounting transactions is messing up the entire scenario as neither

the staffs are presently being properly trained nor proper testing or handling of the

installations is being created (Messier, 2016).

Such an action is an opportunity to conduct fraud as it can clearly be stated at the end that during

the transfer of accounting information into computerized system, the transactions were missed or

lost due to the inefficiency or less knowledge about the system by the staff. Also, in this way, the

person intending to commit fraud can misappropriate the cash balance or can make the

management overlook the fraudulent transactions that has been conducted in the respective

financial year. For example, a director conducted some transactions with the third party on the

name of the company and sold the goods & enjoyed the earnings on his personal account. Taking

advantage of his position, he painted the scenario in such a way that the goods sold were actually

considered as goods lost in the eyes of the management. Now suddenly, a new internal audit

team in January, 2015 was formed which would clearly rectify such a fraudulent activity.

Therefore, under immense pressure, it may happen that the new IT system was formed in June,

2015 itself so as to get such fraudulent activities ignored and at the end, the accounting

department's inefficiency could be blamed (PAVAN KUMAR, 2014).

Plant and Equipment Asset Valuation : There is an increment of Rs. 5,25,000 in the value

of plant and equipment from 2013 to 2014 while the accounts shows a purchase of Rs.

76,50,000 of plant & equipment in 2015. However, the loan obtained from BDO Finance

Ltd. is Rs. 75,00,000. Also, the company made an unusual hasty decision of adopting a

Fraud is an act done intentionally by one or more individuals among the management itself be it

the employees or third parties or the top level management, so as to enjoy an illegal advantage.

Fraud risk factors are the factors that indicate a pressure or an incentive that can result in

committing fraud. Fraud risk factors can be generally classified into three conditions that usually

exists where a fraud occurs - Incentives, Opportunities and Attitudes/Rationalizations.

Based on the given case study, the two key fraud risk factor that DIPL is susceptible to are as

follow:

Adoption of New IT System : The board under extreme pressure invested in the new IT

system so as to automate the entire accounting processes. It created a heavy pressure on

the IT department to install the system in the June, 2015 itself when the company is

supposed to close its books. The IT manager claimed that sudden change of the entire

system of recording accounting transactions is messing up the entire scenario as neither

the staffs are presently being properly trained nor proper testing or handling of the

installations is being created (Messier, 2016).

Such an action is an opportunity to conduct fraud as it can clearly be stated at the end that during

the transfer of accounting information into computerized system, the transactions were missed or

lost due to the inefficiency or less knowledge about the system by the staff. Also, in this way, the

person intending to commit fraud can misappropriate the cash balance or can make the

management overlook the fraudulent transactions that has been conducted in the respective

financial year. For example, a director conducted some transactions with the third party on the

name of the company and sold the goods & enjoyed the earnings on his personal account. Taking

advantage of his position, he painted the scenario in such a way that the goods sold were actually

considered as goods lost in the eyes of the management. Now suddenly, a new internal audit

team in January, 2015 was formed which would clearly rectify such a fraudulent activity.

Therefore, under immense pressure, it may happen that the new IT system was formed in June,

2015 itself so as to get such fraudulent activities ignored and at the end, the accounting

department's inefficiency could be blamed (PAVAN KUMAR, 2014).

Plant and Equipment Asset Valuation : There is an increment of Rs. 5,25,000 in the value

of plant and equipment from 2013 to 2014 while the accounts shows a purchase of Rs.

76,50,000 of plant & equipment in 2015. However, the loan obtained from BDO Finance

Ltd. is Rs. 75,00,000. Also, the company made an unusual hasty decision of adopting a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

computerized accounting system in June, 2015 itself. Thus, the purpose of loan is not

being clearly understood. Also, it is susceptible that under what conditions, the company

directly took the decision of taking such a big amount as loan as well as on the other

hand, it is suddenly showing a high value of asset in its books (Pitt, 2014). Therefore, the

following points are to be considered :

I. It may happen that by showing a high value of assets in its books, the company wants to

show its financial position strong to the stakeholders so as to enjoy smooth public

funding in future.

II. In the board year meeting, the estimated life of the printing presses was changed to 30

years instead of 20 years which is commonly adopted in the industry for the depreciation

purpose. Changing the estimated life from 20 years to 30 years would definitely be

showing less depreciation but it may also happen that it is to compensate for the overall

heavy depreciation amount in comparison to previous two years.

III. Also, such a decision is being taken only on the basis of the CEO's experience which

actually goes against the policy being adopted in the printing industry (Whittington &

Pany, 2016).

It is susceptible in a way that such valuations can be for the purpose of wining the stakeholders

trust so as to enjoy the funding in the future and use such funding for fraudulent purposes. Thus,

such unusual transactions & such not much justified decisions are indicative of fraud risk factors.

being clearly understood. Also, it is susceptible that under what conditions, the company

directly took the decision of taking such a big amount as loan as well as on the other

hand, it is suddenly showing a high value of asset in its books (Pitt, 2014). Therefore, the

following points are to be considered :

I. It may happen that by showing a high value of assets in its books, the company wants to

show its financial position strong to the stakeholders so as to enjoy smooth public

funding in future.

II. In the board year meeting, the estimated life of the printing presses was changed to 30

years instead of 20 years which is commonly adopted in the industry for the depreciation

purpose. Changing the estimated life from 20 years to 30 years would definitely be

showing less depreciation but it may also happen that it is to compensate for the overall

heavy depreciation amount in comparison to previous two years.

III. Also, such a decision is being taken only on the basis of the CEO's experience which

actually goes against the policy being adopted in the printing industry (Whittington &

Pany, 2016).

It is susceptible in a way that such valuations can be for the purpose of wining the stakeholders

trust so as to enjoy the funding in the future and use such funding for fraudulent purposes. Thus,

such unusual transactions & such not much justified decisions are indicative of fraud risk factors.

References:

Auditing & Assurance Services + Connect 2s Access Card. (2016).

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:

Government Institutes.

Fountain, L. Leading the internal audit function.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

Knechel, W., Salterio, S., & Ballou, B. (2017). Auditing. New York: Routledge.

Louwers, T., Blay, A., Sinason, D., Strawser, J., & Thibodeau, J. Auditing & assurance services.

Messier, W. (2016). Auditing & assurance services. [Place of publication not identified]:

Mcgraw-Hill Education.

PAVAN KUMAR, K. (2014). CA-IPCC AUDITING AND ASSURANCE. [S.l.]: S CHAND &

CO LTD.

Pitt, S. (2014). Internal audit quality. Hoboken: Wiley.

Whittington, O., & Pany, K. (2016). Principles of auditing & other assurance services. New

York, N.Y.: McGraw-Hill Education.

Auditing & Assurance Services + Connect 2s Access Card. (2016).

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:

Government Institutes.

Fountain, L. Leading the internal audit function.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

Knechel, W., Salterio, S., & Ballou, B. (2017). Auditing. New York: Routledge.

Louwers, T., Blay, A., Sinason, D., Strawser, J., & Thibodeau, J. Auditing & assurance services.

Messier, W. (2016). Auditing & assurance services. [Place of publication not identified]:

Mcgraw-Hill Education.

PAVAN KUMAR, K. (2014). CA-IPCC AUDITING AND ASSURANCE. [S.l.]: S CHAND &

CO LTD.

Pitt, S. (2014). Internal audit quality. Hoboken: Wiley.

Whittington, O., & Pany, K. (2016). Principles of auditing & other assurance services. New

York, N.Y.: McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.