CQUniversity Auditing and Ethics Report: Assessment Task 2 Analysis

VerifiedAdded on 2022/10/04

|13

|2449

|13

Report

AI Summary

This report, prepared for CQUniversity's ACCT20075 Auditing and Ethics course, analyzes the audit process, focusing on materiality, analytical procedures, and the analysis of financial statements. The report begins by defining materiality and its importance in auditing, using Treasury Wine Estates Ltd as a case study to determine planning materiality. It examines the notes to accounts, specifically addressing intangible assets, property, plant, and equipment, and leases and commitments. The report then explores the application of analytical procedures, including key financial ratios such as liquidity, profitability, asset management, and leverage ratios, to assess business performance. A detailed review of the cash flow statement is conducted, highlighting cash inflows and outflows from operating, investing, and financing activities. Finally, the report analyzes the auditor's report, including the unqualified opinion and key audit matters, providing a comprehensive overview of the audit process and its ethical considerations.

Running head: AUDIT AND ETHICS

Auditing and Ethics

Name of the Student:

Name of the University:

Author’s Note

Auditing and Ethics

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Part 1................................................................................................................................................2

Materiality Principle in Audit......................................................................................................2

Draft Notes and Disclosures........................................................................................................4

Section 2......................................................................................................................................5

Analytical Procedures as a tool of Audit.....................................................................................5

Section 3..........................................................................................................................................9

Analysis of the Cash flow Statement...........................................................................................9

Analysis of Auditor’s Report.....................................................................................................10

Reference.......................................................................................................................................12

Table of Contents

Part 1................................................................................................................................................2

Materiality Principle in Audit......................................................................................................2

Draft Notes and Disclosures........................................................................................................4

Section 2......................................................................................................................................5

Analytical Procedures as a tool of Audit.....................................................................................5

Section 3..........................................................................................................................................9

Analysis of the Cash flow Statement...........................................................................................9

Analysis of Auditor’s Report.....................................................................................................10

Reference.......................................................................................................................................12

2AUDITING AND ETHICS

Part 1

Principle of Materiality in Audit

The auditing process is considered to be a dynamic process which involves estimation

whether the annual report formulated by the top management is showing accurate view of

financial position for the period. The process of audit panning contains numerous segments, one

of the major aspect which is considered is materiality of the item or in other words how

important or significant is the item in the financial statements. The determination of materiality

is considered to be an important aspect and the same requires sound judgement on the part of the

auditor of the business. The assessment would be focusing on Treasury Wine Estates ltd which is

one of the leading wine producers and distributers in the country of Australia (Tweglobal.com.

2019). The annual report which would be considered for the purpose of audit would be that of

the current year.

The materiality concept in simple words reflect the significance of the elements reflected

in the financial reports and whether the same can be have an impact on the financial statement of

the business if the item is misstated (Carraher and Van Auken 2013). In terms of audit, the items

which are more repetitive in the financial statements are considered to be material. In a similar

manner figures which are intricate in nature are also deemed to be material for the business.

Likewise, any element which is of significant amount in the annual report of the business

(Christensen, Glover and Wood 2013). It is to be noted that materiality is two kinds which show

qualitative and quantitative estimates of materiality for the company. The elements which are

covered under qualitative materiality includes items such as sales, costs of sales, net profit while

quantitative materiality involves computation of planning materiality for assessing the

materiality of numerous items which are covered in the financial statement of the business.

Part 1

Principle of Materiality in Audit

The auditing process is considered to be a dynamic process which involves estimation

whether the annual report formulated by the top management is showing accurate view of

financial position for the period. The process of audit panning contains numerous segments, one

of the major aspect which is considered is materiality of the item or in other words how

important or significant is the item in the financial statements. The determination of materiality

is considered to be an important aspect and the same requires sound judgement on the part of the

auditor of the business. The assessment would be focusing on Treasury Wine Estates ltd which is

one of the leading wine producers and distributers in the country of Australia (Tweglobal.com.

2019). The annual report which would be considered for the purpose of audit would be that of

the current year.

The materiality concept in simple words reflect the significance of the elements reflected

in the financial reports and whether the same can be have an impact on the financial statement of

the business if the item is misstated (Carraher and Van Auken 2013). In terms of audit, the items

which are more repetitive in the financial statements are considered to be material. In a similar

manner figures which are intricate in nature are also deemed to be material for the business.

Likewise, any element which is of significant amount in the annual report of the business

(Christensen, Glover and Wood 2013). It is to be noted that materiality is two kinds which show

qualitative and quantitative estimates of materiality for the company. The elements which are

covered under qualitative materiality includes items such as sales, costs of sales, net profit while

quantitative materiality involves computation of planning materiality for assessing the

materiality of numerous items which are covered in the financial statement of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

The computation of planning materiality is usually conducted at the planning stage of an

audit and it is a fact that panning materiality of the business is considered to be the base for

computing performance materiality of a business. The performance materiality is the standards

which the item should be reflecting to be material (Goh, Krishnan and Li 2013). The technique

which is used for computing planning materiality is by considering a value which is greater than

every other value in the financial statements and at the same time a percentage is considered. The

percentage which is taken would be set as per the auditor’s judgement. In order to estimate the

materiality for the business of Treasury wine ltd, the auditor considers total assets as the base as

the figure is the most significant in the balance sheet of the company (Eilifsen and Messier Jr

2014). The value of the total asset is shown in the balance sheet of the business and the same is

shown to be $ 5,445.7 million. The percentage is considered by the auditor on his own

judgement and also referring to the estimate which was taken by the past auditor. The percentage

which is considered for estimation is 2% and the materiality computation is shown in equation

below:

Planning Materiality=Percentage estimated ×Total Assets of the Company

¿ $ 5445.7 million ×2 %

¿ $ 108.914 million

Therefore, the planning materiality which should be considered by the auditor is shown

above and it is on the basis of the same, performance materiality for the business needs to be

computed.

The computation of planning materiality is usually conducted at the planning stage of an

audit and it is a fact that panning materiality of the business is considered to be the base for

computing performance materiality of a business. The performance materiality is the standards

which the item should be reflecting to be material (Goh, Krishnan and Li 2013). The technique

which is used for computing planning materiality is by considering a value which is greater than

every other value in the financial statements and at the same time a percentage is considered. The

percentage which is taken would be set as per the auditor’s judgement. In order to estimate the

materiality for the business of Treasury wine ltd, the auditor considers total assets as the base as

the figure is the most significant in the balance sheet of the company (Eilifsen and Messier Jr

2014). The value of the total asset is shown in the balance sheet of the business and the same is

shown to be $ 5,445.7 million. The percentage is considered by the auditor on his own

judgement and also referring to the estimate which was taken by the past auditor. The percentage

which is considered for estimation is 2% and the materiality computation is shown in equation

below:

Planning Materiality=Percentage estimated ×Total Assets of the Company

¿ $ 5445.7 million ×2 %

¿ $ 108.914 million

Therefore, the planning materiality which should be considered by the auditor is shown

above and it is on the basis of the same, performance materiality for the business needs to be

computed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

Notes to Accounts Explainations

The notes to accounts also forms part of the financial statement of the business and the

same also needs to be reviewed by the auditor so that the management of the company has

provided proper disclosures in the annual report regarding complex treatments for the company.

The notes to account contains key accounting standards, principles and treatments which are

used by the business and some of the important disclosures of the business are discussed below

in details:

Intangible Assets: The intangible assets are demonstrated in balance sheet of a company

and important treatment relating to the same needs to be disclosed in the notes to

accounts section. Some of the intangible assets which is owned by the business of

Treasury Wine Estate are goodwill and rights of vineyards. Important treatments are

associated with intangible assets such as impairment and amortization which can have an

impact on the financial statement as a whole. The role of the auditor in such a case would

be to investigate whether the statements are accurately presented for intangible assets and

if the same is compliant with the accounting standard.

Property, Plants and Equipment: The valuation of property, plant and equipment are

considered to be important treatment and the method which is used for valuing the assets

forms part of accounting policy of the business. In case of Treasury Wine Estate, the

main property of the business is the vineyards for which appropriate valuation needs to be

done and treatment for the same should also be demonstrated as notes to accounts in the

annual report (Todea, Joldos and Cioca 2013). The auditor needs to perform audit

procedures to check assertion of existence and completeness is met in a proper manner or

not while conducting audit procedure

Notes to Accounts Explainations

The notes to accounts also forms part of the financial statement of the business and the

same also needs to be reviewed by the auditor so that the management of the company has

provided proper disclosures in the annual report regarding complex treatments for the company.

The notes to account contains key accounting standards, principles and treatments which are

used by the business and some of the important disclosures of the business are discussed below

in details:

Intangible Assets: The intangible assets are demonstrated in balance sheet of a company

and important treatment relating to the same needs to be disclosed in the notes to

accounts section. Some of the intangible assets which is owned by the business of

Treasury Wine Estate are goodwill and rights of vineyards. Important treatments are

associated with intangible assets such as impairment and amortization which can have an

impact on the financial statement as a whole. The role of the auditor in such a case would

be to investigate whether the statements are accurately presented for intangible assets and

if the same is compliant with the accounting standard.

Property, Plants and Equipment: The valuation of property, plant and equipment are

considered to be important treatment and the method which is used for valuing the assets

forms part of accounting policy of the business. In case of Treasury Wine Estate, the

main property of the business is the vineyards for which appropriate valuation needs to be

done and treatment for the same should also be demonstrated as notes to accounts in the

annual report (Todea, Joldos and Cioca 2013). The auditor needs to perform audit

procedures to check assertion of existence and completeness is met in a proper manner or

not while conducting audit procedure

5AUDITING AND ETHICS

Leases and Commitments: The lease and commitment which is taken by the business

are shown in the disclosures part of the financial statements and the same reflect the

leases which are taken during the current year. The auditor must verify the balances for

the leases and ensure that the same are genuine and are showing correct estimation. The

auditor can also confirm from external parties such as the lessor regarding the lease

amount and terms.

Section 2

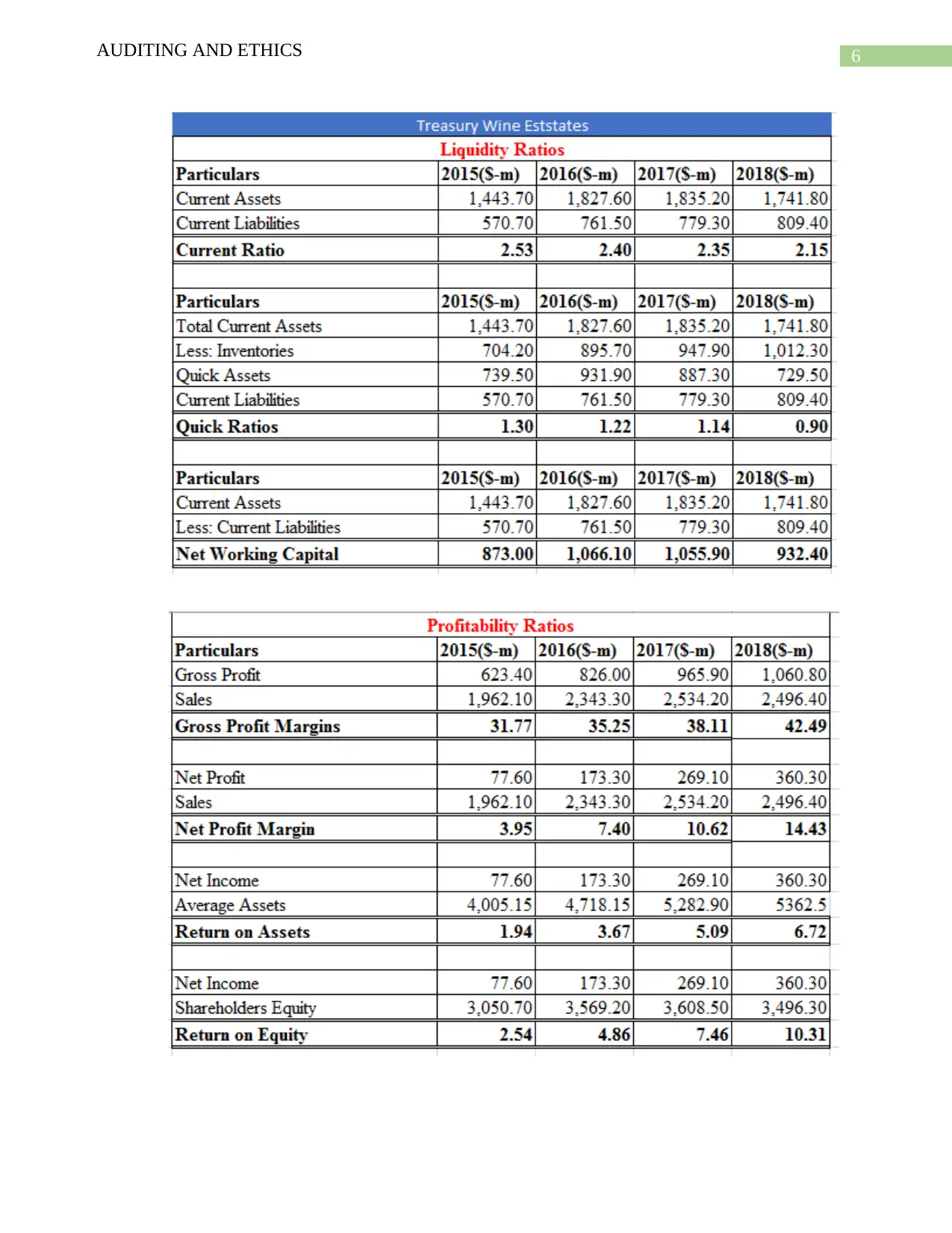

Analytical Procedures as a tool of Audit

The application of analytical procedure is often done for identifying the key areas of

performance of the business and also to ensure that accuracy is maintained in the items which are

represented in the annual reports of the business. The use of key financial ratios is included in

compliance procedures of audit and the same is applied by a business and the same can

effectively reveal the performance of the business in terms of profitability, liquidity, solvency in

the business. Some of the key financial ratios which are computed are shown below:

Leases and Commitments: The lease and commitment which is taken by the business

are shown in the disclosures part of the financial statements and the same reflect the

leases which are taken during the current year. The auditor must verify the balances for

the leases and ensure that the same are genuine and are showing correct estimation. The

auditor can also confirm from external parties such as the lessor regarding the lease

amount and terms.

Section 2

Analytical Procedures as a tool of Audit

The application of analytical procedure is often done for identifying the key areas of

performance of the business and also to ensure that accuracy is maintained in the items which are

represented in the annual reports of the business. The use of key financial ratios is included in

compliance procedures of audit and the same is applied by a business and the same can

effectively reveal the performance of the business in terms of profitability, liquidity, solvency in

the business. Some of the key financial ratios which are computed are shown below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

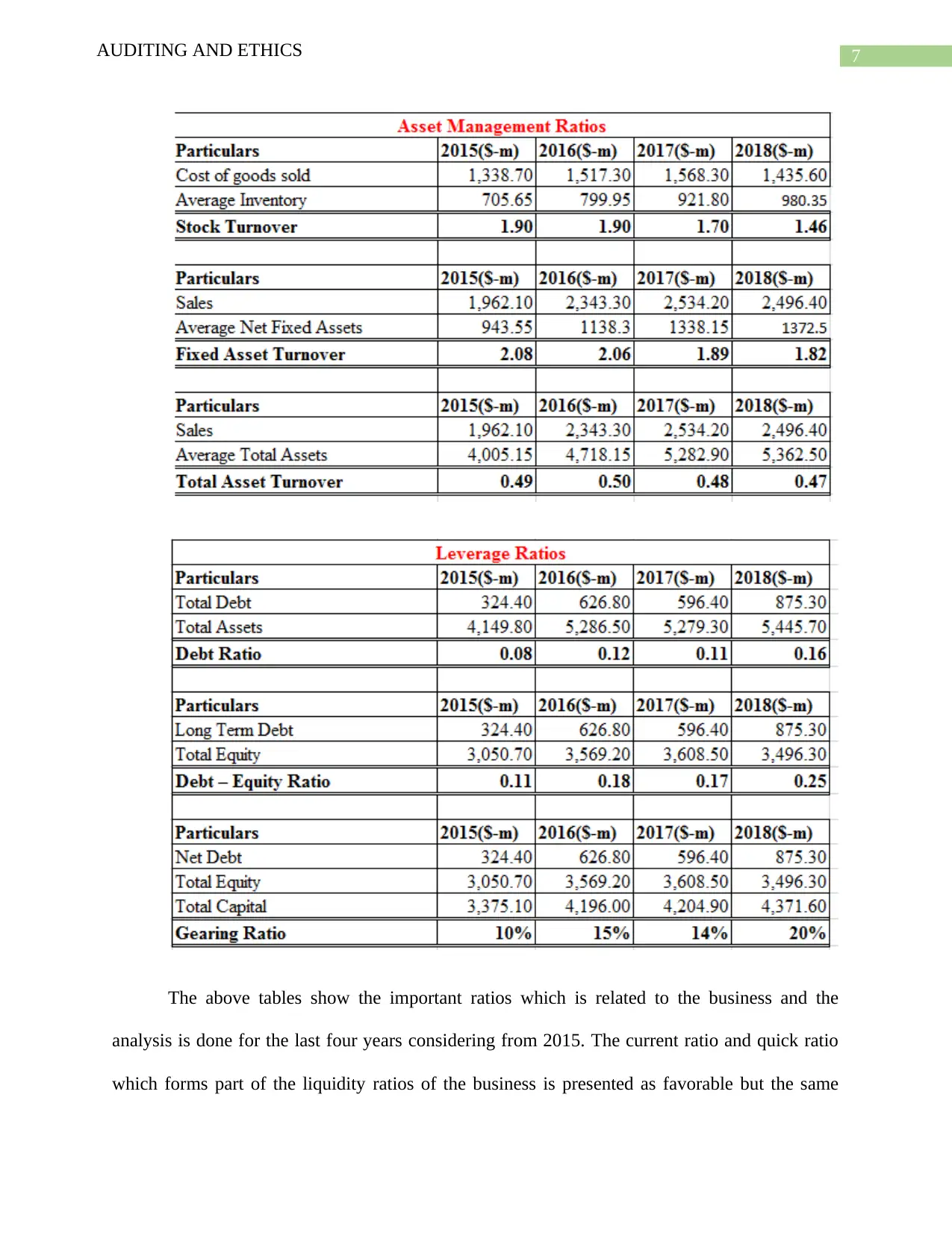

The above tables show the important ratios which is related to the business and the

analysis is done for the last four years considering from 2015. The current ratio and quick ratio

which forms part of the liquidity ratios of the business is presented as favorable but the same

The above tables show the important ratios which is related to the business and the

analysis is done for the last four years considering from 2015. The current ratio and quick ratio

which forms part of the liquidity ratios of the business is presented as favorable but the same

8AUDITING AND ETHICS

have declined from previous years which needs to be considered by the auditor as to the reason

for the decline. The net working capital which shows liquid position also shows a decline which

means that the liquidity position of the business has been slightly affected. The auditor needs to

check the current assets with special emphasis on debtors, cash and inventory balances of the

business.

The profitability ratios are considered to be important ratios and the same comprises of

net profit ratio and other margins related to profitability which is shown in the table above. There

has been significant increase in both net and gross profit margin which a favorable sign for the

business is (Delen, Kuzey and Uyar 2013). There has also been positive impact on the estimates

of returns from equity and assets. The auditor of the business needs to check the sales figure and

also check the cost of goods sold to ascertain all transactions are accurate. In such a case, the

auditor can apply vouching practices for getting a clear idea.

The asset management ratios reflect the ability of the business to appropriately use the

assets of the business for generating revenue. The auditor needs to ascertain whether the balances

which are shown are appropriate or not and whether the assets are properly valued or not. The

auditor in such a case can render some assistance from an expert in regards to valuation of asset

and the opinion of the expert would be considered to be final.

The leverage ratio which is represented in the table above is related to practices which are

adhered to by the management for maintain the capital structure of the business. The debt and

debt equity ratio of the business shows sudden increase from previous year which shows that the

management of the company has taken debts for restructuring the business’s capital structure.

have declined from previous years which needs to be considered by the auditor as to the reason

for the decline. The net working capital which shows liquid position also shows a decline which

means that the liquidity position of the business has been slightly affected. The auditor needs to

check the current assets with special emphasis on debtors, cash and inventory balances of the

business.

The profitability ratios are considered to be important ratios and the same comprises of

net profit ratio and other margins related to profitability which is shown in the table above. There

has been significant increase in both net and gross profit margin which a favorable sign for the

business is (Delen, Kuzey and Uyar 2013). There has also been positive impact on the estimates

of returns from equity and assets. The auditor of the business needs to check the sales figure and

also check the cost of goods sold to ascertain all transactions are accurate. In such a case, the

auditor can apply vouching practices for getting a clear idea.

The asset management ratios reflect the ability of the business to appropriately use the

assets of the business for generating revenue. The auditor needs to ascertain whether the balances

which are shown are appropriate or not and whether the assets are properly valued or not. The

auditor in such a case can render some assistance from an expert in regards to valuation of asset

and the opinion of the expert would be considered to be final.

The leverage ratio which is represented in the table above is related to practices which are

adhered to by the management for maintain the capital structure of the business. The debt and

debt equity ratio of the business shows sudden increase from previous year which shows that the

management of the company has taken debts for restructuring the business’s capital structure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

The auditor needs ascertain the balances of equity share capital and also the debt capital in order

to ensure that there is no material misstatement.

Section 3

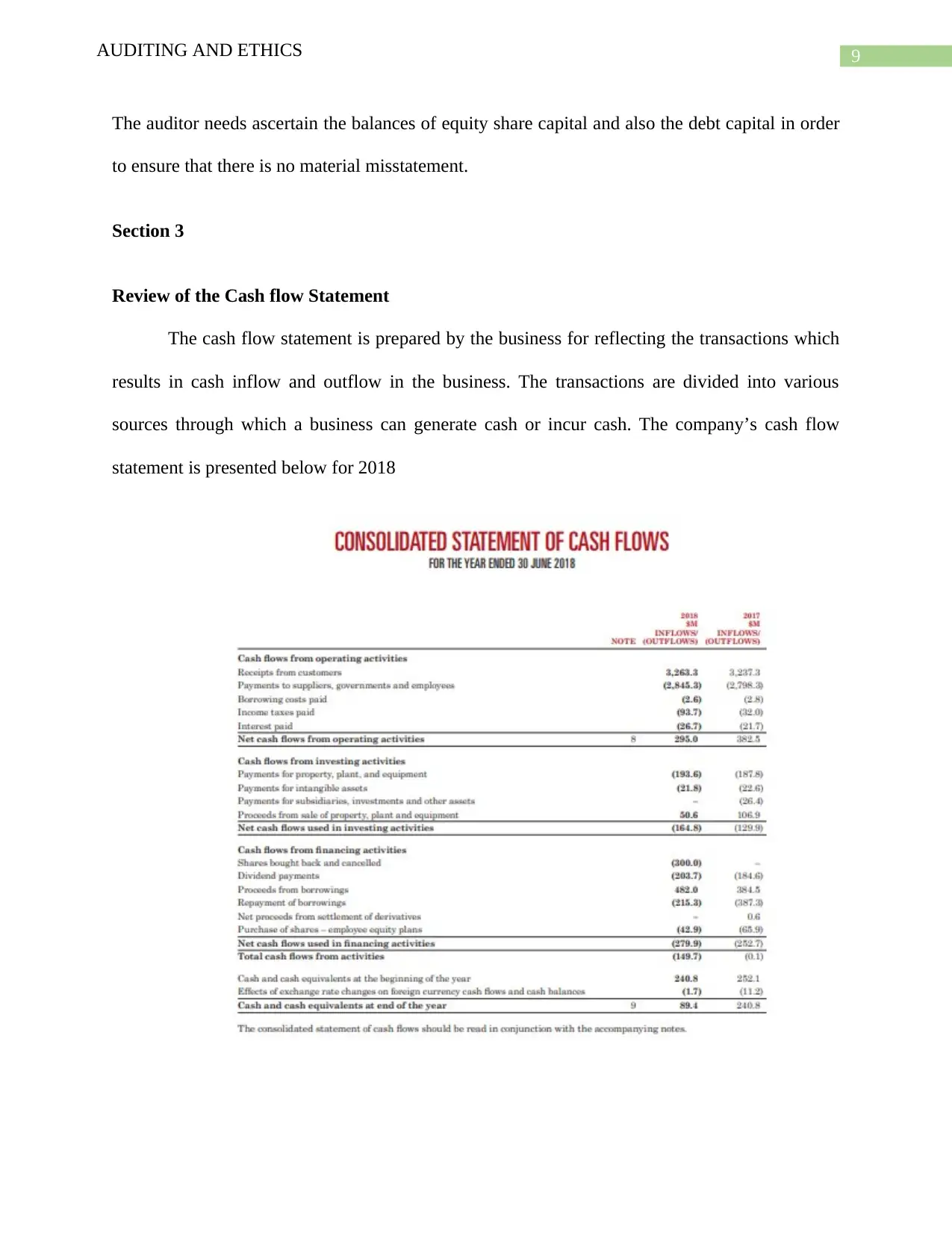

Review of the Cash flow Statement

The cash flow statement is prepared by the business for reflecting the transactions which

results in cash inflow and outflow in the business. The transactions are divided into various

sources through which a business can generate cash or incur cash. The company’s cash flow

statement is presented below for 2018

The auditor needs ascertain the balances of equity share capital and also the debt capital in order

to ensure that there is no material misstatement.

Section 3

Review of the Cash flow Statement

The cash flow statement is prepared by the business for reflecting the transactions which

results in cash inflow and outflow in the business. The transactions are divided into various

sources through which a business can generate cash or incur cash. The company’s cash flow

statement is presented below for 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

The business is able to generate more cash from operating activities than any other

activities and the same is shown to be $ 3263.6 million which shows a slight increase in cash

flow of the business and the main cash outflow for the business is the payments made to

suppliers of the company. The main cash flow associated with investing activities which is

shown is the purchase of property, plant and equipment which are used by the business for the

purpose of generating revenue for the business (Legoria, Melendrez and Reynolds 2013). This

shows that the business has purchased new assets which needs to be reviewed by the auditor of

the business. The main cash flow from financing activity of the business is the loan which is

taken by the business which indicates that changes have been made in the capital structure of the

business.

The going concern principle is one of the to be fundamental for formulation of the

financial statements of a business. This principle states that the business is looking forward to

continue the operations of the business without any stoppage in future. The annual report of

Treasury Wine Estates ltd shows significant improvements in profitability of the business and the

liquidity position of the business is also shown to be accurate. Further more the cash flow

statement formulated by the business is also showing accurate view of the financial strength

which shows that the business is operating well.

Analysis of Auditor’s Report

The opinion which is given by the auditor is that every transactions is appropriately

represented and appropriate treatments are also disclosed in the notes to account section of the

financial statements (Moroney and Trotman 2016). The annual reports also follow necessary

regulations of Corporation Act and is also compliant with relevant accounting standards. This is

the main reason that the auditor has provided unqualified audit report to the business.

The business is able to generate more cash from operating activities than any other

activities and the same is shown to be $ 3263.6 million which shows a slight increase in cash

flow of the business and the main cash outflow for the business is the payments made to

suppliers of the company. The main cash flow associated with investing activities which is

shown is the purchase of property, plant and equipment which are used by the business for the

purpose of generating revenue for the business (Legoria, Melendrez and Reynolds 2013). This

shows that the business has purchased new assets which needs to be reviewed by the auditor of

the business. The main cash flow from financing activity of the business is the loan which is

taken by the business which indicates that changes have been made in the capital structure of the

business.

The going concern principle is one of the to be fundamental for formulation of the

financial statements of a business. This principle states that the business is looking forward to

continue the operations of the business without any stoppage in future. The annual report of

Treasury Wine Estates ltd shows significant improvements in profitability of the business and the

liquidity position of the business is also shown to be accurate. Further more the cash flow

statement formulated by the business is also showing accurate view of the financial strength

which shows that the business is operating well.

Analysis of Auditor’s Report

The opinion which is given by the auditor is that every transactions is appropriately

represented and appropriate treatments are also disclosed in the notes to account section of the

financial statements (Moroney and Trotman 2016). The annual reports also follow necessary

regulations of Corporation Act and is also compliant with relevant accounting standards. This is

the main reason that the auditor has provided unqualified audit report to the business.

11AUDITING AND ETHICS

The key audit matters for the company which have been included in the annual report of

the business are related to inventories of the company which are completed and WIP and

therefore the auditor needs to apply appropriate judgement to ensure that the values are accurate.

The management of the company follows a practice of recording net sales when the wine

products are actually shipped off so that the same can reach the customers in time. This practice

is also included in key audit matter for the business.

Reference

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

The key audit matters for the company which have been included in the annual report of

the business are related to inventories of the company which are completed and WIP and

therefore the auditor needs to apply appropriate judgement to ensure that the values are accurate.

The management of the company follows a practice of recording net sales when the wine

products are actually shipped off so that the same can reach the customers in time. This practice

is also included in key audit matter for the business.

Reference

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.