ACCT20075 CQUniversity: Materiality, Audit Procedures & Ethics Report

VerifiedAdded on 2023/06/08

|13

|3306

|200

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics, focusing on materiality considerations, analytical procedures, and cash flow statement analysis. It assesses the financial statements of Cornwell Group, computing planning materiality and analyzing disclosures related to deferred tax, derivative contracts, and reserves. Key financial ratios, including liquidity, profitability, asset management, leverage, and valuation ratios, are calculated and interpreted to evaluate the company's financial health and identify potential risks. The report also examines the cash flow statement, categorizing activities into operating, investing, and financing, and concludes with a review of the auditor's report, ensuring compliance with auditing standards and ethical considerations. Desklib is a platform which provides all the necessary AI based study tools for students.

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student:

Name of the University:

Author’s Note

Auditing and Ethics

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality Consideration in Audit..............................................................................................2

Analysis of Disclosures and Notes..............................................................................................3

Section 2..........................................................................................................................................5

Analytical Procedures in Auditing...............................................................................................5

Section 3..........................................................................................................................................8

Cash Flow Statement Analysis....................................................................................................8

Review of the Auditor’s Report.................................................................................................10

Reference.......................................................................................................................................11

AUDITING AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality Consideration in Audit..............................................................................................2

Analysis of Disclosures and Notes..............................................................................................3

Section 2..........................................................................................................................................5

Analytical Procedures in Auditing...............................................................................................5

Section 3..........................................................................................................................................8

Cash Flow Statement Analysis....................................................................................................8

Review of the Auditor’s Report.................................................................................................10

Reference.......................................................................................................................................11

2

AUDITING AND ETHICS

Section 1

Materiality Consideration in Audit

The concept of materiality is covered in ISA 320 which is an auditing standard which

covers the significance of materiality while conducting an audit of a business. The materiality

aspect of an item which is shown in the financial statements of a company is based on the

judgement on the auditor which is generally done on the basis of complexity of the item or

relevance of the item in relation to the financial statement of the business. In an audit process,

the materiality of an item plays an important role as the auditor generally concentrates and

applies more audit procedures on items which are considered to be material in nature in respect

to the business of the client (Cox, Dayanandan & Donker, 2014). The assessment will be

considering the financial statements of Cornwell Group which is engaged in the business of real

estate management for clients (Cromwellpropertygroup.com, 2018). The purpose of the

assessment is to analyze the financial statements of the company to comment whether the same

is showing true and fair view or not. The assessment will also be computing planning materiality

for the business.

The materiality concept in audit has a much wider scope and covers both qualitative

material items and quantitative material items. Qualitative material items refer to those

significant items of a financial statement which are generally relevant and most likely to have

material misstatements. On the other hand, quantitative material items refer to which are of

significant value and are shown in the financial statements of the company. The presence of

material items in the financial statements determines the audit procedures which the auditor is

going to apply and also the timing and extent of the audit is also determined similarly

AUDITING AND ETHICS

Section 1

Materiality Consideration in Audit

The concept of materiality is covered in ISA 320 which is an auditing standard which

covers the significance of materiality while conducting an audit of a business. The materiality

aspect of an item which is shown in the financial statements of a company is based on the

judgement on the auditor which is generally done on the basis of complexity of the item or

relevance of the item in relation to the financial statement of the business. In an audit process,

the materiality of an item plays an important role as the auditor generally concentrates and

applies more audit procedures on items which are considered to be material in nature in respect

to the business of the client (Cox, Dayanandan & Donker, 2014). The assessment will be

considering the financial statements of Cornwell Group which is engaged in the business of real

estate management for clients (Cromwellpropertygroup.com, 2018). The purpose of the

assessment is to analyze the financial statements of the company to comment whether the same

is showing true and fair view or not. The assessment will also be computing planning materiality

for the business.

The materiality concept in audit has a much wider scope and covers both qualitative

material items and quantitative material items. Qualitative material items refer to those

significant items of a financial statement which are generally relevant and most likely to have

material misstatements. On the other hand, quantitative material items refer to which are of

significant value and are shown in the financial statements of the company. The presence of

material items in the financial statements determines the audit procedures which the auditor is

going to apply and also the timing and extent of the audit is also determined similarly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING AND ETHICS

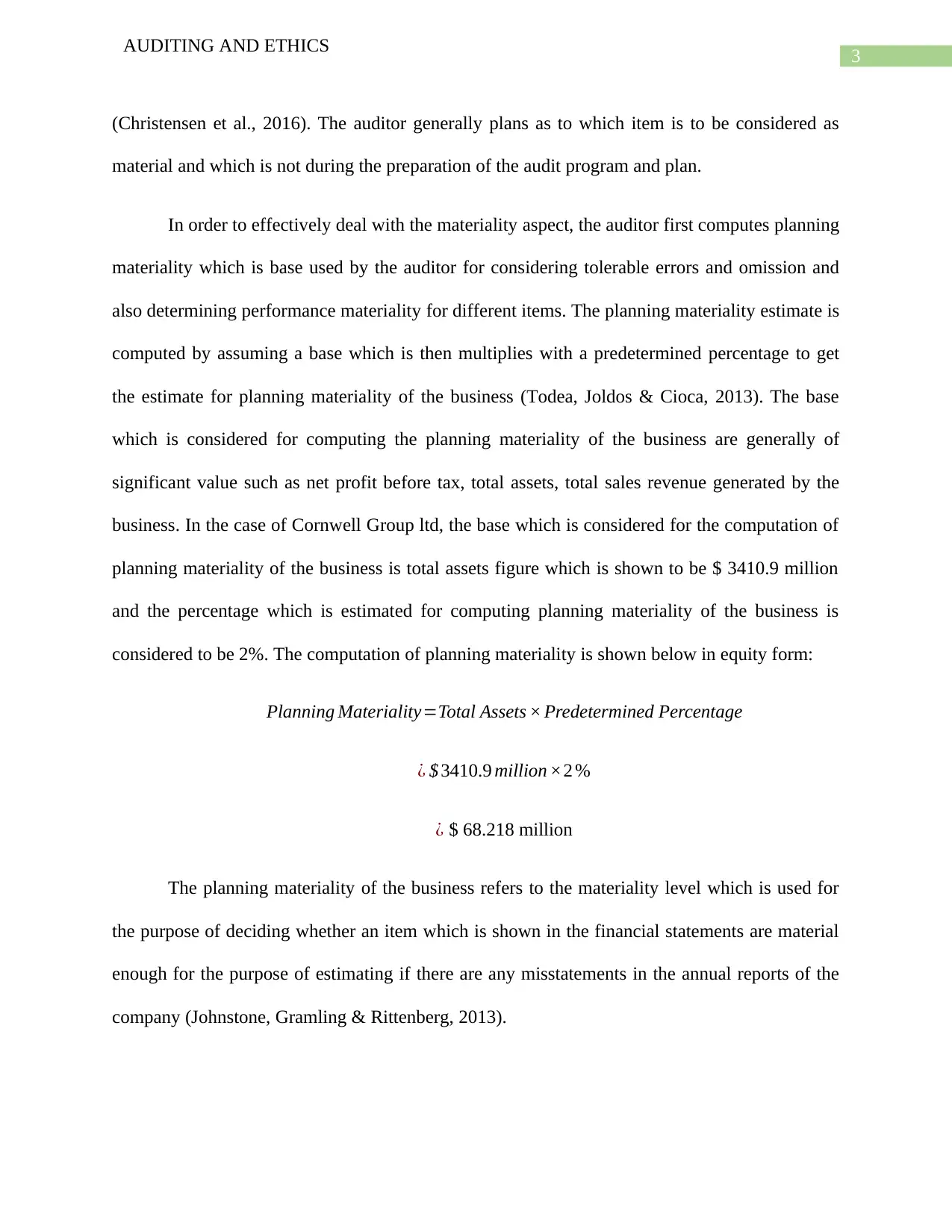

(Christensen et al., 2016). The auditor generally plans as to which item is to be considered as

material and which is not during the preparation of the audit program and plan.

In order to effectively deal with the materiality aspect, the auditor first computes planning

materiality which is base used by the auditor for considering tolerable errors and omission and

also determining performance materiality for different items. The planning materiality estimate is

computed by assuming a base which is then multiplies with a predetermined percentage to get

the estimate for planning materiality of the business (Todea, Joldos & Cioca, 2013). The base

which is considered for computing the planning materiality of the business are generally of

significant value such as net profit before tax, total assets, total sales revenue generated by the

business. In the case of Cornwell Group ltd, the base which is considered for the computation of

planning materiality of the business is total assets figure which is shown to be $ 3410.9 million

and the percentage which is estimated for computing planning materiality of the business is

considered to be 2%. The computation of planning materiality is shown below in equity form:

Planning Materiality=Total Assets × Predetermined Percentage

¿ $ 3410.9 million ×2 %

¿ $ 68.218 million

The planning materiality of the business refers to the materiality level which is used for

the purpose of deciding whether an item which is shown in the financial statements are material

enough for the purpose of estimating if there are any misstatements in the annual reports of the

company (Johnstone, Gramling & Rittenberg, 2013).

AUDITING AND ETHICS

(Christensen et al., 2016). The auditor generally plans as to which item is to be considered as

material and which is not during the preparation of the audit program and plan.

In order to effectively deal with the materiality aspect, the auditor first computes planning

materiality which is base used by the auditor for considering tolerable errors and omission and

also determining performance materiality for different items. The planning materiality estimate is

computed by assuming a base which is then multiplies with a predetermined percentage to get

the estimate for planning materiality of the business (Todea, Joldos & Cioca, 2013). The base

which is considered for computing the planning materiality of the business are generally of

significant value such as net profit before tax, total assets, total sales revenue generated by the

business. In the case of Cornwell Group ltd, the base which is considered for the computation of

planning materiality of the business is total assets figure which is shown to be $ 3410.9 million

and the percentage which is estimated for computing planning materiality of the business is

considered to be 2%. The computation of planning materiality is shown below in equity form:

Planning Materiality=Total Assets × Predetermined Percentage

¿ $ 3410.9 million ×2 %

¿ $ 68.218 million

The planning materiality of the business refers to the materiality level which is used for

the purpose of deciding whether an item which is shown in the financial statements are material

enough for the purpose of estimating if there are any misstatements in the annual reports of the

company (Johnstone, Gramling & Rittenberg, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING AND ETHICS

Analysis of Disclosures and Notes

The notes to accounts are considered to be an important aspect of the financial statements

and contain information regarding the treatments and methods which are used by the

management in the preparation of the financial statements of the business (Hahn & Lülfs, 2014).

The significant items which are covered in the disclosures and notes to account section are

discussed below:

Deferred Tax Assets and Liabilities: The annual reports of the business show that the

same consist of deferred tax assets and liabilities which are shown in the notes to account

section of the annual report. The deferred tax assets and liabilities of the business arises

due to temporary difference and carried forward losses of the business (Laux, 2013). The

deferred tax assets and liabilities of the business contains complex treatments and

therefore the auditor needs to review the same.

Interest and Cross Currency Derivative Contracts: As per the notes to accounts

section of the annual reports, interest and cross currency contracts information are present

which can affect the decision of the auditor. The business in engaged in derivate contracts

and therefore the auditor needs to put emphasis on the valuation for the same in order to

understand that the same is showing true and fair view or not.

Reserves: The reserves which are shown by the business in the annual reports of the

company. The reserves amount which is shown in the annual reports of the company is

considered to be important figure as the same can affect the financial statements of the

business. The auditor needs to analyze the same and ensure that the financial statements

are showing a clear view of the reserves and also the sources which are used for creating

the reserves.

AUDITING AND ETHICS

Analysis of Disclosures and Notes

The notes to accounts are considered to be an important aspect of the financial statements

and contain information regarding the treatments and methods which are used by the

management in the preparation of the financial statements of the business (Hahn & Lülfs, 2014).

The significant items which are covered in the disclosures and notes to account section are

discussed below:

Deferred Tax Assets and Liabilities: The annual reports of the business show that the

same consist of deferred tax assets and liabilities which are shown in the notes to account

section of the annual report. The deferred tax assets and liabilities of the business arises

due to temporary difference and carried forward losses of the business (Laux, 2013). The

deferred tax assets and liabilities of the business contains complex treatments and

therefore the auditor needs to review the same.

Interest and Cross Currency Derivative Contracts: As per the notes to accounts

section of the annual reports, interest and cross currency contracts information are present

which can affect the decision of the auditor. The business in engaged in derivate contracts

and therefore the auditor needs to put emphasis on the valuation for the same in order to

understand that the same is showing true and fair view or not.

Reserves: The reserves which are shown by the business in the annual reports of the

company. The reserves amount which is shown in the annual reports of the company is

considered to be important figure as the same can affect the financial statements of the

business. The auditor needs to analyze the same and ensure that the financial statements

are showing a clear view of the reserves and also the sources which are used for creating

the reserves.

5

AUDITING AND ETHICS

Section 2

Analytical Procedures in Auditing

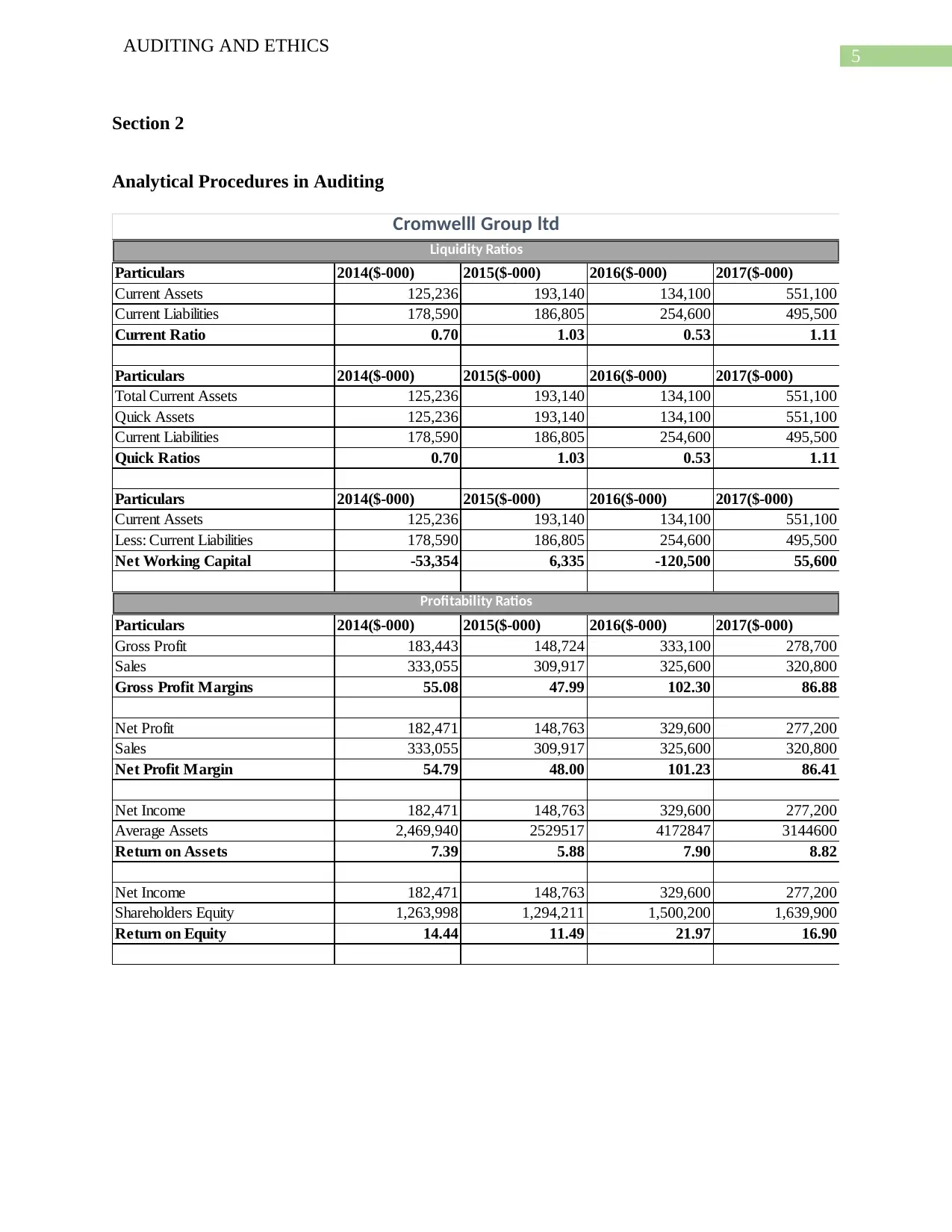

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Current Assets 125,236 193,140 134,100 551,100

Current Liabilities 178,590 186,805 254,600 495,500

Current Ratio 0.70 1.03 0.53 1.11

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Total Current Assets 125,236 193,140 134,100 551,100

Quick Assets 125,236 193,140 134,100 551,100

Current Liabilities 178,590 186,805 254,600 495,500

Quick Ratios 0.70 1.03 0.53 1.11

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Current Assets 125,236 193,140 134,100 551,100

Less: Current Liabilities 178,590 186,805 254,600 495,500

Net Working Capital -53,354 6,335 -120,500 55,600

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Gross Profit 183,443 148,724 333,100 278,700

Sales 333,055 309,917 325,600 320,800

Gross Profit Margins 55.08 47.99 102.30 86.88

Net Profit 182,471 148,763 329,600 277,200

Sales 333,055 309,917 325,600 320,800

Net Profit Margin 54.79 48.00 101.23 86.41

Net Income 182,471 148,763 329,600 277,200

Average Assets 2,469,940 2529517 4172847 3144600

Return on Assets 7.39 5.88 7.90 8.82

Net Income 182,471 148,763 329,600 277,200

Shareholders Equity 1,263,998 1,294,211 1,500,200 1,639,900

Return on Equity 14.44 11.49 21.97 16.90

Cromwelll Group ltd

Liquidity Ratios

Profitability Ratios

AUDITING AND ETHICS

Section 2

Analytical Procedures in Auditing

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Current Assets 125,236 193,140 134,100 551,100

Current Liabilities 178,590 186,805 254,600 495,500

Current Ratio 0.70 1.03 0.53 1.11

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Total Current Assets 125,236 193,140 134,100 551,100

Quick Assets 125,236 193,140 134,100 551,100

Current Liabilities 178,590 186,805 254,600 495,500

Quick Ratios 0.70 1.03 0.53 1.11

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Current Assets 125,236 193,140 134,100 551,100

Less: Current Liabilities 178,590 186,805 254,600 495,500

Net Working Capital -53,354 6,335 -120,500 55,600

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Gross Profit 183,443 148,724 333,100 278,700

Sales 333,055 309,917 325,600 320,800

Gross Profit Margins 55.08 47.99 102.30 86.88

Net Profit 182,471 148,763 329,600 277,200

Sales 333,055 309,917 325,600 320,800

Net Profit Margin 54.79 48.00 101.23 86.41

Net Income 182,471 148,763 329,600 277,200

Average Assets 2,469,940 2529517 4172847 3144600

Return on Assets 7.39 5.88 7.90 8.82

Net Income 182,471 148,763 329,600 277,200

Shareholders Equity 1,263,998 1,294,211 1,500,200 1,639,900

Return on Equity 14.44 11.49 21.97 16.90

Cromwelll Group ltd

Liquidity Ratios

Profitability Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING AND ETHICS

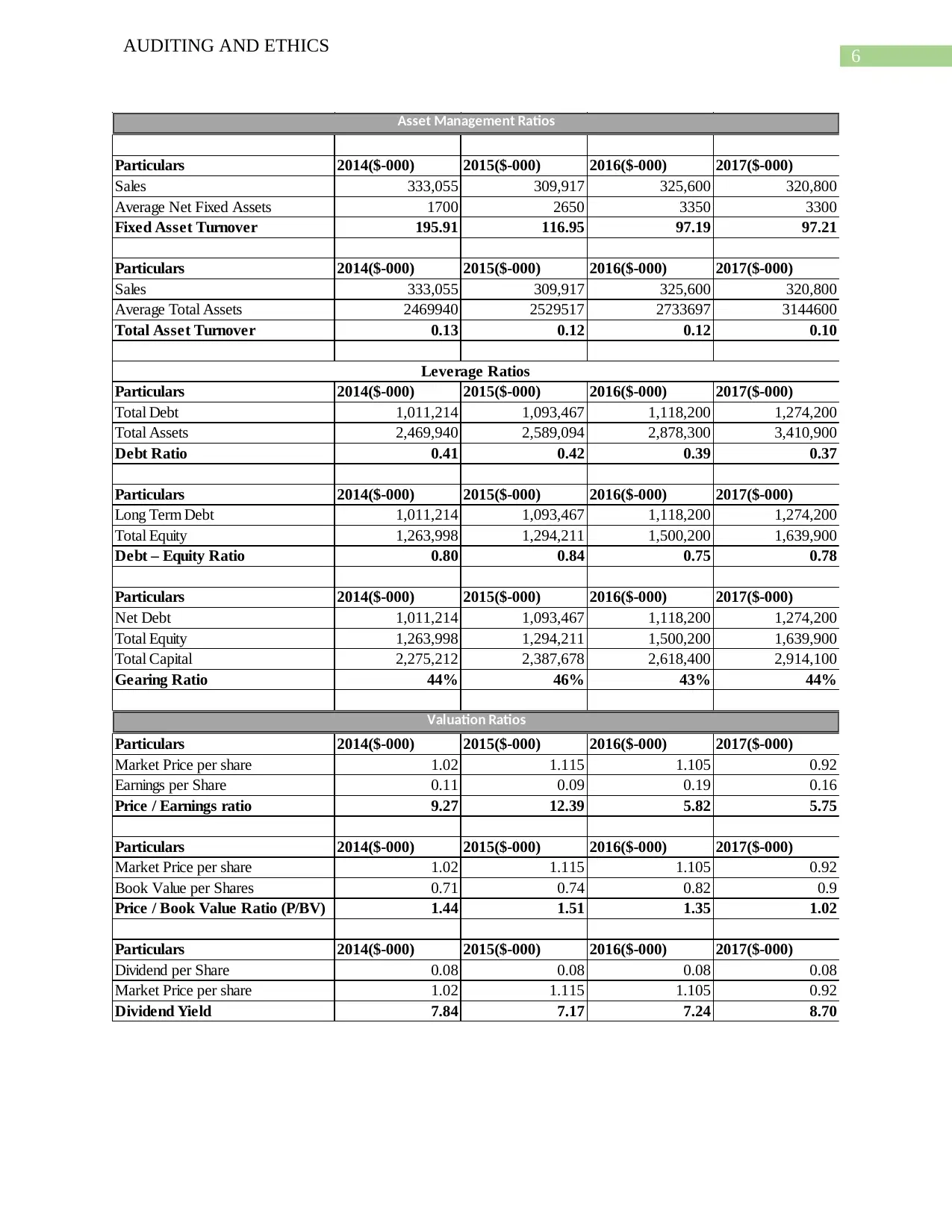

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Sales 333,055 309,917 325,600 320,800

Average Net Fixed Assets 1700 2650 3350 3300

Fixed Asset Turnover 195.91 116.95 97.19 97.21

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Sales 333,055 309,917 325,600 320,800

Average Total Assets 2469940 2529517 2733697 3144600

Total Asset Turnover 0.13 0.12 0.12 0.10

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Total Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Assets 2,469,940 2,589,094 2,878,300 3,410,900

Debt Ratio 0.41 0.42 0.39 0.37

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Long Term Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Equity 1,263,998 1,294,211 1,500,200 1,639,900

Debt – Equity Ratio 0.80 0.84 0.75 0.78

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Net Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Equity 1,263,998 1,294,211 1,500,200 1,639,900

Total Capital 2,275,212 2,387,678 2,618,400 2,914,100

Gearing Ratio 44% 46% 43% 44%

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Market Price per share 1.02 1.115 1.105 0.92

Earnings per Share 0.11 0.09 0.19 0.16

Price / Earnings ratio 9.27 12.39 5.82 5.75

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Market Price per share 1.02 1.115 1.105 0.92

Book Value per Shares 0.71 0.74 0.82 0.9

Price / Book Value Ratio (P/BV) 1.44 1.51 1.35 1.02

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Dividend per Share 0.08 0.08 0.08 0.08

Market Price per share 1.02 1.115 1.105 0.92

Dividend Yield 7.84 7.17 7.24 8.70

Valuation Ratios

Asset Management Ratios

Leverage Ratios

AUDITING AND ETHICS

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Sales 333,055 309,917 325,600 320,800

Average Net Fixed Assets 1700 2650 3350 3300

Fixed Asset Turnover 195.91 116.95 97.19 97.21

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Sales 333,055 309,917 325,600 320,800

Average Total Assets 2469940 2529517 2733697 3144600

Total Asset Turnover 0.13 0.12 0.12 0.10

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Total Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Assets 2,469,940 2,589,094 2,878,300 3,410,900

Debt Ratio 0.41 0.42 0.39 0.37

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Long Term Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Equity 1,263,998 1,294,211 1,500,200 1,639,900

Debt – Equity Ratio 0.80 0.84 0.75 0.78

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Net Debt 1,011,214 1,093,467 1,118,200 1,274,200

Total Equity 1,263,998 1,294,211 1,500,200 1,639,900

Total Capital 2,275,212 2,387,678 2,618,400 2,914,100

Gearing Ratio 44% 46% 43% 44%

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Market Price per share 1.02 1.115 1.105 0.92

Earnings per Share 0.11 0.09 0.19 0.16

Price / Earnings ratio 9.27 12.39 5.82 5.75

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Market Price per share 1.02 1.115 1.105 0.92

Book Value per Shares 0.71 0.74 0.82 0.9

Price / Book Value Ratio (P/BV) 1.44 1.51 1.35 1.02

Particulars 2014($-000) 2015($-000) 2016($-000) 2017($-000)

Dividend per Share 0.08 0.08 0.08 0.08

Market Price per share 1.02 1.115 1.105 0.92

Dividend Yield 7.84 7.17 7.24 8.70

Valuation Ratios

Asset Management Ratios

Leverage Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING AND ETHICS

Analytical Procedure refers to calculations of key financial ratios which are used by the

auditor to assess the risks which are involved in a business. As per the analysis of the financial

statements of Cornwell Group and also the key financial ratios which are computed in above

chart, significant ratios of a business are effectively computed.

The liquidity ratio of the business comprises of current assets and quick assets of the

business. The current ratio and quick ratio of the business are shown to be favorable for the year

2017 as the estimates are shown to be 1.11. The liquidity ratio of the business is considered to be

important for the purpose of estimating the cash position of the business (Jans, Alles &

Vasarhelyi, 2014). The auditor needs to take into consideration the liquidity risks of the business.

The profitability ratio of the business comprises of gross profit ratio, net profit ratio,

return on assets and return of equity of the business. The gross profit ratio of the business is

shown to have tremendously improved from previous year performance of profitability. This

shows that the business has an efficient operational structure and is also performing better in

terms of previous year. The net profit ratio of the business also shows improvement from

estimates of previous year which suggest that company is maintain the costs of the business

(Yoon, Hoogduin & Zhang, 2015). The auditor needs to ensure that the balance which are shown

in the financial statements are showing true view and no item which should be present in the

income statement is missing. The return on assets and return on equity of the business is shown

to be favorable which is also a positive sign for the business. Both these estimates are considered

to be financial indicators for the success of the business.

The asset management ratio comprises of asset turnover ratio which shows the ability of

the business to generate revenue from the use of assets of the business. The asset turnover ratio is

AUDITING AND ETHICS

Analytical Procedure refers to calculations of key financial ratios which are used by the

auditor to assess the risks which are involved in a business. As per the analysis of the financial

statements of Cornwell Group and also the key financial ratios which are computed in above

chart, significant ratios of a business are effectively computed.

The liquidity ratio of the business comprises of current assets and quick assets of the

business. The current ratio and quick ratio of the business are shown to be favorable for the year

2017 as the estimates are shown to be 1.11. The liquidity ratio of the business is considered to be

important for the purpose of estimating the cash position of the business (Jans, Alles &

Vasarhelyi, 2014). The auditor needs to take into consideration the liquidity risks of the business.

The profitability ratio of the business comprises of gross profit ratio, net profit ratio,

return on assets and return of equity of the business. The gross profit ratio of the business is

shown to have tremendously improved from previous year performance of profitability. This

shows that the business has an efficient operational structure and is also performing better in

terms of previous year. The net profit ratio of the business also shows improvement from

estimates of previous year which suggest that company is maintain the costs of the business

(Yoon, Hoogduin & Zhang, 2015). The auditor needs to ensure that the balance which are shown

in the financial statements are showing true view and no item which should be present in the

income statement is missing. The return on assets and return on equity of the business is shown

to be favorable which is also a positive sign for the business. Both these estimates are considered

to be financial indicators for the success of the business.

The asset management ratio comprises of asset turnover ratio which shows the ability of

the business to generate revenue from the use of assets of the business. The asset turnover ratio is

8

AUDITING AND ETHICS

also shown to be favorable. However, the auditor needs to check whether the fixed assets of the

business are valued in a proper way for which the auditor can use the help of an expert for

valuation of the assets of the business. The auditor also needs to check the condition of the assets

and also the depreciation which is charged on the assets which affect the valuation of the assets

of the business.

The leverage ratio of the business is associated with capital structure which is used by the

business during the year. The debt ratio of the business measures the debt of the business and the

calculation which is shown in the financial statements and the same shows that the debt of the

business has reduced significantly as per the policies of the business. The debt to equity ratio of

the business shows the mixture of debt and equity which is used by the business for financing the

activities of the business. The auditor needs to verify whether the balance which are shown for

the borrowings and equity are appropriately shown in the annual reports of the business.

The dividend which is shown in the financial statements of the business shows the current

performance of the business. The dividend yield ratio of the business shows the dividend of the

business has increased significantly during the financial period. The auditor needs to check

whether the financial statements effectively shows the value of dividend paid by the business

during the year.

Section 3

Cash Flow Statement Analysis

The cash flow statement of the business is shown in the financial statement of the company and

shows different activities which are undertaken by the business which includes operating

activities, investing activities and financing activities.

AUDITING AND ETHICS

also shown to be favorable. However, the auditor needs to check whether the fixed assets of the

business are valued in a proper way for which the auditor can use the help of an expert for

valuation of the assets of the business. The auditor also needs to check the condition of the assets

and also the depreciation which is charged on the assets which affect the valuation of the assets

of the business.

The leverage ratio of the business is associated with capital structure which is used by the

business during the year. The debt ratio of the business measures the debt of the business and the

calculation which is shown in the financial statements and the same shows that the debt of the

business has reduced significantly as per the policies of the business. The debt to equity ratio of

the business shows the mixture of debt and equity which is used by the business for financing the

activities of the business. The auditor needs to verify whether the balance which are shown for

the borrowings and equity are appropriately shown in the annual reports of the business.

The dividend which is shown in the financial statements of the business shows the current

performance of the business. The dividend yield ratio of the business shows the dividend of the

business has increased significantly during the financial period. The auditor needs to check

whether the financial statements effectively shows the value of dividend paid by the business

during the year.

Section 3

Cash Flow Statement Analysis

The cash flow statement of the business is shown in the financial statement of the company and

shows different activities which are undertaken by the business which includes operating

activities, investing activities and financing activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING AND ETHICS

The cash from operating activities of the business generates maximum amount of cash

flows for the business as the same is shown to be $ 154.3 million. The cash from investing

activities as shown in the cash flow statement of the business shows the maximum amount of

cash outflows for the business. The cash from investing activities is shown to be $ 187.7 million.

The primary cash receipts as identified from the cash flow statement of the business for the year

2017 is shown to be receipt from customers for the operational activities of the business and the

figure for the same is shown to be $ 342 million. The primary cash payment which is made by

the business as identified in the cash flow statement is the payments which is made to the

suppliers of the business during the year. The cash flow statement shows the two major cash

receipts and cash payments are covered in cash from operating activities of the business.

The main cash from investing activities can be identified as the payments which the

business made for the acquisition of disposal group. The main cash from financing activities of

the business is the receipts which the business gets from taking a loan for the business.

The going concern principle of the business is considered to be an important principle

which all accounting professionals are required to follow while preparing the financial

statements of the business. As per the analysis of the financial statements, the net profits of the

business are shown to be favorable and also the liquidity position of the business is also shown to

be appropriate (Krishnan & Wang, 2014). The business also has positive cash from operations as

per the estimates which are shown in the cash flow statement of the business. Therefore, it can be

assessed from the financial statements of the business that the going concern of the business is

not affected in any way (Feldmann & Read, 2013). However, the audit in order to satisfy the

skeptical attitude needs to apply audit procedures in order to confirm or deny whether the going

concern principle of the business are appropriate or not.

AUDITING AND ETHICS

The cash from operating activities of the business generates maximum amount of cash

flows for the business as the same is shown to be $ 154.3 million. The cash from investing

activities as shown in the cash flow statement of the business shows the maximum amount of

cash outflows for the business. The cash from investing activities is shown to be $ 187.7 million.

The primary cash receipts as identified from the cash flow statement of the business for the year

2017 is shown to be receipt from customers for the operational activities of the business and the

figure for the same is shown to be $ 342 million. The primary cash payment which is made by

the business as identified in the cash flow statement is the payments which is made to the

suppliers of the business during the year. The cash flow statement shows the two major cash

receipts and cash payments are covered in cash from operating activities of the business.

The main cash from investing activities can be identified as the payments which the

business made for the acquisition of disposal group. The main cash from financing activities of

the business is the receipts which the business gets from taking a loan for the business.

The going concern principle of the business is considered to be an important principle

which all accounting professionals are required to follow while preparing the financial

statements of the business. As per the analysis of the financial statements, the net profits of the

business are shown to be favorable and also the liquidity position of the business is also shown to

be appropriate (Krishnan & Wang, 2014). The business also has positive cash from operations as

per the estimates which are shown in the cash flow statement of the business. Therefore, it can be

assessed from the financial statements of the business that the going concern of the business is

not affected in any way (Feldmann & Read, 2013). However, the audit in order to satisfy the

skeptical attitude needs to apply audit procedures in order to confirm or deny whether the going

concern principle of the business are appropriate or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING AND ETHICS

Review of the Auditor’s Report

As per the auditor’s report of the business, the financial statements of the company is

shown to be showing true and fair view and all relevant accounting standards are followed in the

preparation of the financial statements of the business and also all relevant regulations of

accounting are also followed accordingly as per Corporation Act 2001. The auditor of the

company is Pitcher partners and as per their judgement they have issued an unqualified audit

report (Louwers et al., 2015).

The valuation of investment property which is done by the management is a bit complex

in nature and therefore the auditor needs to apply relevant accounting standards for the purpose

of valuation of investment properties. The auditor needs apply verification process for ensuring

that the value of properties are effectively represented. The valuation of intangible assets of the

business are also covered in the key audit matters of the company and the auditor needs to

estimate whether the same are showing true and fair view.

AUDITING AND ETHICS

Review of the Auditor’s Report

As per the auditor’s report of the business, the financial statements of the company is

shown to be showing true and fair view and all relevant accounting standards are followed in the

preparation of the financial statements of the business and also all relevant regulations of

accounting are also followed accordingly as per Corporation Act 2001. The auditor of the

company is Pitcher partners and as per their judgement they have issued an unqualified audit

report (Louwers et al., 2015).

The valuation of investment property which is done by the management is a bit complex

in nature and therefore the auditor needs to apply relevant accounting standards for the purpose

of valuation of investment properties. The auditor needs apply verification process for ensuring

that the value of properties are effectively represented. The valuation of intangible assets of the

business are also covered in the key audit matters of the company and the auditor needs to

estimate whether the same are showing true and fair view.

11

AUDITING AND ETHICS

Reference

Christensen, B. E., Glover, S. M., Omer, T. C., & Shelley, M. K. (2016). Understanding audit

quality: Insights from audit partners and investors. Contemporary Accounting

Research, 33(4), 1648-1684.

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks: A

Canadian perspective. International Journal of Disclosure and Governance, 11(3), 284-

298.

Cromwellpropertygroup.com (2018). Retrieved 1 September 2018, from

https://www.cromwellpropertygroup.com/__data/assets/pdf_file/0015/22920/CMW-

2017-Annual-Report-final-web.pdf

Feldmann, D., & Read, W. J. (2013). Going-concern audit opinions for bankrupt companies–

impact of credit rating. Managerial Auditing Journal, 28(4), 345-363.

Hahn, R., & Lülfs, R. (2014). Legitimizing negative aspects in GRI-oriented sustainability

reporting: A qualitative analysis of corporate disclosure strategies. Journal of business

ethics, 123(3), 401-420.

Jans, M., Alles, M. G., & Vasarhelyi, M. A. (2014). A field study on the use of process mining of

event logs as an analytical procedure in auditing. The Accounting Review, 89(5), 1751-

1773.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

AUDITING AND ETHICS

Reference

Christensen, B. E., Glover, S. M., Omer, T. C., & Shelley, M. K. (2016). Understanding audit

quality: Insights from audit partners and investors. Contemporary Accounting

Research, 33(4), 1648-1684.

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks: A

Canadian perspective. International Journal of Disclosure and Governance, 11(3), 284-

298.

Cromwellpropertygroup.com (2018). Retrieved 1 September 2018, from

https://www.cromwellpropertygroup.com/__data/assets/pdf_file/0015/22920/CMW-

2017-Annual-Report-final-web.pdf

Feldmann, D., & Read, W. J. (2013). Going-concern audit opinions for bankrupt companies–

impact of credit rating. Managerial Auditing Journal, 28(4), 345-363.

Hahn, R., & Lülfs, R. (2014). Legitimizing negative aspects in GRI-oriented sustainability

reporting: A qualitative analysis of corporate disclosure strategies. Journal of business

ethics, 123(3), 401-420.

Jans, M., Alles, M. G., & Vasarhelyi, M. A. (2014). A field study on the use of process mining of

event logs as an analytical procedure in auditing. The Accounting Review, 89(5), 1751-

1773.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.