ACCT20075: Auditing and Ethics - Analyzing Meridian Energy Report

VerifiedAdded on 2023/06/07

|12

|3111

|369

Report

AI Summary

This report assesses the 2017 annual report of Meridian Energy Group Limited, focusing on determining the appropriate level of materiality for the audit. It examines the nature of materiality, its representation in financial statement audits, and the bases and considerations used to arrive at a specific materiality level, advocating for the 5% rule. The report reviews draft notes and disclosures, highlighting the impact of hydro inflow and asset impairments. A preliminary analytical review is conducted, analyzing key balance sheet and profit & loss ratios, including return on shareholder equity, EPS, debt to equity ratio, and current ratio. Relevant assertions and audit procedures, such as accuracy, completeness, and occurrence, are discussed. Finally, the report reviews the statement of cash flows, noting major cash inflows and outflows, and identifies non-cash financial and investing activities. This comprehensive analysis provides a thorough understanding of Meridian Energy's financial standing and audit considerations.

Running head: AUDITING 1

Auditing

Name

Professor

Institution

Date

Auditing

Name

Professor

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING 2

Introduction

Meridian Energy Group Limited is among the largest organizations in New Zealand.

It earns a revenue of $2,762 million in the financial year 2018 and realizes net assets

amounting to $4,823 million. This paper is primarily purposed to examine the 2017 annual

report for Meridian Energy Group Limited and determine the level of materiality that should

be used for the group accounts for the fiscal year ending 2017. This report also represents a

preliminary analytical review on the information that is provided by the company. Key

balance sheet and profit and loss ratios over the period 2014 to 2017 have been addressed.

Additionally, the report gives a review of the cash flow statement of the company and

discusses its primary cash receipts and cash payments during the year ending 2018 (Meridian

Energy Group, 2018).

Section 1: The Level of Materiality to Be Used For the Audit

a. Nature of Materiality

According to International Standards on Auditing (ISA) 320, materiality refers to

misstatements or omissions of key financial items that are considered significant either

individually or collectively, in influencing the financial and economic decisions of various

users of financial statements presented by an entity. However, the nature and magnitude of

materiality is highly dependent on the size of the reporting company or entity, the nature and

size of the financial item. (Reding, & Institute of Internal Auditors Research Foundation.

IIARF, 2013). In Meridian Energy Group Limited, determination of the level of materiality

to be used in the audit is very important (Media, 2012).

Introduction

Meridian Energy Group Limited is among the largest organizations in New Zealand.

It earns a revenue of $2,762 million in the financial year 2018 and realizes net assets

amounting to $4,823 million. This paper is primarily purposed to examine the 2017 annual

report for Meridian Energy Group Limited and determine the level of materiality that should

be used for the group accounts for the fiscal year ending 2017. This report also represents a

preliminary analytical review on the information that is provided by the company. Key

balance sheet and profit and loss ratios over the period 2014 to 2017 have been addressed.

Additionally, the report gives a review of the cash flow statement of the company and

discusses its primary cash receipts and cash payments during the year ending 2018 (Meridian

Energy Group, 2018).

Section 1: The Level of Materiality to Be Used For the Audit

a. Nature of Materiality

According to International Standards on Auditing (ISA) 320, materiality refers to

misstatements or omissions of key financial items that are considered significant either

individually or collectively, in influencing the financial and economic decisions of various

users of financial statements presented by an entity. However, the nature and magnitude of

materiality is highly dependent on the size of the reporting company or entity, the nature and

size of the financial item. (Reding, & Institute of Internal Auditors Research Foundation.

IIARF, 2013). In Meridian Energy Group Limited, determination of the level of materiality

to be used in the audit is very important (Media, 2012).

AUDITING 3

b. What Materiality Represents In Terms of the Audit of a Set of Financial

Statements

Materiality in the audit of financial statements represents significant errors or

misstatements in the amounts reported. Misstatements or errors in financial statements are

often considered as misstatements that have not been recorded or corrected. In normal

financial statement audits, auditors often consider identifying and reporting the dollar amount

of such errors and misstatements on a schedule which normally provides a listing of two

main categories of errors in financial reports (Reding & Institute of Internal Auditors

Research Foundation, 2013). These include:

i. Amounts reported in financial statements which have been recorded

incorrectly. These are transactions which were generally not recorded

correctly since they were posted in incorrect amounts or in wrong accounts.

ii. Amounts that should have been recorded in the financial statements but were

not (Moeller, 2016).

The auditor is responsible for calculating and determining the exact dollar amount of

the financial statement misstatements and errors that are considered to have been unrecorded

or uncorrected in such reports. For errors that are based on an adjustment which is based on

estimates, the auditor must consider them to have been caused by deficiencies or weaknesses

in the internal controls of Meridian Energy Group Limited. Therefore, the auditor must make

a consideration to review each and every financial statement item against an acceptable level

of materiality which is determined prior to the audit, with an aim to determine whether

adjustments should be made to financial statements or not Liu, 2015).

b. What Materiality Represents In Terms of the Audit of a Set of Financial

Statements

Materiality in the audit of financial statements represents significant errors or

misstatements in the amounts reported. Misstatements or errors in financial statements are

often considered as misstatements that have not been recorded or corrected. In normal

financial statement audits, auditors often consider identifying and reporting the dollar amount

of such errors and misstatements on a schedule which normally provides a listing of two

main categories of errors in financial reports (Reding & Institute of Internal Auditors

Research Foundation, 2013). These include:

i. Amounts reported in financial statements which have been recorded

incorrectly. These are transactions which were generally not recorded

correctly since they were posted in incorrect amounts or in wrong accounts.

ii. Amounts that should have been recorded in the financial statements but were

not (Moeller, 2016).

The auditor is responsible for calculating and determining the exact dollar amount of

the financial statement misstatements and errors that are considered to have been unrecorded

or uncorrected in such reports. For errors that are based on an adjustment which is based on

estimates, the auditor must consider them to have been caused by deficiencies or weaknesses

in the internal controls of Meridian Energy Group Limited. Therefore, the auditor must make

a consideration to review each and every financial statement item against an acceptable level

of materiality which is determined prior to the audit, with an aim to determine whether

adjustments should be made to financial statements or not Liu, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING 4

c. Different Bases and Considerations Employed in Arriving at Materiality

In determining the levels of materiality for Meridian Energy Group Limited, the

auditor must consider various bases and factors. For example, the materiality level used

should relate to the various uses and purposes intended for the audit of the company’s

financial statements audit. Therefore, it is essential for the auditor to understand the financial

information which is considered important and useful to decision makers and users of such

reports (VALLABHANENI, 2018). For example, with respect to issues relating to solvency

or regulation, the materiality level is highly dependent on the benchmarks in solvency ratios

derived from the industry in which the group company operates. In addition to this, for

appraisal purposes, the materiality level is specifically determined by the net income or net

worth of the company, as well as it’s per share earnings. Furthermore, for general purposes

which are related to financial statements of the company, the materiality level is highly

dependent on the net surplus and the net capital or net income of the company as well

(Meridian Energy Group, 2018).

The level of materiality is also influenced by other features or characteristics of the

company which include its size and access to capital, as well as the stage of organizational

life cycle. A company’s financial strength is also critical in determination of the level of

materiality that should be adopted for the financial audit. It is generally agreed that as an

entity approaches a given level of materiality, the materiality standard for work relating to

that threshold becomes more rigorous (Meridian Energy Group, 2018).

d. The Rationale behind Your Choice of a Certain Level of Materiality

c. Different Bases and Considerations Employed in Arriving at Materiality

In determining the levels of materiality for Meridian Energy Group Limited, the

auditor must consider various bases and factors. For example, the materiality level used

should relate to the various uses and purposes intended for the audit of the company’s

financial statements audit. Therefore, it is essential for the auditor to understand the financial

information which is considered important and useful to decision makers and users of such

reports (VALLABHANENI, 2018). For example, with respect to issues relating to solvency

or regulation, the materiality level is highly dependent on the benchmarks in solvency ratios

derived from the industry in which the group company operates. In addition to this, for

appraisal purposes, the materiality level is specifically determined by the net income or net

worth of the company, as well as it’s per share earnings. Furthermore, for general purposes

which are related to financial statements of the company, the materiality level is highly

dependent on the net surplus and the net capital or net income of the company as well

(Meridian Energy Group, 2018).

The level of materiality is also influenced by other features or characteristics of the

company which include its size and access to capital, as well as the stage of organizational

life cycle. A company’s financial strength is also critical in determination of the level of

materiality that should be adopted for the financial audit. It is generally agreed that as an

entity approaches a given level of materiality, the materiality standard for work relating to

that threshold becomes more rigorous (Meridian Energy Group, 2018).

d. The Rationale behind Your Choice of a Certain Level of Materiality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING 5

Determining and ascertaining the dollar amounts that are considered material

misstatements and errors in the financial statement is highly influenced by objectivity of the

auditor. The auditor usually applies a specific percentage or range of materiality to dollar

amounts of each item in the financial statements taken as a whole. This percentage is

normally chosen as a benchmark for ascertain the maximum level of materiality beyond

which financial statements and reports must not me misstates, since they would significantly

influence decision making capabilities of users. These chosen benchmarks are based mainly

on financial statement items such as gross profit or total revenues (Meridian Energy Group,

2018).

In determination of the materiality level relating to unrecorded as well as uncorrected

misstatements and errors in the financial statements of Meridian Energy Group Limited, the

auditor should use the 5% rule. This rule is very essential in providing a general level of

materiality that should be adopted in financial statements audits. According to this rule, the

value of misstatements in dollar amounts is determined with key consideration to a specified

percentage of materiality level which should not exceed this limit (Verschoor, 2008). The

auditor must therefore, is therefore a need to take appropriate audit tests and measures for

ascertaining whether or not the actual misstatements happened. In the audit of Meridian

Energy Group Limited, 5% is therefore considered the maximum level of materiality which

must not be exceeded in the financial statements audit. Misstatements which exceed this limit

in the financial statements of Meridian Energy Group Limited are thus considered material

(Key, Riddle & Institute of Internal Auditors, 2012).

e. Review the Various Draft Notes and Disclosures

Determining and ascertaining the dollar amounts that are considered material

misstatements and errors in the financial statement is highly influenced by objectivity of the

auditor. The auditor usually applies a specific percentage or range of materiality to dollar

amounts of each item in the financial statements taken as a whole. This percentage is

normally chosen as a benchmark for ascertain the maximum level of materiality beyond

which financial statements and reports must not me misstates, since they would significantly

influence decision making capabilities of users. These chosen benchmarks are based mainly

on financial statement items such as gross profit or total revenues (Meridian Energy Group,

2018).

In determination of the materiality level relating to unrecorded as well as uncorrected

misstatements and errors in the financial statements of Meridian Energy Group Limited, the

auditor should use the 5% rule. This rule is very essential in providing a general level of

materiality that should be adopted in financial statements audits. According to this rule, the

value of misstatements in dollar amounts is determined with key consideration to a specified

percentage of materiality level which should not exceed this limit (Verschoor, 2008). The

auditor must therefore, is therefore a need to take appropriate audit tests and measures for

ascertaining whether or not the actual misstatements happened. In the audit of Meridian

Energy Group Limited, 5% is therefore considered the maximum level of materiality which

must not be exceeded in the financial statements audit. Misstatements which exceed this limit

in the financial statements of Meridian Energy Group Limited are thus considered material

(Key, Riddle & Institute of Internal Auditors, 2012).

e. Review the Various Draft Notes and Disclosures

AUDITING 6

After reviewing several draft notes and disclosures that accompany the draft annual

report of are thus considered material, various significant issues were observed. For instance,

the Hydro inflow is a significant matter in the financial year of the company. The dry

conditions that were experienced during the start of the financial year continued to January.

However, the conditions changed abruptly in February. This is believed to have caused

material and significant changes in the revenues realized by Meridian Energy Group Limited

since the weather changes enabled the catchment areas to deliver more water into river

Waitaki than in any other time in the previous five years. The company has therefore

experienced a good storage of water since the onset of winter. The Meridian Energy Group

Limited was however affected significantly by the dry conditions since it was forced to

reduce materially its hydro generation production, thus calling of electricity swaptions during

the first half of its 2017 financial year (Wells, 2014).

In addition to this, Meridian Energy Group Limited makes a review of its tangible

and intangible assets at each balance date. These assets are grouped by the company as per

the cash generating units with cash flows that can be identified separately. The recoverable

amount is considered as the higher of the fair value of the asset less the selling costs and the

resent value of the projected cash flows of the asset. In the financial year 2018, Meridian

Energy Group Limited there was a significant impairment in the book value of the central

wind consent. This is because development at the particular location of the item was not most

likely to happen before the existing resource consent had expired (Jubb, 2010).

Section 2: A Preliminary Analytical Review on the Information Provided

a. Key Balance Sheet and Profit & Loss Ratios

After reviewing several draft notes and disclosures that accompany the draft annual

report of are thus considered material, various significant issues were observed. For instance,

the Hydro inflow is a significant matter in the financial year of the company. The dry

conditions that were experienced during the start of the financial year continued to January.

However, the conditions changed abruptly in February. This is believed to have caused

material and significant changes in the revenues realized by Meridian Energy Group Limited

since the weather changes enabled the catchment areas to deliver more water into river

Waitaki than in any other time in the previous five years. The company has therefore

experienced a good storage of water since the onset of winter. The Meridian Energy Group

Limited was however affected significantly by the dry conditions since it was forced to

reduce materially its hydro generation production, thus calling of electricity swaptions during

the first half of its 2017 financial year (Wells, 2014).

In addition to this, Meridian Energy Group Limited makes a review of its tangible

and intangible assets at each balance date. These assets are grouped by the company as per

the cash generating units with cash flows that can be identified separately. The recoverable

amount is considered as the higher of the fair value of the asset less the selling costs and the

resent value of the projected cash flows of the asset. In the financial year 2018, Meridian

Energy Group Limited there was a significant impairment in the book value of the central

wind consent. This is because development at the particular location of the item was not most

likely to happen before the existing resource consent had expired (Jubb, 2010).

Section 2: A Preliminary Analytical Review on the Information Provided

a. Key Balance Sheet and Profit & Loss Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING 7

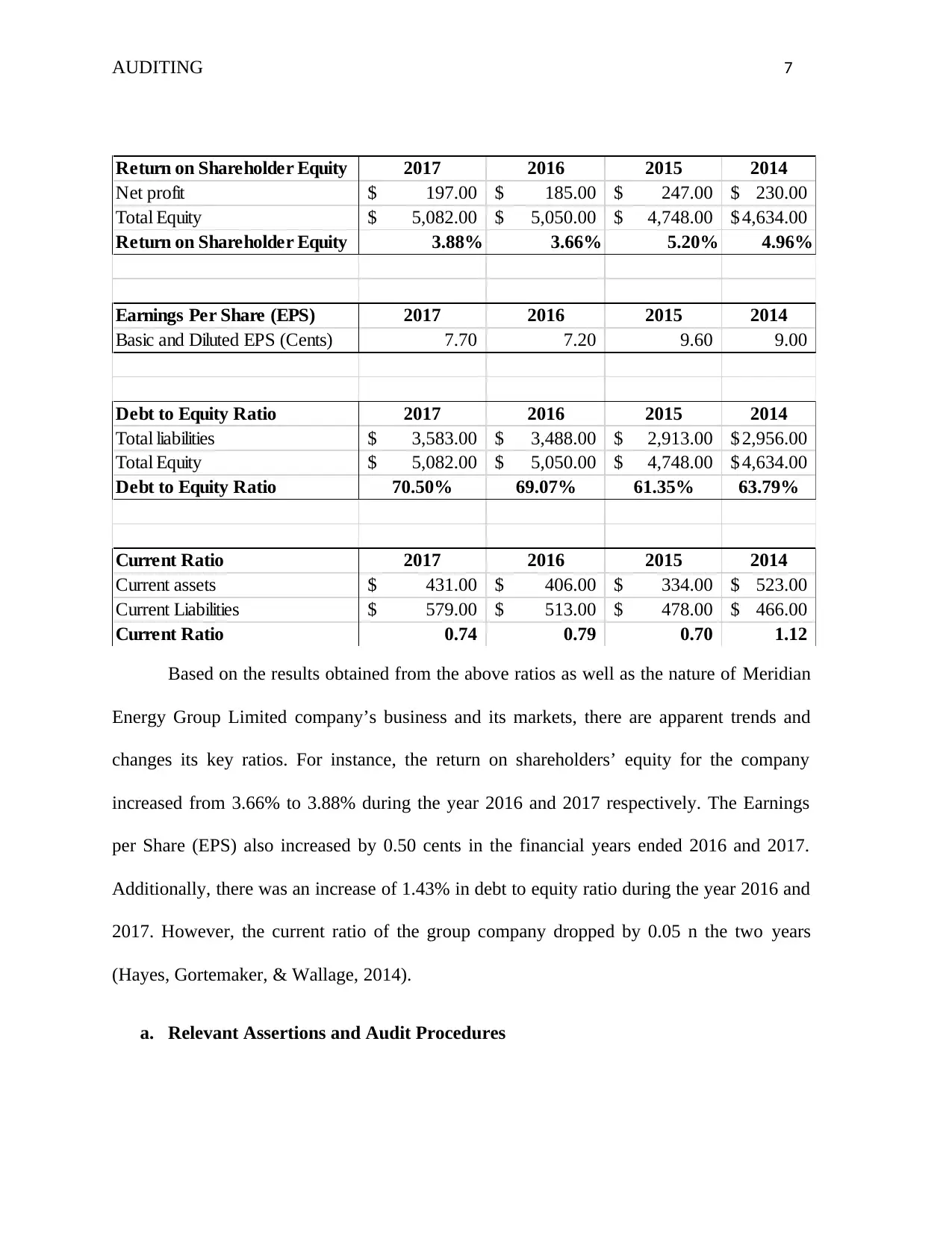

Return on Shareholder Equity 2017 2016 2015 2014

Net profit 197.00$ 185.00$ 247.00$ 230.00$

Total Equity 5,082.00$ 5,050.00$ 4,748.00$ 4,634.00$

Return on Shareholder Equity 3.88% 3.66% 5.20% 4.96%

Earnings Per Share (EPS) 2017 2016 2015 2014

Basic and Diluted EPS (Cents) 7.70 7.20 9.60 9.00

Debt to Equity Ratio 2017 2016 2015 2014

Total liabilities 3,583.00$ 3,488.00$ 2,913.00$ 2,956.00$

Total Equity 5,082.00$ 5,050.00$ 4,748.00$ 4,634.00$

Debt to Equity Ratio 70.50% 69.07% 61.35% 63.79%

Current Ratio 2017 2016 2015 2014

Current assets 431.00$ 406.00$ 334.00$ 523.00$

Current Liabilities 579.00$ 513.00$ 478.00$ 466.00$

Current Ratio 0.74 0.79 0.70 1.12

Based on the results obtained from the above ratios as well as the nature of Meridian

Energy Group Limited company’s business and its markets, there are apparent trends and

changes its key ratios. For instance, the return on shareholders’ equity for the company

increased from 3.66% to 3.88% during the year 2016 and 2017 respectively. The Earnings

per Share (EPS) also increased by 0.50 cents in the financial years ended 2016 and 2017.

Additionally, there was an increase of 1.43% in debt to equity ratio during the year 2016 and

2017. However, the current ratio of the group company dropped by 0.05 n the two years

(Hayes, Gortemaker, & Wallage, 2014).

a. Relevant Assertions and Audit Procedures

Return on Shareholder Equity 2017 2016 2015 2014

Net profit 197.00$ 185.00$ 247.00$ 230.00$

Total Equity 5,082.00$ 5,050.00$ 4,748.00$ 4,634.00$

Return on Shareholder Equity 3.88% 3.66% 5.20% 4.96%

Earnings Per Share (EPS) 2017 2016 2015 2014

Basic and Diluted EPS (Cents) 7.70 7.20 9.60 9.00

Debt to Equity Ratio 2017 2016 2015 2014

Total liabilities 3,583.00$ 3,488.00$ 2,913.00$ 2,956.00$

Total Equity 5,082.00$ 5,050.00$ 4,748.00$ 4,634.00$

Debt to Equity Ratio 70.50% 69.07% 61.35% 63.79%

Current Ratio 2017 2016 2015 2014

Current assets 431.00$ 406.00$ 334.00$ 523.00$

Current Liabilities 579.00$ 513.00$ 478.00$ 466.00$

Current Ratio 0.74 0.79 0.70 1.12

Based on the results obtained from the above ratios as well as the nature of Meridian

Energy Group Limited company’s business and its markets, there are apparent trends and

changes its key ratios. For instance, the return on shareholders’ equity for the company

increased from 3.66% to 3.88% during the year 2016 and 2017 respectively. The Earnings

per Share (EPS) also increased by 0.50 cents in the financial years ended 2016 and 2017.

Additionally, there was an increase of 1.43% in debt to equity ratio during the year 2016 and

2017. However, the current ratio of the group company dropped by 0.05 n the two years

(Hayes, Gortemaker, & Wallage, 2014).

a. Relevant Assertions and Audit Procedures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING 8

In the audit of Meridian Energy Group Limited, it is important for the auditor to make

various assertions regarding the classes of transactions and related disclosures for the

financial year ending 2018 (Meridian Energy Group, 2018).

i. Accuracy

The accuracy of the amounts reported in the financial statements of Meridian Energy

Group Limited need to be examined by the auditor. This can be accomplished by

critically examining the financial records to ascertain that the transactional amounts have

been recorded appropriately and necessary disclosures made (Fiedler & Fiedler, 2010).

ii. Completeness

The auditor must ensure that the all events and transactions that took place in the year

ending 2017 have been recorded in the financial reports. The auditor can do this through

critical examination of the financial records against the original documents (Fiedler &

Fiedler, 2010).

iii. Occurrence

It is necessary for the auditor to verify that the recorded events and transactions have

actually happened and they pertain to Meridian Energy Group Limited. This can be done

by examining and inspecting the original books of accounts such as purchase vouchers

(Arens, Elder & Beasley, 2016).

Section 3: Review the Statement of Cash Flows

After reviewing the cash flow statement of Meridian Energy Group Limited in the

year ended 2018, it has been observed that the majority of the company’s cash inflows

In the audit of Meridian Energy Group Limited, it is important for the auditor to make

various assertions regarding the classes of transactions and related disclosures for the

financial year ending 2018 (Meridian Energy Group, 2018).

i. Accuracy

The accuracy of the amounts reported in the financial statements of Meridian Energy

Group Limited need to be examined by the auditor. This can be accomplished by

critically examining the financial records to ascertain that the transactional amounts have

been recorded appropriately and necessary disclosures made (Fiedler & Fiedler, 2010).

ii. Completeness

The auditor must ensure that the all events and transactions that took place in the year

ending 2017 have been recorded in the financial reports. The auditor can do this through

critical examination of the financial records against the original documents (Fiedler &

Fiedler, 2010).

iii. Occurrence

It is necessary for the auditor to verify that the recorded events and transactions have

actually happened and they pertain to Meridian Energy Group Limited. This can be done

by examining and inspecting the original books of accounts such as purchase vouchers

(Arens, Elder & Beasley, 2016).

Section 3: Review the Statement of Cash Flows

After reviewing the cash flow statement of Meridian Energy Group Limited in the

year ended 2018, it has been observed that the majority of the company’s cash inflows

AUDITING 9

were generated from its cash flows from operating activities, totaling to $2,675 million.

The company generated net cash flows amounting to $427 million from its operating

activities in the year ending 2018. The company’s largest cash outflows were also

reported from its operating activities, which totaled to $2,339 million (Meridian Energy

Group, 2018). During the year ending 2018, Meridian Energy Group Limited received

primary cash receipts of $5,589 million. The company also reported primary cash

payments amounting to $3,520 million (Meridian Energy Group, 2018).

The Main Non-Cash Financial and Investing Activities

According to the cash flow statement of Meridian Energy Group Limited, the

company has several non-cash financial and investing activities. For instance, it receives

significant amounts from sale of its property, plant and equipment amounting to $23 million.

Meridian Energy Group Limited also purchases these items for an amount totaling to $33

million. In addition to this, the group company purchases one of its subsidiaries for $182

million (Crain, Hopwood, Pacini & Young, 2018).

Evaluation of the Going Concern Risk of This Company and Recommended Audit

Procedures

According to question 2 and 4, Meridian Energy Group Limited is experiencing key

risks in regard to ascertainment of its going concern. For instance, the group company is

depends highly on cash inflows from its operating activities because its investing and

financing activities reported a negative net cash flows of $224 million and $225 million

respectively during the year ended 2018 (Meridian Energy Group, 2018). In addition to this,

the greatest cash outflows of the company were reported from its operating activities. This is

were generated from its cash flows from operating activities, totaling to $2,675 million.

The company generated net cash flows amounting to $427 million from its operating

activities in the year ending 2018. The company’s largest cash outflows were also

reported from its operating activities, which totaled to $2,339 million (Meridian Energy

Group, 2018). During the year ending 2018, Meridian Energy Group Limited received

primary cash receipts of $5,589 million. The company also reported primary cash

payments amounting to $3,520 million (Meridian Energy Group, 2018).

The Main Non-Cash Financial and Investing Activities

According to the cash flow statement of Meridian Energy Group Limited, the

company has several non-cash financial and investing activities. For instance, it receives

significant amounts from sale of its property, plant and equipment amounting to $23 million.

Meridian Energy Group Limited also purchases these items for an amount totaling to $33

million. In addition to this, the group company purchases one of its subsidiaries for $182

million (Crain, Hopwood, Pacini & Young, 2018).

Evaluation of the Going Concern Risk of This Company and Recommended Audit

Procedures

According to question 2 and 4, Meridian Energy Group Limited is experiencing key

risks in regard to ascertainment of its going concern. For instance, the group company is

depends highly on cash inflows from its operating activities because its investing and

financing activities reported a negative net cash flows of $224 million and $225 million

respectively during the year ended 2018 (Meridian Energy Group, 2018). In addition to this,

the greatest cash outflows of the company were reported from its operating activities. This is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING 10

an indication that Meridian Energy Group Limited makes exceedingly huge payments which

may lead to significant stoppage of its operations in future should the cash outflows exceed

the inflows. This may highly contradict the going concern of Meridian Energy Group

Limited (Aicpa, 2017).

Recommendations

There are several audit procedures that recommended in order to help Meridian

Energy Group Limited address these risks. For instance, its management should diversify the

operations of the group company in order to ensure that operating activities are not the only

main sources of its cash inflows (Meridian Energy Group, 2018). It should also be ensured

that the huge costs and expenses are cut or reduced materially. This is very essential in

ensuring that the company recognizes an increased amount of free cash flow that can be used

for its future expansions in order to guarantee its going concern and eliminating the

associated risks (Dennis, 2015).

Review of the 2017 Financial Report for the Company

After reviewing the financial statements of Meridian Energy Group Limited for the

year ended 2018, it was observed that the independent auditor issued an unqualified opinion

with regard to its consolidated financial statements. In their opinion, it has been certified that

the financial statements of Meridian Energy Group Limited are prepared in accordance with

the GAAPs. The financial reports of the group company present fairly the financial position

of the group as well as its financial performance for the year ended 2018 (Meridian Energy

Group, 2018).

an indication that Meridian Energy Group Limited makes exceedingly huge payments which

may lead to significant stoppage of its operations in future should the cash outflows exceed

the inflows. This may highly contradict the going concern of Meridian Energy Group

Limited (Aicpa, 2017).

Recommendations

There are several audit procedures that recommended in order to help Meridian

Energy Group Limited address these risks. For instance, its management should diversify the

operations of the group company in order to ensure that operating activities are not the only

main sources of its cash inflows (Meridian Energy Group, 2018). It should also be ensured

that the huge costs and expenses are cut or reduced materially. This is very essential in

ensuring that the company recognizes an increased amount of free cash flow that can be used

for its future expansions in order to guarantee its going concern and eliminating the

associated risks (Dennis, 2015).

Review of the 2017 Financial Report for the Company

After reviewing the financial statements of Meridian Energy Group Limited for the

year ended 2018, it was observed that the independent auditor issued an unqualified opinion

with regard to its consolidated financial statements. In their opinion, it has been certified that

the financial statements of Meridian Energy Group Limited are prepared in accordance with

the GAAPs. The financial reports of the group company present fairly the financial position

of the group as well as its financial performance for the year ended 2018 (Meridian Energy

Group, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING 11

References

Aicpa. (2017). Auditing Standards 2017: Codification of Statements on Standards for Auditing

Standards. John Wiley & Sons Inc.

Arens, Al, A, Elder, R., & Beasley, M. (2016). Auditing, Assurance Services & Ethics in

Australia. Sydney: P. Ed Australia.

Crain, M. A., Hopwood, W. S., Pacini, C., & Young, G. R. (2018). Essentials of Forensic

Accounting. Somerset: John Wiley & Sons, Incorporated.

Dennis, I. (2015). Auditing Theory. New York, NY: Routledge.

Fiedler, B., & Fiedler, B. (2010). Student guide to accompany Essentials of auditing, assurance

services and ethics in Australia: An integrated approach [1st ed.]. Frenchs Forest,

NSW: Pearson Australia.

Hayes, R., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: An introduction to

international standards on auditing. Harlow: Pearson Education Limited.

Jubb, C. (2010). Assurance & auditing: Concepts for a changing environment. s.l.: Thomson

Learning.

Key, J., Riddle, C., & Institute of Internal Auditors. (2012). Sawyer's: Guide for internal

auditors. Altamonte Springs, FL: Institute of Internal Auditors Research Foundation.

Liu, J. (2015). Study on the Auditing Theory of Socialism with Chinese Characteristics, Revised

Edition. Hoboken: Wiley.

Media, B. P. (2012). ACCA F4 - Corp and Business Law (Eng) - Study Text 2013: Study Text.

London: BPP Learning Media.

Meridian Energy Group, inc. (2018). Retrieved from https://www.meridianenergygroupinc.com/

References

Aicpa. (2017). Auditing Standards 2017: Codification of Statements on Standards for Auditing

Standards. John Wiley & Sons Inc.

Arens, Al, A, Elder, R., & Beasley, M. (2016). Auditing, Assurance Services & Ethics in

Australia. Sydney: P. Ed Australia.

Crain, M. A., Hopwood, W. S., Pacini, C., & Young, G. R. (2018). Essentials of Forensic

Accounting. Somerset: John Wiley & Sons, Incorporated.

Dennis, I. (2015). Auditing Theory. New York, NY: Routledge.

Fiedler, B., & Fiedler, B. (2010). Student guide to accompany Essentials of auditing, assurance

services and ethics in Australia: An integrated approach [1st ed.]. Frenchs Forest,

NSW: Pearson Australia.

Hayes, R., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: An introduction to

international standards on auditing. Harlow: Pearson Education Limited.

Jubb, C. (2010). Assurance & auditing: Concepts for a changing environment. s.l.: Thomson

Learning.

Key, J., Riddle, C., & Institute of Internal Auditors. (2012). Sawyer's: Guide for internal

auditors. Altamonte Springs, FL: Institute of Internal Auditors Research Foundation.

Liu, J. (2015). Study on the Auditing Theory of Socialism with Chinese Characteristics, Revised

Edition. Hoboken: Wiley.

Media, B. P. (2012). ACCA F4 - Corp and Business Law (Eng) - Study Text 2013: Study Text.

London: BPP Learning Media.

Meridian Energy Group, inc. (2018). Retrieved from https://www.meridianenergygroupinc.com/

AUDITING 12

Moeller, R. R. (2016). Brink's modern internal auditing: A common body of knowledge.

Hoboken, NJ: Wiley.

Reding, K. F., & Institute of Internal Auditors Research Foundation. IIARF. (2013). Internal

auditing: Assurance & consulting services. Altomonte Springs, Fla.

VALLABHANENI, S. R. (2018). WILEY CIAEXCEL EXAM REVIEW FOCUS NOTES 2019,

PART 1: Essentials of internal auditing. S.l.: JOHN WILEY & SONS.

Verschoor, C. C. (2008). Audit committee essentials. Hoboken, NJ: John Wiley & Sons, Inc.

Wells, J. T. (2014). Principles of fraud examination. (Online version ---> Principles of fraud

examination.) Hoboken, NJ: Wiley & Sons, Inc.

Moeller, R. R. (2016). Brink's modern internal auditing: A common body of knowledge.

Hoboken, NJ: Wiley.

Reding, K. F., & Institute of Internal Auditors Research Foundation. IIARF. (2013). Internal

auditing: Assurance & consulting services. Altomonte Springs, Fla.

VALLABHANENI, S. R. (2018). WILEY CIAEXCEL EXAM REVIEW FOCUS NOTES 2019,

PART 1: Essentials of internal auditing. S.l.: JOHN WILEY & SONS.

Verschoor, C. C. (2008). Audit committee essentials. Hoboken, NJ: John Wiley & Sons, Inc.

Wells, J. T. (2014). Principles of fraud examination. (Online version ---> Principles of fraud

examination.) Hoboken, NJ: Wiley & Sons, Inc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.