Auditing and Ethics: A Financial Statement Analysis of Perpetual Ltd

VerifiedAdded on 2023/06/07

|12

|2995

|486

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics in the context of Perpetual Limited's financial statements. It covers materiality assessment, including quantitative calculations based on sales revenue, total assets, shareholders' equity, and net profit, to determine planning materiality. The report also examines audit materiality for specific items like cash and cash equivalents, receivables, and payables, along with disclosures and draft notes on contingencies and provisions. Furthermore, it includes a ratio computation analysis covering profitability, liquidity, and stability ratios from 2014 to 2017, highlighting key assertions and required audit procedures. Finally, the report reviews the company's cash flow statement and provides observations on operating and financing cash flows. Desklib offers a variety of resources, including past papers and solved assignments, to support students in their studies.

Running head: AUDITING AND ETHICS

Auditing and ethics

Name of the student

Name of the university

Student ID

Author note

Auditing and ethics

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Section 1.....................................................................................................................................2

Materiality..............................................................................................................................2

Audit materiality for Perpetual Limited.................................................................................3

Disclosures and draft notes....................................................................................................4

Section 2.....................................................................................................................................5

Ratio computation..................................................................................................................5

Section 3.....................................................................................................................................8

Cash flow statement...............................................................................................................8

Audit report............................................................................................................................8

Reference..................................................................................................................................10

Table of Contents

Section 1.....................................................................................................................................2

Materiality..............................................................................................................................2

Audit materiality for Perpetual Limited.................................................................................3

Disclosures and draft notes....................................................................................................4

Section 2.....................................................................................................................................5

Ratio computation..................................................................................................................5

Section 3.....................................................................................................................................8

Cash flow statement...............................................................................................................8

Audit report............................................................................................................................8

Reference..................................................................................................................................10

2AUDITING AND ETHICS

Section 1

Materiality

While the auditor carries on the audit procedure the main objective is to express the

opinion regarding whether the financial reports are presented in all the material aspects, as

per the applicable framework for financial reporting. This is separate decision and separate

responsibility that is made by the company while preparing the financial reports (Christensen,

Glover & Wolfe, 2014). In auditing context, the term materiality is the threshold limit above

which the incorrect or missing information related to financial statement is deemed to have

impact on the user’s decision making aspect. Sometimes it is construed in terms of the total

impact on the profits reported or changes in percentage for some specific items included in

financial statement (Moroney & Trotman, 2016). Steps involved in determining the

materiality are as follows –

Identifying external as well as internal shareholders

Conducting initial outreach for the shareholders

Identifying and prioritizing what needs to be measured

Designing the materiality survey

Launching the survey and starting with insight collection

Evaluating the insights

Putting the insights into action (Legoria, Melendrez & Reynolds, 2013).

At the stage of planning the auditor is required to analyse the materiality with regard

to the financial statements. Calculation of the materiality involves both qualitative as well as

quantitative methodologies. Once the materiality involved in financial reports are identified

and assessed by the auditor, performance materiality that is the tolerable misstatement with

Section 1

Materiality

While the auditor carries on the audit procedure the main objective is to express the

opinion regarding whether the financial reports are presented in all the material aspects, as

per the applicable framework for financial reporting. This is separate decision and separate

responsibility that is made by the company while preparing the financial reports (Christensen,

Glover & Wolfe, 2014). In auditing context, the term materiality is the threshold limit above

which the incorrect or missing information related to financial statement is deemed to have

impact on the user’s decision making aspect. Sometimes it is construed in terms of the total

impact on the profits reported or changes in percentage for some specific items included in

financial statement (Moroney & Trotman, 2016). Steps involved in determining the

materiality are as follows –

Identifying external as well as internal shareholders

Conducting initial outreach for the shareholders

Identifying and prioritizing what needs to be measured

Designing the materiality survey

Launching the survey and starting with insight collection

Evaluating the insights

Putting the insights into action (Legoria, Melendrez & Reynolds, 2013).

At the stage of planning the auditor is required to analyse the materiality with regard

to the financial statements. Calculation of the materiality involves both qualitative as well as

quantitative methodologies. Once the materiality involved in financial reports are identified

and assessed by the auditor, performance materiality that is the tolerable misstatement with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

regard to financial statements are set (Eilifsen & Messier, 2014). However, the planning

materiality must be higher than the performance materiality. The quantitative factors used for

computing the materiality planning are –

2% of sales revenue

1% of total assets

2% of shareholders equity

5% of net profit

Therefore, for Perpetual Limited the planning materiality amount will be as follows –

2% of sales revenue = $ 520,881 * 2% = $ 10,417.62 thousand

1% of total assets = $ 11,71,545 * 1% = $ 11,715.45 thousand

2% of shareholders equity = $ 634,381 * 2% = $ 12,687.62 thousand

5% of net profit = $ 137,238 * 5% = $ 6,861.90 thousand (Perpetual.com.au, 2018).

While calculating the materiality planning the auditor may choose to take highest

amount from the above. However, the auditor must understand qualitative factors related to

materiality involved in the financial statements before concluding the planning materiality

size. Therefore, in the given case of Perpetual Limited materiality can be planned at the

amount of $ 11,000 thousand. However, an amount ranging from 50% to 75% of materiality

planning is considered as the performance materiality or tolerable misstatement for Perpetual

Limited (Johnstone, Gramling & Rittenberg, 2013). It is based on the determination of lower

level of significant items involved in the financial reports like cash and cash equivalents,

receivables and payables.

regard to financial statements are set (Eilifsen & Messier, 2014). However, the planning

materiality must be higher than the performance materiality. The quantitative factors used for

computing the materiality planning are –

2% of sales revenue

1% of total assets

2% of shareholders equity

5% of net profit

Therefore, for Perpetual Limited the planning materiality amount will be as follows –

2% of sales revenue = $ 520,881 * 2% = $ 10,417.62 thousand

1% of total assets = $ 11,71,545 * 1% = $ 11,715.45 thousand

2% of shareholders equity = $ 634,381 * 2% = $ 12,687.62 thousand

5% of net profit = $ 137,238 * 5% = $ 6,861.90 thousand (Perpetual.com.au, 2018).

While calculating the materiality planning the auditor may choose to take highest

amount from the above. However, the auditor must understand qualitative factors related to

materiality involved in the financial statements before concluding the planning materiality

size. Therefore, in the given case of Perpetual Limited materiality can be planned at the

amount of $ 11,000 thousand. However, an amount ranging from 50% to 75% of materiality

planning is considered as the performance materiality or tolerable misstatement for Perpetual

Limited (Johnstone, Gramling & Rittenberg, 2013). It is based on the determination of lower

level of significant items involved in the financial reports like cash and cash equivalents,

receivables and payables.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

Audit materiality for Perpetual Limited

Cash and cash equivalents – Perpetual Limited’s cash and cash equivalents included the

short-term deposits that represent rolling for 30 days to 90 days term deposits. The company

mainly holds the cash and cash equivalents for supporting the regulatory requirement of

capital that was amounted to $ 151.2 million. However, there are no specific rules regarding

the amount and by nature cash is regarded as material item. Cash is considered as material

item as it forms integral part in user’s view for the company (Ruhnke & Schmidt, 2014). It is

recognized from the annual report of the company for the year closed on 30th June 2017 that

the cash and cash equivalent of the company has been increased from $ 278,230 to $ 323,487

over the past year. The auditor shall analyse all the receipts and payment related vouchers and

records. The auditor shall further verify the authorisation on payments to satisfy him that no

material misstatement or error has been taken place (Perpetual.com.au, 2018).

Receivables – It is recognized from the annual report of the company for the year closed on

30th June 2017 that the trade receivables of the company has been increased from $ 86,611 to

$ 90,046 over the past year. As receivable is always exposed to risk of bad debt and

misstatement the auditor shall verify all the data related to receivables. It shall carry out the

debtor ageing analysis for verifying the payments due for more than the allowed credit period

(Kanapickienė & Grundienė, 2015). In case of any suspicious transaction the auditor can

confirm the balance from third party also.

Payables – It is recognized from the annual report of the company for the year closed on 30th

June 2017 that the payables of the company has been increased from $ 38,523 to $ 51,850

over the past year. Payables are considered as material as it plays important role in analysing

the company’s liquidity position.

Audit materiality for Perpetual Limited

Cash and cash equivalents – Perpetual Limited’s cash and cash equivalents included the

short-term deposits that represent rolling for 30 days to 90 days term deposits. The company

mainly holds the cash and cash equivalents for supporting the regulatory requirement of

capital that was amounted to $ 151.2 million. However, there are no specific rules regarding

the amount and by nature cash is regarded as material item. Cash is considered as material

item as it forms integral part in user’s view for the company (Ruhnke & Schmidt, 2014). It is

recognized from the annual report of the company for the year closed on 30th June 2017 that

the cash and cash equivalent of the company has been increased from $ 278,230 to $ 323,487

over the past year. The auditor shall analyse all the receipts and payment related vouchers and

records. The auditor shall further verify the authorisation on payments to satisfy him that no

material misstatement or error has been taken place (Perpetual.com.au, 2018).

Receivables – It is recognized from the annual report of the company for the year closed on

30th June 2017 that the trade receivables of the company has been increased from $ 86,611 to

$ 90,046 over the past year. As receivable is always exposed to risk of bad debt and

misstatement the auditor shall verify all the data related to receivables. It shall carry out the

debtor ageing analysis for verifying the payments due for more than the allowed credit period

(Kanapickienė & Grundienė, 2015). In case of any suspicious transaction the auditor can

confirm the balance from third party also.

Payables – It is recognized from the annual report of the company for the year closed on 30th

June 2017 that the payables of the company has been increased from $ 38,523 to $ 51,850

over the past year. Payables are considered as material as it plays important role in analysing

the company’s liquidity position.

5AUDITING AND ETHICS

Disclosures and draft notes

Contingencies – under the ordinary business course, the contingent liabilities are disclosed by

the company with regard to potential claims and existing claims. The company is not sure

regarding the material impact of the contingencies on the financial position or operation of

the company for the year closed on 30th June 2017. When it is not possible to project the

amount in terms of materiality the auditor must project the chances of the contingencies to

take place. However, while projecting the likelihood of occurrence of the event the auditor

must use his professional experience and judgement. Contingent liability shall be disclosed in

the notes associated with the financial report if it is found that the liability is not probable but

reasonably possible or the liability is probable but the amount cannot be estimated. However,

if the occurrence or probability is remote, the contingent liability shall not be disclosed or

recorded.

Provisions – the company recognizes provisions under the financial statements while it has

present constructive or legal obligation owing to the past event and which can be reliably

measured. Further, it shall be probable that the economic benefit outflow is required for

settling down the obligations. Judgements are exercised by the management for estimating

the amount of provisions. There is a chance that outcome in the future year will differ from

the amounts provided s provision in the current year. Hence, the amount will have to be

adjusted for the carrying amount of the liability. While auditing the provisions the auditor

shall verify is with regard to contingencies and liabilities. The auditor shall further assure that

the provided amount is adequate and all the provisions are recorded through debiting profit

and loss account. Moreover, the auditor shall assure that all provisions are properly utilized

for intended purpose. All provisions shall be disclosed properly in financial reports.

Moreover, if the auditor is in the view that the created provisions are not adequate or in

excess, the management shall be advised for providing exact amount.

Disclosures and draft notes

Contingencies – under the ordinary business course, the contingent liabilities are disclosed by

the company with regard to potential claims and existing claims. The company is not sure

regarding the material impact of the contingencies on the financial position or operation of

the company for the year closed on 30th June 2017. When it is not possible to project the

amount in terms of materiality the auditor must project the chances of the contingencies to

take place. However, while projecting the likelihood of occurrence of the event the auditor

must use his professional experience and judgement. Contingent liability shall be disclosed in

the notes associated with the financial report if it is found that the liability is not probable but

reasonably possible or the liability is probable but the amount cannot be estimated. However,

if the occurrence or probability is remote, the contingent liability shall not be disclosed or

recorded.

Provisions – the company recognizes provisions under the financial statements while it has

present constructive or legal obligation owing to the past event and which can be reliably

measured. Further, it shall be probable that the economic benefit outflow is required for

settling down the obligations. Judgements are exercised by the management for estimating

the amount of provisions. There is a chance that outcome in the future year will differ from

the amounts provided s provision in the current year. Hence, the amount will have to be

adjusted for the carrying amount of the liability. While auditing the provisions the auditor

shall verify is with regard to contingencies and liabilities. The auditor shall further assure that

the provided amount is adequate and all the provisions are recorded through debiting profit

and loss account. Moreover, the auditor shall assure that all provisions are properly utilized

for intended purpose. All provisions shall be disclosed properly in financial reports.

Moreover, if the auditor is in the view that the created provisions are not adequate or in

excess, the management shall be advised for providing exact amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

Section 2

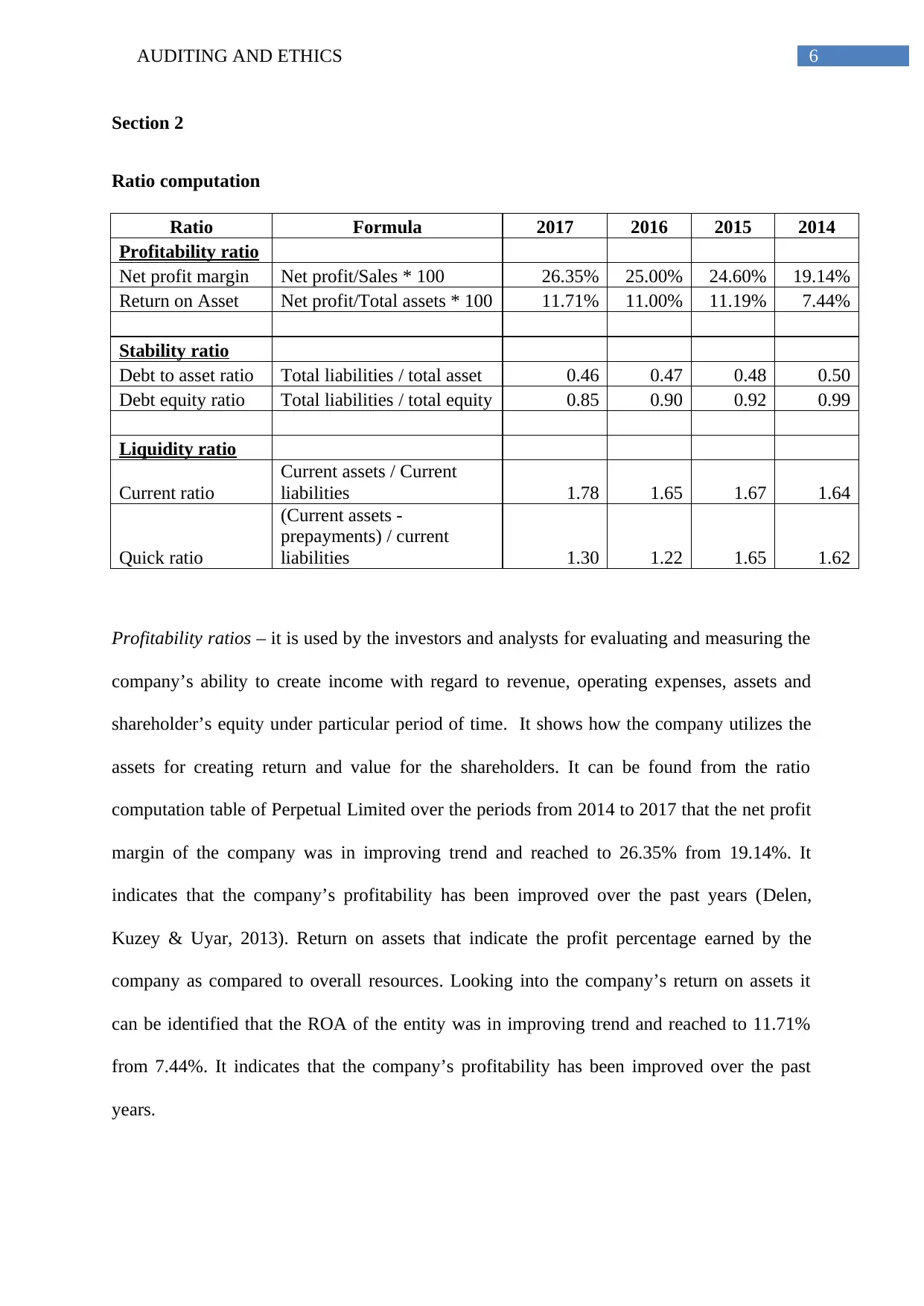

Ratio computation

Ratio Formula 2017 2016 2015 2014

Profitability ratio

Net profit margin Net profit/Sales * 100 26.35% 25.00% 24.60% 19.14%

Return on Asset Net profit/Total assets * 100 11.71% 11.00% 11.19% 7.44%

Stability ratio

Debt to asset ratio Total liabilities / total asset 0.46 0.47 0.48 0.50

Debt equity ratio Total liabilities / total equity 0.85 0.90 0.92 0.99

Liquidity ratio

Current ratio

Current assets / Current

liabilities 1.78 1.65 1.67 1.64

Quick ratio

(Current assets -

prepayments) / current

liabilities 1.30 1.22 1.65 1.62

Profitability ratios – it is used by the investors and analysts for evaluating and measuring the

company’s ability to create income with regard to revenue, operating expenses, assets and

shareholder’s equity under particular period of time. It shows how the company utilizes the

assets for creating return and value for the shareholders. It can be found from the ratio

computation table of Perpetual Limited over the periods from 2014 to 2017 that the net profit

margin of the company was in improving trend and reached to 26.35% from 19.14%. It

indicates that the company’s profitability has been improved over the past years (Delen,

Kuzey & Uyar, 2013). Return on assets that indicate the profit percentage earned by the

company as compared to overall resources. Looking into the company’s return on assets it

can be identified that the ROA of the entity was in improving trend and reached to 11.71%

from 7.44%. It indicates that the company’s profitability has been improved over the past

years.

Section 2

Ratio computation

Ratio Formula 2017 2016 2015 2014

Profitability ratio

Net profit margin Net profit/Sales * 100 26.35% 25.00% 24.60% 19.14%

Return on Asset Net profit/Total assets * 100 11.71% 11.00% 11.19% 7.44%

Stability ratio

Debt to asset ratio Total liabilities / total asset 0.46 0.47 0.48 0.50

Debt equity ratio Total liabilities / total equity 0.85 0.90 0.92 0.99

Liquidity ratio

Current ratio

Current assets / Current

liabilities 1.78 1.65 1.67 1.64

Quick ratio

(Current assets -

prepayments) / current

liabilities 1.30 1.22 1.65 1.62

Profitability ratios – it is used by the investors and analysts for evaluating and measuring the

company’s ability to create income with regard to revenue, operating expenses, assets and

shareholder’s equity under particular period of time. It shows how the company utilizes the

assets for creating return and value for the shareholders. It can be found from the ratio

computation table of Perpetual Limited over the periods from 2014 to 2017 that the net profit

margin of the company was in improving trend and reached to 26.35% from 19.14%. It

indicates that the company’s profitability has been improved over the past years (Delen,

Kuzey & Uyar, 2013). Return on assets that indicate the profit percentage earned by the

company as compared to overall resources. Looking into the company’s return on assets it

can be identified that the ROA of the entity was in improving trend and reached to 11.71%

from 7.44%. It indicates that the company’s profitability has been improved over the past

years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

Key assertion involved with the profitability ratio is accuracy that is the amount of

transaction has been recorded in full without any error. Required audit procedure for

removing this assertion is to check all the vouchers and receipts associated with the receipts

and payments and the amount shall be matched with books of accounts.

Liquidity ratio – it is used for measuring the ability of the entity to pay off the short term

liabilities when it will become due. It has direct impact on the credit rating and credibility of

the entity. Current ratio as well as the quick ratio of the company states whether the current

assets of the company are adequate to meet its short-term obligation. From the ratio

computation table of Perpetual Limited over the periods from 2014 to 2017 it is identified

that the current ratio of the company was in improving trend and reached to 1.78 from 1.64.

However, the quick ratio of the company is reduced from 1.62 to 1.30.

Key assertion involved with the liquidity ratio is completeness that is the amount of

assets and liabilities has been recorded in full without any error. Required audit procedure for

removing this assertion is to check all the transaction associated with the liabilities and assets

and the amount shall be matched with the reported amounts in balance sheet.

Stability ratio – the stability ratios are used to investigate the level of support provided to the

entity through debt and whether the equity and debt are balanced. Debt equity ratio of the

company states the proportion of liabilities as compared to the equity under the capital

structure (Pervan & Kuvek, 2013). On the other hand, debt to asset ratio states the percentage

of debt used by the company purchase its assets. Both the stability ratios of the company are

stating that both the ratios are in improving trend and the debt and equities of the company

are balanced.

Key assertion involved with the stability ratio is valuation that is the amount of assets

and liabilities has been recorded at proper valuations. Required audit procedure for removing

Key assertion involved with the profitability ratio is accuracy that is the amount of

transaction has been recorded in full without any error. Required audit procedure for

removing this assertion is to check all the vouchers and receipts associated with the receipts

and payments and the amount shall be matched with books of accounts.

Liquidity ratio – it is used for measuring the ability of the entity to pay off the short term

liabilities when it will become due. It has direct impact on the credit rating and credibility of

the entity. Current ratio as well as the quick ratio of the company states whether the current

assets of the company are adequate to meet its short-term obligation. From the ratio

computation table of Perpetual Limited over the periods from 2014 to 2017 it is identified

that the current ratio of the company was in improving trend and reached to 1.78 from 1.64.

However, the quick ratio of the company is reduced from 1.62 to 1.30.

Key assertion involved with the liquidity ratio is completeness that is the amount of

assets and liabilities has been recorded in full without any error. Required audit procedure for

removing this assertion is to check all the transaction associated with the liabilities and assets

and the amount shall be matched with the reported amounts in balance sheet.

Stability ratio – the stability ratios are used to investigate the level of support provided to the

entity through debt and whether the equity and debt are balanced. Debt equity ratio of the

company states the proportion of liabilities as compared to the equity under the capital

structure (Pervan & Kuvek, 2013). On the other hand, debt to asset ratio states the percentage

of debt used by the company purchase its assets. Both the stability ratios of the company are

stating that both the ratios are in improving trend and the debt and equities of the company

are balanced.

Key assertion involved with the stability ratio is valuation that is the amount of assets

and liabilities has been recorded at proper valuations. Required audit procedure for removing

8AUDITING AND ETHICS

this assertion is to check all the borrowing related documents and shall be matched with the

amount recorded in balance sheet. Further, the asset amount shall be verified with the asset

register (Lessambo, 2018).

Section 3

Cash flow statement

Looking into the statement of cash flows released by the company for the year ended

30th June 2017 it is found that operating cash flows provided majority of the cash inflows. On

the contrary, cash used for financing led to majority of the cash outflows (Bhandari & Iyer,

2013).

Further, it is observed that proceeds from investment sale amounted to $ 40,925,000

was primary receipts of cash for the company. On the contrary, payment towards dividend

amounted to $ 121,094,000 was primary payments of cash for the company (Chang et al.,

2014).

Non-cash financing expenses was the payment of dividend amounted to $

121,094,000.

On the basis of the company’s financial performance over last 4 years that is from

2014 to 2017 it can be stated that the entity’s profitability ratio improved over the past years.

Further, the stability ratio is indicating that the debt and equity of the company are balanced

(Mock & Fukukawa, 2015). However, to improve the quick ratio is shall pay off the short

term liabilities. Therefore, no major risk regarding going concern is observed in case of

Perpetual Limited.

this assertion is to check all the borrowing related documents and shall be matched with the

amount recorded in balance sheet. Further, the asset amount shall be verified with the asset

register (Lessambo, 2018).

Section 3

Cash flow statement

Looking into the statement of cash flows released by the company for the year ended

30th June 2017 it is found that operating cash flows provided majority of the cash inflows. On

the contrary, cash used for financing led to majority of the cash outflows (Bhandari & Iyer,

2013).

Further, it is observed that proceeds from investment sale amounted to $ 40,925,000

was primary receipts of cash for the company. On the contrary, payment towards dividend

amounted to $ 121,094,000 was primary payments of cash for the company (Chang et al.,

2014).

Non-cash financing expenses was the payment of dividend amounted to $

121,094,000.

On the basis of the company’s financial performance over last 4 years that is from

2014 to 2017 it can be stated that the entity’s profitability ratio improved over the past years.

Further, the stability ratio is indicating that the debt and equity of the company are balanced

(Mock & Fukukawa, 2015). However, to improve the quick ratio is shall pay off the short

term liabilities. Therefore, no major risk regarding going concern is observed in case of

Perpetual Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

Audit report

From the audit report of the company included in the annual report for the year closed

on 30th June 2017 it is observed that the auditor of the company that is KPMG expressed

unqualified opinion. Further, they stated that the financial report has been prepared as per the

requirement of Corporations Regulations 2001 and (AAS) Australian Accounting Standards

(Pucheta‐Martínez & García‐Meca, 2014). However, any additional section has not been

included regarding any audit issue.

Audit report

From the audit report of the company included in the annual report for the year closed

on 30th June 2017 it is observed that the auditor of the company that is KPMG expressed

unqualified opinion. Further, they stated that the financial report has been prepared as per the

requirement of Corporations Regulations 2001 and (AAS) Australian Accounting Standards

(Pucheta‐Martínez & García‐Meca, 2014). However, any additional section has not been

included regarding any audit issue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

Reference

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Bowlin, K. O., Hobson, J. L., & Piercey, M. D. (2015). The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The

Accounting Review, 90(4), 1363-1393.

Chang, X., Dasgupta, S., Wong, G., & Yao, J. (2014). Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), 3628-3657.

Christensen, B. E., Glover, S. M., & Wolfe, C. J. (2014). Do critical audit matter paragraphs

in the audit report change nonprofessional investors' decision to invest?. Auditing: A

Journal of Practice & Theory, 33(4), 71-93.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Kanapickienė, R., & Grundienė, Ž. (2015). The model of fraud detection in financial

statements by means of financial ratios. Procedia-Social and Behavioral

Sciences, 213, 321-327.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

Reference

Bhandari, S. B., & Iyer, R. (2013). Predicting business failure using cash flow statement

based measures. Managerial Finance, 39(7), 667-676.

Bowlin, K. O., Hobson, J. L., & Piercey, M. D. (2015). The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The

Accounting Review, 90(4), 1363-1393.

Chang, X., Dasgupta, S., Wong, G., & Yao, J. (2014). Cash-flow sensitivities and the

allocation of internal cash flow. The Review of Financial Studies, 27(12), 3628-3657.

Christensen, B. E., Glover, S. M., & Wolfe, C. J. (2014). Do critical audit matter paragraphs

in the audit report change nonprofessional investors' decision to invest?. Auditing: A

Journal of Practice & Theory, 33(4), 71-93.

Delen, D., Kuzey, C., & Uyar, A. (2013). Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), 3970-3983.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Johnstone, K., Gramling, A., & Rittenberg, L. E. (2013). Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Kanapickienė, R., & Grundienė, Ž. (2015). The model of fraud detection in financial

statements by means of financial ratios. Procedia-Social and Behavioral

Sciences, 213, 321-327.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

11AUDITING AND ETHICS

Lessambo, F. I. (2018). Audit Risks: Identification and Procedures. In Auditing, Assurance

Services, and Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Mock, T. J., & Fukukawa, H. (2015). Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), 75-84.

Moroney, R., & Trotman, K. T. (2016). Differences in Auditors' Materiality Assessments

When Auditing Financial Statements and Sustainability Reports. Contemporary

Accounting Research, 33(2), 551-575.

Perpetual.com.au. (2018). Investments, superannuation, retirement, & advice | Perpetual.

[online] Retrieved 2 September 2018, from https://www.perpetual.com.au/

Pervan, I., & Kuvek, T. (2013). The relative importance of financial ratios and nonfinancial

variables in predicting of insolvency. Croatian Operational research review, 4(1),

187-197.

Pucheta‐Martínez, M. C., & García‐Meca, E. (2014). Institutional investors on boards and

audit committees and their effects on financial reporting quality. Corporate

Governance: An International Review, 22(4), 347-363.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal

of Practice & Theory, 33(4), 247-269.

Lessambo, F. I. (2018). Audit Risks: Identification and Procedures. In Auditing, Assurance

Services, and Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Mock, T. J., & Fukukawa, H. (2015). Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), 75-84.

Moroney, R., & Trotman, K. T. (2016). Differences in Auditors' Materiality Assessments

When Auditing Financial Statements and Sustainability Reports. Contemporary

Accounting Research, 33(2), 551-575.

Perpetual.com.au. (2018). Investments, superannuation, retirement, & advice | Perpetual.

[online] Retrieved 2 September 2018, from https://www.perpetual.com.au/

Pervan, I., & Kuvek, T. (2013). The relative importance of financial ratios and nonfinancial

variables in predicting of insolvency. Croatian Operational research review, 4(1),

187-197.

Pucheta‐Martínez, M. C., & García‐Meca, E. (2014). Institutional investors on boards and

audit committees and their effects on financial reporting quality. Corporate

Governance: An International Review, 22(4), 347-363.

Ruhnke, K., & Schmidt, M. (2014). Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal

of Practice & Theory, 33(4), 247-269.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.