Auditing and Ethics: Materiality and Audit Procedures for SCG Report

VerifiedAdded on 2022/11/26

|11

|1810

|113

Report

AI Summary

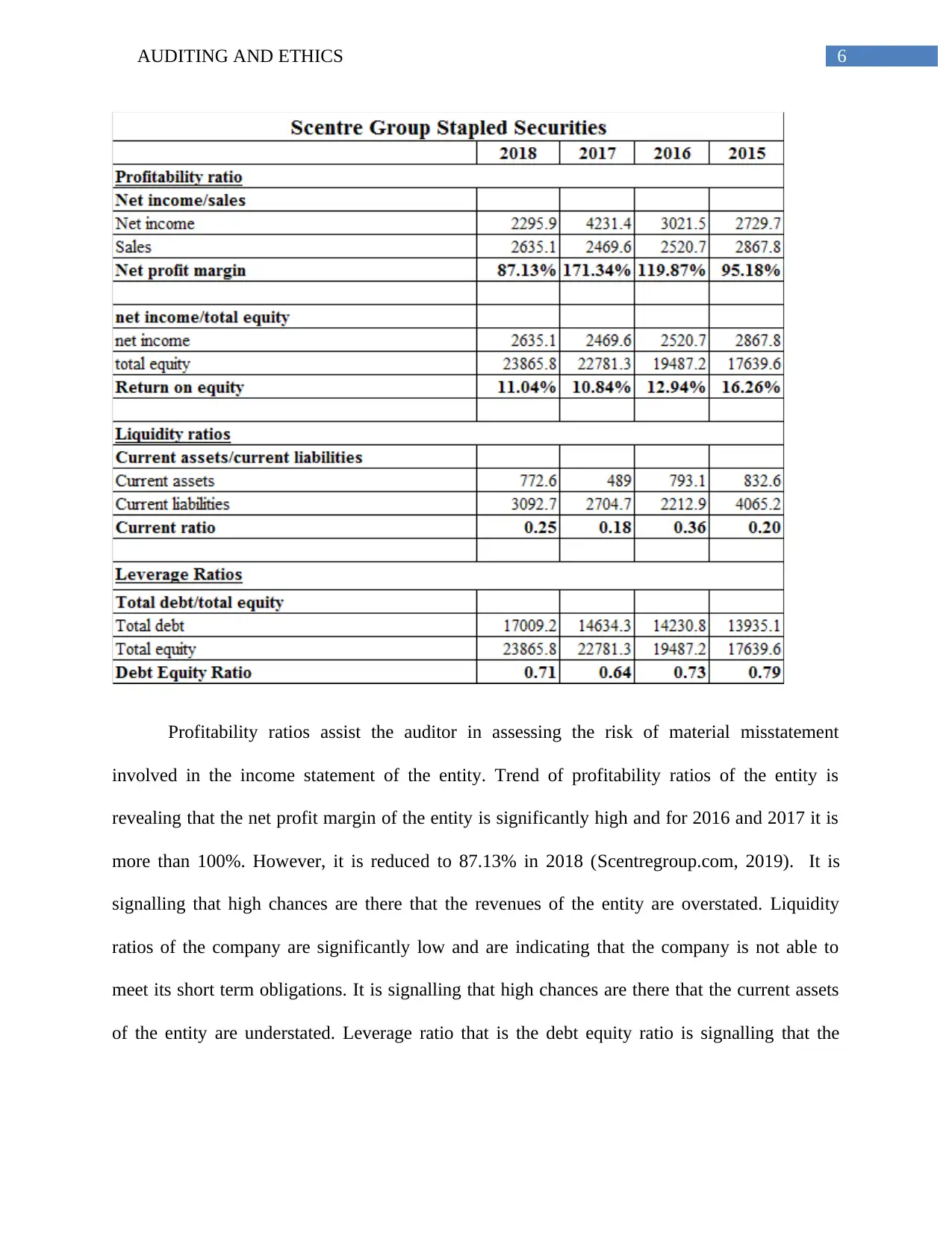

This report examines the auditing and ethics of Scentre Group Stapled Securities (SCG), focusing on materiality, significant audit items, and analytical review procedures. Section 1 defines materiality, discusses its determination based on financial metrics, and calculates tolerable misstatement levels for SCG. It identifies and analyzes significant audit items, including contingent liabilities and the application of AASB 9 for impairment, detailing associated audit procedures. Section 2 employs preliminary analytical review procedures, particularly ratio analysis, to assess financial statement risks. It analyzes SCG's profitability, liquidity, and leverage ratios from 2015 to 2018, identifying key accounts like receivables and revenue for further audit procedures. The report provides audit procedures for key assertions such as existence, classification, accuracy, and cutoff, ensuring a comprehensive evaluation of SCG's financial statements. The report is based on the 2018 annual report of Scentre Group Stapled Securities.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.