Financial Auditing: Addressing the Expectation Gap and Assessing Risks

VerifiedAdded on 2021/09/27

|12

|3580

|159

Report

AI Summary

This report delves into key aspects of financial auditing, beginning with a thorough examination of the audit expectation gap, which is the difference between public perception and the actual scope of a financial audit. It explores methods to narrow this gap, emphasizing the importance of fraud detection through enhanced auditor skills and proactive measures. The report also addresses the critical decisions involved in accepting audit appointments, considering ethical and legal factors such as management pressure, potential conflicts of interest, and compliance with anti-money laundering legislation. Furthermore, it discusses the necessity of sufficient and appropriate audit evidence, highlighting the auditor's judgment in determining adequacy and relevance. The report also analyzes audit risk, focusing on the potential for management to overstate net income to meet lending agreement requirements. Finally, it distinguishes between misstatements arising from fraudulent financial reporting and those resulting from misappropriation of assets, providing a comprehensive overview of the challenges and responsibilities faced by auditors in ensuring the integrity of financial statements.

QUESTION 01

Audit Expectation gap

The audit expectation divides the general public's expectations of the audit with what a

financial audit actually demands. In other cases, this difference is not the result of a failure to

audit but rather the achievements of the auditors' public wishes. There is a difference between

anticipation and reality in either scenario, (Ruhnke & Schmidt, M, 2014, p1 (1))

Approaches to reducing the expectation gap.

These prescriptions are definitely arduous to increase an auditor's ability to detect fraud.

Detection of fraud calls considerable effort and the ability to work together. Capacity is

improved by experience, training and effort. Strong audit planning, brainstorming and skills

boost efforts. All auditors, internally and externally, have the problem of reducing the

expectation gap. While law, regulation and auditing standards have advanced significantly in

this profession, this guidance must be used within its own ranges and the effort expensive and

the ability to narrow this gap, (Salehi, M. 2011, p2(1)).

Uncovering all sorts of fraud cannot be held to account by auditors. It is quite difficult to detect

collusive fraud and other sophisticated methods. However, this does not offer auditors a clear

basis to stop seeking fraud, (Salehi, M. 2011, p2(1)).. Developing the appropriate attitude,

incorporating forensic methods and asking questions about fraud all raise the likelihood of

auditors to uncover it.

Awareness and training of practitioners in public of auditors' obligations and duties •

(external Auditors).

Improve audit standard quality and ongoing audit performance monitoring.

QUESTION 02

Accepting decisions are vital in auditing, because these commitments might represent risks to

objectivity and risk exposure, which should be carefully assessed by the auditing company. Late,

many of the concerns under discussion in the auditing industry are whether the non-audit

service providing for audit clients should be banned outright. In light of a potential new audit

Audit Expectation gap

The audit expectation divides the general public's expectations of the audit with what a

financial audit actually demands. In other cases, this difference is not the result of a failure to

audit but rather the achievements of the auditors' public wishes. There is a difference between

anticipation and reality in either scenario, (Ruhnke & Schmidt, M, 2014, p1 (1))

Approaches to reducing the expectation gap.

These prescriptions are definitely arduous to increase an auditor's ability to detect fraud.

Detection of fraud calls considerable effort and the ability to work together. Capacity is

improved by experience, training and effort. Strong audit planning, brainstorming and skills

boost efforts. All auditors, internally and externally, have the problem of reducing the

expectation gap. While law, regulation and auditing standards have advanced significantly in

this profession, this guidance must be used within its own ranges and the effort expensive and

the ability to narrow this gap, (Salehi, M. 2011, p2(1)).

Uncovering all sorts of fraud cannot be held to account by auditors. It is quite difficult to detect

collusive fraud and other sophisticated methods. However, this does not offer auditors a clear

basis to stop seeking fraud, (Salehi, M. 2011, p2(1)).. Developing the appropriate attitude,

incorporating forensic methods and asking questions about fraud all raise the likelihood of

auditors to uncover it.

Awareness and training of practitioners in public of auditors' obligations and duties •

(external Auditors).

Improve audit standard quality and ongoing audit performance monitoring.

QUESTION 02

Accepting decisions are vital in auditing, because these commitments might represent risks to

objectivity and risk exposure, which should be carefully assessed by the auditing company. Late,

many of the concerns under discussion in the auditing industry are whether the non-audit

service providing for audit clients should be banned outright. In light of a potential new audit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

commitment, the International Standard on Auditing (ISA) criteria require the company to

decide whether preconditions for audits exist. All these factors require careful adoption of

decisions, (Whittington & Pany, 2010, p3 (1)).

In accordance with the Professional Accountants Ethics Code of IFAC, a professional accountant

in public practice shall assess before establishing a new client connection, if acceptance would

threaten the observance of the basic principles. Potential integrity threats or professional

behaviours. Such threats may alert the customer of certain doubtful problems, i.e. its owners,

management or operations, (Whittington & Pany, 2010, p3 (1)). This implies the Company

should look at the potential customer, its owners and its business activity in order to assess

whether doubts about the integrity of the potential customer generate unacceptable risks

when it comes to taking a new customer. These investigation measures are normally carried out

using due diligence methods, also to comply with the legislation on anti-money laundering.

Ethical, legal and other factors to be considered before accepting an audit appointment

Ethical factors

Management Pressure

Public firms may be putting undue stress and pressure on accountants to produce their

accounts and financial statements by the responsibility of success at a high level. For these

accountants, the ethical problem is to preserve honest reporting of the assets, liabilities and

profits of companies without allowing management and corporate managers to exercise any

pressure on them, (Brennan et al, 2007, p3(2)). Unethical accountants can easily change

financial records for companies and maneuver numbers to present deceptive image of

corporate triumphs. Whistleblower's accountant.

A financial accountant may be confronted with the ethical problem that the financial

accountings standard board has detected infringements. Although it is the obligation of an

ethics accountant to disclose these offenses, the repercussions of the reporting present the

difficulty. Government scrutiny of financial records and the bad press of an accounting scandal

might lead to a quick decrease in the company and thousands of employees were dismissed.

decide whether preconditions for audits exist. All these factors require careful adoption of

decisions, (Whittington & Pany, 2010, p3 (1)).

In accordance with the Professional Accountants Ethics Code of IFAC, a professional accountant

in public practice shall assess before establishing a new client connection, if acceptance would

threaten the observance of the basic principles. Potential integrity threats or professional

behaviours. Such threats may alert the customer of certain doubtful problems, i.e. its owners,

management or operations, (Whittington & Pany, 2010, p3 (1)). This implies the Company

should look at the potential customer, its owners and its business activity in order to assess

whether doubts about the integrity of the potential customer generate unacceptable risks

when it comes to taking a new customer. These investigation measures are normally carried out

using due diligence methods, also to comply with the legislation on anti-money laundering.

Ethical, legal and other factors to be considered before accepting an audit appointment

Ethical factors

Management Pressure

Public firms may be putting undue stress and pressure on accountants to produce their

accounts and financial statements by the responsibility of success at a high level. For these

accountants, the ethical problem is to preserve honest reporting of the assets, liabilities and

profits of companies without allowing management and corporate managers to exercise any

pressure on them, (Brennan et al, 2007, p3(2)). Unethical accountants can easily change

financial records for companies and maneuver numbers to present deceptive image of

corporate triumphs. Whistleblower's accountant.

A financial accountant may be confronted with the ethical problem that the financial

accountings standard board has detected infringements. Although it is the obligation of an

ethics accountant to disclose these offenses, the repercussions of the reporting present the

difficulty. Government scrutiny of financial records and the bad press of an accounting scandal

might lead to a quick decrease in the company and thousands of employees were dismissed.

Managers and other business leaders could face criminal prosecution, which might lead to

significant penalties and imprisonment, (Brennan et al, 2007, p3 (2)).

The Greed Effects.

Avidness in the realm of business and finance leads to the removal of ethical limits and

protections to make up more money. An accountant can never let the desire to earn a better

livelihood and gain more wealth prevent her from following the ethical financial reporting

requirements. An accountant who keeps eye on his own bank account more than the balance

sheet of his company becomes responsible to the firm and might lead to actual accounting

infringements, leading to SEC penalties.

Financial records can be issued.

An accountant may be asked by an officer or other executive to hide or exclude specific

financial figures from a budget that could illuminate the business in a negative light for

government and investors, (Brennan et al, 2007, p3 (3)). Omission may not appear to be a

substantial infringement of accounting ethics for an accountant because it does not entail

direct numbers or data manipulation. This is why an accountant must be ethically cautious so

that he does not fall into such a trap.

Legal issues

Financial reporting fraudulent.

Over the last two decades, most accounting scandals have focused on financial reporting fake.

Fraudulent financial reporting is the corporate management's mistake in financial statements.

This is usually done in order to deceive and preserve the share price of the corporation. Whilst

the impacts of false financial reporting may in the short term increase the company's stock

prices, it has nearly always had negative long-term implications. This short-term approach is

sometimes called "myopic management" in company finances, (Krishnan et al, 2011, p2 (3)).

Disclosure.

significant penalties and imprisonment, (Brennan et al, 2007, p3 (2)).

The Greed Effects.

Avidness in the realm of business and finance leads to the removal of ethical limits and

protections to make up more money. An accountant can never let the desire to earn a better

livelihood and gain more wealth prevent her from following the ethical financial reporting

requirements. An accountant who keeps eye on his own bank account more than the balance

sheet of his company becomes responsible to the firm and might lead to actual accounting

infringements, leading to SEC penalties.

Financial records can be issued.

An accountant may be asked by an officer or other executive to hide or exclude specific

financial figures from a budget that could illuminate the business in a negative light for

government and investors, (Brennan et al, 2007, p3 (3)). Omission may not appear to be a

substantial infringement of accounting ethics for an accountant because it does not entail

direct numbers or data manipulation. This is why an accountant must be ethically cautious so

that he does not fall into such a trap.

Legal issues

Financial reporting fraudulent.

Over the last two decades, most accounting scandals have focused on financial reporting fake.

Fraudulent financial reporting is the corporate management's mistake in financial statements.

This is usually done in order to deceive and preserve the share price of the corporation. Whilst

the impacts of false financial reporting may in the short term increase the company's stock

prices, it has nearly always had negative long-term implications. This short-term approach is

sometimes called "myopic management" in company finances, (Krishnan et al, 2011, p2 (3)).

Disclosure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As a sub-topic of falsified financial accounts, breaches of disclosure are ethical faults. While

deliberate recording is not deemed fraudulent financial reporting in line with generally

accepted accounting principles, it could also be considered fraudulent financial reporting unless

investors are able to provide information that would alter their company's investment

decisions. The managers of the company must go ahead and preserve the company's

proprietary information is crucial to the management, (Krishnan et al, 2011, p2 (3)).

Steps that need to be taken prior to the appointment

ISA 210 sets out the prerequisites for an audit. Use by management of an acceptable financial

reporting framework to prepare and consult financial statements and manage as well as for

management at the location of an audit, (Brennan et al, 2007, p3 (3)).This must be done by the

auditor:

The auditor shall examine the suitability of the financial reporting structure while

generating the financial statements.

Evaluation of whether legislation or regulation prescribes the appropriate financial

reporting framework, the financial reporting aim and the type of reporting body. In most

circumstances, the client should merely be confirmed that financial reporting standards

are in place or that the financial statements have an analogous national reporting

structure.

The auditor must also gain management agreement to acknowledge and understand his

responsibilities for the production of financial reporting and internal monitoring

framework, in order to make financial statements prepared without major errors due to

fraud or error.

QUESTION 03

Part a

Sufficient and Appropriate Audit Evidence

deliberate recording is not deemed fraudulent financial reporting in line with generally

accepted accounting principles, it could also be considered fraudulent financial reporting unless

investors are able to provide information that would alter their company's investment

decisions. The managers of the company must go ahead and preserve the company's

proprietary information is crucial to the management, (Krishnan et al, 2011, p2 (3)).

Steps that need to be taken prior to the appointment

ISA 210 sets out the prerequisites for an audit. Use by management of an acceptable financial

reporting framework to prepare and consult financial statements and manage as well as for

management at the location of an audit, (Brennan et al, 2007, p3 (3)).This must be done by the

auditor:

The auditor shall examine the suitability of the financial reporting structure while

generating the financial statements.

Evaluation of whether legislation or regulation prescribes the appropriate financial

reporting framework, the financial reporting aim and the type of reporting body. In most

circumstances, the client should merely be confirmed that financial reporting standards

are in place or that the financial statements have an analogous national reporting

structure.

The auditor must also gain management agreement to acknowledge and understand his

responsibilities for the production of financial reporting and internal monitoring

framework, in order to make financial statements prepared without major errors due to

fraud or error.

QUESTION 03

Part a

Sufficient and Appropriate Audit Evidence

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The word "sufficient" refers to adequate evidence to support the auditor's finding. What is

sufficient at the end of the day relies on the judgment of the auditor, (Florea & Florea, R, 2011,

p2(1)).

The term "evidence adequacy" divides into two main ideas

Audit evidence reliability.

Audit evidence pertinence.

As defined in AS 2315,

In accordance with paragraph 39, the sample items should be selected to be representative of

the population. Thus it should be possible to choose all goods inside the population. Random

selection of things is one way of collecting samples of this kind. Ideally, a selection procedure

should be used that has the capacity to choose things throughout the whole audit period.

If the total misstatement expected is near to the tolerable mistake, the auditor may decide that

the actual population mistakes are unacceptably highly likely to exceed the tolerable mistake.

Conclusion: First of all, sampling chooses by Raymond is almost 60% that cover majority of the

sample part. On the other hand, Actual misstatement is less than tolerable once so we can

conclude it immaterial.

Case 2

The auditor might participate in the inventory. The auditor should also ensure that differences

identified during physical checks are properly addressed and that measures are made in good

time to prevent such events in the future.

Conclusion: Two tiny differences of a single item, which he believed inconsequential, have been

identified by the auditor here. Five small discrepant between the permanent record and the

real amount of data were also detected by the customer. In the current year inventory, these

errors should be addressed.

QUESTION 04

Part a &b

sufficient at the end of the day relies on the judgment of the auditor, (Florea & Florea, R, 2011,

p2(1)).

The term "evidence adequacy" divides into two main ideas

Audit evidence reliability.

Audit evidence pertinence.

As defined in AS 2315,

In accordance with paragraph 39, the sample items should be selected to be representative of

the population. Thus it should be possible to choose all goods inside the population. Random

selection of things is one way of collecting samples of this kind. Ideally, a selection procedure

should be used that has the capacity to choose things throughout the whole audit period.

If the total misstatement expected is near to the tolerable mistake, the auditor may decide that

the actual population mistakes are unacceptably highly likely to exceed the tolerable mistake.

Conclusion: First of all, sampling chooses by Raymond is almost 60% that cover majority of the

sample part. On the other hand, Actual misstatement is less than tolerable once so we can

conclude it immaterial.

Case 2

The auditor might participate in the inventory. The auditor should also ensure that differences

identified during physical checks are properly addressed and that measures are made in good

time to prevent such events in the future.

Conclusion: Two tiny differences of a single item, which he believed inconsequential, have been

identified by the auditor here. Five small discrepant between the permanent record and the

real amount of data were also detected by the customer. In the current year inventory, these

errors should be addressed.

QUESTION 04

Part a &b

Audit Risk

The audit risk is defined as 'When there is a major lack of auditing in the financial statement,

the auditors give an inappropriate audit opinion.' The risk depends on the risk of major errors

and the risk of risk detection.' The risk of significant mistakes is defined as the risk of significant

errors prior to the audit.

The main risk involved in the particular audit would be, the client will try to improve the profit

by hook or crook. Because it is the lending agreement of bank which mandatory to earn profits

and also support from the external sources if the company ceases to earn profit.

By this we can conclude that there will be some behavior by the management to overstate the

net income so that the company would be surviving. And this would be the main risk for the

engagement.

QUESTION 05

Part A

The two forms of financial report failures that may happen as a result of fraud are - mistakes

emerging from falsified financial reports and failures resulting from the misappropriation of

assets, depending on auditing standards mandated, (Yulistyawati et al, 2019, p2(1))

Misstatements arising from fraudulent financial reporting

Intent misrepresentations or omissions in financial statements designed for misleading users of

financial statements in line with non-presented general accounting rules in all significant

respects are misrepresentations resulting from a financial statement (GAAP), (Yulistyawati et al,

2019, p2(2)).

By fake financial reporting, the following can be done:

Manipulation, fabrication or manipulation of accounts or supporting paperwork for

preparing accounts.

Failure or purposeful omission in the financial statements of events, transactions or

other key facts.

The audit risk is defined as 'When there is a major lack of auditing in the financial statement,

the auditors give an inappropriate audit opinion.' The risk depends on the risk of major errors

and the risk of risk detection.' The risk of significant mistakes is defined as the risk of significant

errors prior to the audit.

The main risk involved in the particular audit would be, the client will try to improve the profit

by hook or crook. Because it is the lending agreement of bank which mandatory to earn profits

and also support from the external sources if the company ceases to earn profit.

By this we can conclude that there will be some behavior by the management to overstate the

net income so that the company would be surviving. And this would be the main risk for the

engagement.

QUESTION 05

Part A

The two forms of financial report failures that may happen as a result of fraud are - mistakes

emerging from falsified financial reports and failures resulting from the misappropriation of

assets, depending on auditing standards mandated, (Yulistyawati et al, 2019, p2(1))

Misstatements arising from fraudulent financial reporting

Intent misrepresentations or omissions in financial statements designed for misleading users of

financial statements in line with non-presented general accounting rules in all significant

respects are misrepresentations resulting from a financial statement (GAAP), (Yulistyawati et al,

2019, p2(2)).

By fake financial reporting, the following can be done:

Manipulation, fabrication or manipulation of accounts or supporting paperwork for

preparing accounts.

Failure or purposeful omission in the financial statements of events, transactions or

other key facts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Intentional misuses in amounts, categorization, and forms of submission or disclosure in

accounting standards.

There must not be fraudulent financial reports as a result of a major plan or conspire.

Management officials can simplify the appropriateness of a major mistake, for example as an

aggressive interpretation of complex accounting rules, rather than as the temporary error of

the financial statements, including interim accounts, and then be addressed when improved

operational results,( Dalnial, et al, 2014, p2(1)).

Misstatements arising from misappropriation of assets

Any mismanagement that arises from misappropriation of assets (also called robbery or

defalcation) involves the robbery of the assets of an entity, where the effects of robbery cause

the financial statements in any substantial regard not to be presented in accordance with

GAAP. The misappropriation of assets can be carried out in different manners, including the

misappropriation of revenues, the robbing of assets, or the payment for goods or services not

provided by an institution, (Boumediene, S. L, 2014, p3 (1)). Misappropriation of assets may

involve fake or erroneous records or papers, which may be generated through controlling them.

The scope of this part comprises only the asset misappropriations for which the consequence of

the misappropriation results in an inappropriate presentation, in all material aspects, of the

financial statements according to the GAAP.

Part b

Sr.

No.

Matter Fraud audit risk factor

1 Major bank loans. For objectives other than those for which they were

sanctioned, funds obtained from the bank may be used.

Misuse of loan funds for personal use by directors, etc.

2 Receivable for old

trading accounts.

Fake invoices could have been made to reflect false

receivables in order to increase sales and cover losses.

Increased profits are likely to enhance share values, and

misrepresented financial statements might deceive investors.

accounting standards.

There must not be fraudulent financial reports as a result of a major plan or conspire.

Management officials can simplify the appropriateness of a major mistake, for example as an

aggressive interpretation of complex accounting rules, rather than as the temporary error of

the financial statements, including interim accounts, and then be addressed when improved

operational results,( Dalnial, et al, 2014, p2(1)).

Misstatements arising from misappropriation of assets

Any mismanagement that arises from misappropriation of assets (also called robbery or

defalcation) involves the robbery of the assets of an entity, where the effects of robbery cause

the financial statements in any substantial regard not to be presented in accordance with

GAAP. The misappropriation of assets can be carried out in different manners, including the

misappropriation of revenues, the robbing of assets, or the payment for goods or services not

provided by an institution, (Boumediene, S. L, 2014, p3 (1)). Misappropriation of assets may

involve fake or erroneous records or papers, which may be generated through controlling them.

The scope of this part comprises only the asset misappropriations for which the consequence of

the misappropriation results in an inappropriate presentation, in all material aspects, of the

financial statements according to the GAAP.

Part b

Sr.

No.

Matter Fraud audit risk factor

1 Major bank loans. For objectives other than those for which they were

sanctioned, funds obtained from the bank may be used.

Misuse of loan funds for personal use by directors, etc.

2 Receivable for old

trading accounts.

Fake invoices could have been made to reflect false

receivables in order to increase sales and cover losses.

Increased profits are likely to enhance share values, and

misrepresented financial statements might deceive investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

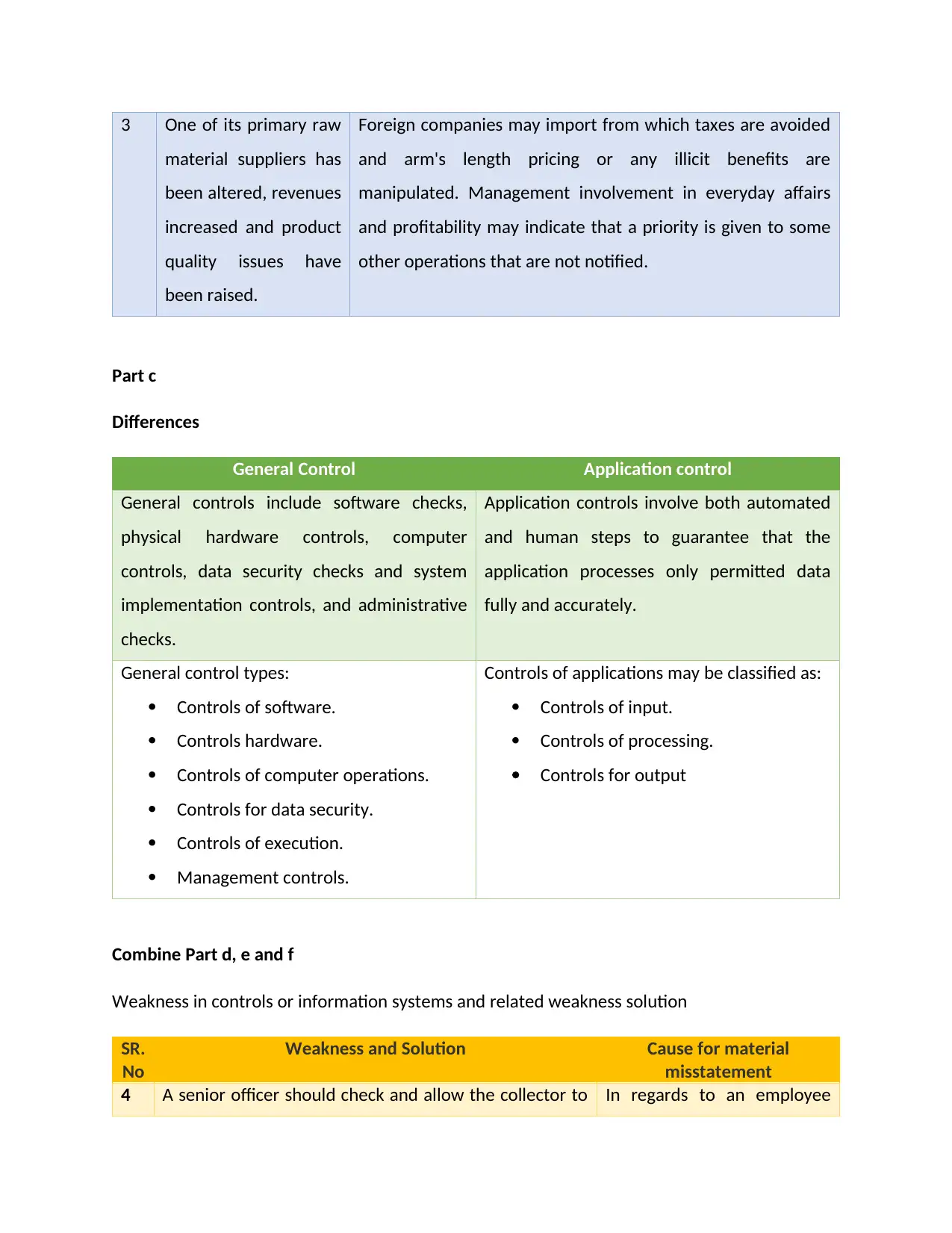

3 One of its primary raw

material suppliers has

been altered, revenues

increased and product

quality issues have

been raised.

Foreign companies may import from which taxes are avoided

and arm's length pricing or any illicit benefits are

manipulated. Management involvement in everyday affairs

and profitability may indicate that a priority is given to some

other operations that are not notified.

Part c

Differences

General Control Application control

General controls include software checks,

physical hardware controls, computer

controls, data security checks and system

implementation controls, and administrative

checks.

Application controls involve both automated

and human steps to guarantee that the

application processes only permitted data

fully and accurately.

General control types:

Controls of software.

Controls hardware.

Controls of computer operations.

Controls for data security.

Controls of execution.

Management controls.

Controls of applications may be classified as:

Controls of input.

Controls of processing.

Controls for output

Combine Part d, e and f

Weakness in controls or information systems and related weakness solution

SR.

No

Weakness and Solution Cause for material

misstatement

4 A senior officer should check and allow the collector to In regards to an employee

material suppliers has

been altered, revenues

increased and product

quality issues have

been raised.

Foreign companies may import from which taxes are avoided

and arm's length pricing or any illicit benefits are

manipulated. Management involvement in everyday affairs

and profitability may indicate that a priority is given to some

other operations that are not notified.

Part c

Differences

General Control Application control

General controls include software checks,

physical hardware controls, computer

controls, data security checks and system

implementation controls, and administrative

checks.

Application controls involve both automated

and human steps to guarantee that the

application processes only permitted data

fully and accurately.

General control types:

Controls of software.

Controls hardware.

Controls of computer operations.

Controls for data security.

Controls of execution.

Management controls.

Controls of applications may be classified as:

Controls of input.

Controls of processing.

Controls for output

Combine Part d, e and f

Weakness in controls or information systems and related weakness solution

SR.

No

Weakness and Solution Cause for material

misstatement

4 A senior officer should check and allow the collector to In regards to an employee

enter information into the payroll system when an

employee is recruited and terminated. This action is not

authorized/approved. The documentation shall be

made by the employee, then authorized by the

supervisor, and the authorization of the staff shall also

be taken for authenticity to accept or terminate

employment

who has gone, the salary

expenses may be over or

below reported. Therefore,

the operational cost and

operating ratio were

improperly assessed.

5 The duties must be separated and the computer

terminal must be controlled properly. In order to enter

data in the system, the factory manager must have a

valid Login Id and password.

Incorrect/high work costs can

be imposed on accounts, and

earnings could be mitigated.

QUESTION 06

a) Three different types of modified opinions are:

Qualified opinion:

The auditor shall express a qualified view where the auditor has obtained adequate audit

evidence or cannot obtain sufficient audit evidence to confirm his view but will, if anything,

conclude that the possible repercussions of undetectable mistakes on the financial statements

are significant but non-pervasive, (Vichitsarawong & Pornupatham, 2015, p2(2)).

Adverse opinions:

The auditor expresses an adverse opinion when the auditor finds that the misconceptions,

either separately or together, are both material and omnipresent, having gathered adequate

audit evidence.

Disclaimer of opinion:

When the auditor is not able to gather adequate audit evidence for their viewpoint, the auditor

will provide a disclosure of opinion but determines that the implications of undetected

employee is recruited and terminated. This action is not

authorized/approved. The documentation shall be

made by the employee, then authorized by the

supervisor, and the authorization of the staff shall also

be taken for authenticity to accept or terminate

employment

who has gone, the salary

expenses may be over or

below reported. Therefore,

the operational cost and

operating ratio were

improperly assessed.

5 The duties must be separated and the computer

terminal must be controlled properly. In order to enter

data in the system, the factory manager must have a

valid Login Id and password.

Incorrect/high work costs can

be imposed on accounts, and

earnings could be mitigated.

QUESTION 06

a) Three different types of modified opinions are:

Qualified opinion:

The auditor shall express a qualified view where the auditor has obtained adequate audit

evidence or cannot obtain sufficient audit evidence to confirm his view but will, if anything,

conclude that the possible repercussions of undetectable mistakes on the financial statements

are significant but non-pervasive, (Vichitsarawong & Pornupatham, 2015, p2(2)).

Adverse opinions:

The auditor expresses an adverse opinion when the auditor finds that the misconceptions,

either separately or together, are both material and omnipresent, having gathered adequate

audit evidence.

Disclaimer of opinion:

When the auditor is not able to gather adequate audit evidence for their viewpoint, the auditor

will provide a disclosure of opinion but determines that the implications of undetected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

mistakes can be significant and general to the financial statements, (Vichitsarawong &

Pornupatham, 2015, p2(2)).

Since the note provided in the financial report completely corresponds with the accounts and

the Company regularly makes the other party's payments, it will not only be a modified opinion

for the note offered to bring the attention of the User.

b). Effects on Audit opinion for the matters raised during the audit work

Inventory Valuation:

In the next month, the company sold 25% of the inventories at a lower cost. In accordance with

the requirements set by the separate boards of directors of different countries, the company is

expected to evaluate Net Realizable Value in cases where such a situation exists in the

succeeding period. This issue will play a crucial part in the audit opinion, (Simamora &

Hendarjatno, 2019, p2 (1))

Payable trade Valuation:

The company has indicated no buying value $53,751, which is not displayed in the funds that is

the omission of a transaction that can directly affect the finances that can make the finances

untrustworthy. This will play a crucial part in the formulation of an audit opinion.

Trade receivables Valuation:

By considering the false exchange rates that directly affect financial activities and may boost the

profits of the company, the company overestimated trade receivables of $75,650, (Simamora &

Hendarjatno, 2019, p2 (2)).

Part c

When taken together, those matters make the funds inaccurate and untrustworthy for

the stakeholders.

What he believes to be prevalent or not, relies on the auditors' professional judgment.

No doubt the issues directly affect the financial accounts, however it depends on the

professional judgment that these difficulties prevail.

Pornupatham, 2015, p2(2)).

Since the note provided in the financial report completely corresponds with the accounts and

the Company regularly makes the other party's payments, it will not only be a modified opinion

for the note offered to bring the attention of the User.

b). Effects on Audit opinion for the matters raised during the audit work

Inventory Valuation:

In the next month, the company sold 25% of the inventories at a lower cost. In accordance with

the requirements set by the separate boards of directors of different countries, the company is

expected to evaluate Net Realizable Value in cases where such a situation exists in the

succeeding period. This issue will play a crucial part in the audit opinion, (Simamora &

Hendarjatno, 2019, p2 (1))

Payable trade Valuation:

The company has indicated no buying value $53,751, which is not displayed in the funds that is

the omission of a transaction that can directly affect the finances that can make the finances

untrustworthy. This will play a crucial part in the formulation of an audit opinion.

Trade receivables Valuation:

By considering the false exchange rates that directly affect financial activities and may boost the

profits of the company, the company overestimated trade receivables of $75,650, (Simamora &

Hendarjatno, 2019, p2 (2)).

Part c

When taken together, those matters make the funds inaccurate and untrustworthy for

the stakeholders.

What he believes to be prevalent or not, relies on the auditors' professional judgment.

No doubt the issues directly affect the financial accounts, however it depends on the

professional judgment that these difficulties prevail.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If the auditor determines that the issues in general are overwhelming, the auditor shall

issue a dissenting opinion.

Qualified views will be issued otherwise.

References

Ruhnke, K., & Schmidt, M. (2014). The audit expectation gap: existence, causes, and the impact

of changes. Accounting and business research, 44(5), 572-601.

https://www.tandfonline.com/doi/abs/10.1080/00014788.2014.929519.

Salehi, M. (2011). Audit expectation gap: Concept, nature and trace. African Journal of Business

Management, 5(21), 8376-8392.

https://academicjournals.org/journal/AJBM/article-abstract/4C4AA7018778.

Whittington, R., & Pany, K. (2010). Principles of auditing and other assurance services.

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.453.1524&rep=rep1&type=pdf.

Brennan, N., & Kelly, J. (2007). A study of whistleblowing among trainee auditors. The British

Accounting Review, 39(1), 61-87.

https://www.sciencedirect.com/science/article/pii/S0890838906001260.

Krishnan, J., Wen, Y., & Zhao, W. (2011). Legal expertise on corporate audit committees and

financial reporting quality. The Accounting Review, 86(6), 2099-2130.

https://meridian.allenpress.com/accounting-review/article-abstract/86/6/2099/53841.

issue a dissenting opinion.

Qualified views will be issued otherwise.

References

Ruhnke, K., & Schmidt, M. (2014). The audit expectation gap: existence, causes, and the impact

of changes. Accounting and business research, 44(5), 572-601.

https://www.tandfonline.com/doi/abs/10.1080/00014788.2014.929519.

Salehi, M. (2011). Audit expectation gap: Concept, nature and trace. African Journal of Business

Management, 5(21), 8376-8392.

https://academicjournals.org/journal/AJBM/article-abstract/4C4AA7018778.

Whittington, R., & Pany, K. (2010). Principles of auditing and other assurance services.

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.453.1524&rep=rep1&type=pdf.

Brennan, N., & Kelly, J. (2007). A study of whistleblowing among trainee auditors. The British

Accounting Review, 39(1), 61-87.

https://www.sciencedirect.com/science/article/pii/S0890838906001260.

Krishnan, J., Wen, Y., & Zhao, W. (2011). Legal expertise on corporate audit committees and

financial reporting quality. The Accounting Review, 86(6), 2099-2130.

https://meridian.allenpress.com/accounting-review/article-abstract/86/6/2099/53841.

Florea, R., & Florea, R. (2011). Audit techniques and audit evidence. Economy

Transdisciplinarity Cognition, 14(1), 350.

http://www.ugb.ro/etc/etc2011no1/FIN-12-full.pdf.

Yulistyawati, N. K. A., Suardikha, I. M. S., & Sudana, I. P. (2019). The analysis of the factor that

causes fraudulent financial reporting with fraud diamond. Jurnal Akuntansi dan Auditing

Indonesia, 23(1), 1-10.

https://journal.uii.ac.id/JAAI/article/view/10834.

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science, 2(1).

http://www.joams.com/uploadfile/2013/1225/20131225035355373.pdf.

Boumediene, S. L. (2014, January). Detection and prediction of managerial fraud in the financial

statements of Tunisian banks. In Global Conference on Business and Finance Proceedings (Vol.

9, No. 1, pp. 421-426).

https://www.researchgate.net/profile/Cristobal_Fernandez/publication/

260364142_TURISMO_DE_INTERESES_ESPECIALES_INVESTIGACION_DE_MERCADO_SOBRE_LA

S_MOTIVACIONES_DESDE_LA_PERSPECTIVA_DEL_CLIENTE/links/

02e7e530e390390694000000/TURISMO-DE-INTERESES-ESPECIALES-INVESTIGACION-DE-

MERCADO-SOBRE-LAS-MOTIVACIONES-DESDE-LA-PERSPECTIVA-DEL-CLIENTE.pdf#page=444.

Vichitsarawong, T., & Pornupatham, S. (2015). Do audit opinions reflect earnings persistence?.

Managerial Auditing Journal.

https://www.emerald.com/insight/content/doi/10.1108/MAJ-12-2013-0973/full/html.

Simamora, R. A., & Hendarjatno, H. (2019). The effects of audit client tenure, audit lag, opinion

shopping, liquidity ratio, and leverage to the going concern audit opinion. Asian Journal of

Accounting Research.

Transdisciplinarity Cognition, 14(1), 350.

http://www.ugb.ro/etc/etc2011no1/FIN-12-full.pdf.

Yulistyawati, N. K. A., Suardikha, I. M. S., & Sudana, I. P. (2019). The analysis of the factor that

causes fraudulent financial reporting with fraud diamond. Jurnal Akuntansi dan Auditing

Indonesia, 23(1), 1-10.

https://journal.uii.ac.id/JAAI/article/view/10834.

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science, 2(1).

http://www.joams.com/uploadfile/2013/1225/20131225035355373.pdf.

Boumediene, S. L. (2014, January). Detection and prediction of managerial fraud in the financial

statements of Tunisian banks. In Global Conference on Business and Finance Proceedings (Vol.

9, No. 1, pp. 421-426).

https://www.researchgate.net/profile/Cristobal_Fernandez/publication/

260364142_TURISMO_DE_INTERESES_ESPECIALES_INVESTIGACION_DE_MERCADO_SOBRE_LA

S_MOTIVACIONES_DESDE_LA_PERSPECTIVA_DEL_CLIENTE/links/

02e7e530e390390694000000/TURISMO-DE-INTERESES-ESPECIALES-INVESTIGACION-DE-

MERCADO-SOBRE-LAS-MOTIVACIONES-DESDE-LA-PERSPECTIVA-DEL-CLIENTE.pdf#page=444.

Vichitsarawong, T., & Pornupatham, S. (2015). Do audit opinions reflect earnings persistence?.

Managerial Auditing Journal.

https://www.emerald.com/insight/content/doi/10.1108/MAJ-12-2013-0973/full/html.

Simamora, R. A., & Hendarjatno, H. (2019). The effects of audit client tenure, audit lag, opinion

shopping, liquidity ratio, and leverage to the going concern audit opinion. Asian Journal of

Accounting Research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.