Auditing Project: Comprehensive Financial Auditing of ZIP TEL Company

VerifiedAdded on 2020/12/09

|17

|4860

|153

Report

AI Summary

This auditing project report analyzes the financial position of ZIP TEL, a telecommunication company. It begins by identifying key business risks, including market, liquidity, and credit risks, and then assesses the company's financial performance through ratio and trend analysis over three years (2014-2016). The project calculates materiality for planning purposes and selects ten account balances to design comprehensive audit work steps, including assertions, audit procedures, and evidence. The report includes detailed analysis of profitability, liquidity, activity, and solvency ratios, along with a sampling plan for testing material account balances like cash at bank and trade receivables. The analysis reveals negative trends in profitability and concerning shifts in equity and debt levels, offering insights into the company's financial health and the effectiveness of its risk management strategies.

AUDITING PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Selecting ASX listed company ..........................................................................................1

2. Understanding of the nature of the entity in particular industry and identifying key business

risks.........................................................................................................................................1

3. Performing analytical procedures of financial statements of using ratio analysis and trend

analysis over the past three years...........................................................................................3

4. Explaining material account balances and calculated materiality for planning purposes and

justification.............................................................................................................................6

5., 6., 7. 8. Selecting ten account balances, listing assertions for items and designing

comprehensive set of audit work steps for material account balances with appropriate

evidence. Including sampling plan for testing each item of material account balances ........7

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

1. Selecting ASX listed company ..........................................................................................1

2. Understanding of the nature of the entity in particular industry and identifying key business

risks.........................................................................................................................................1

3. Performing analytical procedures of financial statements of using ratio analysis and trend

analysis over the past three years...........................................................................................3

4. Explaining material account balances and calculated materiality for planning purposes and

justification.............................................................................................................................6

5., 6., 7. 8. Selecting ten account balances, listing assertions for items and designing

comprehensive set of audit work steps for material account balances with appropriate

evidence. Including sampling plan for testing each item of material account balances ........7

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

INTRODUCTION

Auditing means to analyse the financial position of an organisation through systematic

and independence examination of books of account of business. This is carried out to check the

authenticity and determination of any misrepresentation or misstatement of any transaction in

financial record of firm. In the present report auditing of listed telecommunication company ZIP

TEL is conducted. In this report key business risk related with the firm are anticipated and factor

effecting both inherent and control risk are discussed. For determination of financial

performance of business ratio analysis is carried out. Material information from the financial

record and accounts are found out and their relevancy with organisational performance is

presented.

1. Selecting ASX listed company

2. Understanding of the nature of the entity in particular industry and identifying key business

risks.

ZipTel Ltd is engaged in telecommunication sector which is the highest revenue

generating one for Australian economy leading to growth of overall nation in the best possible

manner. The nature of business entity is that it provides mobile SIM cards and internet data

services which help to attain profits. It can be interpreted from the financial reports that from last

three years ie 2014, 2015 and 2016, organisation is not able to earn profits and huge losses are

suffered. The key business risks are market risk, liquidity risk and credit risks. Risk management

program has been implemented in order to focus on unpredictability of financial markets and to

minimise these threats. However, derivatives are not being used by company.

Market risk is based on Foreign Exchange risk and cash flow and fair value interest rate

risks. ZipTel Ltd has short-term nature of cash and cash equivalents (CCE) bearing interest rates.

It can be analysed that due to its nature, interest rates are not vital at this time and risk is low.

Credit risk is termed as a type of risk where counter party will default on making its payments to

company and substantial loss will occur (Jespersen and Hasle, 2017). Liquidity risk on the part

of company are low as counterparties are banks having high credit risks and as such, risk is low.

3. Performing analytical procedures of financial statements of using ratio analysis and trend

analysis over the past three years

1

Auditing means to analyse the financial position of an organisation through systematic

and independence examination of books of account of business. This is carried out to check the

authenticity and determination of any misrepresentation or misstatement of any transaction in

financial record of firm. In the present report auditing of listed telecommunication company ZIP

TEL is conducted. In this report key business risk related with the firm are anticipated and factor

effecting both inherent and control risk are discussed. For determination of financial

performance of business ratio analysis is carried out. Material information from the financial

record and accounts are found out and their relevancy with organisational performance is

presented.

1. Selecting ASX listed company

2. Understanding of the nature of the entity in particular industry and identifying key business

risks.

ZipTel Ltd is engaged in telecommunication sector which is the highest revenue

generating one for Australian economy leading to growth of overall nation in the best possible

manner. The nature of business entity is that it provides mobile SIM cards and internet data

services which help to attain profits. It can be interpreted from the financial reports that from last

three years ie 2014, 2015 and 2016, organisation is not able to earn profits and huge losses are

suffered. The key business risks are market risk, liquidity risk and credit risks. Risk management

program has been implemented in order to focus on unpredictability of financial markets and to

minimise these threats. However, derivatives are not being used by company.

Market risk is based on Foreign Exchange risk and cash flow and fair value interest rate

risks. ZipTel Ltd has short-term nature of cash and cash equivalents (CCE) bearing interest rates.

It can be analysed that due to its nature, interest rates are not vital at this time and risk is low.

Credit risk is termed as a type of risk where counter party will default on making its payments to

company and substantial loss will occur (Jespersen and Hasle, 2017). Liquidity risk on the part

of company are low as counterparties are banks having high credit risks and as such, risk is low.

3. Performing analytical procedures of financial statements of using ratio analysis and trend

analysis over the past three years

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

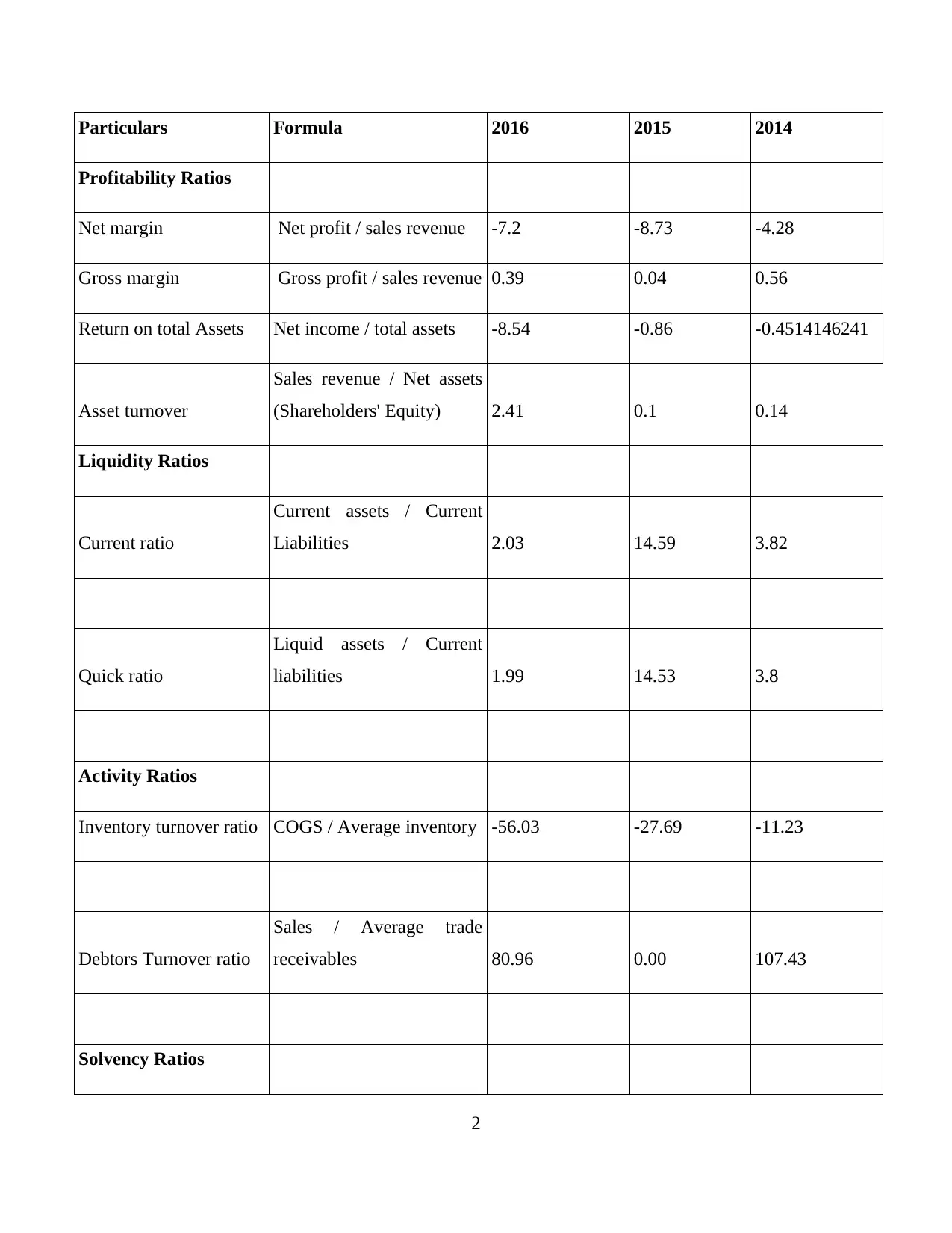

Particulars Formula 2016 2015 2014

Profitability Ratios

Net margin Net profit / sales revenue -7.2 -8.73 -4.28

Gross margin Gross profit / sales revenue 0.39 0.04 0.56

Return on total Assets Net income / total assets -8.54 -0.86 -0.4514146241

Asset turnover

Sales revenue / Net assets

(Shareholders' Equity) 2.41 0.1 0.14

Liquidity Ratios

Current ratio

Current assets / Current

Liabilities 2.03 14.59 3.82

Quick ratio

Liquid assets / Current

liabilities 1.99 14.53 3.8

Activity Ratios

Inventory turnover ratio COGS / Average inventory -56.03 -27.69 -11.23

Debtors Turnover ratio

Sales / Average trade

receivables 80.96 0.00 107.43

Solvency Ratios

2

Profitability Ratios

Net margin Net profit / sales revenue -7.2 -8.73 -4.28

Gross margin Gross profit / sales revenue 0.39 0.04 0.56

Return on total Assets Net income / total assets -8.54 -0.86 -0.4514146241

Asset turnover

Sales revenue / Net assets

(Shareholders' Equity) 2.41 0.1 0.14

Liquidity Ratios

Current ratio

Current assets / Current

Liabilities 2.03 14.59 3.82

Quick ratio

Liquid assets / Current

liabilities 1.99 14.53 3.8

Activity Ratios

Inventory turnover ratio COGS / Average inventory -56.03 -27.69 -11.23

Debtors Turnover ratio

Sales / Average trade

receivables 80.96 0.00 107.43

Solvency Ratios

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

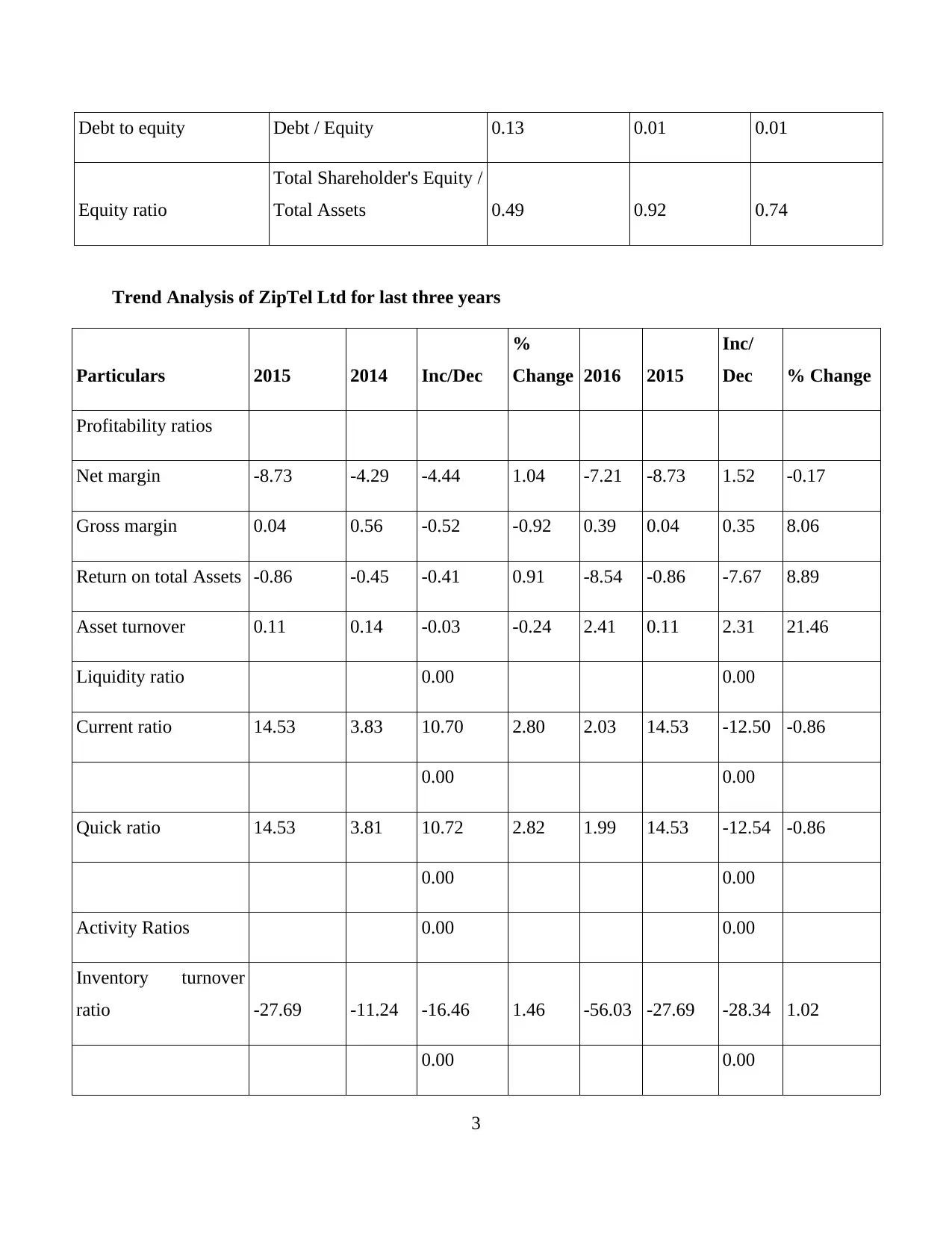

Debt to equity Debt / Equity 0.13 0.01 0.01

Equity ratio

Total Shareholder's Equity /

Total Assets 0.49 0.92 0.74

Trend Analysis of ZipTel Ltd for last three years

Particulars 2015 2014 Inc/Dec

%

Change 2016 2015

Inc/

Dec % Change

Profitability ratios

Net margin -8.73 -4.29 -4.44 1.04 -7.21 -8.73 1.52 -0.17

Gross margin 0.04 0.56 -0.52 -0.92 0.39 0.04 0.35 8.06

Return on total Assets -0.86 -0.45 -0.41 0.91 -8.54 -0.86 -7.67 8.89

Asset turnover 0.11 0.14 -0.03 -0.24 2.41 0.11 2.31 21.46

Liquidity ratio 0.00 0.00

Current ratio 14.53 3.83 10.70 2.80 2.03 14.53 -12.50 -0.86

0.00 0.00

Quick ratio 14.53 3.81 10.72 2.82 1.99 14.53 -12.54 -0.86

0.00 0.00

Activity Ratios 0.00 0.00

Inventory turnover

ratio -27.69 -11.24 -16.46 1.46 -56.03 -27.69 -28.34 1.02

0.00 0.00

3

Equity ratio

Total Shareholder's Equity /

Total Assets 0.49 0.92 0.74

Trend Analysis of ZipTel Ltd for last three years

Particulars 2015 2014 Inc/Dec

%

Change 2016 2015

Inc/

Dec % Change

Profitability ratios

Net margin -8.73 -4.29 -4.44 1.04 -7.21 -8.73 1.52 -0.17

Gross margin 0.04 0.56 -0.52 -0.92 0.39 0.04 0.35 8.06

Return on total Assets -0.86 -0.45 -0.41 0.91 -8.54 -0.86 -7.67 8.89

Asset turnover 0.11 0.14 -0.03 -0.24 2.41 0.11 2.31 21.46

Liquidity ratio 0.00 0.00

Current ratio 14.53 3.83 10.70 2.80 2.03 14.53 -12.50 -0.86

0.00 0.00

Quick ratio 14.53 3.81 10.72 2.82 1.99 14.53 -12.54 -0.86

0.00 0.00

Activity Ratios 0.00 0.00

Inventory turnover

ratio -27.69 -11.24 -16.46 1.46 -56.03 -27.69 -28.34 1.02

0.00 0.00

3

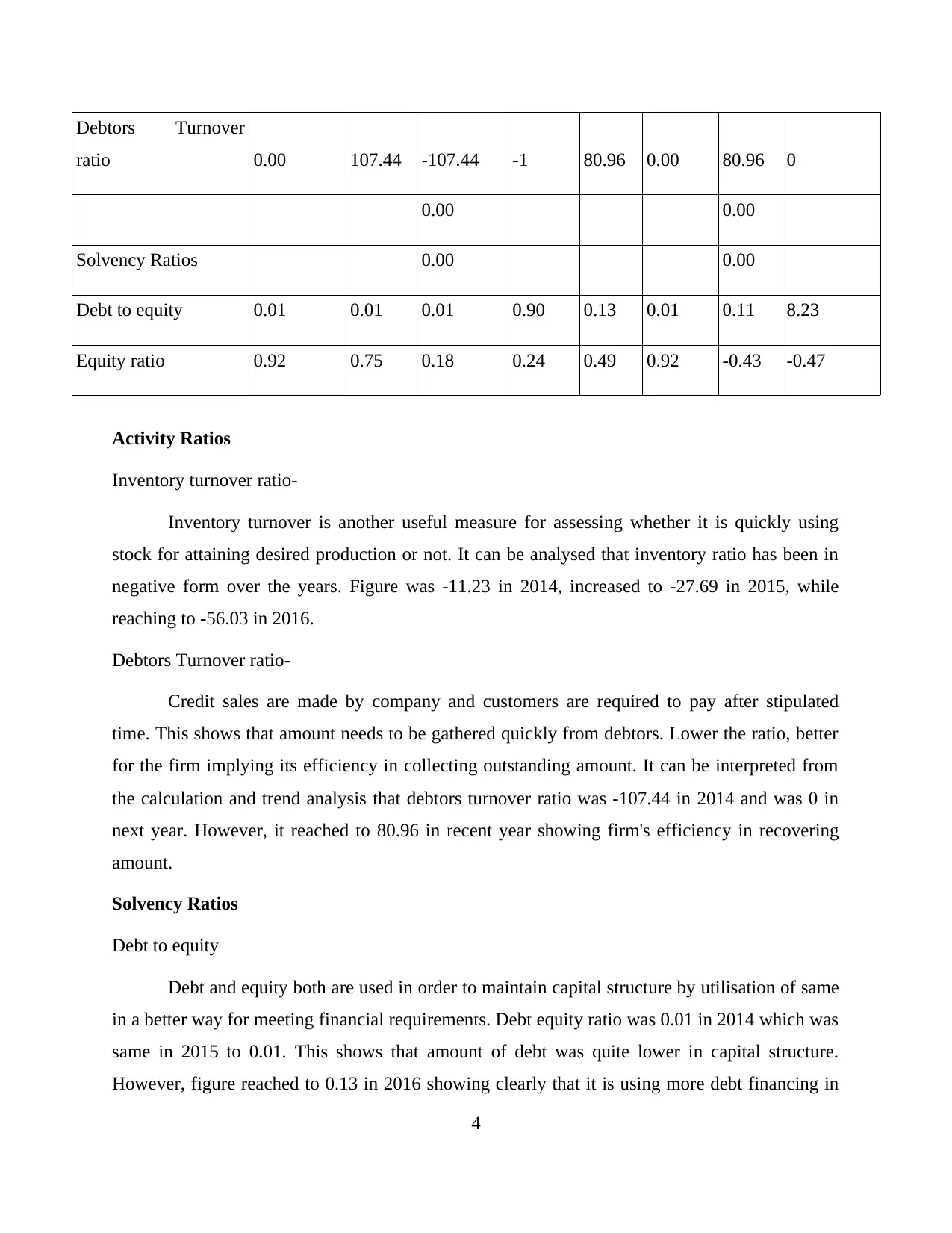

Debtors Turnover

ratio 0.00 107.44 -107.44 -1 80.96 0.00 80.96 0

0.00 0.00

Solvency Ratios 0.00 0.00

Debt to equity 0.01 0.01 0.01 0.90 0.13 0.01 0.11 8.23

Equity ratio 0.92 0.75 0.18 0.24 0.49 0.92 -0.43 -0.47

Activity Ratios

Inventory turnover ratio-

Inventory turnover is another useful measure for assessing whether it is quickly using

stock for attaining desired production or not. It can be analysed that inventory ratio has been in

negative form over the years. Figure was -11.23 in 2014, increased to -27.69 in 2015, while

reaching to -56.03 in 2016.

Debtors Turnover ratio-

Credit sales are made by company and customers are required to pay after stipulated

time. This shows that amount needs to be gathered quickly from debtors. Lower the ratio, better

for the firm implying its efficiency in collecting outstanding amount. It can be interpreted from

the calculation and trend analysis that debtors turnover ratio was -107.44 in 2014 and was 0 in

next year. However, it reached to 80.96 in recent year showing firm's efficiency in recovering

amount.

Solvency Ratios

Debt to equity

Debt and equity both are used in order to maintain capital structure by utilisation of same

in a better way for meeting financial requirements. Debt equity ratio was 0.01 in 2014 which was

same in 2015 to 0.01. This shows that amount of debt was quite lower in capital structure.

However, figure reached to 0.13 in 2016 showing clearly that it is using more debt financing in

4

ratio 0.00 107.44 -107.44 -1 80.96 0.00 80.96 0

0.00 0.00

Solvency Ratios 0.00 0.00

Debt to equity 0.01 0.01 0.01 0.90 0.13 0.01 0.11 8.23

Equity ratio 0.92 0.75 0.18 0.24 0.49 0.92 -0.43 -0.47

Activity Ratios

Inventory turnover ratio-

Inventory turnover is another useful measure for assessing whether it is quickly using

stock for attaining desired production or not. It can be analysed that inventory ratio has been in

negative form over the years. Figure was -11.23 in 2014, increased to -27.69 in 2015, while

reaching to -56.03 in 2016.

Debtors Turnover ratio-

Credit sales are made by company and customers are required to pay after stipulated

time. This shows that amount needs to be gathered quickly from debtors. Lower the ratio, better

for the firm implying its efficiency in collecting outstanding amount. It can be interpreted from

the calculation and trend analysis that debtors turnover ratio was -107.44 in 2014 and was 0 in

next year. However, it reached to 80.96 in recent year showing firm's efficiency in recovering

amount.

Solvency Ratios

Debt to equity

Debt and equity both are used in order to maintain capital structure by utilisation of same

in a better way for meeting financial requirements. Debt equity ratio was 0.01 in 2014 which was

same in 2015 to 0.01. This shows that amount of debt was quite lower in capital structure.

However, figure reached to 0.13 in 2016 showing clearly that it is using more debt financing in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

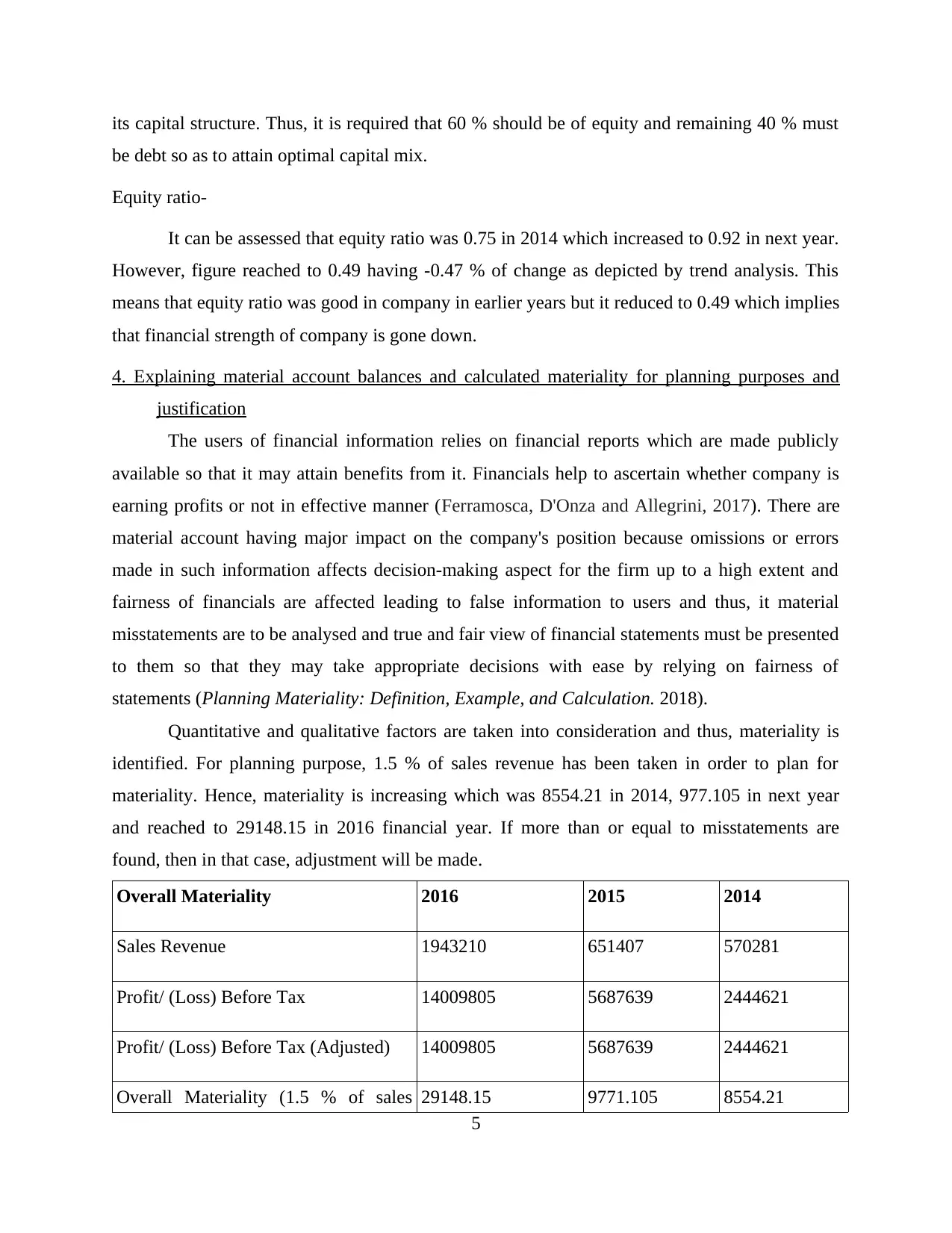

its capital structure. Thus, it is required that 60 % should be of equity and remaining 40 % must

be debt so as to attain optimal capital mix.

Equity ratio-

It can be assessed that equity ratio was 0.75 in 2014 which increased to 0.92 in next year.

However, figure reached to 0.49 having -0.47 % of change as depicted by trend analysis. This

means that equity ratio was good in company in earlier years but it reduced to 0.49 which implies

that financial strength of company is gone down.

4. Explaining material account balances and calculated materiality for planning purposes and

justification

The users of financial information relies on financial reports which are made publicly

available so that it may attain benefits from it. Financials help to ascertain whether company is

earning profits or not in effective manner (Ferramosca, D'Onza and Allegrini, 2017). There are

material account having major impact on the company's position because omissions or errors

made in such information affects decision-making aspect for the firm up to a high extent and

fairness of financials are affected leading to false information to users and thus, it material

misstatements are to be analysed and true and fair view of financial statements must be presented

to them so that they may take appropriate decisions with ease by relying on fairness of

statements (Planning Materiality: Definition, Example, and Calculation. 2018).

Quantitative and qualitative factors are taken into consideration and thus, materiality is

identified. For planning purpose, 1.5 % of sales revenue has been taken in order to plan for

materiality. Hence, materiality is increasing which was 8554.21 in 2014, 977.105 in next year

and reached to 29148.15 in 2016 financial year. If more than or equal to misstatements are

found, then in that case, adjustment will be made.

Overall Materiality 2016 2015 2014

Sales Revenue 1943210 651407 570281

Profit/ (Loss) Before Tax 14009805 5687639 2444621

Profit/ (Loss) Before Tax (Adjusted) 14009805 5687639 2444621

Overall Materiality (1.5 % of sales 29148.15 9771.105 8554.21

5

be debt so as to attain optimal capital mix.

Equity ratio-

It can be assessed that equity ratio was 0.75 in 2014 which increased to 0.92 in next year.

However, figure reached to 0.49 having -0.47 % of change as depicted by trend analysis. This

means that equity ratio was good in company in earlier years but it reduced to 0.49 which implies

that financial strength of company is gone down.

4. Explaining material account balances and calculated materiality for planning purposes and

justification

The users of financial information relies on financial reports which are made publicly

available so that it may attain benefits from it. Financials help to ascertain whether company is

earning profits or not in effective manner (Ferramosca, D'Onza and Allegrini, 2017). There are

material account having major impact on the company's position because omissions or errors

made in such information affects decision-making aspect for the firm up to a high extent and

fairness of financials are affected leading to false information to users and thus, it material

misstatements are to be analysed and true and fair view of financial statements must be presented

to them so that they may take appropriate decisions with ease by relying on fairness of

statements (Planning Materiality: Definition, Example, and Calculation. 2018).

Quantitative and qualitative factors are taken into consideration and thus, materiality is

identified. For planning purpose, 1.5 % of sales revenue has been taken in order to plan for

materiality. Hence, materiality is increasing which was 8554.21 in 2014, 977.105 in next year

and reached to 29148.15 in 2016 financial year. If more than or equal to misstatements are

found, then in that case, adjustment will be made.

Overall Materiality 2016 2015 2014

Sales Revenue 1943210 651407 570281

Profit/ (Loss) Before Tax 14009805 5687639 2444621

Profit/ (Loss) Before Tax (Adjusted) 14009805 5687639 2444621

Overall Materiality (1.5 % of sales 29148.15 9771.105 8554.21

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

revenue)

5., 6., 7. 8. Selecting ten account balances, listing assertions for items and designing

comprehensive set of audit work steps for material account balances with appropriate

evidence. Including sampling plan for testing each item of material account balances

Account Balance Amount

Assertion

(s) Audit Procedures Audit Evidence

1. Cash at Bank

ZipTel.

$AUD

1353070

Existence,

Completenes

s, Accuracy,

Rights and

Obligations,

Valuation

and

Allocation

1. Requested and

examined bank

confirmations

2. Undertake tests

of bank

reconciliation,

follow-up

reconciling items.

Bank Confirmation certificate from

the Bank (Document).

Obtain copies of client’s bank

reconciliation (Document).

Enquiry and notes of reconciling

item (oral)

Assertion -

Existence

It determines that, all the proof of cash to ascertain various recorded receipts which

were have to be deposited in the bank account of ZipTel. Therefore, this dual

confirmation is quite necessary for organisation in making appropriate determination

of all operation (Shilts, 2017).

Assertion -

Completeness

It consists of cross checking data base with number of transactions and amount are

listed in each account. Thus, bank statement is examined with the BRS of ZipTel.

Outstanding amount had been overstated in the cash balance of organisation.

Assertion -

Accuracy

To analyse the accuracy or reliability of details on which bank account of a concern

has been considered to analysed the past records as well as matching the current

position with it. Along with this, it also ensures the preparation of Bank reconciliation

6

5., 6., 7. 8. Selecting ten account balances, listing assertions for items and designing

comprehensive set of audit work steps for material account balances with appropriate

evidence. Including sampling plan for testing each item of material account balances

Account Balance Amount

Assertion

(s) Audit Procedures Audit Evidence

1. Cash at Bank

ZipTel.

$AUD

1353070

Existence,

Completenes

s, Accuracy,

Rights and

Obligations,

Valuation

and

Allocation

1. Requested and

examined bank

confirmations

2. Undertake tests

of bank

reconciliation,

follow-up

reconciling items.

Bank Confirmation certificate from

the Bank (Document).

Obtain copies of client’s bank

reconciliation (Document).

Enquiry and notes of reconciling

item (oral)

Assertion -

Existence

It determines that, all the proof of cash to ascertain various recorded receipts which

were have to be deposited in the bank account of ZipTel. Therefore, this dual

confirmation is quite necessary for organisation in making appropriate determination

of all operation (Shilts, 2017).

Assertion -

Completeness

It consists of cross checking data base with number of transactions and amount are

listed in each account. Thus, bank statement is examined with the BRS of ZipTel.

Outstanding amount had been overstated in the cash balance of organisation.

Assertion -

Accuracy

To analyse the accuracy or reliability of details on which bank account of a concern

has been considered to analysed the past records as well as matching the current

position with it. Along with this, it also ensures the preparation of Bank reconciliation

6

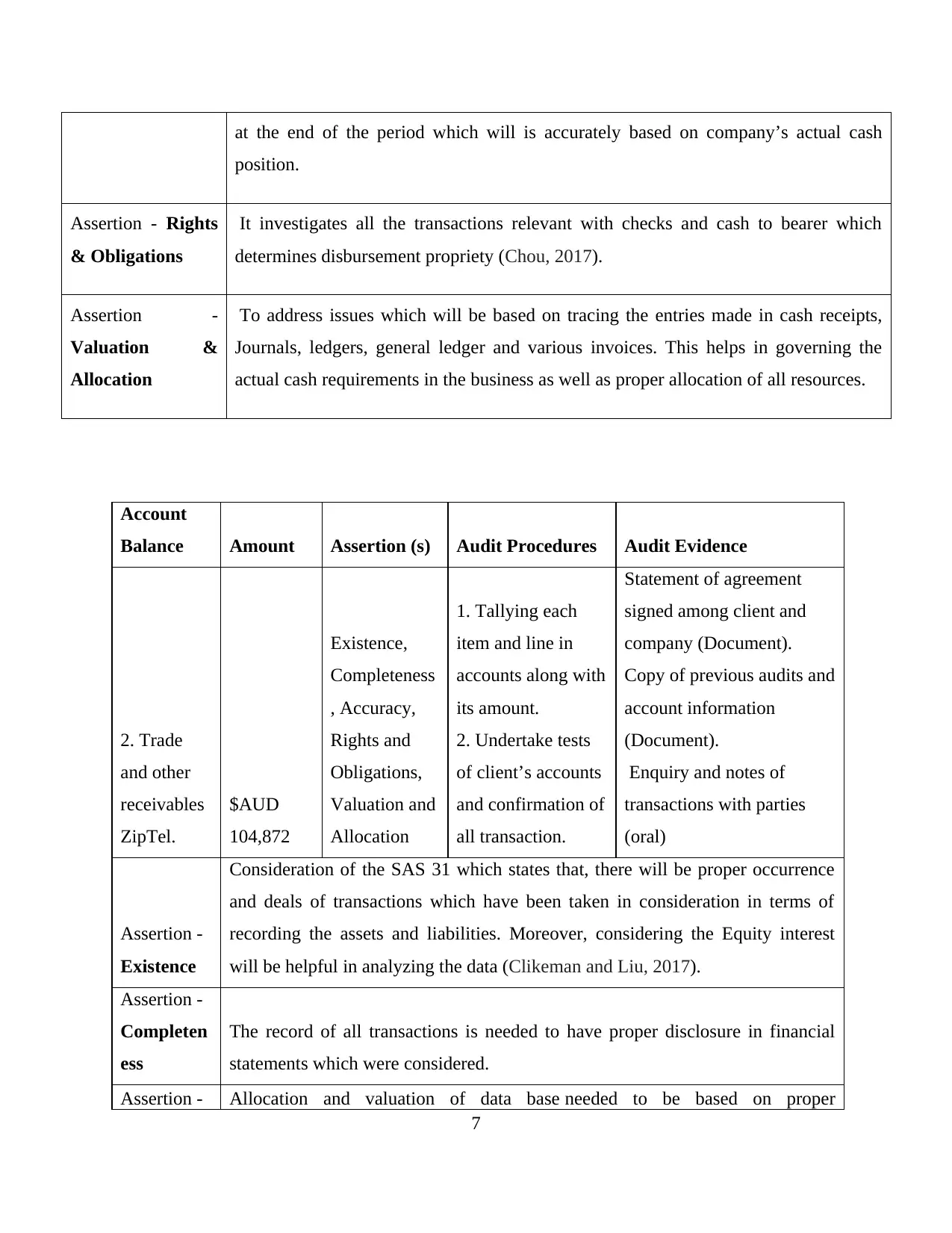

at the end of the period which will is accurately based on company’s actual cash

position.

Assertion - Rights

& Obligations

It investigates all the transactions relevant with checks and cash to bearer which

determines disbursement propriety (Chou, 2017).

Assertion -

Valuation &

Allocation

To address issues which will be based on tracing the entries made in cash receipts,

Journals, ledgers, general ledger and various invoices. This helps in governing the

actual cash requirements in the business as well as proper allocation of all resources.

Account

Balance Amount Assertion (s) Audit Procedures Audit Evidence

2. Trade

and other

receivables

ZipTel.

$AUD

104,872

Existence,

Completeness

, Accuracy,

Rights and

Obligations,

Valuation and

Allocation

1. Tallying each

item and line in

accounts along with

its amount.

2. Undertake tests

of client’s accounts

and confirmation of

all transaction.

Statement of agreement

signed among client and

company (Document).

Copy of previous audits and

account information

(Document).

Enquiry and notes of

transactions with parties

(oral)

Assertion -

Existence

Consideration of the SAS 31 which states that, there will be proper occurrence

and deals of transactions which have been taken in consideration in terms of

recording the assets and liabilities. Moreover, considering the Equity interest

will be helpful in analyzing the data (Clikeman and Liu, 2017).

Assertion -

Completen

ess

The record of all transactions is needed to have proper disclosure in financial

statements which were considered.

Assertion - Allocation and valuation of data base needed to be based on proper

7

position.

Assertion - Rights

& Obligations

It investigates all the transactions relevant with checks and cash to bearer which

determines disbursement propriety (Chou, 2017).

Assertion -

Valuation &

Allocation

To address issues which will be based on tracing the entries made in cash receipts,

Journals, ledgers, general ledger and various invoices. This helps in governing the

actual cash requirements in the business as well as proper allocation of all resources.

Account

Balance Amount Assertion (s) Audit Procedures Audit Evidence

2. Trade

and other

receivables

ZipTel.

$AUD

104,872

Existence,

Completeness

, Accuracy,

Rights and

Obligations,

Valuation and

Allocation

1. Tallying each

item and line in

accounts along with

its amount.

2. Undertake tests

of client’s accounts

and confirmation of

all transaction.

Statement of agreement

signed among client and

company (Document).

Copy of previous audits and

account information

(Document).

Enquiry and notes of

transactions with parties

(oral)

Assertion -

Existence

Consideration of the SAS 31 which states that, there will be proper occurrence

and deals of transactions which have been taken in consideration in terms of

recording the assets and liabilities. Moreover, considering the Equity interest

will be helpful in analyzing the data (Clikeman and Liu, 2017).

Assertion -

Completen

ess

The record of all transactions is needed to have proper disclosure in financial

statements which were considered.

Assertion - Allocation and valuation of data base needed to be based on proper

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accuracy administration and making proper disclosure of data set.

Assertion -

Rights &

Obligation

s

Rights of firm ate associated with the assets while obligations are with the

liabilities.

Assertion -

Valuation

&

Allocation

It consists of proper disclosure of all data base which were relevant with proper

applicability and financial reporting based on proper framework.

Account

Balance Amount Assertion (s) Audit Procedures Audit Evidence

3.

Prepayments

ZipTel.

$AUD

6,868

Existence,

Completeness,

Accuracy, Rights

and Obligations,

Valuation and

Allocation

1. Analysing all

accounts as per

advance payments

2. Determining the

costs incurred in all

transactional

activities.

Past invoices of all

transactions

(Document).

Obtain copies of

expenses (Document).

Enquiry and notes of

transaction (oral)

Assertion -

Existence Future expenses have been represented on the current balance sheet date.

Assertion -

Completene

ss

Enquiring existence of such prepayments in the balance sheet with proper

amount and transactional process (Mccollum, 2017).

Assertion -

Accuracy

Proper classification of expenses along with its amount as well as proper

process of disclosure.

Assertion -

Rights &

Obligations

Responsibilities of client in analysing all risks which were being associated

with business.

8

Assertion -

Rights &

Obligation

s

Rights of firm ate associated with the assets while obligations are with the

liabilities.

Assertion -

Valuation

&

Allocation

It consists of proper disclosure of all data base which were relevant with proper

applicability and financial reporting based on proper framework.

Account

Balance Amount Assertion (s) Audit Procedures Audit Evidence

3.

Prepayments

ZipTel.

$AUD

6,868

Existence,

Completeness,

Accuracy, Rights

and Obligations,

Valuation and

Allocation

1. Analysing all

accounts as per

advance payments

2. Determining the

costs incurred in all

transactional

activities.

Past invoices of all

transactions

(Document).

Obtain copies of

expenses (Document).

Enquiry and notes of

transaction (oral)

Assertion -

Existence Future expenses have been represented on the current balance sheet date.

Assertion -

Completene

ss

Enquiring existence of such prepayments in the balance sheet with proper

amount and transactional process (Mccollum, 2017).

Assertion -

Accuracy

Proper classification of expenses along with its amount as well as proper

process of disclosure.

Assertion -

Rights &

Obligations

Responsibilities of client in analysing all risks which were being associated

with business.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

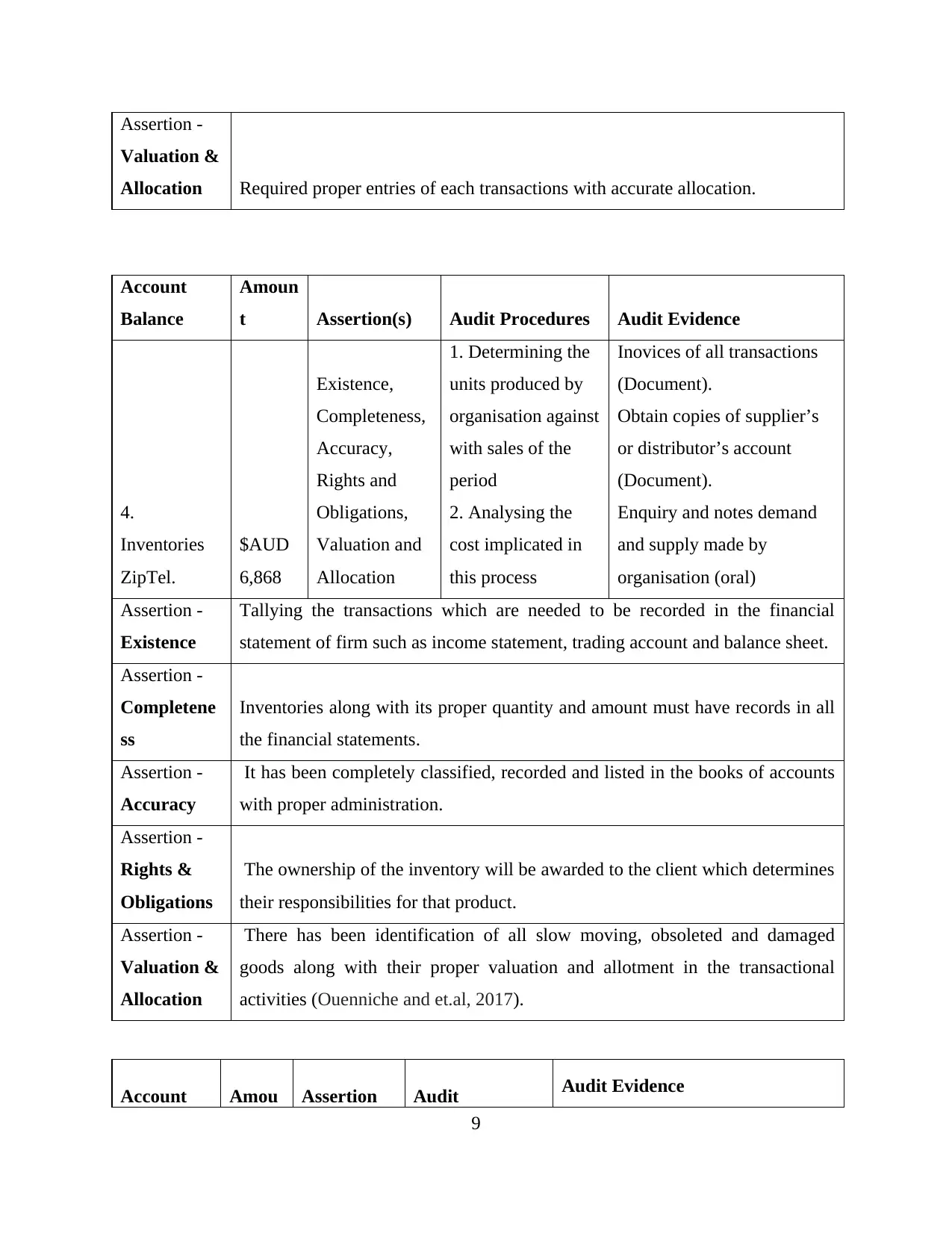

Assertion -

Valuation &

Allocation Required proper entries of each transactions with accurate allocation.

Account

Balance

Amoun

t Assertion(s) Audit Procedures Audit Evidence

4.

Inventories

ZipTel.

$AUD

6,868

Existence,

Completeness,

Accuracy,

Rights and

Obligations,

Valuation and

Allocation

1. Determining the

units produced by

organisation against

with sales of the

period

2. Analysing the

cost implicated in

this process

Inovices of all transactions

(Document).

Obtain copies of supplier’s

or distributor’s account

(Document).

Enquiry and notes demand

and supply made by

organisation (oral)

Assertion -

Existence

Tallying the transactions which are needed to be recorded in the financial

statement of firm such as income statement, trading account and balance sheet.

Assertion -

Completene

ss

Inventories along with its proper quantity and amount must have records in all

the financial statements.

Assertion -

Accuracy

It has been completely classified, recorded and listed in the books of accounts

with proper administration.

Assertion -

Rights &

Obligations

The ownership of the inventory will be awarded to the client which determines

their responsibilities for that product.

Assertion -

Valuation &

Allocation

There has been identification of all slow moving, obsoleted and damaged

goods along with their proper valuation and allotment in the transactional

activities (Ouenniche and et.al, 2017).

Account Amou Assertion Audit Audit Evidence

9

Valuation &

Allocation Required proper entries of each transactions with accurate allocation.

Account

Balance

Amoun

t Assertion(s) Audit Procedures Audit Evidence

4.

Inventories

ZipTel.

$AUD

6,868

Existence,

Completeness,

Accuracy,

Rights and

Obligations,

Valuation and

Allocation

1. Determining the

units produced by

organisation against

with sales of the

period

2. Analysing the

cost implicated in

this process

Inovices of all transactions

(Document).

Obtain copies of supplier’s

or distributor’s account

(Document).

Enquiry and notes demand

and supply made by

organisation (oral)

Assertion -

Existence

Tallying the transactions which are needed to be recorded in the financial

statement of firm such as income statement, trading account and balance sheet.

Assertion -

Completene

ss

Inventories along with its proper quantity and amount must have records in all

the financial statements.

Assertion -

Accuracy

It has been completely classified, recorded and listed in the books of accounts

with proper administration.

Assertion -

Rights &

Obligations

The ownership of the inventory will be awarded to the client which determines

their responsibilities for that product.

Assertion -

Valuation &

Allocation

There has been identification of all slow moving, obsoleted and damaged

goods along with their proper valuation and allotment in the transactional

activities (Ouenniche and et.al, 2017).

Account Amou Assertion Audit Audit Evidence

9

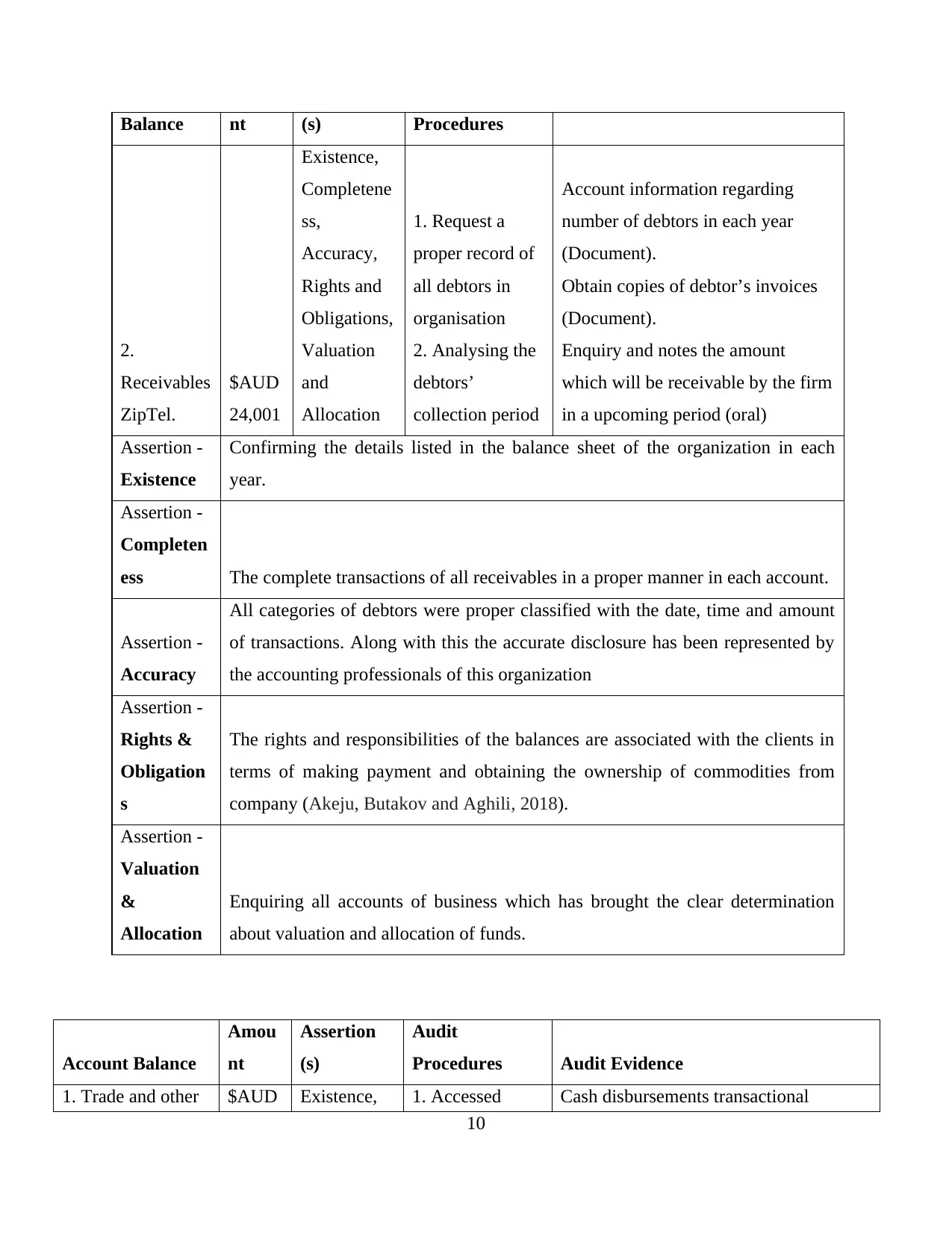

Balance nt (s) Procedures

2.

Receivables

ZipTel.

$AUD

24,001

Existence,

Completene

ss,

Accuracy,

Rights and

Obligations,

Valuation

and

Allocation

1. Request a

proper record of

all debtors in

organisation

2. Analysing the

debtors’

collection period

Account information regarding

number of debtors in each year

(Document).

Obtain copies of debtor’s invoices

(Document).

Enquiry and notes the amount

which will be receivable by the firm

in a upcoming period (oral)

Assertion -

Existence

Confirming the details listed in the balance sheet of the organization in each

year.

Assertion -

Completen

ess The complete transactions of all receivables in a proper manner in each account.

Assertion -

Accuracy

All categories of debtors were proper classified with the date, time and amount

of transactions. Along with this the accurate disclosure has been represented by

the accounting professionals of this organization

Assertion -

Rights &

Obligation

s

The rights and responsibilities of the balances are associated with the clients in

terms of making payment and obtaining the ownership of commodities from

company (Akeju, Butakov and Aghili, 2018).

Assertion -

Valuation

&

Allocation

Enquiring all accounts of business which has brought the clear determination

about valuation and allocation of funds.

Account Balance

Amou

nt

Assertion

(s)

Audit

Procedures Audit Evidence

1. Trade and other $AUD Existence, 1. Accessed Cash disbursements transactional

10

2.

Receivables

ZipTel.

$AUD

24,001

Existence,

Completene

ss,

Accuracy,

Rights and

Obligations,

Valuation

and

Allocation

1. Request a

proper record of

all debtors in

organisation

2. Analysing the

debtors’

collection period

Account information regarding

number of debtors in each year

(Document).

Obtain copies of debtor’s invoices

(Document).

Enquiry and notes the amount

which will be receivable by the firm

in a upcoming period (oral)

Assertion -

Existence

Confirming the details listed in the balance sheet of the organization in each

year.

Assertion -

Completen

ess The complete transactions of all receivables in a proper manner in each account.

Assertion -

Accuracy

All categories of debtors were proper classified with the date, time and amount

of transactions. Along with this the accurate disclosure has been represented by

the accounting professionals of this organization

Assertion -

Rights &

Obligation

s

The rights and responsibilities of the balances are associated with the clients in

terms of making payment and obtaining the ownership of commodities from

company (Akeju, Butakov and Aghili, 2018).

Assertion -

Valuation

&

Allocation

Enquiring all accounts of business which has brought the clear determination

about valuation and allocation of funds.

Account Balance

Amou

nt

Assertion

(s)

Audit

Procedures Audit Evidence

1. Trade and other $AUD Existence, 1. Accessed Cash disbursements transactional

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.