Auditing and Ethics: Audit Procedures and Financial Analysis Report

VerifiedAdded on 2020/10/05

|12

|2552

|384

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics, focusing on materiality, audit procedures, and financial analysis. It begins with an introduction to the code of ethics and its relevance to internal auditing, followed by a detailed examination of materiality and its quantitative estimation, specifically for Speedcast International Limited. The report then explores the significance of different notes and disclosures, particularly contingent liabilities, and their impact on audit procedures. It includes a ratio analysis, examining trends and changes with respect to audit risk. The report further reviews the statement of cash flows, including cash inflows, outflows, and non-cash activities. Finally, it discusses the review of the audit report, including its expressed opinion and going concern risk. The report offers insights into revenue recognition and accounting for business combinations. This report is valuable for students studying finance and auditing, providing practical examples and analysis.

AUDITING AND ETHIC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1.1 Level of materiality with its quantitative estimate................................................................1

1.2 Representing different notes and disclosures with significance of audit..............................2

SECTION 2......................................................................................................................................3

2.1 Trend and changes in ratio with audit risk............................................................................3

SECTION 3......................................................................................................................................6

3.1 Reviewing statement of cash flows.......................................................................................6

3.2 Reviewing audit report by stating its expressed opinion......................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1.1 Level of materiality with its quantitative estimate................................................................1

1.2 Representing different notes and disclosures with significance of audit..............................2

SECTION 2......................................................................................................................................3

2.1 Trend and changes in ratio with audit risk............................................................................3

SECTION 3......................................................................................................................................6

3.1 Reviewing statement of cash flows.......................................................................................6

3.2 Reviewing audit report by stating its expressed opinion......................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

The main objective of code of ethics of any institute is for promoting an ethical culture

with context of profession of internal auditing. There are various principles which are relevant

for perspective of profession and internal auditing practice. There are different rules of conduct

which helps in describing behaviour norms with context of internal auditors. The present report

is giving brief review for developing critical analysis skills linked to materiality with application

of audit, its procedures, analytical review and framing an opinion. It also helps in determining

level of materiality which is used by audit group for Speedcast International Limited of year

2017. It had also discussed about various drafts and disclosures in its annual report related to

contingency and its significance. In the same series, it had also presented preliminary analytical

review with its information of balance sheet and profit and loss statement. It had also discussed

about its business risks and audit procedure which had been undertaken. It had also articulated

statement of cash flow and recommendation to follow audit procedure.

SECTION 1

1.1 Level of materiality with its quantitative estimate

The framework of financial reporting elaborates concept of materiality with reference to

presentation and preparation of financial report. Materiality could be explained as misstatements

along with omissions are termed to be material if they are influencing economic decisions with

respect to user on basis of financial report. The materiality is determined when audit is planned

without need of establishing amount below uncorrected misstatements Hoque, & Pearson,

(2018). It could be on individual or aggregate basis for evaluation of immaterial. There are

various circumstances linked to misstatements which might give impact to auditor for evaluating

its level below materiality. The procedure of audit could not be designed practically for

extracting misstatements which might be material solely due to its nature. The assessment and

identification of risk of material misstatement includes application of professional judgement for

determining classes of transactions, disclosures and account balances. It consists of qualitative

disclosures and misstatements which might be material. While there is possibility that material

misstatement exists in qualitative disclosures and auditor should be capable to determine some

relevant factors like:

The circumstances of business entity for given duration.

The framework of applicable financial reporting which consists of various charges.

1

The main objective of code of ethics of any institute is for promoting an ethical culture

with context of profession of internal auditing. There are various principles which are relevant

for perspective of profession and internal auditing practice. There are different rules of conduct

which helps in describing behaviour norms with context of internal auditors. The present report

is giving brief review for developing critical analysis skills linked to materiality with application

of audit, its procedures, analytical review and framing an opinion. It also helps in determining

level of materiality which is used by audit group for Speedcast International Limited of year

2017. It had also discussed about various drafts and disclosures in its annual report related to

contingency and its significance. In the same series, it had also presented preliminary analytical

review with its information of balance sheet and profit and loss statement. It had also discussed

about its business risks and audit procedure which had been undertaken. It had also articulated

statement of cash flow and recommendation to follow audit procedure.

SECTION 1

1.1 Level of materiality with its quantitative estimate

The framework of financial reporting elaborates concept of materiality with reference to

presentation and preparation of financial report. Materiality could be explained as misstatements

along with omissions are termed to be material if they are influencing economic decisions with

respect to user on basis of financial report. The materiality is determined when audit is planned

without need of establishing amount below uncorrected misstatements Hoque, & Pearson,

(2018). It could be on individual or aggregate basis for evaluation of immaterial. There are

various circumstances linked to misstatements which might give impact to auditor for evaluating

its level below materiality. The procedure of audit could not be designed practically for

extracting misstatements which might be material solely due to its nature. The assessment and

identification of risk of material misstatement includes application of professional judgement for

determining classes of transactions, disclosures and account balances. It consists of qualitative

disclosures and misstatements which might be material. While there is possibility that material

misstatement exists in qualitative disclosures and auditor should be capable to determine some

relevant factors like:

The circumstances of business entity for given duration.

The framework of applicable financial reporting which consists of various charges.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Qualitative disclosure which is very important for users of financial reports due to entity's

nature.

Speedcast International Limited had undertaken materiality for the objective of audit

which was around $3000000 which signifies approx. 2.5% of EBITDA of group as it does not

consider acquisition linked to expenses and revenue. EBITDA was adjusted for items of revenue

and expense which was associated with different acquisitions along with cost of transaction,

restructuring and integration for removing impact of item to recur from every year. They have

utilised 2.5% threshold on basis of professional judgement within particular range of thresholds

which is acceptable. In the same series, they have applied threshold along with different

qualitative considerations for identifying scope of audit with its nature, extent and timing of

procedure for evaluating impact of misstatement on its financial report.

1.2 Representing different notes and disclosures with significance of audit

Auditing is referred as very important function of business which includes appropriate

evaluation of evidence and documentation of various transactions and economic activities of

organisation. The audit system helps in evaluating internal control of organization with its

application linked to organization for adhering its goals Laing & Hoy, (2018).

Generally, auditors have requirement by management for stating acknowledging

statement which is disclosed as contingent liabilities. It is referred as possibility of a particular

liability which had been raised with respect to future event. Liability is known as contingent if

event is occurred or not. The common source for contingent liabilities are identified as

outstanding lawsuits and warranties about product.

In the present scenario, all contingent liabilities are disclosed by management to its

auditors. Generally, it does not happen in continuous series, as auditors must be capable to

perform its extended search procedure after primary inquiry. The internal revenue service reports

could be reviewed by auditor for purpose of unsettling income and tax liabilities. Auditors must

lay special emphasis on content of legal expense account with reference to accounting system.

Further, supporting documentation with context of transactions of legal expense might be

capable for revealing contingent liabilities.

In the same series, for identifying correct treatment of accounting there is requirement of

evaluation of materiality by auditors with reference to contingent liabilities Hutabarat, (2018). If

2

nature.

Speedcast International Limited had undertaken materiality for the objective of audit

which was around $3000000 which signifies approx. 2.5% of EBITDA of group as it does not

consider acquisition linked to expenses and revenue. EBITDA was adjusted for items of revenue

and expense which was associated with different acquisitions along with cost of transaction,

restructuring and integration for removing impact of item to recur from every year. They have

utilised 2.5% threshold on basis of professional judgement within particular range of thresholds

which is acceptable. In the same series, they have applied threshold along with different

qualitative considerations for identifying scope of audit with its nature, extent and timing of

procedure for evaluating impact of misstatement on its financial report.

1.2 Representing different notes and disclosures with significance of audit

Auditing is referred as very important function of business which includes appropriate

evaluation of evidence and documentation of various transactions and economic activities of

organisation. The audit system helps in evaluating internal control of organization with its

application linked to organization for adhering its goals Laing & Hoy, (2018).

Generally, auditors have requirement by management for stating acknowledging

statement which is disclosed as contingent liabilities. It is referred as possibility of a particular

liability which had been raised with respect to future event. Liability is known as contingent if

event is occurred or not. The common source for contingent liabilities are identified as

outstanding lawsuits and warranties about product.

In the present scenario, all contingent liabilities are disclosed by management to its

auditors. Generally, it does not happen in continuous series, as auditors must be capable to

perform its extended search procedure after primary inquiry. The internal revenue service reports

could be reviewed by auditor for purpose of unsettling income and tax liabilities. Auditors must

lay special emphasis on content of legal expense account with reference to accounting system.

Further, supporting documentation with context of transactions of legal expense might be

capable for revealing contingent liabilities.

In the same series, for identifying correct treatment of accounting there is requirement of

evaluation of materiality by auditors with reference to contingent liabilities Hutabarat, (2018). If

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

contingent liability is considered in immateriality limit with absence of special treatment or

disclosure is necessary.

Being an auditor following steps will be considered for the purpose of financial investigation

such as:

Requesting for documents: At the first step, auditor requests to higher management team

for official documents such as bank statement, previous receipts, ledgers and accounts for

auditing purpose.

Audit plan preparation: Once documents have been received then auditor prepares plan

for the purpose of auditing.

Organizing meeting: In the third step, meeting is conducted for doing discussion

regarding financial or accounting matters.

Doing fieldwork: At this, auditor assesses whether business unit has complied with all

the policies and procedures or not.

Drafting report: Auditor drafts report at this stage by including all the findings derived

through investigation.

Conducting closure meeting: In the last step, auditor presents report to the team of

higher management to assess whether they are agreed with the issues identified or not.

SECTION 2

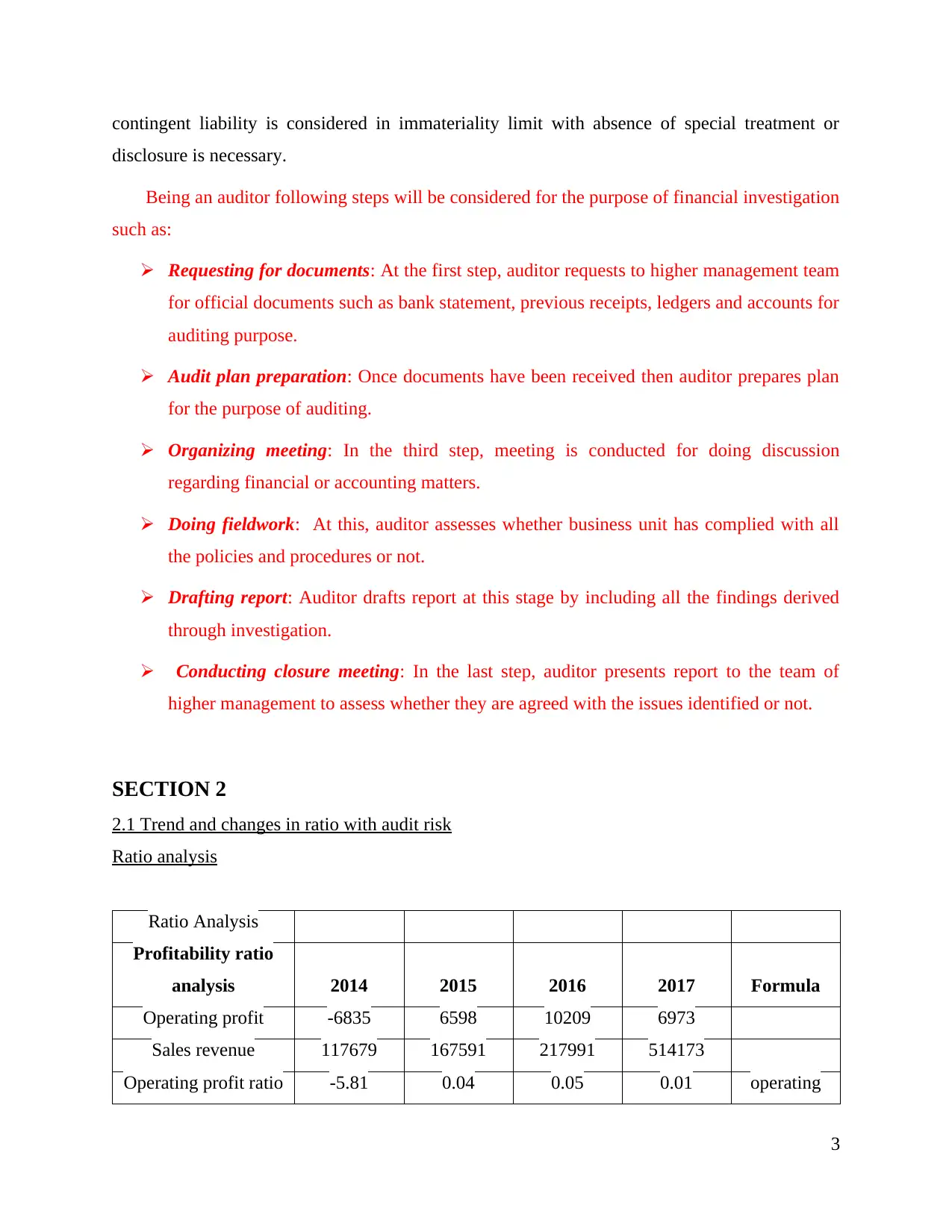

2.1 Trend and changes in ratio with audit risk

Ratio analysis

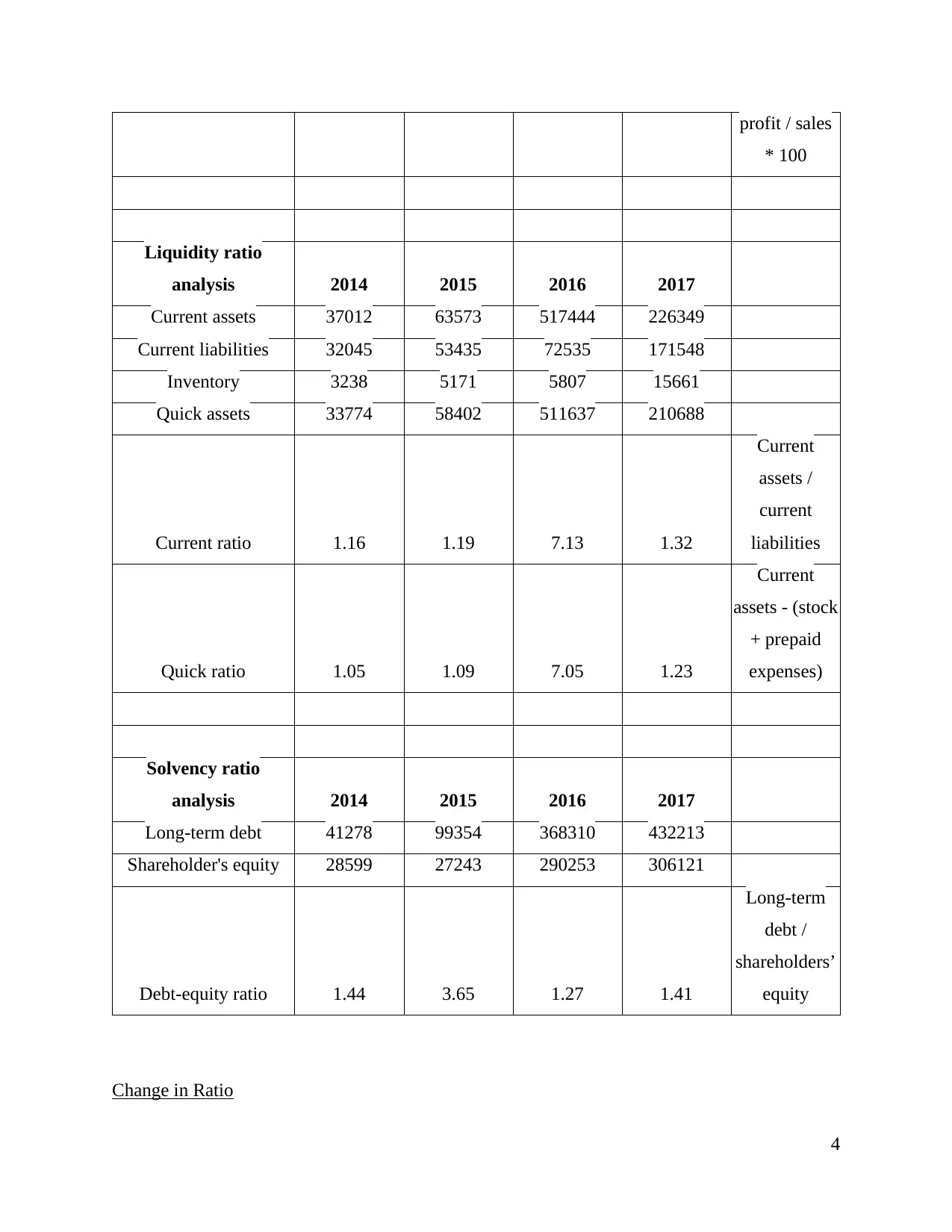

Ratio Analysis

Profitability ratio

analysis 2014 2015 2016 2017 Formula

Operating profit -6835 6598 10209 6973

Sales revenue 117679 167591 217991 514173

Operating profit ratio -5.81 0.04 0.05 0.01 operating

3

disclosure is necessary.

Being an auditor following steps will be considered for the purpose of financial investigation

such as:

Requesting for documents: At the first step, auditor requests to higher management team

for official documents such as bank statement, previous receipts, ledgers and accounts for

auditing purpose.

Audit plan preparation: Once documents have been received then auditor prepares plan

for the purpose of auditing.

Organizing meeting: In the third step, meeting is conducted for doing discussion

regarding financial or accounting matters.

Doing fieldwork: At this, auditor assesses whether business unit has complied with all

the policies and procedures or not.

Drafting report: Auditor drafts report at this stage by including all the findings derived

through investigation.

Conducting closure meeting: In the last step, auditor presents report to the team of

higher management to assess whether they are agreed with the issues identified or not.

SECTION 2

2.1 Trend and changes in ratio with audit risk

Ratio analysis

Ratio Analysis

Profitability ratio

analysis 2014 2015 2016 2017 Formula

Operating profit -6835 6598 10209 6973

Sales revenue 117679 167591 217991 514173

Operating profit ratio -5.81 0.04 0.05 0.01 operating

3

profit / sales

* 100

Liquidity ratio

analysis 2014 2015 2016 2017

Current assets 37012 63573 517444 226349

Current liabilities 32045 53435 72535 171548

Inventory 3238 5171 5807 15661

Quick assets 33774 58402 511637 210688

Current ratio 1.16 1.19 7.13 1.32

Current

assets /

current

liabilities

Quick ratio 1.05 1.09 7.05 1.23

Current

assets - (stock

+ prepaid

expenses)

Solvency ratio

analysis 2014 2015 2016 2017

Long-term debt 41278 99354 368310 432213

Shareholder's equity 28599 27243 290253 306121

Debt-equity ratio 1.44 3.65 1.27 1.41

Long-term

debt /

shareholders’

equity

Change in Ratio

4

* 100

Liquidity ratio

analysis 2014 2015 2016 2017

Current assets 37012 63573 517444 226349

Current liabilities 32045 53435 72535 171548

Inventory 3238 5171 5807 15661

Quick assets 33774 58402 511637 210688

Current ratio 1.16 1.19 7.13 1.32

Current

assets /

current

liabilities

Quick ratio 1.05 1.09 7.05 1.23

Current

assets - (stock

+ prepaid

expenses)

Solvency ratio

analysis 2014 2015 2016 2017

Long-term debt 41278 99354 368310 432213

Shareholder's equity 28599 27243 290253 306121

Debt-equity ratio 1.44 3.65 1.27 1.41

Long-term

debt /

shareholders’

equity

Change in Ratio

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

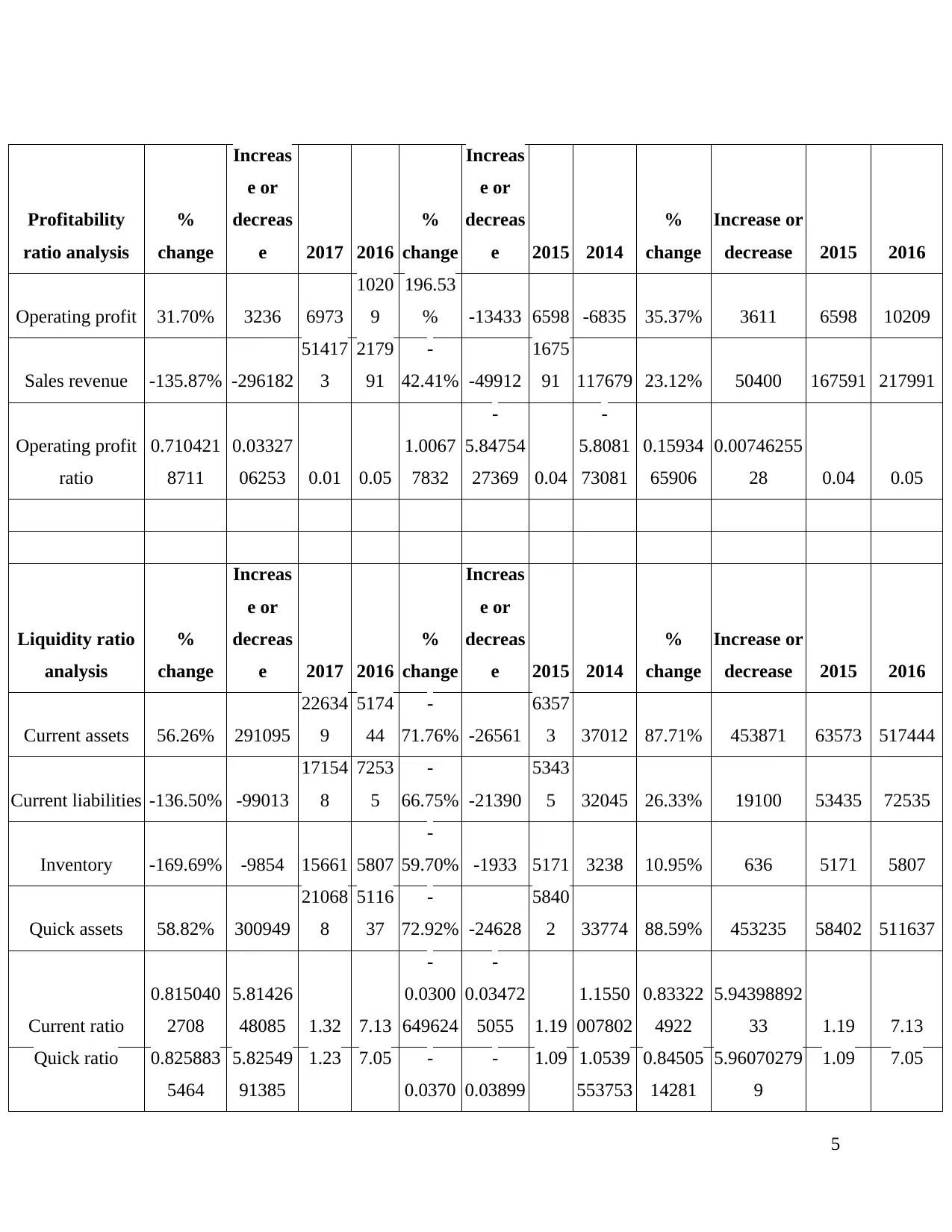

Profitability

ratio analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Operating profit 31.70% 3236 6973

1020

9

196.53

% -13433 6598 -6835 35.37% 3611 6598 10209

Sales revenue -135.87% -296182

51417

3

2179

91

-

42.41% -49912

1675

91 117679 23.12% 50400 167591 217991

Operating profit

ratio

0.710421

8711

0.03327

06253 0.01 0.05

1.0067

7832

-

5.84754

27369 0.04

-

5.8081

73081

0.15934

65906

0.00746255

28 0.04 0.05

Liquidity ratio

analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Current assets 56.26% 291095

22634

9

5174

44

-

71.76% -26561

6357

3 37012 87.71% 453871 63573 517444

Current liabilities -136.50% -99013

17154

8

7253

5

-

66.75% -21390

5343

5 32045 26.33% 19100 53435 72535

Inventory -169.69% -9854 15661 5807

-

59.70% -1933 5171 3238 10.95% 636 5171 5807

Quick assets 58.82% 300949

21068

8

5116

37

-

72.92% -24628

5840

2 33774 88.59% 453235 58402 511637

Current ratio

0.815040

2708

5.81426

48085 1.32 7.13

-

0.0300

649624

-

0.03472

5055 1.19

1.1550

007802

0.83322

4922

5.94398892

33 1.19 7.13

Quick ratio 0.825883

5464

5.82549

91385

1.23 7.05 -

0.0370

-

0.03899

1.09 1.0539

553753

0.84505

14281

5.96070279

9

1.09 7.05

5

ratio analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Operating profit 31.70% 3236 6973

1020

9

196.53

% -13433 6598 -6835 35.37% 3611 6598 10209

Sales revenue -135.87% -296182

51417

3

2179

91

-

42.41% -49912

1675

91 117679 23.12% 50400 167591 217991

Operating profit

ratio

0.710421

8711

0.03327

06253 0.01 0.05

1.0067

7832

-

5.84754

27369 0.04

-

5.8081

73081

0.15934

65906

0.00746255

28 0.04 0.05

Liquidity ratio

analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Current assets 56.26% 291095

22634

9

5174

44

-

71.76% -26561

6357

3 37012 87.71% 453871 63573 517444

Current liabilities -136.50% -99013

17154

8

7253

5

-

66.75% -21390

5343

5 32045 26.33% 19100 53435 72535

Inventory -169.69% -9854 15661 5807

-

59.70% -1933 5171 3238 10.95% 636 5171 5807

Quick assets 58.82% 300949

21068

8

5116

37

-

72.92% -24628

5840

2 33774 88.59% 453235 58402 511637

Current ratio

0.815040

2708

5.81426

48085 1.32 7.13

-

0.0300

649624

-

0.03472

5055 1.19

1.1550

007802

0.83322

4922

5.94398892

33 1.19 7.13

Quick ratio 0.825883

5464

5.82549

91385

1.23 7.05 -

0.0370

-

0.03899

1.09 1.0539

553753

0.84505

14281

5.96070279

9

1.09 7.05

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

022128 86811

Solvency ratio

analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Long-term debt -17.35% -63903

43221

3

3683

10

-

140.69

% -58076

9935

4 41278 73.02% 268956 99354 368310

Shareholder's

equity -5.47% -15868

30612

1

2902

53 4.74% 1356

2724

3 28599 90.61% 263010 27243 290253

Debt-equity ratio

-

0.112673

9198

-

0.14297

50301 1.41 1.27

-

1.5267

520526

-

2.20361

80015 3.65

1.4433

371796

-

1.87404

54568

-

2.37802772

82 3.65 1.27

Audit risk areas and matters with its procedure

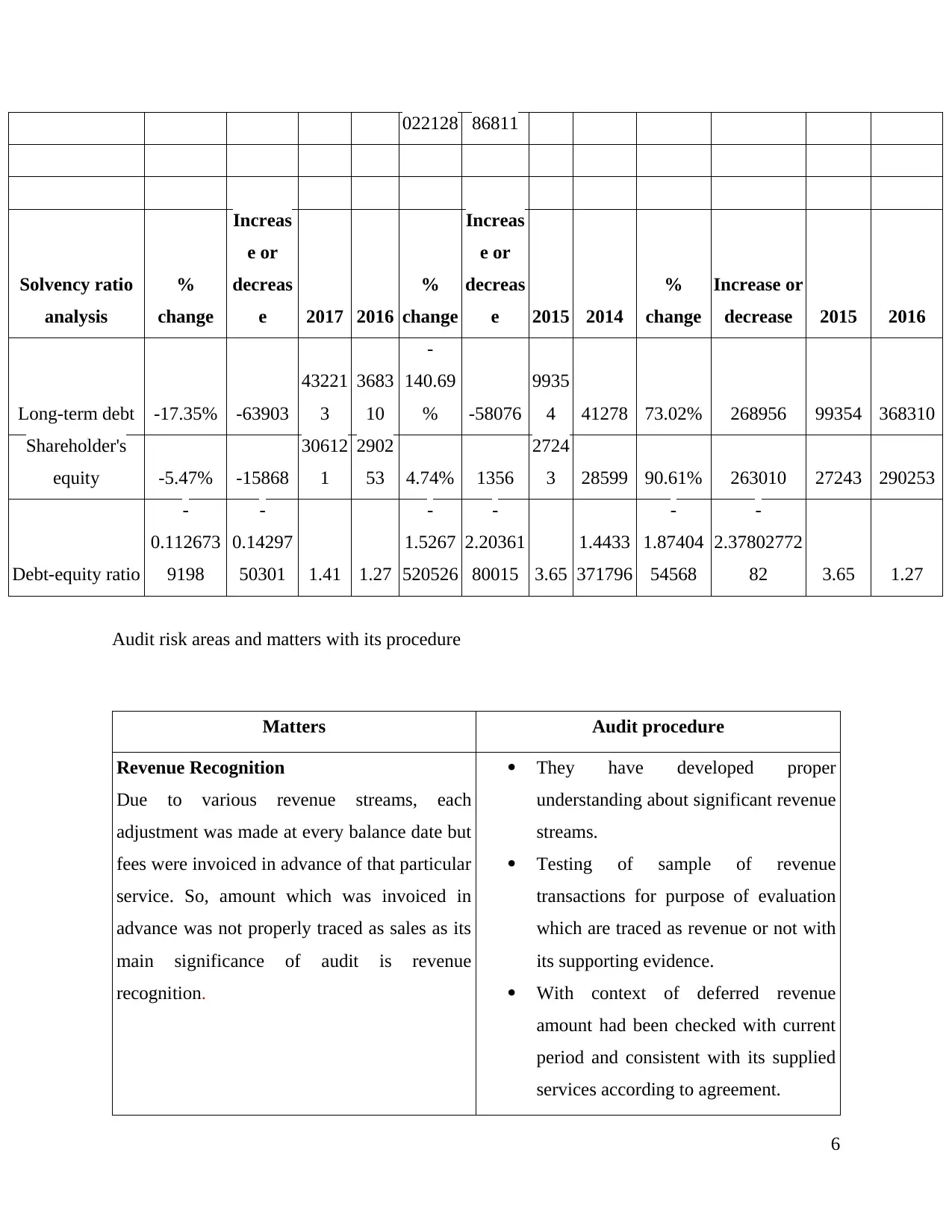

Matters Audit procedure

Revenue Recognition

Due to various revenue streams, each

adjustment was made at every balance date but

fees were invoiced in advance of that particular

service. So, amount which was invoiced in

advance was not properly traced as sales as its

main significance of audit is revenue

recognition.

They have developed proper

understanding about significant revenue

streams.

Testing of sample of revenue

transactions for purpose of evaluation

which are traced as revenue or not with

its supporting evidence.

With context of deferred revenue

amount had been checked with current

period and consistent with its supplied

services according to agreement.

6

Solvency ratio

analysis

%

change

Increas

e or

decreas

e 2017 2016

%

change

Increas

e or

decreas

e 2015 2014

%

change

Increase or

decrease 2015 2016

Long-term debt -17.35% -63903

43221

3

3683

10

-

140.69

% -58076

9935

4 41278 73.02% 268956 99354 368310

Shareholder's

equity -5.47% -15868

30612

1

2902

53 4.74% 1356

2724

3 28599 90.61% 263010 27243 290253

Debt-equity ratio

-

0.112673

9198

-

0.14297

50301 1.41 1.27

-

1.5267

520526

-

2.20361

80015 3.65

1.4433

371796

-

1.87404

54568

-

2.37802772

82 3.65 1.27

Audit risk areas and matters with its procedure

Matters Audit procedure

Revenue Recognition

Due to various revenue streams, each

adjustment was made at every balance date but

fees were invoiced in advance of that particular

service. So, amount which was invoiced in

advance was not properly traced as sales as its

main significance of audit is revenue

recognition.

They have developed proper

understanding about significant revenue

streams.

Testing of sample of revenue

transactions for purpose of evaluation

which are traced as revenue or not with

its supporting evidence.

With context of deferred revenue

amount had been checked with current

period and consistent with its supplied

services according to agreement.

6

By following FRS 102 concerned

authorities can recognize revenue

effectually.

Accounting for business combination

(Harris CapRock and UltiSat)

Estimation of purchase consideration with

reference to payable of contingent

consideration for attaining various operational

performance targets. Appropriate estimation of

acquired assets and liability's fair value. It also

consists of judging about over the value of

relationships which had been acquired.

Procedure for Harris CapRock

With purchase and sale agreement for

determining consideration of contingent

purchase. It depends on attaining

various operational performance target.

Agreed on fair value of assets and

liabilities which were acquired.

With reference to customer relationship

tangible asset they had considered rate

of customer attrition and discount. In

the same series mathematical accuracy

had been assessed.

They had considered input of cash flow

to market contract and rate data.

Assisted through valuation experts

along with assessment of used discount

rate.

Procedure for UltiSat Acquisition

Presence of payable of contingent

consideration for purpose of attaining

future level of EBITDA, gross margin

and revenue.

Group's provisional was assessed with

appropriate estimation of fair value of

assets and liabilities which were

acquired.

By doing evaluation, it has identified that ASA

545 helps in investigating aspects related to

7

authorities can recognize revenue

effectually.

Accounting for business combination

(Harris CapRock and UltiSat)

Estimation of purchase consideration with

reference to payable of contingent

consideration for attaining various operational

performance targets. Appropriate estimation of

acquired assets and liability's fair value. It also

consists of judging about over the value of

relationships which had been acquired.

Procedure for Harris CapRock

With purchase and sale agreement for

determining consideration of contingent

purchase. It depends on attaining

various operational performance target.

Agreed on fair value of assets and

liabilities which were acquired.

With reference to customer relationship

tangible asset they had considered rate

of customer attrition and discount. In

the same series mathematical accuracy

had been assessed.

They had considered input of cash flow

to market contract and rate data.

Assisted through valuation experts

along with assessment of used discount

rate.

Procedure for UltiSat Acquisition

Presence of payable of contingent

consideration for purpose of attaining

future level of EBITDA, gross margin

and revenue.

Group's provisional was assessed with

appropriate estimation of fair value of

assets and liabilities which were

acquired.

By doing evaluation, it has identified that ASA

545 helps in investigating aspects related to

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

asset’s fair value.

SECTION 3

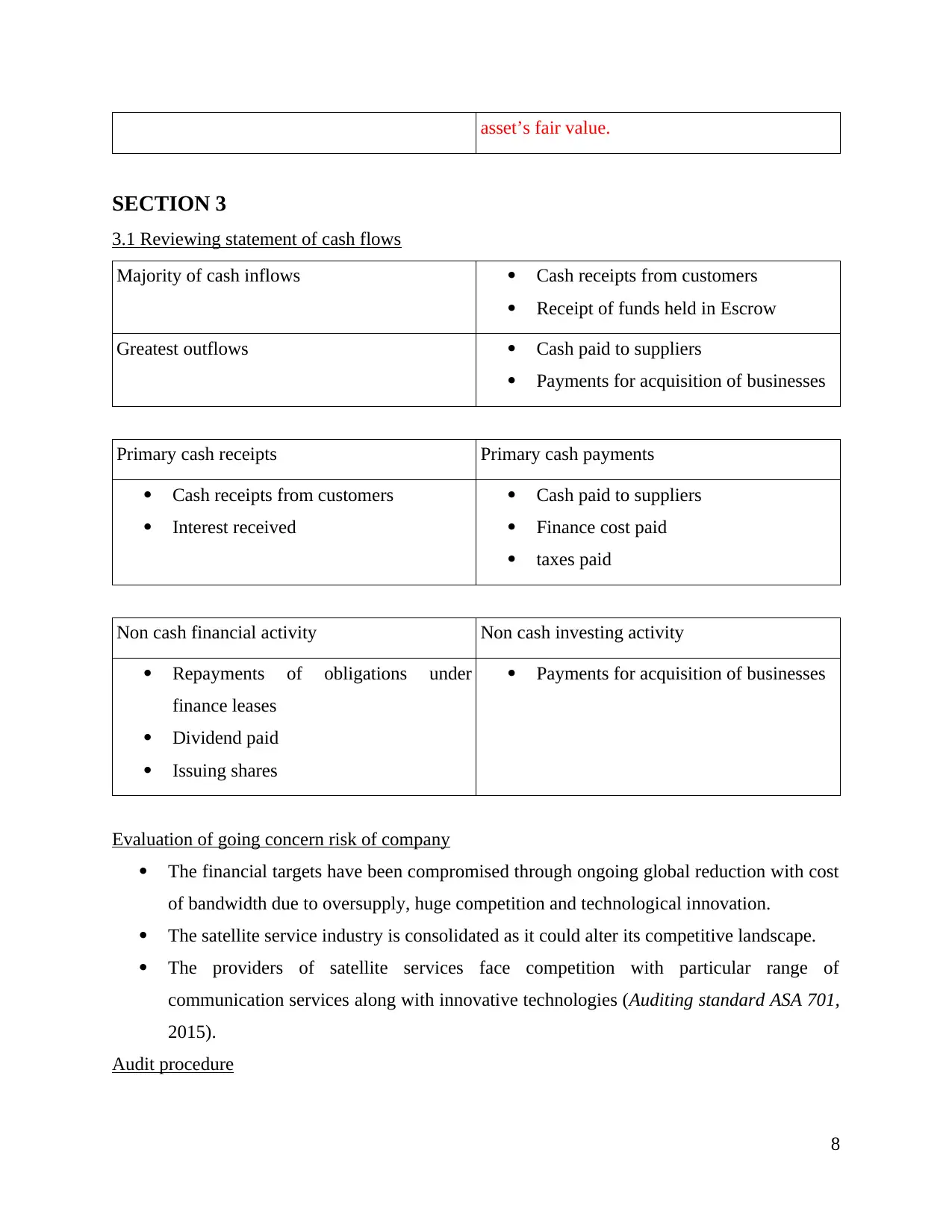

3.1 Reviewing statement of cash flows

Majority of cash inflows Cash receipts from customers

Receipt of funds held in Escrow

Greatest outflows Cash paid to suppliers

Payments for acquisition of businesses

Primary cash receipts Primary cash payments

Cash receipts from customers

Interest received

Cash paid to suppliers

Finance cost paid

taxes paid

Non cash financial activity Non cash investing activity

Repayments of obligations under

finance leases

Dividend paid

Issuing shares

Payments for acquisition of businesses

Evaluation of going concern risk of company

The financial targets have been compromised through ongoing global reduction with cost

of bandwidth due to oversupply, huge competition and technological innovation.

The satellite service industry is consolidated as it could alter its competitive landscape.

The providers of satellite services face competition with particular range of

communication services along with innovative technologies (Auditing standard ASA 701,

2015).

Audit procedure

8

SECTION 3

3.1 Reviewing statement of cash flows

Majority of cash inflows Cash receipts from customers

Receipt of funds held in Escrow

Greatest outflows Cash paid to suppliers

Payments for acquisition of businesses

Primary cash receipts Primary cash payments

Cash receipts from customers

Interest received

Cash paid to suppliers

Finance cost paid

taxes paid

Non cash financial activity Non cash investing activity

Repayments of obligations under

finance leases

Dividend paid

Issuing shares

Payments for acquisition of businesses

Evaluation of going concern risk of company

The financial targets have been compromised through ongoing global reduction with cost

of bandwidth due to oversupply, huge competition and technological innovation.

The satellite service industry is consolidated as it could alter its competitive landscape.

The providers of satellite services face competition with particular range of

communication services along with innovative technologies (Auditing standard ASA 701,

2015).

Audit procedure

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analytical procedure is recommended for auditors to extract and confirm major business

indicators, relationship of financial statements, business performance and operating trends.

Generally, they perform with financial analysts for reviewing its historical data and comparison

of current data from its future. Generally, auditors lay special emphasis on relationships of

accounts for verifying completeness and accuracy of reporting data.

In the same series, it could use internal control testing, guidelines and mechanisms for

controlling effectiveness and adequacy for detecting its trends of operating performance and for

assessing its major productivity ratio of business. The specialists evaluate controls for verifying

adherence to its guidelines by regulators, operating principles and governance of committee

procedures in particular industries where business entities are performing. Controls are referred

as effective if correct weakness had been built along with adequate policies, clear hierarchy lines

and step by step procedures for resolving its issues (List of audit procedures, 2018).

3.2 Reviewing audit report by stating its expressed opinion

It provides true and fair aspect of financial position of group on its ending of year. It also

complies with Corporations Regulations 2001 and Australian Accounting Standards. Their main

responsibility in these specific standards is to describe responsibility of auditor for the purpose of

audit with financial report. Their audit helps in providing reasonable assurance with context of

financial report from its material misstatement. Generally, it might arise because of error or

fraud. It is referred as material from individual or aggregate aspect which might influence

economic decisions with context to users on basis of financial report. The scope of audit is

ensured for performing sufficient work to provide opinion about whole financial report. It

considers geographic and management structure of particular group with its processes of

accounting and control along with operation of industry.

The activities of group consist of provisions of satellite bandwidth services to its

government, enterprise, maritime energy and emerging markets. Scope of audit report is too wide

due to the presence of various operations and business entities in various countries such as US,

UK, Australia and Hong Kong.

CONCLUSION

From the above study it had been concluded that auditing and ethics is very important

concept for any business entity. In this report it had shown with reference to Speedcast

International limited of year 2017 with its official accounting inspection procedures. It had

9

indicators, relationship of financial statements, business performance and operating trends.

Generally, they perform with financial analysts for reviewing its historical data and comparison

of current data from its future. Generally, auditors lay special emphasis on relationships of

accounts for verifying completeness and accuracy of reporting data.

In the same series, it could use internal control testing, guidelines and mechanisms for

controlling effectiveness and adequacy for detecting its trends of operating performance and for

assessing its major productivity ratio of business. The specialists evaluate controls for verifying

adherence to its guidelines by regulators, operating principles and governance of committee

procedures in particular industries where business entities are performing. Controls are referred

as effective if correct weakness had been built along with adequate policies, clear hierarchy lines

and step by step procedures for resolving its issues (List of audit procedures, 2018).

3.2 Reviewing audit report by stating its expressed opinion

It provides true and fair aspect of financial position of group on its ending of year. It also

complies with Corporations Regulations 2001 and Australian Accounting Standards. Their main

responsibility in these specific standards is to describe responsibility of auditor for the purpose of

audit with financial report. Their audit helps in providing reasonable assurance with context of

financial report from its material misstatement. Generally, it might arise because of error or

fraud. It is referred as material from individual or aggregate aspect which might influence

economic decisions with context to users on basis of financial report. The scope of audit is

ensured for performing sufficient work to provide opinion about whole financial report. It

considers geographic and management structure of particular group with its processes of

accounting and control along with operation of industry.

The activities of group consist of provisions of satellite bandwidth services to its

government, enterprise, maritime energy and emerging markets. Scope of audit report is too wide

due to the presence of various operations and business entities in various countries such as US,

UK, Australia and Hong Kong.

CONCLUSION

From the above study it had been concluded that auditing and ethics is very important

concept for any business entity. In this report it had shown with reference to Speedcast

International limited of year 2017 with its official accounting inspection procedures. It had

9

shown audit procedure follows specific rules of code of conduct with its behaviour norms with

context of its internal auditors.

10

context of its internal auditors.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.