ACCT20075 Auditing Report: ASX Limited Financial Analysis

VerifiedAdded on 2022/12/23

|11

|2651

|67

Report

AI Summary

This report provides an in-depth analysis of the auditing process conducted on ASX Limited. It begins with an introduction to auditing, emphasizing the auditor's role in verifying financial reports and ensuring compliance with regulations. The report then delves into key concepts such as materiality and the scope of the audit, including how auditors assess and determine the significance of errors or omissions in financial statements. It also examines the disclosure requirements in company reports, the application of analytical procedures, and the use of financial ratios like current, debt, and debt-equity ratios to assess the company's financial health. A review of the company's cash flow statement and annual report, including the auditor's opinion and key audit matters, is also included. The report analyzes the financial performance of ASX Limited and the audit procedures applied. The report concludes with a summary of the key findings and the overall auditing process.

Running head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Introduction................................................................................................................................4

Materiality and Scope of Audit..................................................................................................4

Disclosure in Company Reports.................................................................................................5

Analytical Procedure in Company.............................................................................................6

Current Ratio..........................................................................................................................6

Debt Ratio..............................................................................................................................7

Debt-Equity Ratio..................................................................................................................8

Analysis of Company Cash Flow Statement..............................................................................8

Review of Company Annual Report..........................................................................................9

Key Audit Matters......................................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

AUDITING

Table of Contents

Introduction................................................................................................................................4

Materiality and Scope of Audit..................................................................................................4

Disclosure in Company Reports.................................................................................................5

Analytical Procedure in Company.............................................................................................6

Current Ratio..........................................................................................................................6

Debt Ratio..............................................................................................................................7

Debt-Equity Ratio..................................................................................................................8

Analysis of Company Cash Flow Statement..............................................................................8

Review of Company Annual Report..........................................................................................9

Key Audit Matters......................................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

2

AUDITING

Introduction

Auditing is process which is carried by Auditor to know the financial report error and

omission so it can carry its procedure so that it can see how the company can carry its

business operation quickly and effectively in the business (Coppage & Shastri 2014). The

company should able to follow all the rules and regulation so that it can carry all its business

operation easily. Auditor has to know the company details so it can see how the company can

manage its business activities, which help it to ascertain the amount of risk which is involved

in company business. The report shows the company name ASX Limited, which based on the

investment. The report shows the materiality concept and how the Auditor can carry its

process to ascertain the materiality in the financial statement, it also shows about the

company financial ratio show this show how company can carry all its operation easily in

their business. It also shows the analysis of company cash flow statement so that it can know

the inflow and outflow of cash in the business (DeFond & Zhang 2014). It also shows the

analysis of the annual report and what is the opinion which is given by the Auditor on the

company financial statement.

Materiality and Scope of Audit

Auditor has to plan the scope of the audit so it can know how it will able to analysis

the company financial statement quickly and effectively in business. Materiality refers to the

error and omission, which is done by the company in regards to their annual report. The

company should carry all the information correctly in its financial statement so it can give

proper information to the commercial user (Eilifsen & Messier Jr 2014). Auditor has to know

the materiality which is involved in the company so that it can carry all the audit process and

able to give a proper opinion upon the company reports.

AUDITING

Introduction

Auditing is process which is carried by Auditor to know the financial report error and

omission so it can carry its procedure so that it can see how the company can carry its

business operation quickly and effectively in the business (Coppage & Shastri 2014). The

company should able to follow all the rules and regulation so that it can carry all its business

operation easily. Auditor has to know the company details so it can see how the company can

manage its business activities, which help it to ascertain the amount of risk which is involved

in company business. The report shows the company name ASX Limited, which based on the

investment. The report shows the materiality concept and how the Auditor can carry its

process to ascertain the materiality in the financial statement, it also shows about the

company financial ratio show this show how company can carry all its operation easily in

their business. It also shows the analysis of company cash flow statement so that it can know

the inflow and outflow of cash in the business (DeFond & Zhang 2014). It also shows the

analysis of the annual report and what is the opinion which is given by the Auditor on the

company financial statement.

Materiality and Scope of Audit

Auditor has to plan the scope of the audit so it can know how it will able to analysis

the company financial statement quickly and effectively in business. Materiality refers to the

error and omission, which is done by the company in regards to their annual report. The

company should carry all the information correctly in its financial statement so it can give

proper information to the commercial user (Eilifsen & Messier Jr 2014). Auditor has to know

the materiality which is involved in the company so that it can carry all the audit process and

able to give a proper opinion upon the company reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

Auditor has to take the concept of materiality with proper importance so that it can

know the business risk, which is associated with the company financial statement. It has to

plan to the materiality so it can all the audit process in the business so while calculating the

materiality it should consider the sales, total asset and equity (Elder et al., 2013). This will

help the Auditor to know how to carry its audit process so that it can able to gain more

amount of audit evidence which will help them to give a proper report to the company. The

Auditor is taking the total asset as the base for the calculation of total planning materiality.

The total planning materiality calculated as

Planning Materiality=Total Asset∗5 %

¿ $ 12923

¿ 5 %

¿ $ 646.5

The above calculation shows the planning materiality, so the Auditor has to ascertain

the procedure of audit and able to carry its activity easily on the company financial statement,

this will also affect the overall auditor report as if there a high amount of materiality so this

will increase the overall risk in the business.

Disclosure in Company Reports

Management can give the proper amount of disclosure in the company business so

that it can show all the detail information which the company should provide to the financial

user so that it can take the proper decision of investment in the company. The company

should able to provide all the required information as per the standard so that it can able to

present appropriate information in the company (Furnham & Gunter 2015). The Auditor

should check that the company is able to give all the required information in the disclosure as

AUDITING

Auditor has to take the concept of materiality with proper importance so that it can

know the business risk, which is associated with the company financial statement. It has to

plan to the materiality so it can all the audit process in the business so while calculating the

materiality it should consider the sales, total asset and equity (Elder et al., 2013). This will

help the Auditor to know how to carry its audit process so that it can able to gain more

amount of audit evidence which will help them to give a proper report to the company. The

Auditor is taking the total asset as the base for the calculation of total planning materiality.

The total planning materiality calculated as

Planning Materiality=Total Asset∗5 %

¿ $ 12923

¿ 5 %

¿ $ 646.5

The above calculation shows the planning materiality, so the Auditor has to ascertain

the procedure of audit and able to carry its activity easily on the company financial statement,

this will also affect the overall auditor report as if there a high amount of materiality so this

will increase the overall risk in the business.

Disclosure in Company Reports

Management can give the proper amount of disclosure in the company business so

that it can show all the detail information which the company should provide to the financial

user so that it can take the proper decision of investment in the company. The company

should able to provide all the required information as per the standard so that it can able to

present appropriate information in the company (Furnham & Gunter 2015). The Auditor

should check that the company is able to give all the required information in the disclosure as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

it should know the assumption which the company is to take in their business activities. It

should carry its audit process properly so that the Auditor can know all the required

information accurately in the annual report.

Auditor has to ascertain the information are true and accurate so that the user can take

proper decision in regards to company financial statement. It helps them to gain all the

information activities about the company business activities in the market.

Analytical Procedure in Company

It is the process which is carried by Auditor to know how the company can carry its

business operation, and it shows how the company is working in the business. It helps the

Auditor to understand many aspects of the company so can know the business risk in the

market (Goh, Krishnan & Li 2013). This help to know the amount of risk and able to give a

proper opinion in the company business, Auditor can have an adequate opinion on the

company financial statement.

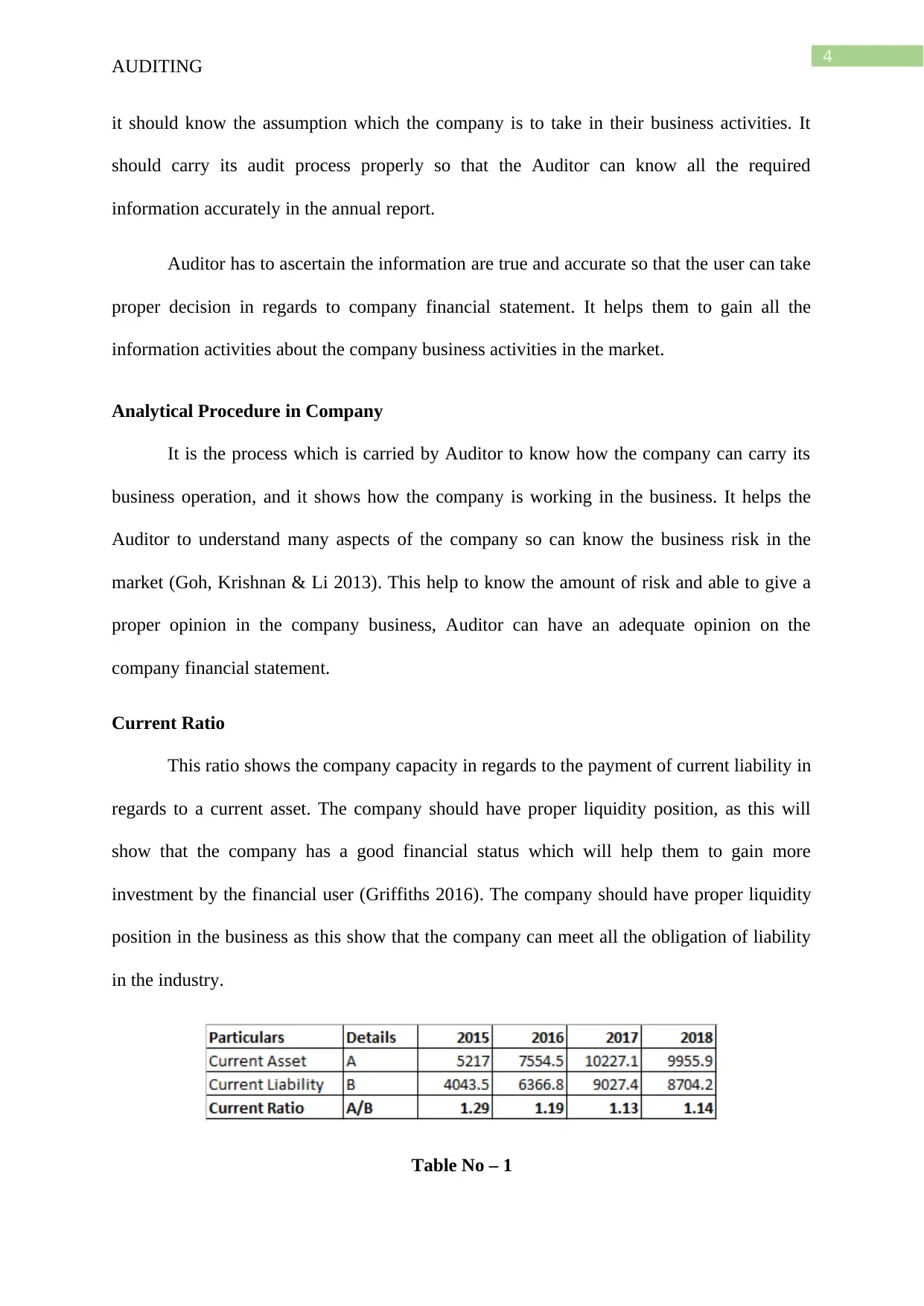

Current Ratio

This ratio shows the company capacity in regards to the payment of current liability in

regards to a current asset. The company should have proper liquidity position, as this will

show that the company has a good financial status which will help them to gain more

investment by the financial user (Griffiths 2016). The company should have proper liquidity

position in the business as this show that the company can meet all the obligation of liability

in the industry.

Table No – 1

AUDITING

it should know the assumption which the company is to take in their business activities. It

should carry its audit process properly so that the Auditor can know all the required

information accurately in the annual report.

Auditor has to ascertain the information are true and accurate so that the user can take

proper decision in regards to company financial statement. It helps them to gain all the

information activities about the company business activities in the market.

Analytical Procedure in Company

It is the process which is carried by Auditor to know how the company can carry its

business operation, and it shows how the company is working in the business. It helps the

Auditor to understand many aspects of the company so can know the business risk in the

market (Goh, Krishnan & Li 2013). This help to know the amount of risk and able to give a

proper opinion in the company business, Auditor can have an adequate opinion on the

company financial statement.

Current Ratio

This ratio shows the company capacity in regards to the payment of current liability in

regards to a current asset. The company should have proper liquidity position, as this will

show that the company has a good financial status which will help them to gain more

investment by the financial user (Griffiths 2016). The company should have proper liquidity

position in the business as this show that the company can meet all the obligation of liability

in the industry.

Table No – 1

5

AUDITING

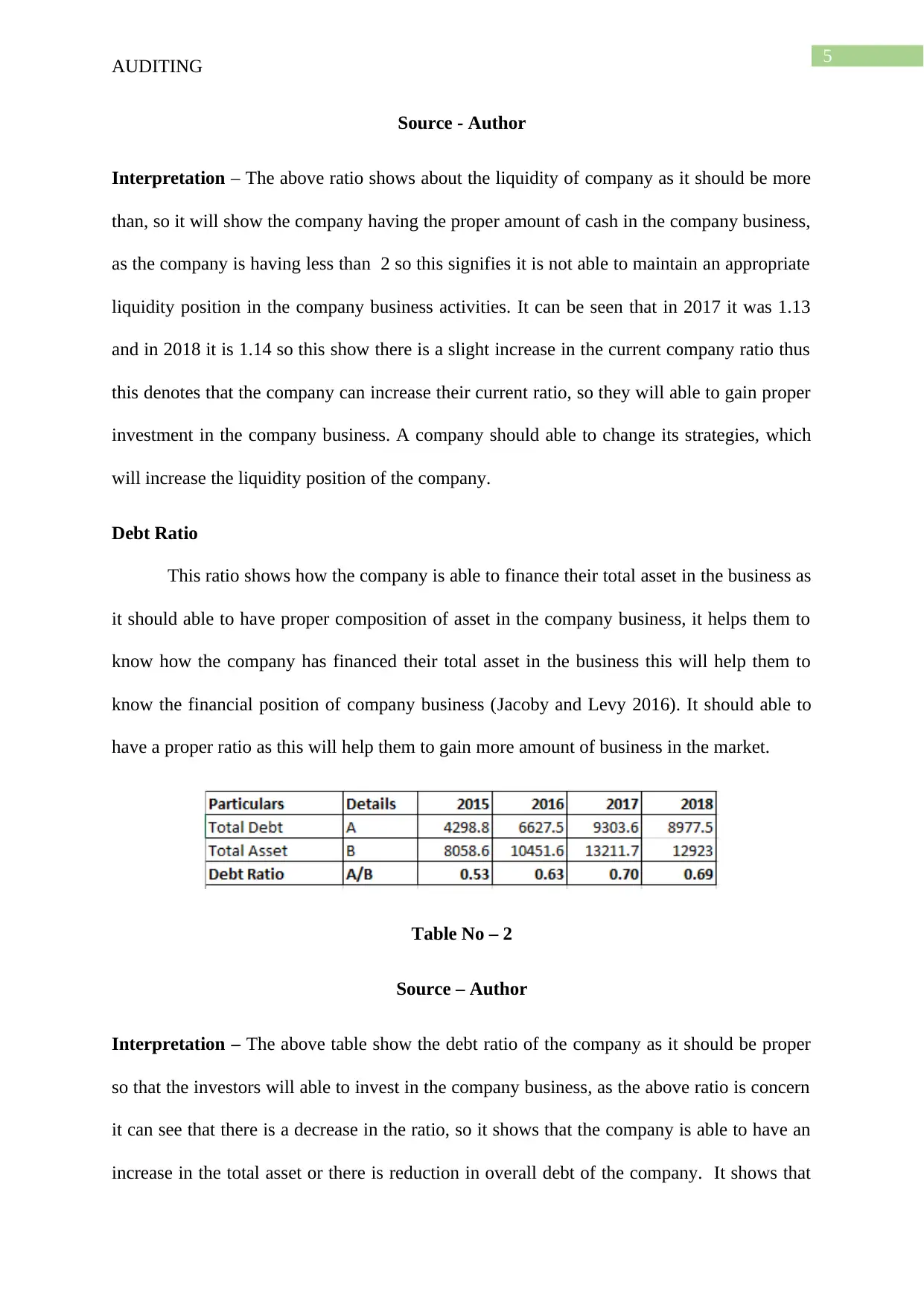

Source - Author

Interpretation – The above ratio shows about the liquidity of company as it should be more

than, so it will show the company having the proper amount of cash in the company business,

as the company is having less than 2 so this signifies it is not able to maintain an appropriate

liquidity position in the company business activities. It can be seen that in 2017 it was 1.13

and in 2018 it is 1.14 so this show there is a slight increase in the current company ratio thus

this denotes that the company can increase their current ratio, so they will able to gain proper

investment in the company business. A company should able to change its strategies, which

will increase the liquidity position of the company.

Debt Ratio

This ratio shows how the company is able to finance their total asset in the business as

it should able to have proper composition of asset in the company business, it helps them to

know how the company has financed their total asset in the business this will help them to

know the financial position of company business (Jacoby and Levy 2016). It should able to

have a proper ratio as this will help them to gain more amount of business in the market.

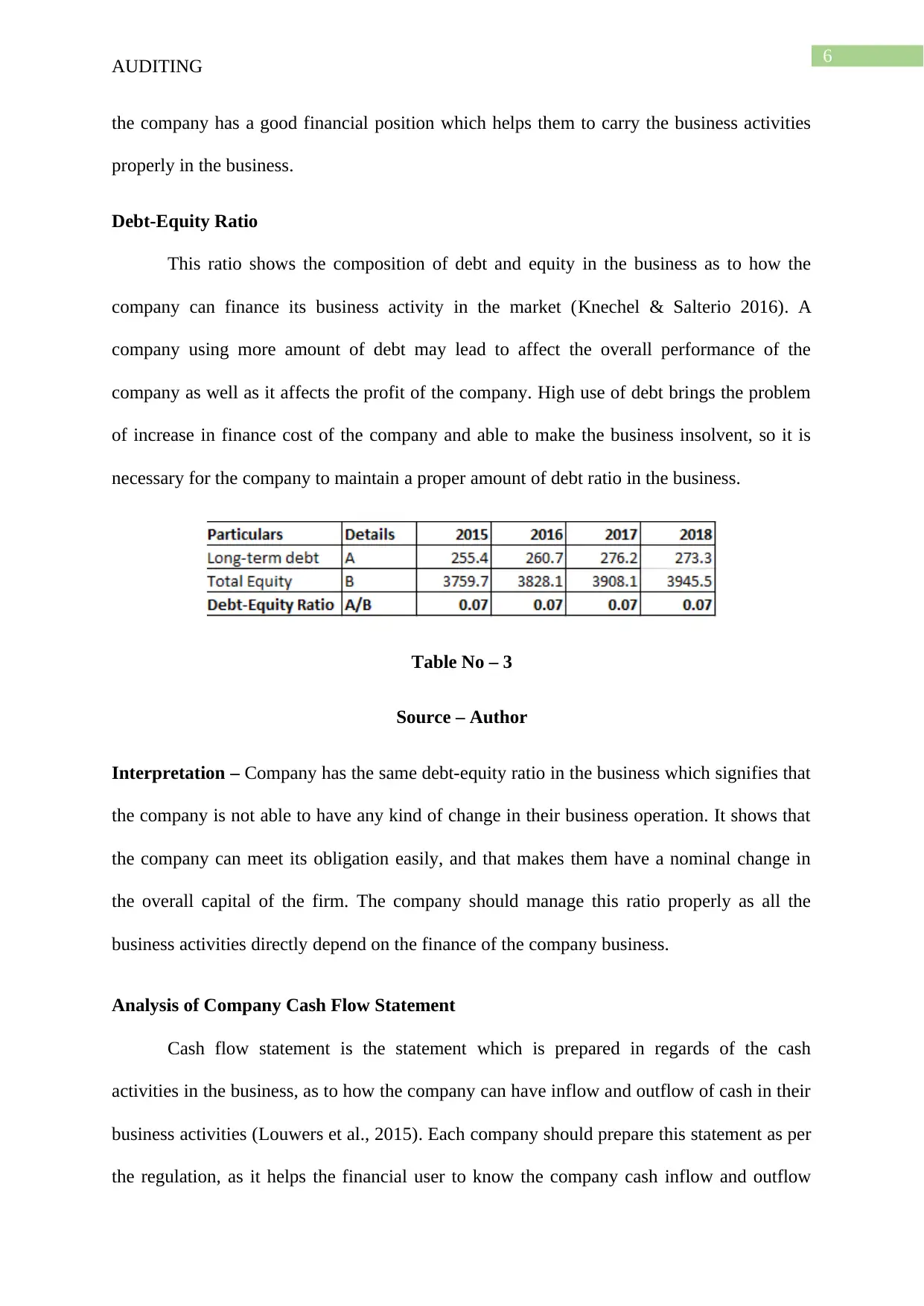

Table No – 2

Source – Author

Interpretation – The above table show the debt ratio of the company as it should be proper

so that the investors will able to invest in the company business, as the above ratio is concern

it can see that there is a decrease in the ratio, so it shows that the company is able to have an

increase in the total asset or there is reduction in overall debt of the company. It shows that

AUDITING

Source - Author

Interpretation – The above ratio shows about the liquidity of company as it should be more

than, so it will show the company having the proper amount of cash in the company business,

as the company is having less than 2 so this signifies it is not able to maintain an appropriate

liquidity position in the company business activities. It can be seen that in 2017 it was 1.13

and in 2018 it is 1.14 so this show there is a slight increase in the current company ratio thus

this denotes that the company can increase their current ratio, so they will able to gain proper

investment in the company business. A company should able to change its strategies, which

will increase the liquidity position of the company.

Debt Ratio

This ratio shows how the company is able to finance their total asset in the business as

it should able to have proper composition of asset in the company business, it helps them to

know how the company has financed their total asset in the business this will help them to

know the financial position of company business (Jacoby and Levy 2016). It should able to

have a proper ratio as this will help them to gain more amount of business in the market.

Table No – 2

Source – Author

Interpretation – The above table show the debt ratio of the company as it should be proper

so that the investors will able to invest in the company business, as the above ratio is concern

it can see that there is a decrease in the ratio, so it shows that the company is able to have an

increase in the total asset or there is reduction in overall debt of the company. It shows that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

the company has a good financial position which helps them to carry the business activities

properly in the business.

Debt-Equity Ratio

This ratio shows the composition of debt and equity in the business as to how the

company can finance its business activity in the market (Knechel & Salterio 2016). A

company using more amount of debt may lead to affect the overall performance of the

company as well as it affects the profit of the company. High use of debt brings the problem

of increase in finance cost of the company and able to make the business insolvent, so it is

necessary for the company to maintain a proper amount of debt ratio in the business.

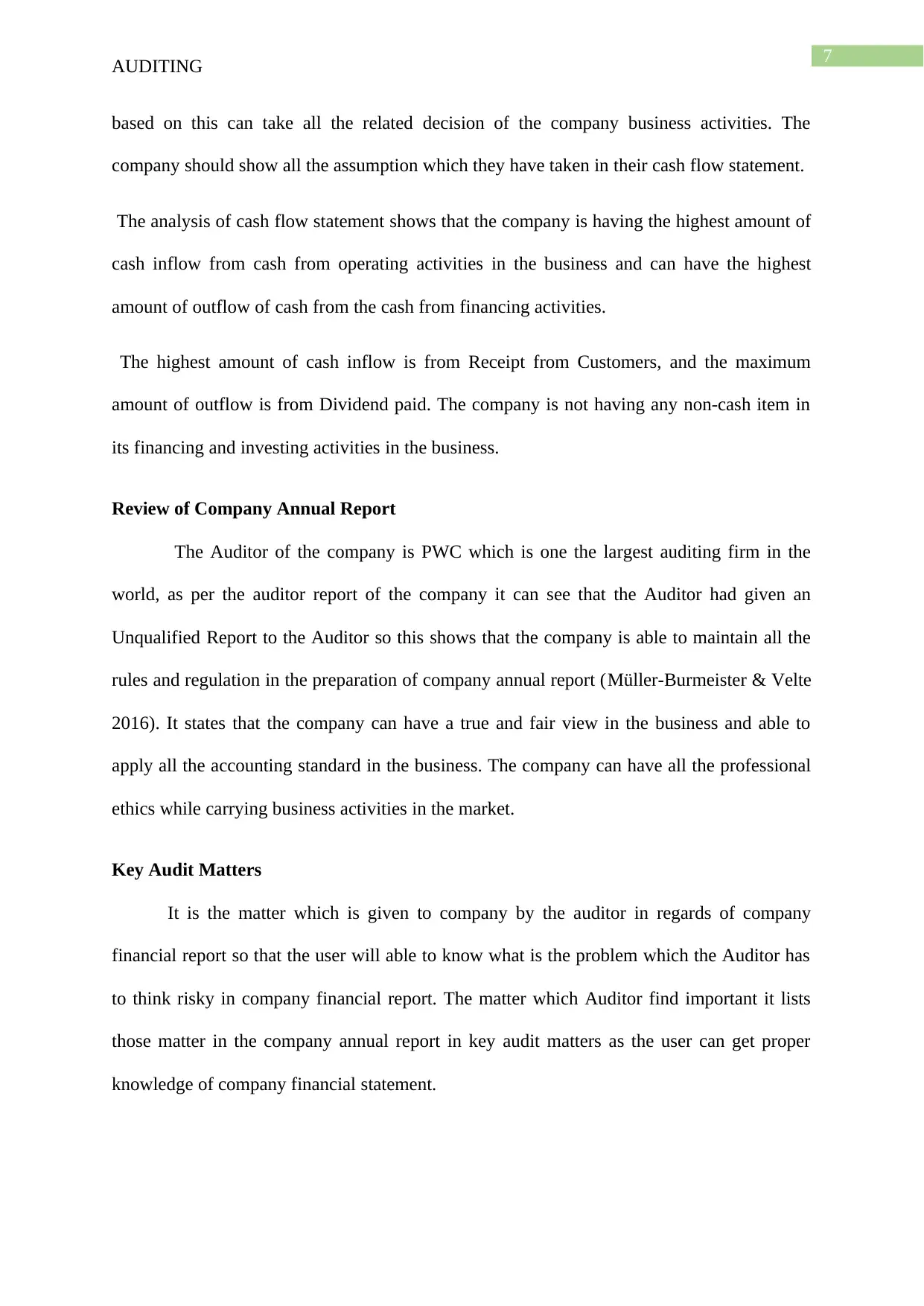

Table No – 3

Source – Author

Interpretation – Company has the same debt-equity ratio in the business which signifies that

the company is not able to have any kind of change in their business operation. It shows that

the company can meet its obligation easily, and that makes them have a nominal change in

the overall capital of the firm. The company should manage this ratio properly as all the

business activities directly depend on the finance of the company business.

Analysis of Company Cash Flow Statement

Cash flow statement is the statement which is prepared in regards of the cash

activities in the business, as to how the company can have inflow and outflow of cash in their

business activities (Louwers et al., 2015). Each company should prepare this statement as per

the regulation, as it helps the financial user to know the company cash inflow and outflow

AUDITING

the company has a good financial position which helps them to carry the business activities

properly in the business.

Debt-Equity Ratio

This ratio shows the composition of debt and equity in the business as to how the

company can finance its business activity in the market (Knechel & Salterio 2016). A

company using more amount of debt may lead to affect the overall performance of the

company as well as it affects the profit of the company. High use of debt brings the problem

of increase in finance cost of the company and able to make the business insolvent, so it is

necessary for the company to maintain a proper amount of debt ratio in the business.

Table No – 3

Source – Author

Interpretation – Company has the same debt-equity ratio in the business which signifies that

the company is not able to have any kind of change in their business operation. It shows that

the company can meet its obligation easily, and that makes them have a nominal change in

the overall capital of the firm. The company should manage this ratio properly as all the

business activities directly depend on the finance of the company business.

Analysis of Company Cash Flow Statement

Cash flow statement is the statement which is prepared in regards of the cash

activities in the business, as to how the company can have inflow and outflow of cash in their

business activities (Louwers et al., 2015). Each company should prepare this statement as per

the regulation, as it helps the financial user to know the company cash inflow and outflow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

based on this can take all the related decision of the company business activities. The

company should show all the assumption which they have taken in their cash flow statement.

The analysis of cash flow statement shows that the company is having the highest amount of

cash inflow from cash from operating activities in the business and can have the highest

amount of outflow of cash from the cash from financing activities.

The highest amount of cash inflow is from Receipt from Customers, and the maximum

amount of outflow is from Dividend paid. The company is not having any non-cash item in

its financing and investing activities in the business.

Review of Company Annual Report

The Auditor of the company is PWC which is one the largest auditing firm in the

world, as per the auditor report of the company it can see that the Auditor had given an

Unqualified Report to the Auditor so this shows that the company is able to maintain all the

rules and regulation in the preparation of company annual report (Müller-Burmeister & Velte

2016). It states that the company can have a true and fair view in the business and able to

apply all the accounting standard in the business. The company can have all the professional

ethics while carrying business activities in the market.

Key Audit Matters

It is the matter which is given to company by the auditor in regards of company

financial report so that the user will able to know what is the problem which the Auditor has

to think risky in company financial report. The matter which Auditor find important it lists

those matter in the company annual report in key audit matters as the user can get proper

knowledge of company financial statement.

AUDITING

based on this can take all the related decision of the company business activities. The

company should show all the assumption which they have taken in their cash flow statement.

The analysis of cash flow statement shows that the company is having the highest amount of

cash inflow from cash from operating activities in the business and can have the highest

amount of outflow of cash from the cash from financing activities.

The highest amount of cash inflow is from Receipt from Customers, and the maximum

amount of outflow is from Dividend paid. The company is not having any non-cash item in

its financing and investing activities in the business.

Review of Company Annual Report

The Auditor of the company is PWC which is one the largest auditing firm in the

world, as per the auditor report of the company it can see that the Auditor had given an

Unqualified Report to the Auditor so this shows that the company is able to maintain all the

rules and regulation in the preparation of company annual report (Müller-Burmeister & Velte

2016). It states that the company can have a true and fair view in the business and able to

apply all the accounting standard in the business. The company can have all the professional

ethics while carrying business activities in the market.

Key Audit Matters

It is the matter which is given to company by the auditor in regards of company

financial report so that the user will able to know what is the problem which the Auditor has

to think risky in company financial report. The matter which Auditor find important it lists

those matter in the company annual report in key audit matters as the user can get proper

knowledge of company financial statement.

8

AUDITING

Conclusion

The report concludes about the auditing process in the company as to how the Auditor

can carry its procedure to gain audit evidence in regards to company financial statement. It

also shows about the Auditor, as the Auditor has to ascertain the business risk and able to

carry its process to know about the company financial statement, the Auditor has to give a

proper opinion whether the company has a true and fair view or not. The report concludes the

auditing process in the company ASX Limited; it shows the materiality which is there in the

company financial statement as it is the error and omission which happen due to human error.

It shows the planning materiality which the Auditor has to ascertain in regards to the

company and how it able to carry its audit process in the company financial statement. It also

concludes on the company financial performance and the analysis of the same done with the

help of financial ratio of the company. Lastly, the report concludes about the analysis of

company cash flow statement and auditor report as the Auditor has given the company an

Unqualified report in the business.

AUDITING

Conclusion

The report concludes about the auditing process in the company as to how the Auditor

can carry its procedure to gain audit evidence in regards to company financial statement. It

also shows about the Auditor, as the Auditor has to ascertain the business risk and able to

carry its process to know about the company financial statement, the Auditor has to give a

proper opinion whether the company has a true and fair view or not. The report concludes the

auditing process in the company ASX Limited; it shows the materiality which is there in the

company financial statement as it is the error and omission which happen due to human error.

It shows the planning materiality which the Auditor has to ascertain in regards to the

company and how it able to carry its audit process in the company financial statement. It also

concludes on the company financial performance and the analysis of the same done with the

help of financial ratio of the company. Lastly, the report concludes about the analysis of

company cash flow statement and auditor report as the Auditor has given the company an

Unqualified report in the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

Reference

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

AUDITING

Reference

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

international standard setting. International Journal of Critical Accounting, 8(3-4),

227-245.

Power, M. K., & Gendron, Y. (2015). Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), 147-165.

Reid, L. C. (2015). Are auditor and audit committee report changes useful to investors?

Evidence from the United Kingdom.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Wang, B., Li, B., & Li, H. (2014). Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), 43-56.

AUDITING

international standard setting. International Journal of Critical Accounting, 8(3-4),

227-245.

Power, M. K., & Gendron, Y. (2015). Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), 147-165.

Reid, L. C. (2015). Are auditor and audit committee report changes useful to investors?

Evidence from the United Kingdom.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Wang, B., Li, B., & Li, H. (2014). Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), 43-56.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.