CQUniversity: ACCT20075 Auditing and Ethics Report - STW Fund Analysis

VerifiedAdded on 2022/12/21

|12

|2731

|45

Report

AI Summary

This report presents a comprehensive analysis of auditing and ethics, focusing on the financial performance of STW (SPDR S&P/ASX 200 Fund). The report begins by determining materiality, calculating quantitative estimates based on various benchmarks, and justifying the chosen materiality level. It then reviews the annual report's draft notes and disclosures, identifying significant items requiring further verification. Key risk areas are identified through ratio analysis, including expense ratio, debt ratio, and net earnings to total assets, along with relevant audit assertions and procedures. The report evaluates the going concern risk by analyzing the cash flow statement, assessing the impact of operating and financing activities. Finally, it reviews the auditor's opinion and report, addressing audit issues related to the valuation and existence of investments. The analysis concludes by highlighting key risky areas and confirming the financial statements' fair presentation, while acknowledging an audit risk concerning investment valuation.

Running head: AUDITING AND ETHICS

Auditing and ethics

Name of the Student

Name of the University

Author’s note

Auditing and ethics

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Section 1:....................................................................................................................................2

Determining the materiality in the audit plan for the year 2018:...............................................2

Reviewing various draft notes and disclosures in the annual report of the company:...............2

Section 2:....................................................................................................................................2

Identifying the key risk areas for audit:.....................................................................................2

Section 3:....................................................................................................................................3

Evaluating the going concern risk by reviewing the cash flow:................................................3

Reviewing the opinions and audit report of the auditors of company for financial year 2018:.3

Conclusion:................................................................................................................................3

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Section 1:....................................................................................................................................2

Determining the materiality in the audit plan for the year 2018:...............................................2

Reviewing various draft notes and disclosures in the annual report of the company:...............2

Section 2:....................................................................................................................................2

Identifying the key risk areas for audit:.....................................................................................2

Section 3:....................................................................................................................................3

Evaluating the going concern risk by reviewing the cash flow:................................................3

Reviewing the opinions and audit report of the auditors of company for financial year 2018:.3

Conclusion:................................................................................................................................3

2AUDITING AND ETHICS

Introduction:

In this report, the development of audit plan of the company has been demonstrated

and the first section addressing the requirement is to determine the materiality by evaluating

the factors. The chosen company for the assessment is STW which is an exchange traded

fund tracking the performance S & P/ASX 200 index. Investment is made by the fund is done

in the securities comprising the index in proportion to the relative weightings. Such index is

comprised of most liquid securities in Australia and 200 largest securities by market

capitalization. The analysis will be confined to SPDR S&P/ASX 200 Fund of the company.

The disclosures and the draft notes accompanying in the annual report of the company has

been examined. All the relevant information are retrieved from the financial report that is

used for preparing analytical review. Tool of ratio analysis is implemented for outlining the

changes in the ratio and apparent trend of the financials. For each of the identified ratio,

relevant assertions are determined along with the audit procedure. In addition to this, cash

flow statement of the company has been reviewed for evaluating the gong concern risk faced

by the company and recommendation is made by referring to ASA 700 (Bennett & Hatfield,

2017). Later section of the report conducts a review of the opinion and the auditor’s report for

addressing the audit issues.

Discussion:

Section 1:

Determining the materiality in the audit plan for the year 2018:

Auditors are provided with the reference frame when they discuss about the

materiality which is determined by the preparation and presentation of the financial

statements. Identification of performance materiality at the planning stage of audit is

primarily required for determining materiality. Materiality factor is considered to be crucial

Introduction:

In this report, the development of audit plan of the company has been demonstrated

and the first section addressing the requirement is to determine the materiality by evaluating

the factors. The chosen company for the assessment is STW which is an exchange traded

fund tracking the performance S & P/ASX 200 index. Investment is made by the fund is done

in the securities comprising the index in proportion to the relative weightings. Such index is

comprised of most liquid securities in Australia and 200 largest securities by market

capitalization. The analysis will be confined to SPDR S&P/ASX 200 Fund of the company.

The disclosures and the draft notes accompanying in the annual report of the company has

been examined. All the relevant information are retrieved from the financial report that is

used for preparing analytical review. Tool of ratio analysis is implemented for outlining the

changes in the ratio and apparent trend of the financials. For each of the identified ratio,

relevant assertions are determined along with the audit procedure. In addition to this, cash

flow statement of the company has been reviewed for evaluating the gong concern risk faced

by the company and recommendation is made by referring to ASA 700 (Bennett & Hatfield,

2017). Later section of the report conducts a review of the opinion and the auditor’s report for

addressing the audit issues.

Discussion:

Section 1:

Determining the materiality in the audit plan for the year 2018:

Auditors are provided with the reference frame when they discuss about the

materiality which is determined by the preparation and presentation of the financial

statements. Identification of performance materiality at the planning stage of audit is

primarily required for determining materiality. Materiality factor is considered to be crucial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

in the audit procedure as the concept is applied by the auditors in determining the existing

material misstatement which leads to uncertainty. Materiality is determined by using three

steps that is selecting the appropriate benchmark, considering an appropriate percentage of

benchmark for determining materiality and choice justification. The concept of materiality is

applied by the auditors at the planning stage when evaluating the impact of any identified

material misstatements in the financial report of the organization. However, there exist some

of the practical issues associated with materiality such as accumulation of misstatements,

assessing materiality misstatement and categorization of the misstatements.

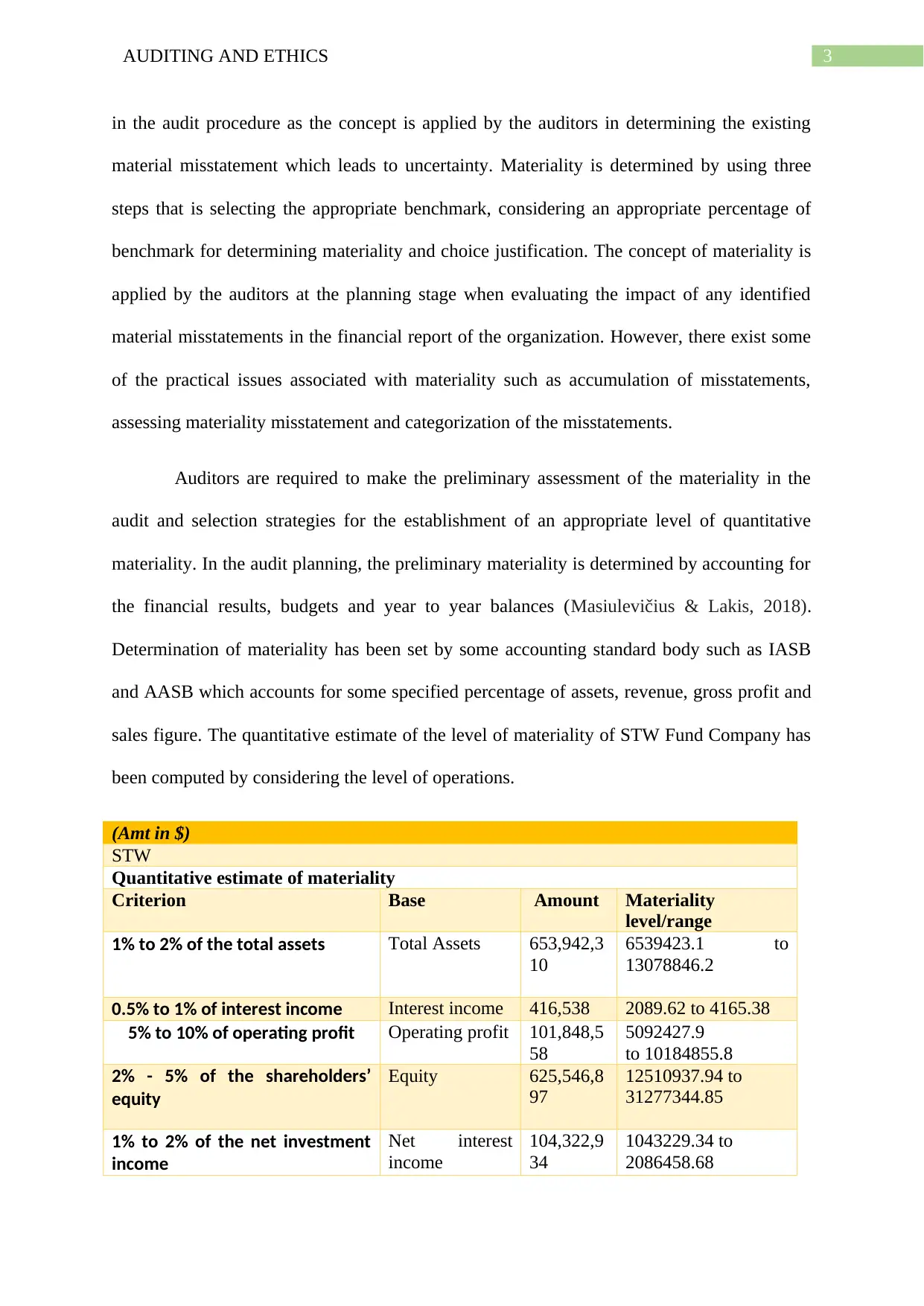

Auditors are required to make the preliminary assessment of the materiality in the

audit and selection strategies for the establishment of an appropriate level of quantitative

materiality. In the audit planning, the preliminary materiality is determined by accounting for

the financial results, budgets and year to year balances (Masiulevičius & Lakis, 2018).

Determination of materiality has been set by some accounting standard body such as IASB

and AASB which accounts for some specified percentage of assets, revenue, gross profit and

sales figure. The quantitative estimate of the level of materiality of STW Fund Company has

been computed by considering the level of operations.

(Amt in $)

STW

Quantitative estimate of materiality

Criterion Base Amount Materiality

level/range

1% to 2% of the total assets Total Assets 653,942,3

10

6539423.1 to

13078846.2

0.5% to 1% of interest income Interest income 416,538 2089.62 to 4165.38

5% to 10% of operating profit Operating profit 101,848,5

58

5092427.9

to 10184855.8

2% - 5% of the shareholders’

equity

Equity 625,546,8

97

12510937.94 to

31277344.85

1% to 2% of the net investment

income

Net interest

income

104,322,9

34

1043229.34 to

2086458.68

in the audit procedure as the concept is applied by the auditors in determining the existing

material misstatement which leads to uncertainty. Materiality is determined by using three

steps that is selecting the appropriate benchmark, considering an appropriate percentage of

benchmark for determining materiality and choice justification. The concept of materiality is

applied by the auditors at the planning stage when evaluating the impact of any identified

material misstatements in the financial report of the organization. However, there exist some

of the practical issues associated with materiality such as accumulation of misstatements,

assessing materiality misstatement and categorization of the misstatements.

Auditors are required to make the preliminary assessment of the materiality in the

audit and selection strategies for the establishment of an appropriate level of quantitative

materiality. In the audit planning, the preliminary materiality is determined by accounting for

the financial results, budgets and year to year balances (Masiulevičius & Lakis, 2018).

Determination of materiality has been set by some accounting standard body such as IASB

and AASB which accounts for some specified percentage of assets, revenue, gross profit and

sales figure. The quantitative estimate of the level of materiality of STW Fund Company has

been computed by considering the level of operations.

(Amt in $)

STW

Quantitative estimate of materiality

Criterion Base Amount Materiality

level/range

1% to 2% of the total assets Total Assets 653,942,3

10

6539423.1 to

13078846.2

0.5% to 1% of interest income Interest income 416,538 2089.62 to 4165.38

5% to 10% of operating profit Operating profit 101,848,5

58

5092427.9

to 10184855.8

2% - 5% of the shareholders’

equity

Equity 625,546,8

97

12510937.94 to

31277344.85

1% to 2% of the net investment

income

Net interest

income

104,322,9

34

1043229.34 to

2086458.68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

The above table depicts the quantitative estimates of the materiality which has been

calculated by setting the benchmark provided by the accounting standard. The quantitative

estimate of materiality of STW should be between $ 6539423.1 and $ 13078846.2 as

considering the activities of the company, this is the most appropriate level. The rationale for

selecting interest income as the basis of materiality is that selection of such accounts would

help in ensuring that none of the accounts in the preliminary assessment is being ignored.

Reviewing various draft notes and disclosures in the annual report of the company:

On reviewing drafts and disclosure in the annual report of STW, some of the

accounts that are significant in the auditing procedure and needs further verification include

expenses account on the items such as administrator and custody fees as in the financial year

2019, no such fees was applicable as against $ 717,313 in the financial year 2018. In addition

to this, there has been considerable increase in the figures of other operating income and the

net cash flow from operating activities has also increased which needs to be accounted for. It

is required by the auditors to check the mathematical accuracy using appropriate techniques.

Total amount of cash and cash equivalent at the end of the financial year 2019 has increased

considerably which should be scrutinized. Furthermore, in the current year, no financial

instruments was held by fund using observable inputs. It is mentioned in the notes that no

financial instruments was held by fund at the fair value in the statement of financial position

(Choudhary et al., 2019). Therefore, this area is susceptible to materiality as the financial

instruments are measured at the fair value when recognising in the financial statements.

The above table depicts the quantitative estimates of the materiality which has been

calculated by setting the benchmark provided by the accounting standard. The quantitative

estimate of materiality of STW should be between $ 6539423.1 and $ 13078846.2 as

considering the activities of the company, this is the most appropriate level. The rationale for

selecting interest income as the basis of materiality is that selection of such accounts would

help in ensuring that none of the accounts in the preliminary assessment is being ignored.

Reviewing various draft notes and disclosures in the annual report of the company:

On reviewing drafts and disclosure in the annual report of STW, some of the

accounts that are significant in the auditing procedure and needs further verification include

expenses account on the items such as administrator and custody fees as in the financial year

2019, no such fees was applicable as against $ 717,313 in the financial year 2018. In addition

to this, there has been considerable increase in the figures of other operating income and the

net cash flow from operating activities has also increased which needs to be accounted for. It

is required by the auditors to check the mathematical accuracy using appropriate techniques.

Total amount of cash and cash equivalent at the end of the financial year 2019 has increased

considerably which should be scrutinized. Furthermore, in the current year, no financial

instruments was held by fund using observable inputs. It is mentioned in the notes that no

financial instruments was held by fund at the fair value in the statement of financial position

(Choudhary et al., 2019). Therefore, this area is susceptible to materiality as the financial

instruments are measured at the fair value when recognising in the financial statements.

5AUDITING AND ETHICS

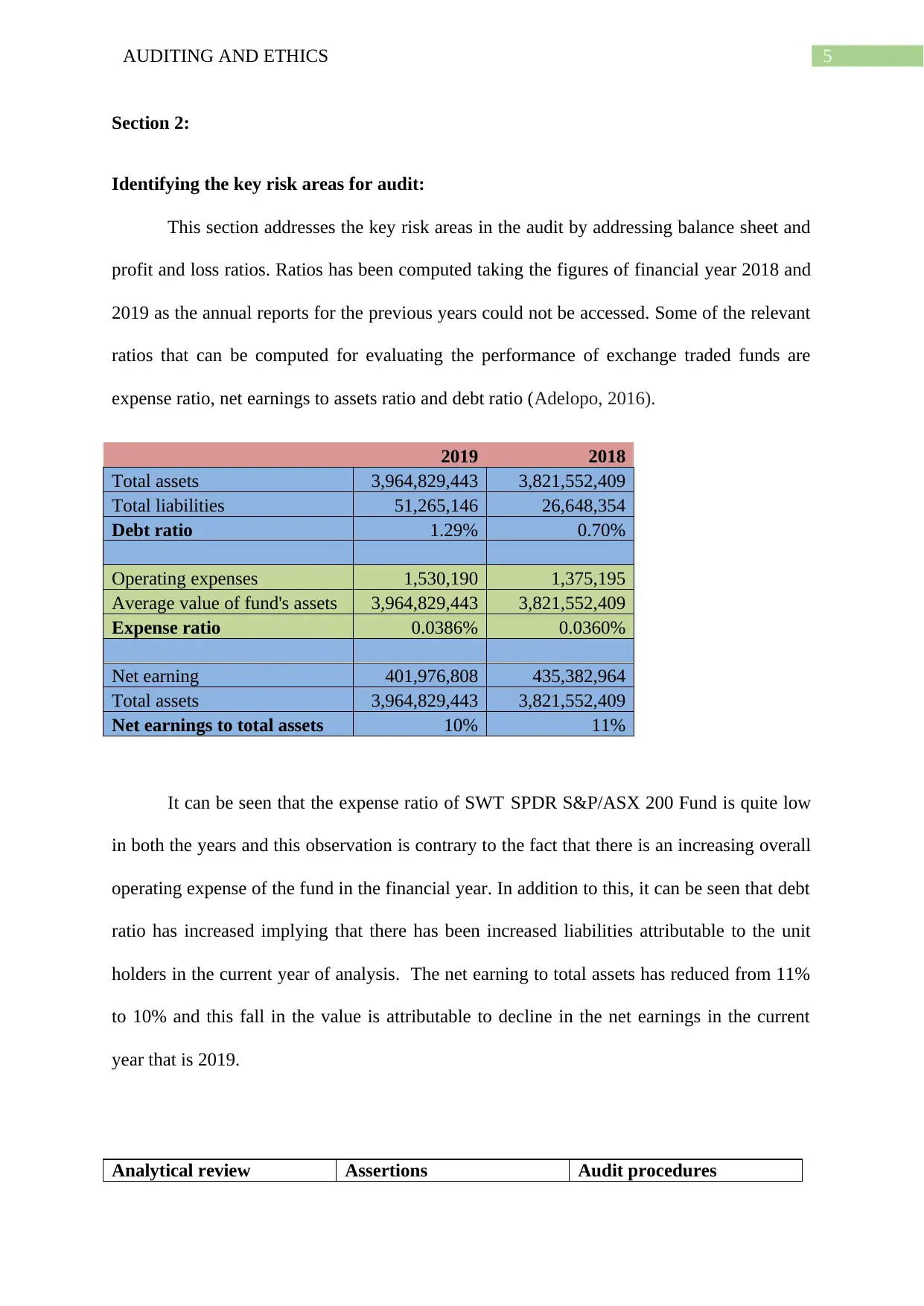

Section 2:

Identifying the key risk areas for audit:

This section addresses the key risk areas in the audit by addressing balance sheet and

profit and loss ratios. Ratios has been computed taking the figures of financial year 2018 and

2019 as the annual reports for the previous years could not be accessed. Some of the relevant

ratios that can be computed for evaluating the performance of exchange traded funds are

expense ratio, net earnings to assets ratio and debt ratio (Adelopo, 2016).

2019 2018

Total assets 3,964,829,443 3,821,552,409

Total liabilities 51,265,146 26,648,354

Debt ratio 1.29% 0.70%

Operating expenses 1,530,190 1,375,195

Average value of fund's assets 3,964,829,443 3,821,552,409

Expense ratio 0.0386% 0.0360%

Net earning 401,976,808 435,382,964

Total assets 3,964,829,443 3,821,552,409

Net earnings to total assets 10% 11%

It can be seen that the expense ratio of SWT SPDR S&P/ASX 200 Fund is quite low

in both the years and this observation is contrary to the fact that there is an increasing overall

operating expense of the fund in the financial year. In addition to this, it can be seen that debt

ratio has increased implying that there has been increased liabilities attributable to the unit

holders in the current year of analysis. The net earning to total assets has reduced from 11%

to 10% and this fall in the value is attributable to decline in the net earnings in the current

year that is 2019.

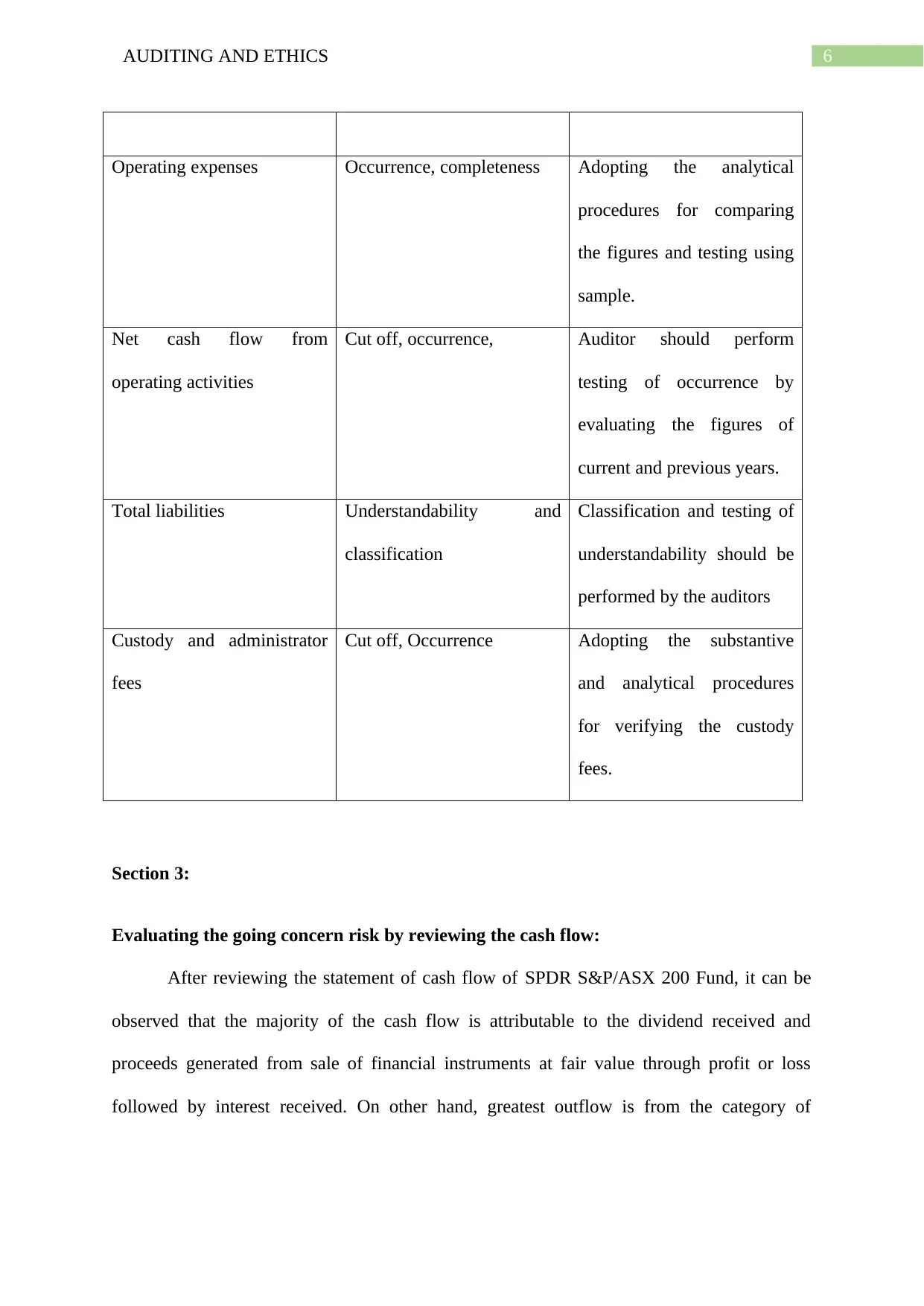

Analytical review Assertions Audit procedures

Section 2:

Identifying the key risk areas for audit:

This section addresses the key risk areas in the audit by addressing balance sheet and

profit and loss ratios. Ratios has been computed taking the figures of financial year 2018 and

2019 as the annual reports for the previous years could not be accessed. Some of the relevant

ratios that can be computed for evaluating the performance of exchange traded funds are

expense ratio, net earnings to assets ratio and debt ratio (Adelopo, 2016).

2019 2018

Total assets 3,964,829,443 3,821,552,409

Total liabilities 51,265,146 26,648,354

Debt ratio 1.29% 0.70%

Operating expenses 1,530,190 1,375,195

Average value of fund's assets 3,964,829,443 3,821,552,409

Expense ratio 0.0386% 0.0360%

Net earning 401,976,808 435,382,964

Total assets 3,964,829,443 3,821,552,409

Net earnings to total assets 10% 11%

It can be seen that the expense ratio of SWT SPDR S&P/ASX 200 Fund is quite low

in both the years and this observation is contrary to the fact that there is an increasing overall

operating expense of the fund in the financial year. In addition to this, it can be seen that debt

ratio has increased implying that there has been increased liabilities attributable to the unit

holders in the current year of analysis. The net earning to total assets has reduced from 11%

to 10% and this fall in the value is attributable to decline in the net earnings in the current

year that is 2019.

Analytical review Assertions Audit procedures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

Operating expenses Occurrence, completeness Adopting the analytical

procedures for comparing

the figures and testing using

sample.

Net cash flow from

operating activities

Cut off, occurrence, Auditor should perform

testing of occurrence by

evaluating the figures of

current and previous years.

Total liabilities Understandability and

classification

Classification and testing of

understandability should be

performed by the auditors

Custody and administrator

fees

Cut off, Occurrence Adopting the substantive

and analytical procedures

for verifying the custody

fees.

Section 3:

Evaluating the going concern risk by reviewing the cash flow:

After reviewing the statement of cash flow of SPDR S&P/ASX 200 Fund, it can be

observed that the majority of the cash flow is attributable to the dividend received and

proceeds generated from sale of financial instruments at fair value through profit or loss

followed by interest received. On other hand, greatest outflow is from the category of

Operating expenses Occurrence, completeness Adopting the analytical

procedures for comparing

the figures and testing using

sample.

Net cash flow from

operating activities

Cut off, occurrence, Auditor should perform

testing of occurrence by

evaluating the figures of

current and previous years.

Total liabilities Understandability and

classification

Classification and testing of

understandability should be

performed by the auditors

Custody and administrator

fees

Cut off, Occurrence Adopting the substantive

and analytical procedures

for verifying the custody

fees.

Section 3:

Evaluating the going concern risk by reviewing the cash flow:

After reviewing the statement of cash flow of SPDR S&P/ASX 200 Fund, it can be

observed that the majority of the cash flow is attributable to the dividend received and

proceeds generated from sale of financial instruments at fair value through profit or loss

followed by interest received. On other hand, greatest outflow is from the category of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

purchasing financial instruments at fair value through profit or loss and the fees paid to the

investment manager (William et al., 2016).

The primary cash receipt is from the sale of financial instruments and the amount

received from brokers for margin. Primary cash payment is made in terms of purchase of

financial instruments at fair value through profit and loss. Some of the non-cash financing

activities include the satisfaction of application by an in specie asset transfer, satisfaction of

redemption by an in specie asset transfer and payment made to the distributions by issuing

unit under the plan of distribution reinvestment (Brennan, 2016).

The going concern risk of the company can be evaluated by determining the

appropriateness of the disclosures relating to the cash flow. Existence of the material

uncertainty might cause the auditors to cast considerable doubts on the ability of the entity to

continue as a going concern (Auasb.gov.au, 2019). It can be concluded from analysing the

status of the cash flow of the company that the assumptions of the going concern holds good

as it there is a positive impact on the operating and the financing activities. This is depicted in

the increased value as the net cash inflow from operating and financing activities has

increased. However, it is required by the auditors to enquire about the increasing operating

expenses and adopt proper auditing techniques to address such risks.

Reviewing the opinions and audit report of the auditors of company for financial year

2018:

The financial report of STW has been audited by Pwc who opined that the report is

prepared in accordance with the Corporation Act, 2011 and adheres to Corporations

regulation 2001 and Australian accounting standard. In addition to this, financial statements

of the company provide a fair and true view of the financial position of the company as on

30th June, 2019. The basis of opinion is the framework of the Australian Auditing standards

purchasing financial instruments at fair value through profit or loss and the fees paid to the

investment manager (William et al., 2016).

The primary cash receipt is from the sale of financial instruments and the amount

received from brokers for margin. Primary cash payment is made in terms of purchase of

financial instruments at fair value through profit and loss. Some of the non-cash financing

activities include the satisfaction of application by an in specie asset transfer, satisfaction of

redemption by an in specie asset transfer and payment made to the distributions by issuing

unit under the plan of distribution reinvestment (Brennan, 2016).

The going concern risk of the company can be evaluated by determining the

appropriateness of the disclosures relating to the cash flow. Existence of the material

uncertainty might cause the auditors to cast considerable doubts on the ability of the entity to

continue as a going concern (Auasb.gov.au, 2019). It can be concluded from analysing the

status of the cash flow of the company that the assumptions of the going concern holds good

as it there is a positive impact on the operating and the financing activities. This is depicted in

the increased value as the net cash inflow from operating and financing activities has

increased. However, it is required by the auditors to enquire about the increasing operating

expenses and adopt proper auditing techniques to address such risks.

Reviewing the opinions and audit report of the auditors of company for financial year

2018:

The financial report of STW has been audited by Pwc who opined that the report is

prepared in accordance with the Corporation Act, 2011 and adheres to Corporations

regulation 2001 and Australian accounting standard. In addition to this, financial statements

of the company provide a fair and true view of the financial position of the company as on

30th June, 2019. The basis of opinion is the framework of the Australian Auditing standards

8AUDITING AND ETHICS

and obtaining of sufficient and appropriate audit evidences. The scope of audit has been

tailored so that the opinion of the report can be provided as a whole (Ferramosca et al., 2017).

In addition to this, there are additional sections depicting the key audit matters that

has significant value in determining the materiality and thereby risk assertions. Audit issues is

associated with valuation and existence of investment for which the auditors adopted

appropriate procedure to address the risk. Valuation and existence of investment is regarded

as the audit issue because the principal elements of the statement of financial position is

represented by financial assets and liabilities as they accounted for the majority of net assets

(Ssga.com, 2019). The net assets that are attributable to the unit holders has the risk of being

materially misstated if there is any discrepancy in the existence or valuation of the

investments. Such discrepancy would also impact the performance of funds as the main

driver in the movement of the fund’s profitability is the valuation of financial assets and

liabilities.

Conclusion:

From the analysis of the financial report of STW of SPDR S&P/ASX 200 Fund, it has

been found that there are some key risky areas which could have material impact on the

financial performance of fund. One of the major area of concern is the increasing operating

expenses that has caused expense ratio to shoot up. Reviewing of the cash flow provides us

the information about the risk associated with the going concern and it has been found that

the cash position of fund is healthy. In addition to this, analysis of the opinion of the auditor’s

report of the company, it is inferred that the financial statements are not materially misstated

and they present true financial position. However, there exist one audit risk concerning the

existence and valuation of investment.

and obtaining of sufficient and appropriate audit evidences. The scope of audit has been

tailored so that the opinion of the report can be provided as a whole (Ferramosca et al., 2017).

In addition to this, there are additional sections depicting the key audit matters that

has significant value in determining the materiality and thereby risk assertions. Audit issues is

associated with valuation and existence of investment for which the auditors adopted

appropriate procedure to address the risk. Valuation and existence of investment is regarded

as the audit issue because the principal elements of the statement of financial position is

represented by financial assets and liabilities as they accounted for the majority of net assets

(Ssga.com, 2019). The net assets that are attributable to the unit holders has the risk of being

materially misstated if there is any discrepancy in the existence or valuation of the

investments. Such discrepancy would also impact the performance of funds as the main

driver in the movement of the fund’s profitability is the valuation of financial assets and

liabilities.

Conclusion:

From the analysis of the financial report of STW of SPDR S&P/ASX 200 Fund, it has

been found that there are some key risky areas which could have material impact on the

financial performance of fund. One of the major area of concern is the increasing operating

expenses that has caused expense ratio to shoot up. Reviewing of the cash flow provides us

the information about the risk associated with the going concern and it has been found that

the cash position of fund is healthy. In addition to this, analysis of the opinion of the auditor’s

report of the company, it is inferred that the financial statements are not materially misstated

and they present true financial position. However, there exist one audit risk concerning the

existence and valuation of investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

References list:

Adelopo, I. (2016). Auditor Independence: Auditing, Corporate Governance and Market

Confidence. Routledge. (https://www.taylorfrancis.com/books/9781315568300)

Auasb.gov.au. (2019). Retrieved 5 September 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_700_Compiled_2019-

FRL.pdf

Audsabumrungrat, J., Pornupatham, S., & Tan, H. T. (2015). Joint Impact of Materiality

Guidance and Justification Requirement on Auditors' Planning

Materiality. Behavioral Research in Accounting, 28(2), 17-27.

Bennett, G. B., & Hatfield, R. C. (2017). Do approaching deadlines influence auditors'

materiality assessments?. Auditing: A Journal of Practice & Theory, 36(4), 29-48.

(https://www.aaajournals.org/doi/abs/10.2308/ajpt-51683)

Brennan, N. (2016). Are Ethics Relevant to the Practice of Professional

Accounting?. Accountancy Plus, (1), 23-24.

References list:

Adelopo, I. (2016). Auditor Independence: Auditing, Corporate Governance and Market

Confidence. Routledge. (https://www.taylorfrancis.com/books/9781315568300)

Auasb.gov.au. (2019). Retrieved 5 September 2019, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_700_Compiled_2019-

FRL.pdf

Audsabumrungrat, J., Pornupatham, S., & Tan, H. T. (2015). Joint Impact of Materiality

Guidance and Justification Requirement on Auditors' Planning

Materiality. Behavioral Research in Accounting, 28(2), 17-27.

Bennett, G. B., & Hatfield, R. C. (2017). Do approaching deadlines influence auditors'

materiality assessments?. Auditing: A Journal of Practice & Theory, 36(4), 29-48.

(https://www.aaajournals.org/doi/abs/10.2308/ajpt-51683)

Brennan, N. (2016). Are Ethics Relevant to the Practice of Professional

Accounting?. Accountancy Plus, (1), 23-24.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

Bringselius, L. (2018). Efficiency, economy and effectiveness—but what about ethics?

Supreme audit institutions at a critical juncture. Public Money & Management, 38(2),

105-110.

Choudhary, P., Merkley, K. J., & Schipper, K. (2019, March). Auditors’ Quantitative

Materiality Judgments: Properties and Implications for Financial Reporting

Reliability. In 28th Annual Conference on Financial Economics and Accounting.

(https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2958405)

Ferramosca, S., D'Onza, G., & Allegrini, M. (2017). The internal auditing of corporate

governance, risk management and ethics: comparing banks with other

industries. International Journal of Business Governance and Ethics, 12(3), 218-240.

García-Marzá, D. (2017). From ethical codes to ethical auditing: An ethical infrastructure for

corporate social responsibility communication. El profesional de la información

(EPI), 26(2), 268-276.

(http://www.elprofesionaldelainformacion.com/contenidos/2017/mar/13.html)

Masiulevičius, A., & Lakis, V. (2018). Differentiation of performance materiality in audit

based on business needs. Entrepreneurship and sustainability issues, 115-124.(

https://epublications.vu.lt/object/elaba:31188807/)

Sheikh, A. S. A. (2019). The impact of the auditor's compliance with the ethics of the

auditing profession on the quality of professional performance Theoretical

research. Qalaai Zanist Journal, 4(1).(

http://journal.lfu.edu.krd/index.php/Files/article/view/78)

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing: A

Bringselius, L. (2018). Efficiency, economy and effectiveness—but what about ethics?

Supreme audit institutions at a critical juncture. Public Money & Management, 38(2),

105-110.

Choudhary, P., Merkley, K. J., & Schipper, K. (2019, March). Auditors’ Quantitative

Materiality Judgments: Properties and Implications for Financial Reporting

Reliability. In 28th Annual Conference on Financial Economics and Accounting.

(https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2958405)

Ferramosca, S., D'Onza, G., & Allegrini, M. (2017). The internal auditing of corporate

governance, risk management and ethics: comparing banks with other

industries. International Journal of Business Governance and Ethics, 12(3), 218-240.

García-Marzá, D. (2017). From ethical codes to ethical auditing: An ethical infrastructure for

corporate social responsibility communication. El profesional de la información

(EPI), 26(2), 268-276.

(http://www.elprofesionaldelainformacion.com/contenidos/2017/mar/13.html)

Masiulevičius, A., & Lakis, V. (2018). Differentiation of performance materiality in audit

based on business needs. Entrepreneurship and sustainability issues, 115-124.(

https://epublications.vu.lt/object/elaba:31188807/)

Sheikh, A. S. A. (2019). The impact of the auditor's compliance with the ethics of the

auditing profession on the quality of professional performance Theoretical

research. Qalaai Zanist Journal, 4(1).(

http://journal.lfu.edu.krd/index.php/Files/article/view/78)

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and

assurance research: Trends, methodological issues, and opportunities. Auditing: A

11AUDITING AND ETHICS

Journal of Practice & Theory, 35(3), 1-32.

(https://www.aaajournals.org/doi/abs/10.2308/ajpt-51377)

Ssga.com. (2019). [online] Available at:

https://www.ssga.com/library-content/products/fund-docs/etfs/apac/au/ar/annual-

report-au-en-stw.pdf [Accessed 5 Sep. 2019].

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Journal of Practice & Theory, 35(3), 1-32.

(https://www.aaajournals.org/doi/abs/10.2308/ajpt-51377)

Ssga.com. (2019). [online] Available at:

https://www.ssga.com/library-content/products/fund-docs/etfs/apac/au/ar/annual-

report-au-en-stw.pdf [Accessed 5 Sep. 2019].

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.