Auditing and Materiality: Konekt Limited Financial Statement Analysis

VerifiedAdded on 2023/03/31

|15

|3409

|488

Report

AI Summary

This auditing report analyzes the financial statements of Konekt Limited, an Australian service industry company. It begins with an executive summary and introduction, providing an overview of the company and the concept of materiality in financial statements. The report identifies and discusses five significant accounts—Other Assets, Cash Account, Intangible Assets, Provisions, and Trade and Other Payables—highlighting potential material misstatements. It details the planning materiality, risk assessment procedures, and relevant auditing standards (ASA 300 and ASA 320). The report examines qualitative and quantitative aspects of materiality and includes a table showing the calculation of planning materiality based on the company's revenue. It concludes by emphasizing the importance of risk assessment in the audit process and references relevant sources. The report's structure includes an introduction, discussion, conclusion, and references, fulfilling the assignment brief's requirements for an audit planning document for an Audit Manager.

Running head: Auditing

Auditing

Name of the Student

Name of the University

Author Note

Auditing

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Auditing

Executive Summary

The assignment show about the auditing in the company and the materiality concept which is

there in the financial statement of the company. It also show about the planning materiality

and risk assessment procedure which is been carried by the auditor in regards of the financial

statement of the company.

Auditing

Executive Summary

The assignment show about the auditing in the company and the materiality concept which is

there in the financial statement of the company. It also show about the planning materiality

and risk assessment procedure which is been carried by the auditor in regards of the financial

statement of the company.

2

Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Company.....................................................................................................3

Materiality in the Company financial statement....................................................................4

Planning Materiality...............................................................................................................7

Risk Assessment in Audit......................................................................................................7

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Company.....................................................................................................3

Materiality in the Company financial statement....................................................................4

Planning Materiality...............................................................................................................7

Risk Assessment in Audit......................................................................................................7

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Auditing

Introduction

The process of the inspection and evaluation of the financial statement of the

company is known as auditing. This process is to be carried upon the financial statement of

the company so that it can be know that the company had comply with all the rules and

regulation while preparing the financial statement of the company1. The process of auditing is

can be carried by both the employee of the company and the external auditor of the company.

The internal audit is been carried by the employer of the company it is been done so that it

can able to inspect the strategies of the management so that it can able to know the mistake

which are there in the strategy and help the company to overcome the mistake in the

strategy2. External auditor are the one who carry it audit process in the company as it from

external source so it can able to give an independent opinion on the financial statement of the

company. It have to carry some procedure in the company business so that it can able to

know how the company is performing its activities and it will able to judge the risk which is

been associated in the company so that the auditor is able to know the materiality and

misstatement in the financial statement and able to carry the audit process as related to it in

the company financial statement3. The report show about the Konekt Limited which is listed

in Australia, it contain an details of the concept of materiality and also show about the 5

account which are there in the company having material misstatement of the company. It also

1 Brusca, Isabel, et al., eds. Public sector accounting and auditing in Europe: The challenge

of harmonization. Springer, 2016.

2 Cannon, Nathan H., and Jean C. Bedard. "Auditing challenging fair value measurements:

Evidence from the field." The Accounting Review 92.4 (2016): 81-114.

3 Chiu, Victoria, Qi Liu, and Miklos A. Vasarhelyi. "The Development and Intellectual

Structure of Continuous Auditing Research 1." Continuous Auditing: Theory and

Application. Emerald Publishing Limited, 2018. 53-85

Auditing

Introduction

The process of the inspection and evaluation of the financial statement of the

company is known as auditing. This process is to be carried upon the financial statement of

the company so that it can be know that the company had comply with all the rules and

regulation while preparing the financial statement of the company1. The process of auditing is

can be carried by both the employee of the company and the external auditor of the company.

The internal audit is been carried by the employer of the company it is been done so that it

can able to inspect the strategies of the management so that it can able to know the mistake

which are there in the strategy and help the company to overcome the mistake in the

strategy2. External auditor are the one who carry it audit process in the company as it from

external source so it can able to give an independent opinion on the financial statement of the

company. It have to carry some procedure in the company business so that it can able to

know how the company is performing its activities and it will able to judge the risk which is

been associated in the company so that the auditor is able to know the materiality and

misstatement in the financial statement and able to carry the audit process as related to it in

the company financial statement3. The report show about the Konekt Limited which is listed

in Australia, it contain an details of the concept of materiality and also show about the 5

account which are there in the company having material misstatement of the company. It also

1 Brusca, Isabel, et al., eds. Public sector accounting and auditing in Europe: The challenge

of harmonization. Springer, 2016.

2 Cannon, Nathan H., and Jean C. Bedard. "Auditing challenging fair value measurements:

Evidence from the field." The Accounting Review 92.4 (2016): 81-114.

3 Chiu, Victoria, Qi Liu, and Miklos A. Vasarhelyi. "The Development and Intellectual

Structure of Continuous Auditing Research 1." Continuous Auditing: Theory and

Application. Emerald Publishing Limited, 2018. 53-85

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Auditing

shows about the planning materiality of the company and how it can be affected the auditing

process of the auditor.

Discussion

Overview of the Company

The reports deal with the company Konekt Limited. The company is based upon

Australia and it a service industry which provide the service in different industry as it help the

company to reduce the employee turnover and also show how the company can able to keep

the minimization of injury happens in the company regarding employee. The company have

much experience industry so it helps to build a good image of the industry in regards of the

public so it help them in gaining more business in the company.

Materiality in the Company financial statement

The auditors carry different procedure in the company to check whether it contain any

material misstatement of not in the financial statement of the company4. So the error and

misstatement of the company financial statement are been treated as materiality in the

business. It is the biggest type of risk which can be there in the financial statement of the

company and auditors have to be very much careful while checking the materiality in the

financial statement of the company5. As if there will error or omission in the financial

statement than it will directly affect the financial user decision as they take information from

the financial statement so it able to know the position of the company in the industry but if

4 DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

5 Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing

a Company's Personality. Routledge, 2015.

Auditing

shows about the planning materiality of the company and how it can be affected the auditing

process of the auditor.

Discussion

Overview of the Company

The reports deal with the company Konekt Limited. The company is based upon

Australia and it a service industry which provide the service in different industry as it help the

company to reduce the employee turnover and also show how the company can able to keep

the minimization of injury happens in the company regarding employee. The company have

much experience industry so it helps to build a good image of the industry in regards of the

public so it help them in gaining more business in the company.

Materiality in the Company financial statement

The auditors carry different procedure in the company to check whether it contain any

material misstatement of not in the financial statement of the company4. So the error and

misstatement of the company financial statement are been treated as materiality in the

business. It is the biggest type of risk which can be there in the financial statement of the

company and auditors have to be very much careful while checking the materiality in the

financial statement of the company5. As if there will error or omission in the financial

statement than it will directly affect the financial user decision as they take information from

the financial statement so it able to know the position of the company in the industry but if

4 DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

5 Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing

a Company's Personality. Routledge, 2015.

5

Auditing

the company financial statement is having some error than it will make a false

misrepresentation of the company upon the stakeholders of the company. The materiality can

be of two types in the financial statement and it is been given below:

Qualitative Aspects of Materiality

1. No Disclosure in Notes of Account – As per the accounting standard an company

should disclose all the material facts in the financial statement notes so that the

stakeholder are able to know about the adjustment which is done by the company in

order to make the financial statement 6. There are some matter which are to be done

by the company and all the matters required to be disclosed properly so that it can

able to know the user about the need of the transaction in the company.

2. Misstatement or error in the Financial Statement – The accountant of the

company should do all the transaction properly and should record the same in the

financial statement of the company so if the company financial statement have some

types of error than it will not able to provide a fair report to the financial user so it is

been a misstatement which is consider so the company should not have any error in

their financial statement and should show a fair value to the user of the financial

statement7.

Quantitative Aspects of Materiality

6 Griffiths, Phil. Risk-based auditing. Routledge, 2016.

7 Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

Auditing

the company financial statement is having some error than it will make a false

misrepresentation of the company upon the stakeholders of the company. The materiality can

be of two types in the financial statement and it is been given below:

Qualitative Aspects of Materiality

1. No Disclosure in Notes of Account – As per the accounting standard an company

should disclose all the material facts in the financial statement notes so that the

stakeholder are able to know about the adjustment which is done by the company in

order to make the financial statement 6. There are some matter which are to be done

by the company and all the matters required to be disclosed properly so that it can

able to know the user about the need of the transaction in the company.

2. Misstatement or error in the Financial Statement – The accountant of the

company should do all the transaction properly and should record the same in the

financial statement of the company so if the company financial statement have some

types of error than it will not able to provide a fair report to the financial user so it is

been a misstatement which is consider so the company should not have any error in

their financial statement and should show a fair value to the user of the financial

statement7.

Quantitative Aspects of Materiality

6 Griffiths, Phil. Risk-based auditing. Routledge, 2016.

7 Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Auditing

In order to get the materiality of the company an auditor has to follow certain in

regards of the financial statement of the company. These steps help the company to know

which is there in the financial statement of the company. The steps are:

1. It should make a estimation of the materiality which can be there in the financial

statement of the company, this step is been done by the auditor before its start the

audit process in the company so that it can able to plan the audit accordingly8. It

should make a base of the account so that it can able to get a proper amount of the

materiality in the financial statement of the company.

2. It should analysis the financial and should check the account which can have material

misstatement and can directly affect the financial statement of the company.

3. After doing the assertion of the account than it should do the total of the amount

which it have found out so that it can know the actual amount of materiality

4. Lastly it should do the comparison of the estimated and the actual so that it can able to

know the risk which is been associated in the financial statement as if there is a big

difference than it should check all the document properly in the financial statement of

the company.

Company Accounts which contain materiality

1. Other Assets – Company annual report show that there is an increase in other asset

account of the company which can be consider as material misstatement from the

auditor viewpoint as it can happen that the company have increased it so that it can

show a good position of the company as if there is an increase in the other asset than it

will show a good increase in the overall financial position of the company.

8 Hall, James A. Information technology auditing. Cengage Learning, 2015.

Auditing

In order to get the materiality of the company an auditor has to follow certain in

regards of the financial statement of the company. These steps help the company to know

which is there in the financial statement of the company. The steps are:

1. It should make a estimation of the materiality which can be there in the financial

statement of the company, this step is been done by the auditor before its start the

audit process in the company so that it can able to plan the audit accordingly8. It

should make a base of the account so that it can able to get a proper amount of the

materiality in the financial statement of the company.

2. It should analysis the financial and should check the account which can have material

misstatement and can directly affect the financial statement of the company.

3. After doing the assertion of the account than it should do the total of the amount

which it have found out so that it can know the actual amount of materiality

4. Lastly it should do the comparison of the estimated and the actual so that it can able to

know the risk which is been associated in the financial statement as if there is a big

difference than it should check all the document properly in the financial statement of

the company.

Company Accounts which contain materiality

1. Other Assets – Company annual report show that there is an increase in other asset

account of the company which can be consider as material misstatement from the

auditor viewpoint as it can happen that the company have increased it so that it can

show a good position of the company as if there is an increase in the other asset than it

will show a good increase in the overall financial position of the company.

8 Hall, James A. Information technology auditing. Cengage Learning, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Auditing

2. Cash Account – Company annual report show an increase in cash so this show this is

been consider as a material misstatement of the company as there cannot be so much

increase in the financial statement in regards of cash9. It may be done by the company

so that it can able to show a good position of the company and let investors do the

investment in the company.

3. Intangible Asset – Company annual report show that there is an increase in the

intangible asset so this is been consider as a material misstatement by the auditor as

how in one year the intangible asset can increase so much, so the auditor have to carry

some procedure so that it can able to know the reason of the increase in the intangible

asset of the company10.

4. Provisions - Company annual reports show that they were no provision account in

previous year but the company have made in the current year so this is been consider

material misstatement in the company account so the auditor have to carry different

audit procedure as to know about the reason of the creation of provision in the annual

report of the company11.

5. Trade and other payable – Company annual report show that they is in increase in

the trade payable account so it is been consider as material misstatement as why there

9 Harris, James, et al. "Systems and methods for using end point auditing in connection with

traffic management." U.S. Patent No. 8,844,040. 23 Sep. 2014.

10 Hicks, Michael A. "Image overlaying and comparison for inventory display auditing." U.S.

Patent No. 8,917,902. 23 Dec. 2014.

11 Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge,

2016.

Auditing

2. Cash Account – Company annual report show an increase in cash so this show this is

been consider as a material misstatement of the company as there cannot be so much

increase in the financial statement in regards of cash9. It may be done by the company

so that it can able to show a good position of the company and let investors do the

investment in the company.

3. Intangible Asset – Company annual report show that there is an increase in the

intangible asset so this is been consider as a material misstatement by the auditor as

how in one year the intangible asset can increase so much, so the auditor have to carry

some procedure so that it can able to know the reason of the increase in the intangible

asset of the company10.

4. Provisions - Company annual reports show that they were no provision account in

previous year but the company have made in the current year so this is been consider

material misstatement in the company account so the auditor have to carry different

audit procedure as to know about the reason of the creation of provision in the annual

report of the company11.

5. Trade and other payable – Company annual report show that they is in increase in

the trade payable account so it is been consider as material misstatement as why there

9 Harris, James, et al. "Systems and methods for using end point auditing in connection with

traffic management." U.S. Patent No. 8,844,040. 23 Sep. 2014.

10 Hicks, Michael A. "Image overlaying and comparison for inventory display auditing." U.S.

Patent No. 8,917,902. 23 Dec. 2014.

11 Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge,

2016.

8

Auditing

is such increase in the trade payable account as it can be done by the company so that

it can able to make a good impression of the company in front of the stakeholder12.

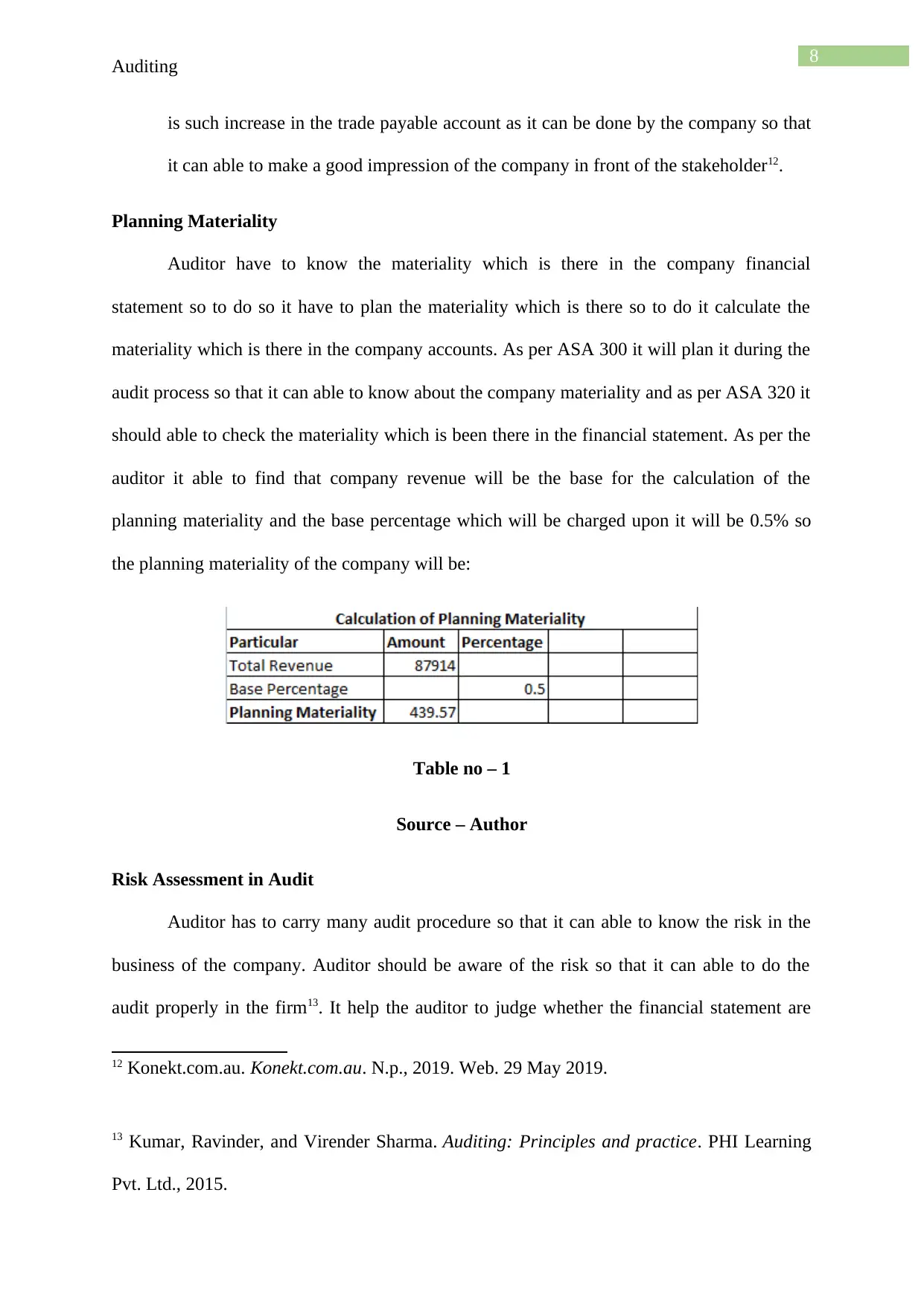

Planning Materiality

Auditor have to know the materiality which is there in the company financial

statement so to do so it have to plan the materiality which is there so to do it calculate the

materiality which is there in the company accounts. As per ASA 300 it will plan it during the

audit process so that it can able to know about the company materiality and as per ASA 320 it

should able to check the materiality which is been there in the financial statement. As per the

auditor it able to find that company revenue will be the base for the calculation of the

planning materiality and the base percentage which will be charged upon it will be 0.5% so

the planning materiality of the company will be:

Table no – 1

Source – Author

Risk Assessment in Audit

Auditor has to carry many audit procedure so that it can able to know the risk in the

business of the company. Auditor should be aware of the risk so that it can able to do the

audit properly in the firm13. It help the auditor to judge whether the financial statement are

12 Konekt.com.au. Konekt.com.au. N.p., 2019. Web. 29 May 2019.

13 Kumar, Ravinder, and Virender Sharma. Auditing: Principles and practice. PHI Learning

Pvt. Ltd., 2015.

Auditing

is such increase in the trade payable account as it can be done by the company so that

it can able to make a good impression of the company in front of the stakeholder12.

Planning Materiality

Auditor have to know the materiality which is there in the company financial

statement so to do so it have to plan the materiality which is there so to do it calculate the

materiality which is there in the company accounts. As per ASA 300 it will plan it during the

audit process so that it can able to know about the company materiality and as per ASA 320 it

should able to check the materiality which is been there in the financial statement. As per the

auditor it able to find that company revenue will be the base for the calculation of the

planning materiality and the base percentage which will be charged upon it will be 0.5% so

the planning materiality of the company will be:

Table no – 1

Source – Author

Risk Assessment in Audit

Auditor has to carry many audit procedure so that it can able to know the risk in the

business of the company. Auditor should be aware of the risk so that it can able to do the

audit properly in the firm13. It help the auditor to judge whether the financial statement are

12 Konekt.com.au. Konekt.com.au. N.p., 2019. Web. 29 May 2019.

13 Kumar, Ravinder, and Virender Sharma. Auditing: Principles and practice. PHI Learning

Pvt. Ltd., 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Auditing

been showing true and fair view or not. There are many things which the auditors have to

know than only it will be able to know the risk which is there in the company accounts. The

things which auditor needs to check are shown below:

Primarily the auditor should be aware so the industry in which it have to carry the

audit procedure as this will help it to know more about the business practices which

can be carry by the management and it will help the auditor to judge the risk which

can be found in the financial statement of the company.

It should know all the business practices which the company used to attract the

customers as this will help the auditor to know about the company internal control

more properly and as a result it able to know the risk and mistake which can be there

in the financial statement of the company14.

Auditor have to know about the board of the company as it will help it to know how

the company is been managed internally and also show about level of knowledge

which the managers have in regards of the business which is been carry by the same.

Proper questionnaire should take place by the auditor to the employee of the

comp0any so that it can able to know all then internal matters which are happening in

the company and also the amount of risk which is been there in the financial

statement of the company15.

14 Yu, Jia, Kui Ren, and Cong Wang. "Enabling cloud storage auditing with verifiable

outsourcing of key updates." IEEE transactions on information forensics and security 11.6

(2016): 1362-1375.

15 Zhang, Juan, Xiongsheng Yang, and Deniz Appelbaum. "Toward effective Big Data

analysis in continuous auditing." Accounting Horizons 29.2 (2015): 469-476.

Auditing

been showing true and fair view or not. There are many things which the auditors have to

know than only it will be able to know the risk which is there in the company accounts. The

things which auditor needs to check are shown below:

Primarily the auditor should be aware so the industry in which it have to carry the

audit procedure as this will help it to know more about the business practices which

can be carry by the management and it will help the auditor to judge the risk which

can be found in the financial statement of the company.

It should know all the business practices which the company used to attract the

customers as this will help the auditor to know about the company internal control

more properly and as a result it able to know the risk and mistake which can be there

in the financial statement of the company14.

Auditor have to know about the board of the company as it will help it to know how

the company is been managed internally and also show about level of knowledge

which the managers have in regards of the business which is been carry by the same.

Proper questionnaire should take place by the auditor to the employee of the

comp0any so that it can able to know all then internal matters which are happening in

the company and also the amount of risk which is been there in the financial

statement of the company15.

14 Yu, Jia, Kui Ren, and Cong Wang. "Enabling cloud storage auditing with verifiable

outsourcing of key updates." IEEE transactions on information forensics and security 11.6

(2016): 1362-1375.

15 Zhang, Juan, Xiongsheng Yang, and Deniz Appelbaum. "Toward effective Big Data

analysis in continuous auditing." Accounting Horizons 29.2 (2015): 469-476.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Auditing

Proper analysis of the financial statement should be done by the auditor as it should

check different trends which are been found in the company so that it can able to

know the different aspects of the company and as a result it will able to give proper

opinion upon the financial statement of the company.

Risk assessment in the company accounts

1. Other Asset – As per ASA 330 the auditor should carry audit procedure as it should

the document of the company to know whether there any error or omission of the

transaction in regards of the other asset 16. As it will also check about how the

company is able to carry the value of asset as proper value is only be used by the

company and no false misstatement is been done by the company in regards of the

same in the account.

2. Cash Account – As per ASA 330 the auditor have to check all the cash transaction

which are been done in the company and also it should analysis the cash flow of the

company so that it can know where the inflow and out flow of the cash is happening

and it will help the auditor to know more about the financial performance of the

company17.

3. Intangible Asset - As per ASA 330 it should carry the audit process upon the

company intangible asset as it should check all the items which are there in the

16 Neystadt, John, R. Eric Fitzgerald, and Leonid Verny. "Security virtual machine for

advanced auditing." U.S. Patent No. 8,955,108. 10 Feb. 2015.

17 Sandvig, Christian, et al. "Auditing algorithms: Research methods for detecting

discrimination on internet platforms." Data and discrimination: converting critical concerns

into productive inquiry 22 (2014).

Auditing

Proper analysis of the financial statement should be done by the auditor as it should

check different trends which are been found in the company so that it can able to

know the different aspects of the company and as a result it will able to give proper

opinion upon the financial statement of the company.

Risk assessment in the company accounts

1. Other Asset – As per ASA 330 the auditor should carry audit procedure as it should

the document of the company to know whether there any error or omission of the

transaction in regards of the other asset 16. As it will also check about how the

company is able to carry the value of asset as proper value is only be used by the

company and no false misstatement is been done by the company in regards of the

same in the account.

2. Cash Account – As per ASA 330 the auditor have to check all the cash transaction

which are been done in the company and also it should analysis the cash flow of the

company so that it can know where the inflow and out flow of the cash is happening

and it will help the auditor to know more about the financial performance of the

company17.

3. Intangible Asset - As per ASA 330 it should carry the audit process upon the

company intangible asset as it should check all the items which are there in the

16 Neystadt, John, R. Eric Fitzgerald, and Leonid Verny. "Security virtual machine for

advanced auditing." U.S. Patent No. 8,955,108. 10 Feb. 2015.

17 Sandvig, Christian, et al. "Auditing algorithms: Research methods for detecting

discrimination on internet platforms." Data and discrimination: converting critical concerns

into productive inquiry 22 (2014).

11

Auditing

company intangible asset and should check whether the company have done valuation

as per the accounting standard of intangible asset or not18. It should check disclosure

which is been given by the company in regards of the intangible asset so that it can

able to know that proper process is been followed by the company or not.

4. Provisions – As per ASA 330 it should carry audit procedure as it should check the

reason about why the company have make provision in the current year as it have not

done before and also it should check the industry norms so that it can know whether

the amount which the company have made in provision is as per the industry norms or

not and how they have disclose the same in the financial statement of the company19.

5. Trade and other Payable – Auditor should carry audit procedure as per ASA330 as

it should do external confirmation from the third party so that it able to know the

reason about the amount which is actually due and should check the same with the

financial record so the company so that it can able to know the risk which is been

associated in the account also it should check the same in the financial statement

disclosure so that it can know how the company have disclosed the same in the

financial statement of the company20.

18 Sookhak, Mehdi, et al. "Remote data auditing in cloud computing environments: a survey,

taxonomy, and open issues." ACM Computing Surveys (CSUR) 47.4 (2015): 65.

19 Tian, Hui, et al. "Dynamic-hash-table based public auditing for secure cloud storage." IEEE

Transactions on Services Computing 10.5 (2015): 701-714.

20 Wang, Boyang, Baochun Li, and Hui Li. "Oruta: Privacy-preserving public auditing for

shared data in the cloud." IEEE transactions on cloud computing 2.1 (2014): 43-56.

Auditing

company intangible asset and should check whether the company have done valuation

as per the accounting standard of intangible asset or not18. It should check disclosure

which is been given by the company in regards of the intangible asset so that it can

able to know that proper process is been followed by the company or not.

4. Provisions – As per ASA 330 it should carry audit procedure as it should check the

reason about why the company have make provision in the current year as it have not

done before and also it should check the industry norms so that it can know whether

the amount which the company have made in provision is as per the industry norms or

not and how they have disclose the same in the financial statement of the company19.

5. Trade and other Payable – Auditor should carry audit procedure as per ASA330 as

it should do external confirmation from the third party so that it able to know the

reason about the amount which is actually due and should check the same with the

financial record so the company so that it can able to know the risk which is been

associated in the account also it should check the same in the financial statement

disclosure so that it can know how the company have disclosed the same in the

financial statement of the company20.

18 Sookhak, Mehdi, et al. "Remote data auditing in cloud computing environments: a survey,

taxonomy, and open issues." ACM Computing Surveys (CSUR) 47.4 (2015): 65.

19 Tian, Hui, et al. "Dynamic-hash-table based public auditing for secure cloud storage." IEEE

Transactions on Services Computing 10.5 (2015): 701-714.

20 Wang, Boyang, Baochun Li, and Hui Li. "Oruta: Privacy-preserving public auditing for

shared data in the cloud." IEEE transactions on cloud computing 2.1 (2014): 43-56.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.