CQUniversity Auditing and Ethics Report: Goodman Group Analysis

VerifiedAdded on 2022/08/29

|14

|2834

|19

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics principles, focusing on the audit of Goodman Group. The report begins by examining materiality, including its calculation and significance in identifying material misstatements in financial reports, as per ASA 32. It then delves into preliminary analytical review, analyzing key balance sheet and profitability ratios to identify areas of potential risk, such as profit margin fluctuations and changes in liquidity ratios. The report further assesses the cash flow statement, evaluating Goodman Group's going concern risk and the auditor's responsibilities in this context. The analysis includes an examination of cash inflows and outflows, non-cash transactions, and the auditor's assessment of the company's ability to continue as a going concern. The report concludes by discussing the auditor's opinion on the financial statements and highlights key audit matters.

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Requirement 1.1...........................................................................................................................2

Requirement 1.2...........................................................................................................................4

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................7

Requirement 3.1...........................................................................................................................7

Requirement 3.2...........................................................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Section 1..........................................................................................................................................2

Requirement 1.1...........................................................................................................................2

Requirement 1.2...........................................................................................................................4

Section 2..........................................................................................................................................4

Section 3..........................................................................................................................................7

Requirement 3.1...........................................................................................................................7

Requirement 3.2...........................................................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

2AUDITING AND ETHICS

Introduction

There are different aspects of auditing and the responsibility of the auditors is to properly

carry out the audit procedures by considering all these aspects. Calculation of the materiality

level is one crucial aspect where the auditors are responsible for determining the appropriate

threshold for recognizing the areas of material misstatements in client’s accounting books. This

is a crucial step as the outcome of the whole audit largely depends on the determination of

materiality level. After this step, the auditors are responsible for carrying out the required

preliminary analytical review of the financial information of the client and analysis of certain

ratios is a major procedure under this. This helps the auditors in identifying the areas of risk in

the client’s financial reports. Moreover, assessment of the cash flows statement of the client is

required by the auditors for assessing the going concern risk of the client. This report is based on

Goodman Group Limited. First section discusses about materiality level determination, second

section shows the preliminary analytical review and the last section analyses the cash flow

statement and audit report of the chosen company.

Section 1

Requirement 1.1

Materiality is a key concept used in auditing which is used by the auditors for

recognizing material misstatements in financial reports. It is mentioned in ASA 32, Paragraph 2

that the auditors consider misstatements in financial reports as material if the decisions of the

users are affected by this. Different factors are required to be considered by the auditors for

determining the level of materiality (auasb.gov.au, 2020).

Introduction

There are different aspects of auditing and the responsibility of the auditors is to properly

carry out the audit procedures by considering all these aspects. Calculation of the materiality

level is one crucial aspect where the auditors are responsible for determining the appropriate

threshold for recognizing the areas of material misstatements in client’s accounting books. This

is a crucial step as the outcome of the whole audit largely depends on the determination of

materiality level. After this step, the auditors are responsible for carrying out the required

preliminary analytical review of the financial information of the client and analysis of certain

ratios is a major procedure under this. This helps the auditors in identifying the areas of risk in

the client’s financial reports. Moreover, assessment of the cash flows statement of the client is

required by the auditors for assessing the going concern risk of the client. This report is based on

Goodman Group Limited. First section discusses about materiality level determination, second

section shows the preliminary analytical review and the last section analyses the cash flow

statement and audit report of the chosen company.

Section 1

Requirement 1.1

Materiality is a key concept used in auditing which is used by the auditors for

recognizing material misstatements in financial reports. It is mentioned in ASA 32, Paragraph 2

that the auditors consider misstatements in financial reports as material if the decisions of the

users are affected by this. Different factors are required to be considered by the auditors for

determining the level of materiality (auasb.gov.au, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

It is required to determine the materiality level for the 2019 audit of Goodman Group

through three steps. Calculation of materiality is done through charging a suitable percentage on

a certain base. This base needs to be selected in accordance with the nature of business of

Goodman Group and its business sector. Commonly used bases are total sales, total assets, profit

before tax, net profit and others. For the 2019 audit of Goodman Group, the base for determining

the materiality level is Profit before income tax, commonly known as PBT. As per the 2019

annual report of Goodman Group, the amount of PBT in 2019 is $1744.7 million.

It is required to charge a pre-determined percentage on the selected base for getting the

level of materiality; and this is called Quantitative Threshold of materiality. The obligation on

the auditors is to determine this quantitative threshold by adhering to the norms of AASB 1031

Materiality. As per AASB 1031, the auditor needs to select wither more or equal to 5% or less or

equal to 5% on the base as the percentage (auasb.gov.au, 2020). Again, determining this

percentage is a matter of judgment of the auditors. For the 2019 audit of Goodman Group, 5% is

the quantitative threshold or percentage of materiality level determination.

After the selection of base and percentage, it is needed to get the quantitative estimate of

materiality of 2019 audit of Goodman Group. This process is showing below:

Materiality Level = Base × Percentage

= PBT × 5%

=$1744.7 million × 5/100

= $87.24 million (approximately)

It is required to determine the materiality level for the 2019 audit of Goodman Group

through three steps. Calculation of materiality is done through charging a suitable percentage on

a certain base. This base needs to be selected in accordance with the nature of business of

Goodman Group and its business sector. Commonly used bases are total sales, total assets, profit

before tax, net profit and others. For the 2019 audit of Goodman Group, the base for determining

the materiality level is Profit before income tax, commonly known as PBT. As per the 2019

annual report of Goodman Group, the amount of PBT in 2019 is $1744.7 million.

It is required to charge a pre-determined percentage on the selected base for getting the

level of materiality; and this is called Quantitative Threshold of materiality. The obligation on

the auditors is to determine this quantitative threshold by adhering to the norms of AASB 1031

Materiality. As per AASB 1031, the auditor needs to select wither more or equal to 5% or less or

equal to 5% on the base as the percentage (auasb.gov.au, 2020). Again, determining this

percentage is a matter of judgment of the auditors. For the 2019 audit of Goodman Group, 5% is

the quantitative threshold or percentage of materiality level determination.

After the selection of base and percentage, it is needed to get the quantitative estimate of

materiality of 2019 audit of Goodman Group. This process is showing below:

Materiality Level = Base × Percentage

= PBT × 5%

=$1744.7 million × 5/100

= $87.24 million (approximately)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

Therefore, as per the above calculation, $87.24 million is the level of materiality of

quantitative estimate of the materiality for the 2019 audit of Goodman Group; it means any

misstatements above this amount needs to be considered as material.

Requirement 1.2

According to Note 21 Contingencies of 2019 Annual Report, Goodman Group has

disclosed two situations of contingencies; they are Capitalization Deed Poll and United States

and Reg S Senior Notes (goodman.com, 2020).

Under first contingency case, any payment by an investor to a borrower will be

considered as a loan to the borrower by the investor. Under the second contingency case,

controlled entities of Goodman Group have unconditional and irrevocable guarantee on the

payment of principal and interest in respect of each of the notes. Therefore, these cases can

increase the liability of Goodman Group in case they become due (goodman.com, 2020).

Therefore, the responsibility of the auditor of Goodman Group is to assess the chances of

occurrence of these events; and rate them based on probable, remote and logically possible.

Based on the outcome of this assessment, it is required to take appropriate actions. This will help

in reducing the audit risk.

Section 2

Undertaking preliminary analytical review helps the auditor of Goodman Group to

identify the areas that need to be addressed in the audit plan. For the 2019 audit of this company,

certain key balance sheet and profitability ratios are analysis as a part of preliminary analytical

review. These ratios are provided below in the table:

Therefore, as per the above calculation, $87.24 million is the level of materiality of

quantitative estimate of the materiality for the 2019 audit of Goodman Group; it means any

misstatements above this amount needs to be considered as material.

Requirement 1.2

According to Note 21 Contingencies of 2019 Annual Report, Goodman Group has

disclosed two situations of contingencies; they are Capitalization Deed Poll and United States

and Reg S Senior Notes (goodman.com, 2020).

Under first contingency case, any payment by an investor to a borrower will be

considered as a loan to the borrower by the investor. Under the second contingency case,

controlled entities of Goodman Group have unconditional and irrevocable guarantee on the

payment of principal and interest in respect of each of the notes. Therefore, these cases can

increase the liability of Goodman Group in case they become due (goodman.com, 2020).

Therefore, the responsibility of the auditor of Goodman Group is to assess the chances of

occurrence of these events; and rate them based on probable, remote and logically possible.

Based on the outcome of this assessment, it is required to take appropriate actions. This will help

in reducing the audit risk.

Section 2

Undertaking preliminary analytical review helps the auditor of Goodman Group to

identify the areas that need to be addressed in the audit plan. For the 2019 audit of this company,

certain key balance sheet and profitability ratios are analysis as a part of preliminary analytical

review. These ratios are provided below in the table:

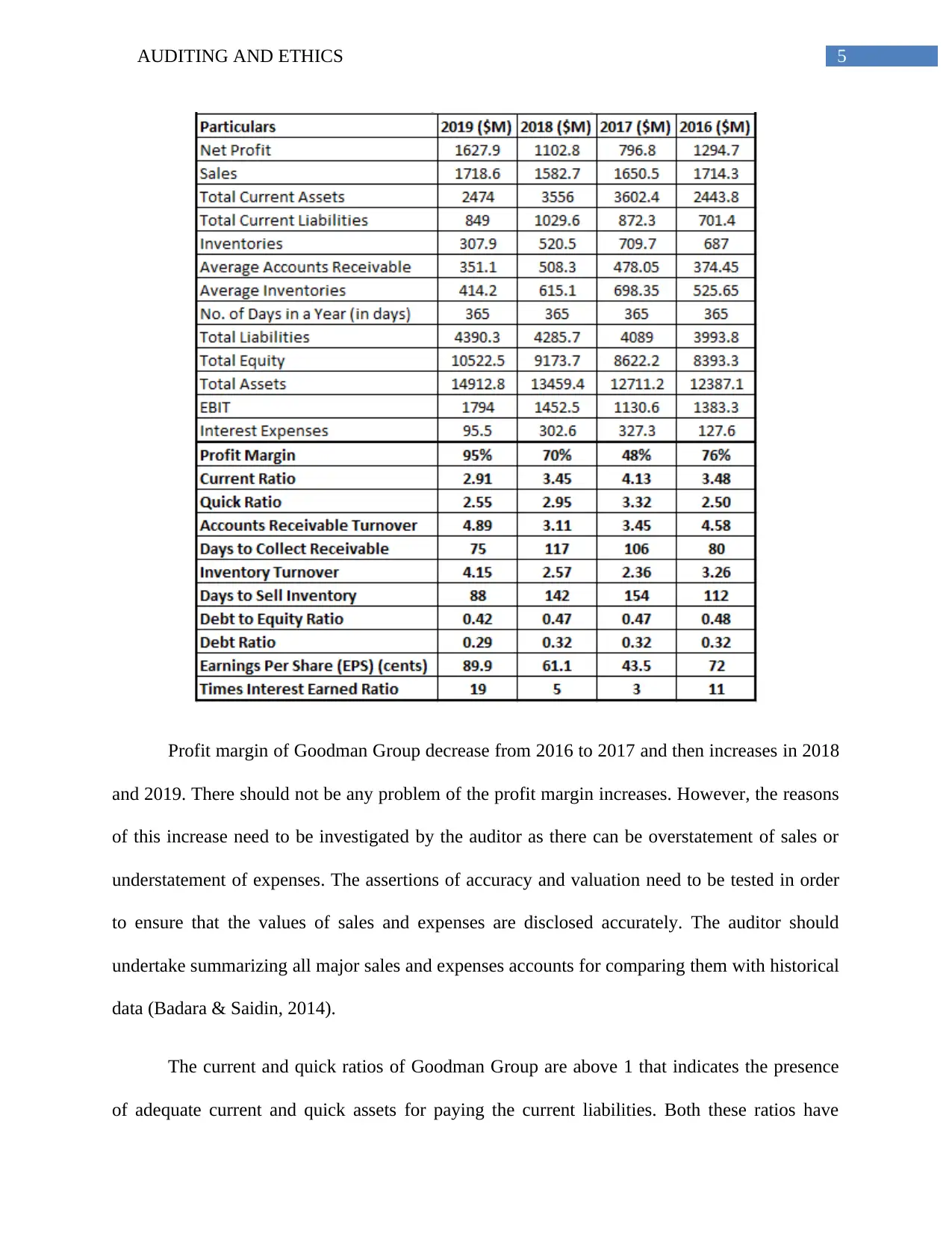

5AUDITING AND ETHICS

Profit margin of Goodman Group decrease from 2016 to 2017 and then increases in 2018

and 2019. There should not be any problem of the profit margin increases. However, the reasons

of this increase need to be investigated by the auditor as there can be overstatement of sales or

understatement of expenses. The assertions of accuracy and valuation need to be tested in order

to ensure that the values of sales and expenses are disclosed accurately. The auditor should

undertake summarizing all major sales and expenses accounts for comparing them with historical

data (Badara & Saidin, 2014).

The current and quick ratios of Goodman Group are above 1 that indicates the presence

of adequate current and quick assets for paying the current liabilities. Both these ratios have

Profit margin of Goodman Group decrease from 2016 to 2017 and then increases in 2018

and 2019. There should not be any problem of the profit margin increases. However, the reasons

of this increase need to be investigated by the auditor as there can be overstatement of sales or

understatement of expenses. The assertions of accuracy and valuation need to be tested in order

to ensure that the values of sales and expenses are disclosed accurately. The auditor should

undertake summarizing all major sales and expenses accounts for comparing them with historical

data (Badara & Saidin, 2014).

The current and quick ratios of Goodman Group are above 1 that indicates the presence

of adequate current and quick assets for paying the current liabilities. Both these ratios have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

increased from 2016 to 2017; and then decreased in 2018 and 2019. It means that Goodman

Group might be reporting more current and quick asset that it should or it might be reporting less

current liabilities than it should. This needs to be investigated. Therefore, the existence assertion

needs to be tested by assessing the related papers and documents associated with these assets and

liabilities (Chan & Kogan, 2016).

Accounts receivable turnover has decreased from 2016 to 2018 and increased in 2019;

days to collect receivables have increased from 2016 to 2018 and decreased in 2019. It implies

that Goodman Group has increased average collection of receivables when they collect the dues

in fewer days. This is in line with the current and quick ratio; and thus, the reason for this need to

be investigated by the auditor. There might not be appropriate write off of accounts receivable.

Therefore, valuation assertion needs to be tested through getting confirmation of the key

accounts receivable balances (Utami et al., 2014).

Inventory turnover has decreased from 2016 to 2018 and increased in 2019; days to sell

inventory have increased from 2016 to 2018 and decreased in 2019. It implies that Goodman

Group has increased selling its inventories by reducing the inventory holding period. This is in

line with the increase in profit margin of the company. Therefore, the reason for this

improvement needs to be investigated by the auditor. Therefore, the valuation assertion needs to

be tested by the auditor by investigating the inventory valuation process undertaken by Goodman

Group as this can spot any cost that has not be allocated or any abnormal wastages (Rozario &

Vasarhelyi, 2018).

Debt to equity ratio has decreased from 2016 to 2019; and debt ratio has also decreased

from 2016 to 2019. Both of these ratios are under 0.5 which indicates less debt capital as

increased from 2016 to 2017; and then decreased in 2018 and 2019. It means that Goodman

Group might be reporting more current and quick asset that it should or it might be reporting less

current liabilities than it should. This needs to be investigated. Therefore, the existence assertion

needs to be tested by assessing the related papers and documents associated with these assets and

liabilities (Chan & Kogan, 2016).

Accounts receivable turnover has decreased from 2016 to 2018 and increased in 2019;

days to collect receivables have increased from 2016 to 2018 and decreased in 2019. It implies

that Goodman Group has increased average collection of receivables when they collect the dues

in fewer days. This is in line with the current and quick ratio; and thus, the reason for this need to

be investigated by the auditor. There might not be appropriate write off of accounts receivable.

Therefore, valuation assertion needs to be tested through getting confirmation of the key

accounts receivable balances (Utami et al., 2014).

Inventory turnover has decreased from 2016 to 2018 and increased in 2019; days to sell

inventory have increased from 2016 to 2018 and decreased in 2019. It implies that Goodman

Group has increased selling its inventories by reducing the inventory holding period. This is in

line with the increase in profit margin of the company. Therefore, the reason for this

improvement needs to be investigated by the auditor. Therefore, the valuation assertion needs to

be tested by the auditor by investigating the inventory valuation process undertaken by Goodman

Group as this can spot any cost that has not be allocated or any abnormal wastages (Rozario &

Vasarhelyi, 2018).

Debt to equity ratio has decreased from 2016 to 2019; and debt ratio has also decreased

from 2016 to 2019. Both of these ratios are under 0.5 which indicates less debt capital as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

compared to equity capital. It means Goodman Group might be understating its long-term debts

or there has been major repayment of debts. Whatever the reason is, it needs to be investigated

by the auditors. The assertion of classification needs to be tested by the auditor through

determining all the debts are properly classified into short-term and long-term debts (Alhosban &

Al-Sharairi, 2017).

EPS has decreased from 2016 to 2018 and increased in 2019 and the reason for this

sudden increase in EPS needs to be investigated by the auditor of Goodman Group. Times

interest earned ratio has decreased from 2016 to 2017; and then increased in 2018 and 2019.

Since, the company has less debt capital this ratio should not be increased. Increase in this ratio

means increase in interest payment. This needs to be investigated by the auditor. The assertion is

classification where the auditor will test whether the debts are classified properly (Hurtt et al.,

2013).

Section 3

Requirement 3.1

1. Majority of cash inflows can be seen in operating activities and majority of cash outflows

can be seen in financing activities (goodman.com, 2020).

2. The primary cash receipts are cash receipts from development activities, other cash

receipts from provided services, income received from property, income from

investments and interest received. The primary cash payments are payment for the

development activities, other cash payments associated with course of operations and

payment of finance cost and net income tax (goodman.com, 2020).

compared to equity capital. It means Goodman Group might be understating its long-term debts

or there has been major repayment of debts. Whatever the reason is, it needs to be investigated

by the auditors. The assertion of classification needs to be tested by the auditor through

determining all the debts are properly classified into short-term and long-term debts (Alhosban &

Al-Sharairi, 2017).

EPS has decreased from 2016 to 2018 and increased in 2019 and the reason for this

sudden increase in EPS needs to be investigated by the auditor of Goodman Group. Times

interest earned ratio has decreased from 2016 to 2017; and then increased in 2018 and 2019.

Since, the company has less debt capital this ratio should not be increased. Increase in this ratio

means increase in interest payment. This needs to be investigated by the auditor. The assertion is

classification where the auditor will test whether the debts are classified properly (Hurtt et al.,

2013).

Section 3

Requirement 3.1

1. Majority of cash inflows can be seen in operating activities and majority of cash outflows

can be seen in financing activities (goodman.com, 2020).

2. The primary cash receipts are cash receipts from development activities, other cash

receipts from provided services, income received from property, income from

investments and interest received. The primary cash payments are payment for the

development activities, other cash payments associated with course of operations and

payment of finance cost and net income tax (goodman.com, 2020).

8AUDITING AND ETHICS

3. According to Note. 18 (c) Non-cash transactions, Goodman Group did not have any

major non-cash transactions in financial and operating activities during 2019

(goodman.com, 2020).

4. Goodman Group as positive cash flows from operation during 2019 which indicates that

the key operations of the firm are able to generate adequate cash flows for continuing its

operations along with meeting the liabilities. Goodman Group has made large repayments

of borrowings and derivative financial instruments; along with the payment of dividends.

Payment of dividend indicates towards adequate profitability of Goodman Group.

Moreover, Goodman Group has made investments and purchased plant and equipment

that show the intention to expand the business (accaglobal.com, 2020). All these reduce

the risk of going concern in Goodman Group. As per Paragraph 10 of ASA 570 Going

Concern, the following steps are recommended:

The auditor needs to assess whether there is any major doubt on the firm’s ability

to operate as a going concern (auasb.gov.au, 2020).

The auditor needs to determine whether the management of Goodman Group has

already performed the preliminary assessment of the ability to continue as a going

concern.

In case this has already been performed, the auditor needs to discuss with the

management whether there is any doubt and whether they have planned the

processes to address them (auasb.gov.au, 2020).

In case this assessment has not been performed, the auditor needs to undertake the

assessment of going concern.

3. According to Note. 18 (c) Non-cash transactions, Goodman Group did not have any

major non-cash transactions in financial and operating activities during 2019

(goodman.com, 2020).

4. Goodman Group as positive cash flows from operation during 2019 which indicates that

the key operations of the firm are able to generate adequate cash flows for continuing its

operations along with meeting the liabilities. Goodman Group has made large repayments

of borrowings and derivative financial instruments; along with the payment of dividends.

Payment of dividend indicates towards adequate profitability of Goodman Group.

Moreover, Goodman Group has made investments and purchased plant and equipment

that show the intention to expand the business (accaglobal.com, 2020). All these reduce

the risk of going concern in Goodman Group. As per Paragraph 10 of ASA 570 Going

Concern, the following steps are recommended:

The auditor needs to assess whether there is any major doubt on the firm’s ability

to operate as a going concern (auasb.gov.au, 2020).

The auditor needs to determine whether the management of Goodman Group has

already performed the preliminary assessment of the ability to continue as a going

concern.

In case this has already been performed, the auditor needs to discuss with the

management whether there is any doubt and whether they have planned the

processes to address them (auasb.gov.au, 2020).

In case this assessment has not been performed, the auditor needs to undertake the

assessment of going concern.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

Moreover, the auditor needs to stay alert in the audit process for audit evidence

that may raise major doubts on the ability of Goodman Group to continue as a

going concern (auasb.gov.au, 2020).

Requirement 3.2

1. The auditor of Goodman Group has mentioned that all the consolidated financial

statements of Goodman Group along with the accompanied notes have been prepared in

line with the appropriate accounting standards and they give true and fair view of the

company’s financial performance and position (goodman.com, 2020). It means an

unqualified audit opinion is provided to Goodman Group as there is not any material

misstatements in the financial statements and all the standards have been followed in

preparing the financial statements (Wenjun, 2014).

2. An additional section named “Key Audit Matters” is provided in the audit report of

Goodman Group that indicates certain significant issues faced by the auditing during the

audit of Goodman Group. These issues are in the recognition of portfolio performance fee

income, development income recognition, investment property related valuation and

intangible asset value (goodman.com, 2020). However, the auditors have exercised

appropriate audit procedures in order to make sure that there is not any material

misstatement in them (Cordoş & Fülöp, 2015).

Conclusion

The above discussion analyzes about the process undertaken by the auditors in order to

ascertain quantitative estimation of the level of materiality. Selecting appropriate base and

quantitative threshold or percentage is required for determining the materiality level. Analysis of

Moreover, the auditor needs to stay alert in the audit process for audit evidence

that may raise major doubts on the ability of Goodman Group to continue as a

going concern (auasb.gov.au, 2020).

Requirement 3.2

1. The auditor of Goodman Group has mentioned that all the consolidated financial

statements of Goodman Group along with the accompanied notes have been prepared in

line with the appropriate accounting standards and they give true and fair view of the

company’s financial performance and position (goodman.com, 2020). It means an

unqualified audit opinion is provided to Goodman Group as there is not any material

misstatements in the financial statements and all the standards have been followed in

preparing the financial statements (Wenjun, 2014).

2. An additional section named “Key Audit Matters” is provided in the audit report of

Goodman Group that indicates certain significant issues faced by the auditing during the

audit of Goodman Group. These issues are in the recognition of portfolio performance fee

income, development income recognition, investment property related valuation and

intangible asset value (goodman.com, 2020). However, the auditors have exercised

appropriate audit procedures in order to make sure that there is not any material

misstatement in them (Cordoş & Fülöp, 2015).

Conclusion

The above discussion analyzes about the process undertaken by the auditors in order to

ascertain quantitative estimation of the level of materiality. Selecting appropriate base and

quantitative threshold or percentage is required for determining the materiality level. Analysis of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

key ration assists the auditor to recognize the areas that need to be considered in the audit

planning of 2019; some of these areas are large increase in liquidity ratios, major reduction in

long-terms loans, increase in interest payment and others. Testing of appropriate assertions and

undertaking of appropriate audit steps are recommended above. The cash flow analysis shows

generation of adequate positive cash inflows that ensures the future ability of Goodman Group to

continue as a going concern. However, the audit steps are suggested in case the auditor has to

perform going concern assessment. The auditor of Goodman Group has provided the company

with unqualified audit opinion due to the absence of any material misstatements in the financial

reports.

key ration assists the auditor to recognize the areas that need to be considered in the audit

planning of 2019; some of these areas are large increase in liquidity ratios, major reduction in

long-terms loans, increase in interest payment and others. Testing of appropriate assertions and

undertaking of appropriate audit steps are recommended above. The cash flow analysis shows

generation of adequate positive cash inflows that ensures the future ability of Goodman Group to

continue as a going concern. However, the audit steps are suggested in case the auditor has to

perform going concern assessment. The auditor of Goodman Group has provided the company

with unqualified audit opinion due to the absence of any material misstatements in the financial

reports.

11AUDITING AND ETHICS

References

Aasb.gov.au. (2020). Materiality. Retrieved 8 January 2020, from

https://www.aasb.gov.au/admin/file/content102/c3/AASB1031_9-95.pdf

Alhosban, A. A., & Al-Sharairi, M. (2017). Role of internal auditor in dealing with computer

networks technology-Applied study in Islamic banks in Jordan. International Business

Research, 10(6), 259-269.

Auasb.gov.au. (2020). Auditing Standard ASA 320 Materiality in Planning and Performing an

Audit. Retrieved 8 January 2020, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

Auasb.gov.au. (2020). Going Concern. Retrieved 8 January 2020, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf

Badara, M. A. S., & Saidin, S. Z. (2014). Internal audit effectiveness: Data screening and

preliminary analysis. Asian Social Science, 10(10), 76-85.

Chan, D. Y., & Kogan, A. (2016). Data analytics: Introduction to using analytics in

auditing. Journal of Emerging Technologies in Accounting, 13(1), 121-140.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Goodman.com. (2020). Goodman Group Annual Report 2016. Retrieved 8 January 2020, from

https://www.goodman.com/-/media/Files/Sites/Global/Investor-Centre/GMG-Goodman-

References

Aasb.gov.au. (2020). Materiality. Retrieved 8 January 2020, from

https://www.aasb.gov.au/admin/file/content102/c3/AASB1031_9-95.pdf

Alhosban, A. A., & Al-Sharairi, M. (2017). Role of internal auditor in dealing with computer

networks technology-Applied study in Islamic banks in Jordan. International Business

Research, 10(6), 259-269.

Auasb.gov.au. (2020). Auditing Standard ASA 320 Materiality in Planning and Performing an

Audit. Retrieved 8 January 2020, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

Auasb.gov.au. (2020). Going Concern. Retrieved 8 January 2020, from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf

Badara, M. A. S., & Saidin, S. Z. (2014). Internal audit effectiveness: Data screening and

preliminary analysis. Asian Social Science, 10(10), 76-85.

Chan, D. Y., & Kogan, A. (2016). Data analytics: Introduction to using analytics in

auditing. Journal of Emerging Technologies in Accounting, 13(1), 121-140.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Goodman.com. (2020). Goodman Group Annual Report 2016. Retrieved 8 January 2020, from

https://www.goodman.com/-/media/Files/Sites/Global/Investor-Centre/GMG-Goodman-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.