Auditing Theory and Practice: Internal Control & Audit Risk at GPSA

VerifiedAdded on 2019/10/30

|13

|3013

|269

Report

AI Summary

This report analyzes the internal control effectiveness of GPSA in the context of its audit plan. It identifies potential audit risks, including those related to accounts receivables, current investments, and property assets, and discusses steps to mitigate these risks. The report emphasizes the role of effective internal controls in reducing these risks and outlines tests of control to ensure efficiency. Furthermore, it highlights weaknesses in GPSA's trade receivables and sales systems, such as the concentration of responsibilities with the trade receivables clerk and potential conflicts of interest in sales bonus structures. The analysis includes financial ratio analysis, such as debt-to-equity, days to collect receivables and return on assets, to assess business risks and financial performance, along with recommendations to improve internal controls and safeguard against audit risks.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the University

Name of the student

Authors note

Auditing theory and practice

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared to analyse the internal control effectiveness of GPSA in the

preparation of audit plan. Potential audit risks of organization have been analyzed and

sufficient steps are taken for minimizations of such risks have been discussed in the report.

Report also demonstrates the risks that can be alleviated due to the effective internal control

system of organization. Test of control has been adopted for making the internal control

efficient. Later part of report discusses the weakness that might arise in the trade receivables

and sales system of organization.

Executive summary:

The report is prepared to analyse the internal control effectiveness of GPSA in the

preparation of audit plan. Potential audit risks of organization have been analyzed and

sufficient steps are taken for minimizations of such risks have been discussed in the report.

Report also demonstrates the risks that can be alleviated due to the effective internal control

system of organization. Test of control has been adopted for making the internal control

efficient. Later part of report discusses the weakness that might arise in the trade receivables

and sales system of organization.

2AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................5

Answer to question 1A:..............................................................................................................5

Accounts-...................................................................................................................................5

Analysis-....................................................................................................................................5

Audit risk-..................................................................................................................................6

Audit risk faced by GPSA can be reduced by performing following steps:..............................7

Answer to question 1B:..............................................................................................................7

Answer to question 2A:..............................................................................................................8

Effective control-.......................................................................................................................8

Risk alleviated-...........................................................................................................................9

Test of control-...........................................................................................................................9

Answer to question 2b:.............................................................................................................11

Weakness identified in the internal control for trade receivables and sales of GPSA:............11

Conclusion:..............................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................5

Answer to question 1A:..............................................................................................................5

Accounts-...................................................................................................................................5

Analysis-....................................................................................................................................5

Audit risk-..................................................................................................................................6

Audit risk faced by GPSA can be reduced by performing following steps:..............................7

Answer to question 1B:..............................................................................................................7

Answer to question 2A:..............................................................................................................8

Effective control-.......................................................................................................................8

Risk alleviated-...........................................................................................................................9

Test of control-...........................................................................................................................9

Answer to question 2b:.............................................................................................................11

Weakness identified in the internal control for trade receivables and sales of GPSA:............11

Conclusion:..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

Introduction:

Auditing firm Miller Yates and Howarth is engaged in the preparation of audit plan.

One of the most outstanding and significant clients of MYH is GPSA for which accounting

records are audited. Internal control of organizations are placed great reliance by the auditing

firm derived from extensive test control. There are several area of concerns related to some

accounts of organization in preparation of audit plan. Analysis of ratio has been done that

helps in evaluation of the effectiveness of internal control systems (Bik et al., 2017).

Discussion:

Answer to question 1A:

Accounts-

The five types of accounts that is a concern for the auditors of GPSA while carrying

out audit plan includes accounts receivables, current investment, property assets, intangible

assets and research and development capitalization. The audit partner of organization is

concerned about these areas of accounts prior to conducting the audit program (Pitt, 2014).

Analysis-

The reconciliation of trade receivable ledger in the general ledger to the debtor control

account is to be done by trade receivable clerk. All the receipt from debtors and preparation

of bank slip is done by clerk. Payments made to debtors are recorded in the computer system

as debtor payment. Current investment is made by GPSA relating to research activities for the

commencement of new laser surgery device. Research activities of organization are financed

by borrowing loan of amount of $ 5 million during a year. In addition to this, GPSA has

branched out in the property market and acquired a number of properties relating to medical

Introduction:

Auditing firm Miller Yates and Howarth is engaged in the preparation of audit plan.

One of the most outstanding and significant clients of MYH is GPSA for which accounting

records are audited. Internal control of organizations are placed great reliance by the auditing

firm derived from extensive test control. There are several area of concerns related to some

accounts of organization in preparation of audit plan. Analysis of ratio has been done that

helps in evaluation of the effectiveness of internal control systems (Bik et al., 2017).

Discussion:

Answer to question 1A:

Accounts-

The five types of accounts that is a concern for the auditors of GPSA while carrying

out audit plan includes accounts receivables, current investment, property assets, intangible

assets and research and development capitalization. The audit partner of organization is

concerned about these areas of accounts prior to conducting the audit program (Pitt, 2014).

Analysis-

The reconciliation of trade receivable ledger in the general ledger to the debtor control

account is to be done by trade receivable clerk. All the receipt from debtors and preparation

of bank slip is done by clerk. Payments made to debtors are recorded in the computer system

as debtor payment. Current investment is made by GPSA relating to research activities for the

commencement of new laser surgery device. Research activities of organization are financed

by borrowing loan of amount of $ 5 million during a year. In addition to this, GPSA has

branched out in the property market and acquired a number of properties relating to medical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

practitioners. They have made investment in property market and there has been decline in

property value in recent years. However, they are susceptible to such investments due to

bearish property market. GPSA has other principal activities of being involved in research

developmental activities in technologies relating to medical equipment. For enabling the

borrowing of loan amount to make investment in research and development activities,

bankers requires GPSA to maintain debt to equity ratio around 1.2:1. An increase in ration

above this level would lead to make repayment of bank loan. When looking at the audited

value of debt to equity ratio, it can be seen than GPSA is near the banker’s criteria ratio

maintenance. It can be seen that time taken by organization to collect receivables form

customer has increased that reflects that organization might have lenient credit policy criteria

(Quick, 2014).

Audit risk-

Analysis of audit risk is essential part of audit plan and there are several risks

associated while carrying out audit. Analysis of risk is carried out for evaluating, identifying

and prioritizing the risks associated with the management of all the accounts mentioned

above. When looking at recording of trade receivables value that is done by trade receivable

clerk, it is certainly possible that management might not be efficient in keeping the tracks of

such record. Investment made in the implementation of new information technology system

and the function of information technology in organization is looked after by sales director.

However, the sales director duties toward information technology function are not regarded

as full time job by organization’s management. Risk is associated because there is no proper

segregation of duties and this might manipulate data (Boone et al., 2017). There are several

risk associated with accounts receivables as there can be improper reconciliation of accounts

receivables into the general ledger account. Measures of collecting receivables might be

practitioners. They have made investment in property market and there has been decline in

property value in recent years. However, they are susceptible to such investments due to

bearish property market. GPSA has other principal activities of being involved in research

developmental activities in technologies relating to medical equipment. For enabling the

borrowing of loan amount to make investment in research and development activities,

bankers requires GPSA to maintain debt to equity ratio around 1.2:1. An increase in ration

above this level would lead to make repayment of bank loan. When looking at the audited

value of debt to equity ratio, it can be seen than GPSA is near the banker’s criteria ratio

maintenance. It can be seen that time taken by organization to collect receivables form

customer has increased that reflects that organization might have lenient credit policy criteria

(Quick, 2014).

Audit risk-

Analysis of audit risk is essential part of audit plan and there are several risks

associated while carrying out audit. Analysis of risk is carried out for evaluating, identifying

and prioritizing the risks associated with the management of all the accounts mentioned

above. When looking at recording of trade receivables value that is done by trade receivable

clerk, it is certainly possible that management might not be efficient in keeping the tracks of

such record. Investment made in the implementation of new information technology system

and the function of information technology in organization is looked after by sales director.

However, the sales director duties toward information technology function are not regarded

as full time job by organization’s management. Risk is associated because there is no proper

segregation of duties and this might manipulate data (Boone et al., 2017). There are several

risk associated with accounts receivables as there can be improper reconciliation of accounts

receivables into the general ledger account. Measures of collecting receivables might be

5AUDITING THEORY AND PRACTICE

ineffective. While making investigation into the property investment made by organization, is

susceptible to the fact that organization can engaged in fluctuating or inflating the value of

their investment made in property market because of decline.

Audit risk faced by GPSA can be reduced by performing following steps:

Stakeholders of organization should be well informed about the duration of audit risks

and audit engagement should be conducted in accordance with International standards on

auditing.

The business risk faced by GPSA can be outlined by analysing the information of

ratio. Some of the enquires are required to be done by auditors that form an essential part of

audit plan.

Risk of material misstatement relating to all the accounts can be identified by making

enquiries to management that requires enquiries of financial and non financial data.

Analytical procedures are required to be performed by auditor for identifying

plausible relationship between several accounts.

Risk of transactions in normal course of operations relating to accounts receivable are

assessed and identified.

Inspection and observation process are collaborated with management and other

reporting authority within organization.

Answer to question 1B:

The business risk of organization can be outlined by evaluating the ratio analysis. The

tool of ratio analysis helps in explaining the relationship between widely used analytical

procedures and relevant items of financial information. In order to derive at audit evidence

and deriving at audit relevance, auditors make the comparison of ratios. When looking at the

ineffective. While making investigation into the property investment made by organization, is

susceptible to the fact that organization can engaged in fluctuating or inflating the value of

their investment made in property market because of decline.

Audit risk faced by GPSA can be reduced by performing following steps:

Stakeholders of organization should be well informed about the duration of audit risks

and audit engagement should be conducted in accordance with International standards on

auditing.

The business risk faced by GPSA can be outlined by analysing the information of

ratio. Some of the enquires are required to be done by auditors that form an essential part of

audit plan.

Risk of material misstatement relating to all the accounts can be identified by making

enquiries to management that requires enquiries of financial and non financial data.

Analytical procedures are required to be performed by auditor for identifying

plausible relationship between several accounts.

Risk of transactions in normal course of operations relating to accounts receivable are

assessed and identified.

Inspection and observation process are collaborated with management and other

reporting authority within organization.

Answer to question 1B:

The business risk of organization can be outlined by evaluating the ratio analysis. The

tool of ratio analysis helps in explaining the relationship between widely used analytical

procedures and relevant items of financial information. In order to derive at audit evidence

and deriving at audit relevance, auditors make the comparison of ratios. When looking at the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

audited financial ratios, debt to equity ratios has decreased inn year 2015 to 1.02 from 1.04 in

year 2014 respectively. For unaudited ratio, debt to equity ratio has increased considerably to

1.11. This is indicative of the fact that the proportion of debt in relation to equity has

increased. Number of days required to collect receivables has increased considerably as

depicted from unaudited financial ratio. Return on total assets has declined significantly from

13.7% in year 2015 to 4.86% in year 2016. This is indicative of the fact that total assets have

not been efficiently utilised in the current year (De Santis, 2016). Current ratio has also

reduced from 1.66 in year 2015 to 1.54 in year 2016 respectively. The unaudited financial

ratio depicts that current ratio stand at 1.80. Increase in current ratio shows that organization

is capable of meeting its short term obligations using current ratio. Looking at return on

equity, it can be seen that, ratio has been significantly falling return to shareholders is

declining.

Answer to question 2A:

Effective control-

The internal control system of GPSA is effective and there has not been any change is

the control system for the last few years. There is no internal audit function and the system of

internal control is being refined at the planning stage of conducting audit. The sales invoices

are properly documented as there are proper procedures for deciding of data related to sakes

made. If there is any manual delivery made, dispatch department raises the sales order and in

event of incomplete deliveries, it is essential to have proper follow up.

The quality and conditions of medical equipments returned by customers are properly

checked by the staff of dispatch department. There is proper procedures related to trade

receivables follow up. In order to achieve the objective of sales system for reviewing the

audited financial ratios, debt to equity ratios has decreased inn year 2015 to 1.02 from 1.04 in

year 2014 respectively. For unaudited ratio, debt to equity ratio has increased considerably to

1.11. This is indicative of the fact that the proportion of debt in relation to equity has

increased. Number of days required to collect receivables has increased considerably as

depicted from unaudited financial ratio. Return on total assets has declined significantly from

13.7% in year 2015 to 4.86% in year 2016. This is indicative of the fact that total assets have

not been efficiently utilised in the current year (De Santis, 2016). Current ratio has also

reduced from 1.66 in year 2015 to 1.54 in year 2016 respectively. The unaudited financial

ratio depicts that current ratio stand at 1.80. Increase in current ratio shows that organization

is capable of meeting its short term obligations using current ratio. Looking at return on

equity, it can be seen that, ratio has been significantly falling return to shareholders is

declining.

Answer to question 2A:

Effective control-

The internal control system of GPSA is effective and there has not been any change is

the control system for the last few years. There is no internal audit function and the system of

internal control is being refined at the planning stage of conducting audit. The sales invoices

are properly documented as there are proper procedures for deciding of data related to sakes

made. If there is any manual delivery made, dispatch department raises the sales order and in

event of incomplete deliveries, it is essential to have proper follow up.

The quality and conditions of medical equipments returned by customers are properly

checked by the staff of dispatch department. There is proper procedures related to trade

receivables follow up. In order to achieve the objective of sales system for reviewing the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

procedures of internal control procedures, some of relevant aspects are required to be

examined and this involves organizational control, segregation of duties, authorization,

physical control and accounting control (Gendron & Power, 2015).

Risk alleviated-

The effective internal control system could help in alleviating the risk that might arise

in organization. Implementation of effective measures would helps in eliminating the risks

that may arise from the manual recording of data and invoices. Recording of trade receivable

data are done by trade receivable clerk and he is responsible for posting the same into ledger

accounts (Zadek et al., 2013). If organization has effective internal control, system then there

can be reduced risks arising from recording of accounting transactions. It is certainly possible

that the trade receivable slip by trade receivable clerk might have some defect as there can be

manipulation or improper recording of list of debtors in preparing the slip. The individual

customer volume rating is updated manually by trade receivable clerk and sale director is

responsible for authorizing the report. All the possible risks associated with accounting and

transactions recording of data would be alleviated by the effective control system of

organization. Thus is so because it helps in facilitating efficient and effective operations as it

becomes easy to respond appropriately to operations, finance and compliance of business.

Quality of external and internal control of reporting is ensured by maintenance of processes

and proper records that helps in generating relevant timely and reliable information within

and outside the organization (Davies & Goddard, 2017).

procedures of internal control procedures, some of relevant aspects are required to be

examined and this involves organizational control, segregation of duties, authorization,

physical control and accounting control (Gendron & Power, 2015).

Risk alleviated-

The effective internal control system could help in alleviating the risk that might arise

in organization. Implementation of effective measures would helps in eliminating the risks

that may arise from the manual recording of data and invoices. Recording of trade receivable

data are done by trade receivable clerk and he is responsible for posting the same into ledger

accounts (Zadek et al., 2013). If organization has effective internal control, system then there

can be reduced risks arising from recording of accounting transactions. It is certainly possible

that the trade receivable slip by trade receivable clerk might have some defect as there can be

manipulation or improper recording of list of debtors in preparing the slip. The individual

customer volume rating is updated manually by trade receivable clerk and sale director is

responsible for authorizing the report. All the possible risks associated with accounting and

transactions recording of data would be alleviated by the effective control system of

organization. Thus is so because it helps in facilitating efficient and effective operations as it

becomes easy to respond appropriately to operations, finance and compliance of business.

Quality of external and internal control of reporting is ensured by maintenance of processes

and proper records that helps in generating relevant timely and reliable information within

and outside the organization (Davies & Goddard, 2017).

8AUDITING THEORY AND PRACTICE

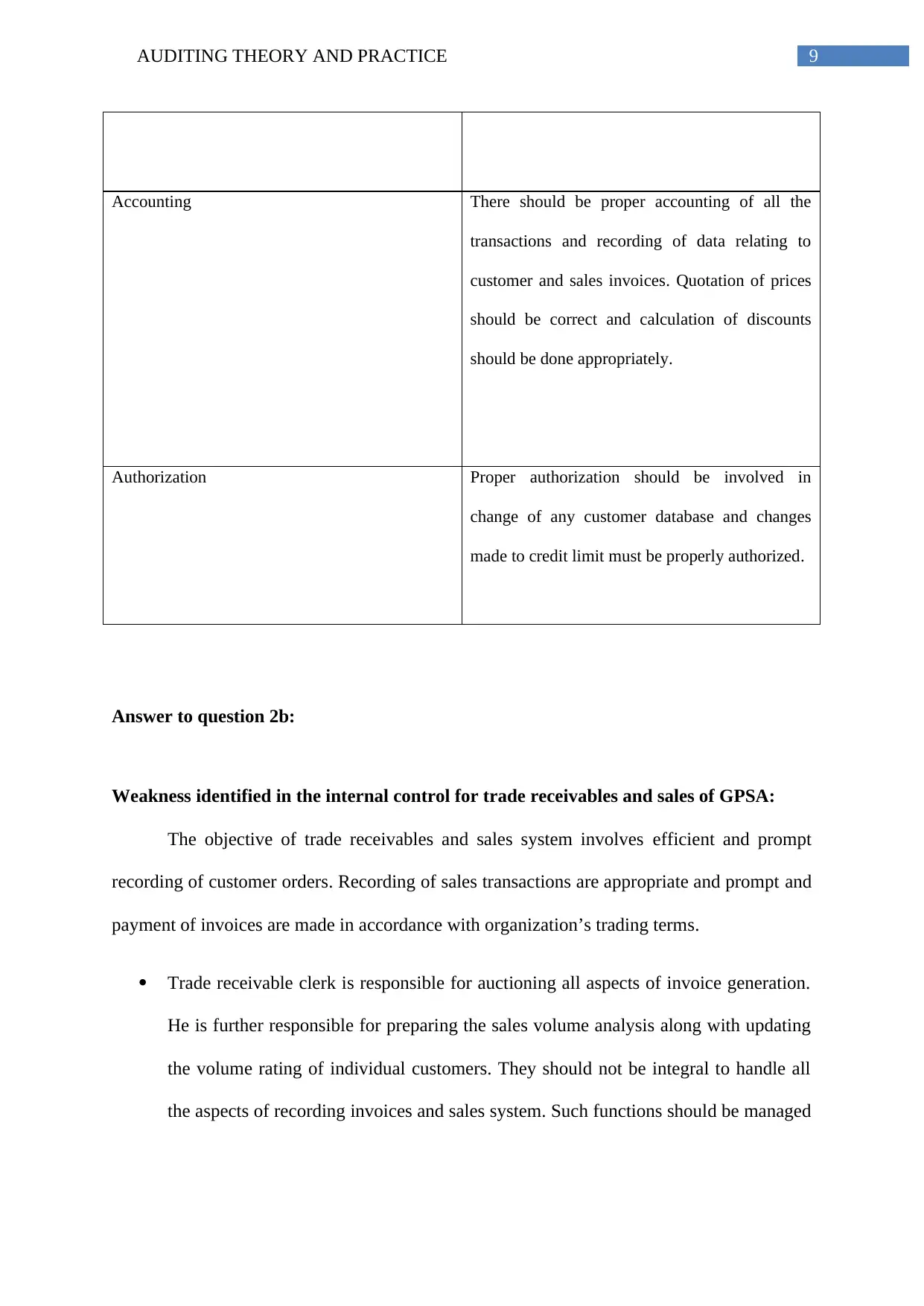

Test of control-

Organizational control Written procedures should be there for granting

credit to customers and receiving orders and

recoding of sales amount.

Physical control The documents related to sales order should have

physical control and their should be numbering of

re order sales forms. The monitoring of condition

and quantity of goods supplied should be done.

Sales invoices and delivery notes should be pre

numbered. Notes related to service performance

and goods delivery notes should be pre

numbered.

Segregation of duties Different members of sales team should be

involve in different aspects of the process of

sales. There should not be any involvement of

sales team members in some other functional

areas such as information technology department

as this cam lead to some potential risks to internal

system. Moreover, if looking within the same

department, there needs to be segregation, for

instance, same staff should not be involved in

raising invoices and dispatching the good to

customers (Earley, 2015).

Test of control-

Organizational control Written procedures should be there for granting

credit to customers and receiving orders and

recoding of sales amount.

Physical control The documents related to sales order should have

physical control and their should be numbering of

re order sales forms. The monitoring of condition

and quantity of goods supplied should be done.

Sales invoices and delivery notes should be pre

numbered. Notes related to service performance

and goods delivery notes should be pre

numbered.

Segregation of duties Different members of sales team should be

involve in different aspects of the process of

sales. There should not be any involvement of

sales team members in some other functional

areas such as information technology department

as this cam lead to some potential risks to internal

system. Moreover, if looking within the same

department, there needs to be segregation, for

instance, same staff should not be involved in

raising invoices and dispatching the good to

customers (Earley, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

Accounting There should be proper accounting of all the

transactions and recording of data relating to

customer and sales invoices. Quotation of prices

should be correct and calculation of discounts

should be done appropriately.

Authorization Proper authorization should be involved in

change of any customer database and changes

made to credit limit must be properly authorized.

Answer to question 2b:

Weakness identified in the internal control for trade receivables and sales of GPSA:

The objective of trade receivables and sales system involves efficient and prompt

recording of customer orders. Recording of sales transactions are appropriate and prompt and

payment of invoices are made in accordance with organization’s trading terms.

Trade receivable clerk is responsible for auctioning all aspects of invoice generation.

He is further responsible for preparing the sales volume analysis along with updating

the volume rating of individual customers. They should not be integral to handle all

the aspects of recording invoices and sales system. Such functions should be managed

Accounting There should be proper accounting of all the

transactions and recording of data relating to

customer and sales invoices. Quotation of prices

should be correct and calculation of discounts

should be done appropriately.

Authorization Proper authorization should be involved in

change of any customer database and changes

made to credit limit must be properly authorized.

Answer to question 2b:

Weakness identified in the internal control for trade receivables and sales of GPSA:

The objective of trade receivables and sales system involves efficient and prompt

recording of customer orders. Recording of sales transactions are appropriate and prompt and

payment of invoices are made in accordance with organization’s trading terms.

Trade receivable clerk is responsible for auctioning all aspects of invoice generation.

He is further responsible for preparing the sales volume analysis along with updating

the volume rating of individual customers. They should not be integral to handle all

the aspects of recording invoices and sales system. Such functions should be managed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

and controlled by employee who is independent of recording transactions and

performing the analysis relating sales and purchase.

Sales bonuses are paid to employees against their targeted monthly sales volume and

target ratios and there is high risk of part of management making bonus payments in

event of inadequate sales transactions (Broberg, 2013).

As depicted from the case study that financial controller is concerned about the

balance of doubtful debtors and there is no prescribed payment received from

customers that should be withhold. Since clerk is responsible for handling all matters

relating to trade receivables, there is increased risk that there will be bad debts and

doubtful debts. In this regard, they would have conflict of interest in minimizing the

doubtful debts and maximising the sales volume.

Since there is no internal audit function of GPSA, there exists weakness in recording

of sales transactions in the account department (Griffin & Wright, 2015). In regard to

this, there is increase risk that the accounting record of company will be inaccurate

and inadequate relating to sales transactions.

Conclusion:

The given case study depicts the internal control system of GPSA that is actively

engaged in development of technologies relating to medical equipment. It has been

ascertained for the analysis of the given case that the internal control system of organization

is somewhat effective. However, there are some risks associated with the trade receivable and

sales system that can be mitigated by the effective implementation of audit plan.

Investigations have been carried out manly in five accounts listed by audit partner of

organization. Furthermore, the test of control is also employed for effective implementing of

internal control so that they are able to address the concern area.

and controlled by employee who is independent of recording transactions and

performing the analysis relating sales and purchase.

Sales bonuses are paid to employees against their targeted monthly sales volume and

target ratios and there is high risk of part of management making bonus payments in

event of inadequate sales transactions (Broberg, 2013).

As depicted from the case study that financial controller is concerned about the

balance of doubtful debtors and there is no prescribed payment received from

customers that should be withhold. Since clerk is responsible for handling all matters

relating to trade receivables, there is increased risk that there will be bad debts and

doubtful debts. In this regard, they would have conflict of interest in minimizing the

doubtful debts and maximising the sales volume.

Since there is no internal audit function of GPSA, there exists weakness in recording

of sales transactions in the account department (Griffin & Wright, 2015). In regard to

this, there is increase risk that the accounting record of company will be inaccurate

and inadequate relating to sales transactions.

Conclusion:

The given case study depicts the internal control system of GPSA that is actively

engaged in development of technologies relating to medical equipment. It has been

ascertained for the analysis of the given case that the internal control system of organization

is somewhat effective. However, there are some risks associated with the trade receivable and

sales system that can be mitigated by the effective implementation of audit plan.

Investigations have been carried out manly in five accounts listed by audit partner of

organization. Furthermore, the test of control is also employed for effective implementing of

internal control so that they are able to address the concern area.

11AUDITING THEORY AND PRACTICE

References:

Bik, O., Hooghiemstra, R., Bishop, C. C., DeZoort, F. T., Hermanson, D. R.,

Officers’Judgments, F., ... & Glover, S. M. (2017). Auditing: A Journal of Practice &

Theory A Publication of the Auditing Section of the American Accounting

Association.

Boone, J. P., Khurana, I. K., Raman, K. K., Chen, L. H., Chung, H. H. S., Peters, G. F., ... &

Truong, C. (2017). Auditing: A Journal of Practice & Theory A Publication of the

Auditing Section of the American Accounting Association.

Broberg, P. (2013). The auditor at work: A study of auditor practice in Big 4 audit firms

(Doctoral dissertation, Department of Business Administration, School of Economics

and Management, Lund University).

Curtis, E., Humphrey, C., & Turley, W. S. (2016). Standards of innovation in auditing.

Auditing: A Journal of Practice & Theory, 35(3), 75-98.

Davies, J., & Goddard, J. (2017, July). Peri-operative delirium quality improvement project:

auditing best practice. In ANAESTHESIA (Vol. 72, pp. 76-76). 111 RIVER ST,

HOBOKEN 07030-5774, NJ USA: WILEY.

De Santis, F. (2016). Auditing Standard Change and Auditors' Everyday Practice: A Field

Study. International Business Research, 9(12), 41.

Earley, C. E. (2015). Data analytics in auditing: Opportunities and challenges. Business

Horizons, 58(5), 493-500.

References:

Bik, O., Hooghiemstra, R., Bishop, C. C., DeZoort, F. T., Hermanson, D. R.,

Officers’Judgments, F., ... & Glover, S. M. (2017). Auditing: A Journal of Practice &

Theory A Publication of the Auditing Section of the American Accounting

Association.

Boone, J. P., Khurana, I. K., Raman, K. K., Chen, L. H., Chung, H. H. S., Peters, G. F., ... &

Truong, C. (2017). Auditing: A Journal of Practice & Theory A Publication of the

Auditing Section of the American Accounting Association.

Broberg, P. (2013). The auditor at work: A study of auditor practice in Big 4 audit firms

(Doctoral dissertation, Department of Business Administration, School of Economics

and Management, Lund University).

Curtis, E., Humphrey, C., & Turley, W. S. (2016). Standards of innovation in auditing.

Auditing: A Journal of Practice & Theory, 35(3), 75-98.

Davies, J., & Goddard, J. (2017, July). Peri-operative delirium quality improvement project:

auditing best practice. In ANAESTHESIA (Vol. 72, pp. 76-76). 111 RIVER ST,

HOBOKEN 07030-5774, NJ USA: WILEY.

De Santis, F. (2016). Auditing Standard Change and Auditors' Everyday Practice: A Field

Study. International Business Research, 9(12), 41.

Earley, C. E. (2015). Data analytics in auditing: Opportunities and challenges. Business

Horizons, 58(5), 493-500.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.