Auditing Assignment: Ethical and Independence Issues in Finance

VerifiedAdded on 2019/10/31

|9

|2103

|186

Homework Assignment

AI Summary

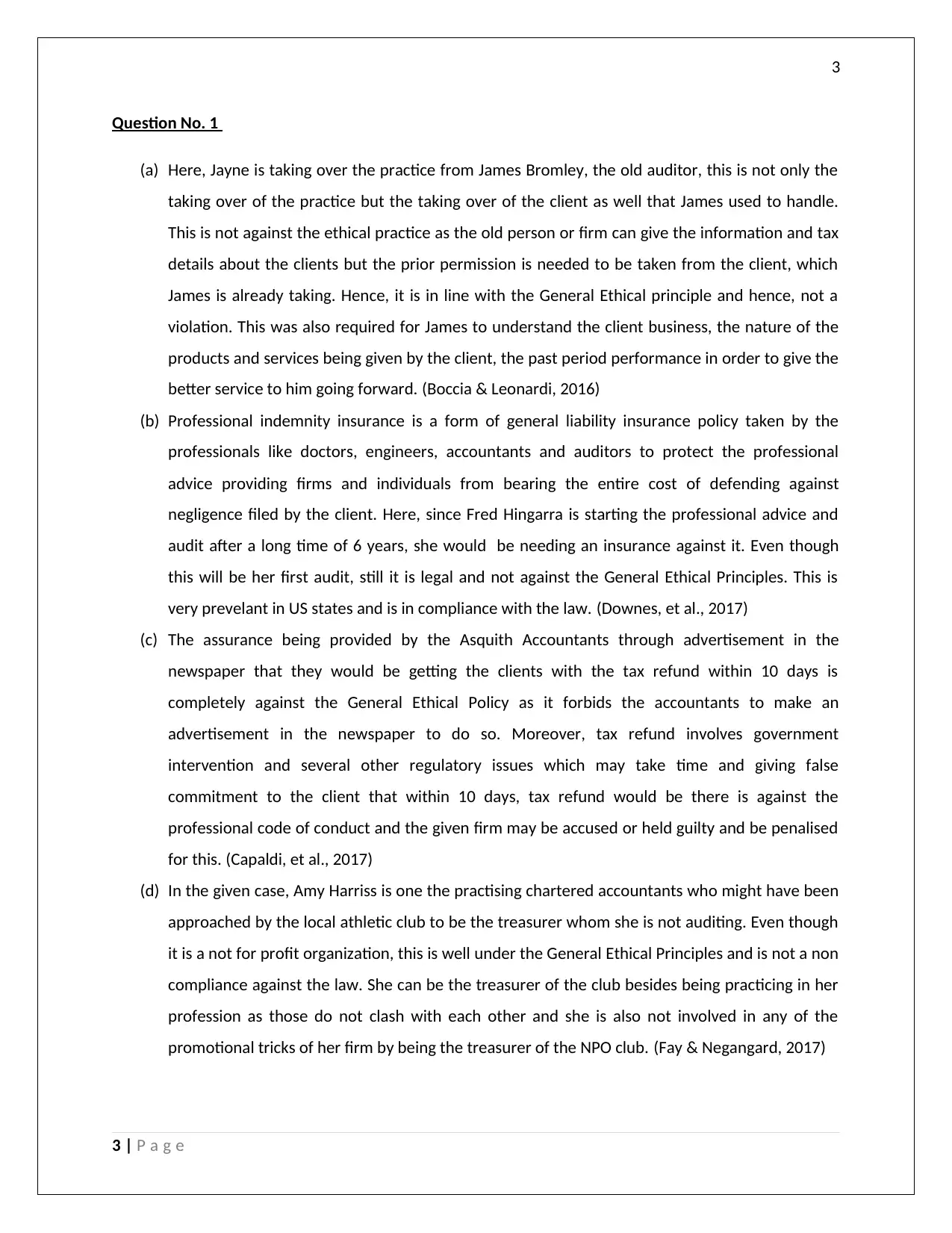

This auditing assignment addresses several scenarios related to ethical considerations and independence in auditing practices. The assignment examines situations involving the transfer of audit practices, professional indemnity insurance, misleading advertisements, conflicts of interest, and the influence of client payments on audit reports. It also explores issues of auditor independence when staff from the client's team join the audit team and when auditors encounter pressure to be flexible in their approach. The assignment also delves into reporting requirements for public companies, including the types of audit opinions, compliance with accounting standards, and the disclosure of material matters within audit reports. The assignment emphasizes adherence to ethical principles, professional conduct, and the importance of maintaining independence in financial auditing.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.