Auditing and Assurance Report: ASA 701, ASA 570 and Key Audit Matters

VerifiedAdded on 2022/08/24

|20

|3584

|19

Report

AI Summary

This report provides a comprehensive analysis of auditing and assurance, specifically focusing on the impact of the Lehman Brothers collapse and the subsequent introduction of auditing standards ASA 701 and ASA 570. It explores how the financial crisis and the failure of Lehman Brothers led to the development of these standards, which aim to improve financial reporting and provide investors with more contextual information. The report delves into the key features of ASA 701, which mandates the disclosure of key audit matters, and ASA 570, which addresses the going concern status of companies. It also examines the importance of these standards in the aftermath of the collapse, emphasizing the role of key audit matters in enhancing audit quality and improving financial reporting. Additionally, the report discusses the application of these standards within the Australian consumer staples sector, comparing and contrasting key audit matters across various companies. The report concludes with recommendations for improving the reporting of key audit matters.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Executive Summary

The collapse of Lehman Brothers along with the occurrence of world financial crisis has

largely contributed to the introduction of two specific auditing standards that are ASA 701

and ASA 570. ASA 701 requires the disclosure of the risk areas in the financial statements of

the audit client so that the investors can get more contextual information on the company’s

financial position. On the other hand, ASA 570 demands the calculation of the going concern

status of the companies by assessing that whether there is any material uncertainty that cast

major doubts on the business organizations’ capability to continue as a going concern.

Executive Summary

The collapse of Lehman Brothers along with the occurrence of world financial crisis has

largely contributed to the introduction of two specific auditing standards that are ASA 701

and ASA 570. ASA 701 requires the disclosure of the risk areas in the financial statements of

the audit client so that the investors can get more contextual information on the company’s

financial position. On the other hand, ASA 570 demands the calculation of the going concern

status of the companies by assessing that whether there is any material uncertainty that cast

major doubts on the business organizations’ capability to continue as a going concern.

2AUDITING AND ASSURANCE

Table of Contents

Introduction................................................................................................................................3

Failure of Lehman Brother.........................................................................................................3

About the Lehman Brother Case............................................................................................3

How Failure of Lehman Brothers Contribute to the Development of ASA 701...................3

What Happened in Lehman Brother Case..............................................................................3

ASA 701 and ASA 570..............................................................................................................4

ASA 701.................................................................................................................................4

ASA 570.................................................................................................................................4

Reasons for these Standards...................................................................................................4

Importance of ASA 701 and ASA 570 after the Failure of Lehman Brother........................5

Reasons for the Importance of Key Audit Matters................................................................5

What ASA 570 Tells about a Company’s Long-Term Existence..........................................5

Key Audit Matters......................................................................................................................5

Key Audit Matters of the Companies under Consumers Staples Sector................................5

Conclusion and Recommendations............................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Failure of Lehman Brother.........................................................................................................3

About the Lehman Brother Case............................................................................................3

How Failure of Lehman Brothers Contribute to the Development of ASA 701...................3

What Happened in Lehman Brother Case..............................................................................3

ASA 701 and ASA 570..............................................................................................................4

ASA 701.................................................................................................................................4

ASA 570.................................................................................................................................4

Reasons for these Standards...................................................................................................4

Importance of ASA 701 and ASA 570 after the Failure of Lehman Brother........................5

Reasons for the Importance of Key Audit Matters................................................................5

What ASA 570 Tells about a Company’s Long-Term Existence..........................................5

Key Audit Matters......................................................................................................................5

Key Audit Matters of the Companies under Consumers Staples Sector................................5

Conclusion and Recommendations............................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

Introduction

The occurrence of the world financial crisis has contributed to certain financial

accounting reforms in the form of the introduction of new accounting standards like ASA 701

and ASA 570. These standards put increased obligation of the firms to disclose more aspects

of financial reports. For example, due to the introduction of ASA 701, the firms have the

accountability to disclose information on the key audit matters in financial statements. One

prime cause of implementing these standards is to provide the investors and other users with

more precise and accurate information on the companies. There are three key parts of this

report. The first part provides detailed discussion on the collapse of Lehman Brothers and

how this collapse has contributed to the inception of ASA 701. The second part of the reports

provides discussion on two specific auditing standards named ASA 101 and ASA 570 along

with the key reasons why these standards have been introduced. The third part of the report

discusses about the key audit matters of five key business organizations in Australian

consumer staples sector along with the similarities and dissimilarities among the key audit

matters of these firms. The report also contains a concussion and suitable recommendations

on the reporting of key audit matters based on the whole analysis.

Failure of Lehman Brother

About the Lehman Brother Case

Lehman Brothers filed bankruptcy on 15 September, 2008. In the presence of $639

billion of assets and $619 billion of debts, the bankruptcy filing of Lehman Brothers is

considered as the largest bankruptcy in the history and the asset position of the company

exceeded the same of the large collapsed companies like Enron and WorldCom. At the time

of the collapse, Lehman Brothers was regarded as the fourth-largest investment banks in the

United States (US) with an employee base of 25000. It was also considered as the greatest

prey of the subprime-mortgage financial crisis of the country (Quax, Kandhai and Sloot,

2013).

How Failure of Lehman Brothers Contribute to the Development of ASA 701

The collapse of Lehman Brothers in 2008 helps in establishing the relationship

between Lehman Brothers collapse and introducing ASA 701. The Australian auditing

authority felt the necessity of introducing an auditing standard like ASA 701 because of

Lehman Brothers collapse and following financial crisis; and the auditing issued that were

largely unaddressed while Lehman Brothers was audited are now considered in ASA 701. It

was largely obligatory to address the gaps due to poor auditing of Lehman Brothers and this

contributed to the recommendation of ASA 701 (Lewis, 2015). Many key audit matters

would be identified and communicated to the management of Lehman Brothers in case ASA

701 was there while Lehman Brothers collapsed. This would enable the auditors of Lehman

Brothers in identifying and disclosing the areas with high risk in the audit report and this

could help in identifying the forthcoming collapse of the mortgage market. The fall of

Lehman Brothers would be possible to be avoided in case the auditors could assess the same.

At that time, ASA 701 would also help in recognizing specific transactions and events that

were not appropriate as per the accounting rules. This would understandably take into

consideration the use of repo rate by Lehman Brothers for covering high leverage position of

the business. In the presence of ASA 701, it would be possible for the management of

Lehman Brothers to make better strategic decision related investment at the time of housing

boom in US. This would also make it possible to properly communicate the areas where the

management and auditors made key judgments in order to comprehend the accounting

procedures of the company (Cordoş, 2015). All these aspects together contributed to the

development of ASA 701.

Introduction

The occurrence of the world financial crisis has contributed to certain financial

accounting reforms in the form of the introduction of new accounting standards like ASA 701

and ASA 570. These standards put increased obligation of the firms to disclose more aspects

of financial reports. For example, due to the introduction of ASA 701, the firms have the

accountability to disclose information on the key audit matters in financial statements. One

prime cause of implementing these standards is to provide the investors and other users with

more precise and accurate information on the companies. There are three key parts of this

report. The first part provides detailed discussion on the collapse of Lehman Brothers and

how this collapse has contributed to the inception of ASA 701. The second part of the reports

provides discussion on two specific auditing standards named ASA 101 and ASA 570 along

with the key reasons why these standards have been introduced. The third part of the report

discusses about the key audit matters of five key business organizations in Australian

consumer staples sector along with the similarities and dissimilarities among the key audit

matters of these firms. The report also contains a concussion and suitable recommendations

on the reporting of key audit matters based on the whole analysis.

Failure of Lehman Brother

About the Lehman Brother Case

Lehman Brothers filed bankruptcy on 15 September, 2008. In the presence of $639

billion of assets and $619 billion of debts, the bankruptcy filing of Lehman Brothers is

considered as the largest bankruptcy in the history and the asset position of the company

exceeded the same of the large collapsed companies like Enron and WorldCom. At the time

of the collapse, Lehman Brothers was regarded as the fourth-largest investment banks in the

United States (US) with an employee base of 25000. It was also considered as the greatest

prey of the subprime-mortgage financial crisis of the country (Quax, Kandhai and Sloot,

2013).

How Failure of Lehman Brothers Contribute to the Development of ASA 701

The collapse of Lehman Brothers in 2008 helps in establishing the relationship

between Lehman Brothers collapse and introducing ASA 701. The Australian auditing

authority felt the necessity of introducing an auditing standard like ASA 701 because of

Lehman Brothers collapse and following financial crisis; and the auditing issued that were

largely unaddressed while Lehman Brothers was audited are now considered in ASA 701. It

was largely obligatory to address the gaps due to poor auditing of Lehman Brothers and this

contributed to the recommendation of ASA 701 (Lewis, 2015). Many key audit matters

would be identified and communicated to the management of Lehman Brothers in case ASA

701 was there while Lehman Brothers collapsed. This would enable the auditors of Lehman

Brothers in identifying and disclosing the areas with high risk in the audit report and this

could help in identifying the forthcoming collapse of the mortgage market. The fall of

Lehman Brothers would be possible to be avoided in case the auditors could assess the same.

At that time, ASA 701 would also help in recognizing specific transactions and events that

were not appropriate as per the accounting rules. This would understandably take into

consideration the use of repo rate by Lehman Brothers for covering high leverage position of

the business. In the presence of ASA 701, it would be possible for the management of

Lehman Brothers to make better strategic decision related investment at the time of housing

boom in US. This would also make it possible to properly communicate the areas where the

management and auditors made key judgments in order to comprehend the accounting

procedures of the company (Cordoş, 2015). All these aspects together contributed to the

development of ASA 701.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

What Happened in Lehman Brother Case

At the time of housing boom in mid-2000s, Lehman Brothers and other investment

firms were hugely involved in mortgage-backed securities and collateral debt obligation. In

mid-2006, the housing prices started to fall quickly that made many subprime borrowers

defaulters in making the payments that showed the risky nature of these debts. Even in the

presence of these red flags, Lehman Brothers continued originating subprime mortgages. In

the presence of weakening real estate market and the absence of adequate market liquidity,

investors and other parties started to lose confidence on Lehman Brothers and firms. Like

Bear Srearns and other investment banks, the use of repurchase agreement known as ‘repo’

by Lehman Brothers for raising billions of dollars to run the business operations made the

company more exposed to any crisis in the market. The federal government refused to bail

out Lehman Brothers even after known the consequences of its collapse. Other financial

institutions like Bank of America and Barclays refuse to buy the company. Running of

options, Lehman Brothers declared its bankruptcy on 15 September, 2008 which made the

largest bankruptcy in the history of US (Azadinamin, 2013).

ASA 701 and ASA 570

ASA 701

ASA 701 Communicating Key Audit Matters in the Independent Auditor’s Report

provides the requirements to maintain the audit quality (auasb.gov.au, 2020). This standard

contains the following features:

i. This mandates communicating the key audit matters in the audit report;

ii. This permits auditors to decide on whether key audit matters need to include in the

auditor’s report;

iii. This prescribes how the auditors need to determine the key audit matters;

iv. This shows how the audit matters need to be described;

v. This assesses the circumstances when the key audit matters are not communicated;

and,

vi. This provides the documentations required for key audit matters (legislation.gov.au,

2020).

ASA 570

ASA 570 Going Concern handles the responsibility of the auditors regarding the

going concern along with its implications for the auditor’s report (auasb.gov.au, 2020). This

standard contains the following features:

i. This provides the procedures to assess the risks along with the related activities to the

auditors;

ii. This helps in evaluating the assessment of the managements regarding going concern;

iii. This needs the auditors to assess the period beyond the assessment of the

management;

iv. This prescribes the additional audit procedures when going concern issues are

identified; and,

v. This helps the auditors in concluding on the going concern issues (auasb.gov.au,

2020).

Reasons for these Standards

ASA 701 – The main purpose for having ASA 701 is to avoid the collapses like Lehman

Brothers in Australia and this also works as an alarm for the companies in the situations like

2008 global financial crisis. One main reason for the collapse of Lehman Brothers is the

disappointment of the auditors in identifying the major issue in the company’s financial

What Happened in Lehman Brother Case

At the time of housing boom in mid-2000s, Lehman Brothers and other investment

firms were hugely involved in mortgage-backed securities and collateral debt obligation. In

mid-2006, the housing prices started to fall quickly that made many subprime borrowers

defaulters in making the payments that showed the risky nature of these debts. Even in the

presence of these red flags, Lehman Brothers continued originating subprime mortgages. In

the presence of weakening real estate market and the absence of adequate market liquidity,

investors and other parties started to lose confidence on Lehman Brothers and firms. Like

Bear Srearns and other investment banks, the use of repurchase agreement known as ‘repo’

by Lehman Brothers for raising billions of dollars to run the business operations made the

company more exposed to any crisis in the market. The federal government refused to bail

out Lehman Brothers even after known the consequences of its collapse. Other financial

institutions like Bank of America and Barclays refuse to buy the company. Running of

options, Lehman Brothers declared its bankruptcy on 15 September, 2008 which made the

largest bankruptcy in the history of US (Azadinamin, 2013).

ASA 701 and ASA 570

ASA 701

ASA 701 Communicating Key Audit Matters in the Independent Auditor’s Report

provides the requirements to maintain the audit quality (auasb.gov.au, 2020). This standard

contains the following features:

i. This mandates communicating the key audit matters in the audit report;

ii. This permits auditors to decide on whether key audit matters need to include in the

auditor’s report;

iii. This prescribes how the auditors need to determine the key audit matters;

iv. This shows how the audit matters need to be described;

v. This assesses the circumstances when the key audit matters are not communicated;

and,

vi. This provides the documentations required for key audit matters (legislation.gov.au,

2020).

ASA 570

ASA 570 Going Concern handles the responsibility of the auditors regarding the

going concern along with its implications for the auditor’s report (auasb.gov.au, 2020). This

standard contains the following features:

i. This provides the procedures to assess the risks along with the related activities to the

auditors;

ii. This helps in evaluating the assessment of the managements regarding going concern;

iii. This needs the auditors to assess the period beyond the assessment of the

management;

iv. This prescribes the additional audit procedures when going concern issues are

identified; and,

v. This helps the auditors in concluding on the going concern issues (auasb.gov.au,

2020).

Reasons for these Standards

ASA 701 – The main purpose for having ASA 701 is to avoid the collapses like Lehman

Brothers in Australia and this also works as an alarm for the companies in the situations like

2008 global financial crisis. One main reason for the collapse of Lehman Brothers is the

disappointment of the auditors in identifying the major issue in the company’s financial

5AUDITING AND ASSURANCE

reports and the effects of the global financial crisis on the company’s financial statements.

Reviving this situation is the main reason for ASA 701 as this enables the auditors in

communicating the areas of risks in the auditor’s report so that the company’s management

and investors can know about this. Knowing these risk areas helps in formulating effective

strategies (Azim, 2013). All these aspects together help in increasing the quality of overall

audit.

ASA 570 – The occurrence of the global financial crisis and the fall of Lehman Brothers has

put major doubts on the ability of the firms to continue as a going concern in coming future.

For the collapse of Lehman Brothers, no one had the idea that the fourth largest investment

bank of US was going to be bankrupt due to major issue inside it. This is the main reason of

having ASA 570 in Australia so that the presence of any material uncertainty in the

companies that cast major doubts on their capability for continuing as going concerns can be

identified. Identification of the presence of any material uncertainty in the companies help the

managements in taking corrective measures to revive the situation; and communication of the

same helps the investors in knowing the actual going concern position of the businesses.

These are the main reasons of having ASA 570 (Brunelli, 2018).

Importance of ASA 701 and ASA 570 after the Failure of Lehman Brother

Both ASA 701 and ASA 570 have key importance while considering the collapse of

Lehman Brothers. The company collapsed as poor auditing failed in the identification as well

as communication of major financial issues within the organization. At the same time, the

auditors also failed in assessing the impact of the subprime mortgage crisis on the business of

Lehman Brothers. The inception of these two accounting standards could be seen after the

collapse of Lehman Brothers in order to strengthen auditing with the aim to identify and

communicate the major areas of risks and material uncertainties on the going concern status

of the firms. All these make these standards of key significance (Mawutor, 2014).

Reasons for the Importance of Key Audit Matters

The concept of key audit matters came into the picture out of the investors’ demand

for more details and contextual information for helping them in determining the clean audit

report. Three main causes for the increased importance of key audit matters are discussed

below:

1. Better conversations between the auditors and those who are charged with governance

have become possible because of the key audit matters. Sequentially, this has

contributed to better governance (Cordoş and Fülöp, 2015).

2. Key audit matters assist the auditor in focusing on the parts of the audit that require

the most cautious audit judgment. Sequentially, this has contributes to better audit

judgment.

3. Key audit matters deliver the preparers of the financial reports with the motivations

for revisiting the financial reporting as well as disclosures in the areas associated with

key audit matters. This in turn has led to high quality of financial reporting (Sirois,

Bédard and Bera, 2018).

What ASA 570 Tells about a Company’s Long-Term Existence

ASA 570 discusses about the going concern issues within the organizations that is

most relevant at the time of economic difficulty and in certain circumstances where the

management may determine that the business may not be able in continuing as a going

concern because of certain issues. As per ASA 570, three aspects need to be considered by

the management of the companies for the going concern; they are the amount of

improbability associated with the outcome of an even casting major doubts on the company’s

reports and the effects of the global financial crisis on the company’s financial statements.

Reviving this situation is the main reason for ASA 701 as this enables the auditors in

communicating the areas of risks in the auditor’s report so that the company’s management

and investors can know about this. Knowing these risk areas helps in formulating effective

strategies (Azim, 2013). All these aspects together help in increasing the quality of overall

audit.

ASA 570 – The occurrence of the global financial crisis and the fall of Lehman Brothers has

put major doubts on the ability of the firms to continue as a going concern in coming future.

For the collapse of Lehman Brothers, no one had the idea that the fourth largest investment

bank of US was going to be bankrupt due to major issue inside it. This is the main reason of

having ASA 570 in Australia so that the presence of any material uncertainty in the

companies that cast major doubts on their capability for continuing as going concerns can be

identified. Identification of the presence of any material uncertainty in the companies help the

managements in taking corrective measures to revive the situation; and communication of the

same helps the investors in knowing the actual going concern position of the businesses.

These are the main reasons of having ASA 570 (Brunelli, 2018).

Importance of ASA 701 and ASA 570 after the Failure of Lehman Brother

Both ASA 701 and ASA 570 have key importance while considering the collapse of

Lehman Brothers. The company collapsed as poor auditing failed in the identification as well

as communication of major financial issues within the organization. At the same time, the

auditors also failed in assessing the impact of the subprime mortgage crisis on the business of

Lehman Brothers. The inception of these two accounting standards could be seen after the

collapse of Lehman Brothers in order to strengthen auditing with the aim to identify and

communicate the major areas of risks and material uncertainties on the going concern status

of the firms. All these make these standards of key significance (Mawutor, 2014).

Reasons for the Importance of Key Audit Matters

The concept of key audit matters came into the picture out of the investors’ demand

for more details and contextual information for helping them in determining the clean audit

report. Three main causes for the increased importance of key audit matters are discussed

below:

1. Better conversations between the auditors and those who are charged with governance

have become possible because of the key audit matters. Sequentially, this has

contributed to better governance (Cordoş and Fülöp, 2015).

2. Key audit matters assist the auditor in focusing on the parts of the audit that require

the most cautious audit judgment. Sequentially, this has contributes to better audit

judgment.

3. Key audit matters deliver the preparers of the financial reports with the motivations

for revisiting the financial reporting as well as disclosures in the areas associated with

key audit matters. This in turn has led to high quality of financial reporting (Sirois,

Bédard and Bera, 2018).

What ASA 570 Tells about a Company’s Long-Term Existence

ASA 570 discusses about the going concern issues within the organizations that is

most relevant at the time of economic difficulty and in certain circumstances where the

management may determine that the business may not be able in continuing as a going

concern because of certain issues. As per ASA 570, three aspects need to be considered by

the management of the companies for the going concern; they are the amount of

improbability associated with the outcome of an even casting major doubts on the company’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

ability of continuing the business operations as a going concern; the entity’s size and

complexity and any judgment about the future. It implies that ASA 570 helps in assessing the

fact that whether a company has the sufficient cash inflows and other resources to continue

its business operations for long-term (Xu, et al., 2013).

Key Audit Matters

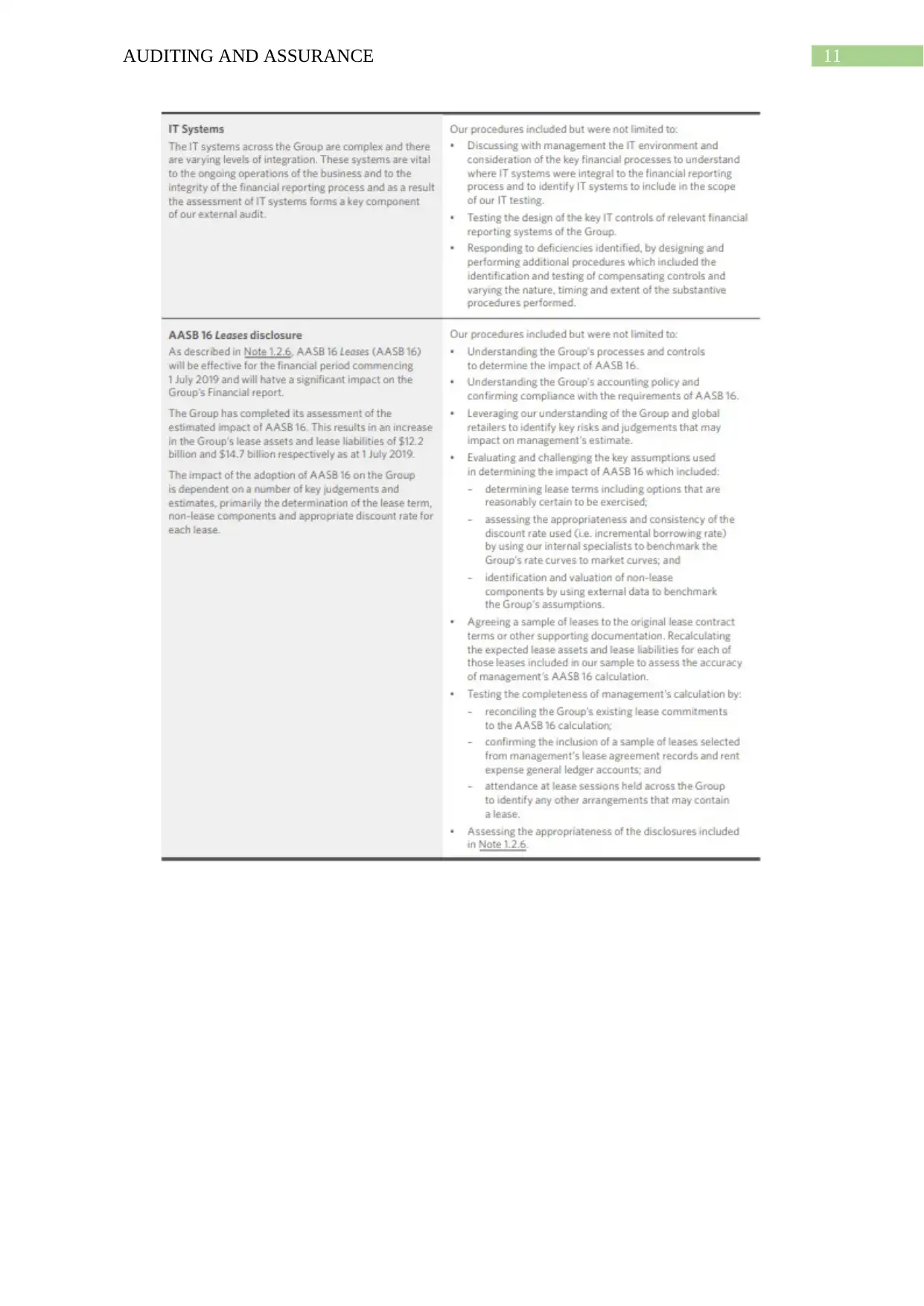

Key Audit Matters of the Companies under Consumers Staples Sector

The following table shows the key audit matters of the top five ASX listed companies

operating in the Australian consumer staples sector.

Company Name Key Audit Matters

Woolworths Group Limited The auditors have reported three key audit matters; they

are Onerous lease provision and impairment of asset in the

BIG W business; IT system and Disclosure of AASB 16

Leases. The auditor’s responses include evaluation of

major assumptions, evaluation of historical accuracy,

sensitivity analysis and others (woolworthsgroup.com.au,

2020).

Treasury Wine Estate There are two key audit matters. They are inventory

valuation that includes total finished goods and work-in-

progress inventory worth $2032.2 million; and Discounts

and debates recognition that include net sales revenue that

is the net sales of trade discount and volume rebates worth

$2831.6 million. The audit procedures include testing of

control, yean-end inventory test and others

(tweglobal.com, 2020).

The A2 Milk Company The auditors have reported only one key audit matters that

is Discounts and rebates provided to the customers. The

audit procedures include consideration of the

appropriateness of revenue recognition, evaluation of the

company’s processes, sample testing and others

(thea2milkcompany.com, 2020).

Coles Group Seven key audit matters have been reported by the

auditors. They are commercial income; non-current asset

impairment that includes intangible assets; IT

environment, AASB 16 Leases, existence of inventory,

Accounting for the department of the Group from

Wesfarmers Limited; and Accounting related to major

contracts. The audit procedures are gaining understanding

of the company’s material commercial incomes, taking the

assistance of valuation experts, testing of significant

agreements and others (colesgroup.com.au, 2020).

Coca-Cola Amatil Three key audit matters have been reported by the

auditors. They are Carrying value of the cash generating

units of Indonesia; Accounting related to rebates and

promotional allowance; and SPC asset held for sale. The

audit procedures include valuation of the appropriateness

of the used methodology, testing the mathematical

accuracy of cash flows model, consideration of the

application of Australian Accounting Standards and others

ability of continuing the business operations as a going concern; the entity’s size and

complexity and any judgment about the future. It implies that ASA 570 helps in assessing the

fact that whether a company has the sufficient cash inflows and other resources to continue

its business operations for long-term (Xu, et al., 2013).

Key Audit Matters

Key Audit Matters of the Companies under Consumers Staples Sector

The following table shows the key audit matters of the top five ASX listed companies

operating in the Australian consumer staples sector.

Company Name Key Audit Matters

Woolworths Group Limited The auditors have reported three key audit matters; they

are Onerous lease provision and impairment of asset in the

BIG W business; IT system and Disclosure of AASB 16

Leases. The auditor’s responses include evaluation of

major assumptions, evaluation of historical accuracy,

sensitivity analysis and others (woolworthsgroup.com.au,

2020).

Treasury Wine Estate There are two key audit matters. They are inventory

valuation that includes total finished goods and work-in-

progress inventory worth $2032.2 million; and Discounts

and debates recognition that include net sales revenue that

is the net sales of trade discount and volume rebates worth

$2831.6 million. The audit procedures include testing of

control, yean-end inventory test and others

(tweglobal.com, 2020).

The A2 Milk Company The auditors have reported only one key audit matters that

is Discounts and rebates provided to the customers. The

audit procedures include consideration of the

appropriateness of revenue recognition, evaluation of the

company’s processes, sample testing and others

(thea2milkcompany.com, 2020).

Coles Group Seven key audit matters have been reported by the

auditors. They are commercial income; non-current asset

impairment that includes intangible assets; IT

environment, AASB 16 Leases, existence of inventory,

Accounting for the department of the Group from

Wesfarmers Limited; and Accounting related to major

contracts. The audit procedures are gaining understanding

of the company’s material commercial incomes, taking the

assistance of valuation experts, testing of significant

agreements and others (colesgroup.com.au, 2020).

Coca-Cola Amatil Three key audit matters have been reported by the

auditors. They are Carrying value of the cash generating

units of Indonesia; Accounting related to rebates and

promotional allowance; and SPC asset held for sale. The

audit procedures include valuation of the appropriateness

of the used methodology, testing the mathematical

accuracy of cash flows model, consideration of the

application of Australian Accounting Standards and others

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

(asx.com.au, 2020).

The above table shows that there are certain similarities among the reported key audit

matters in these five companies. Most of these companies have certain key audit matters in

common. For example, accounting for rebate is a common key audit matter in this industry

that can be seen in Treasury Wine Estate, The A2 Mil Company and Coca Cola Amatil as the

companies have to provide discount to the customers in the industry. Impairment of assets is

another common key audit matter that can be seen Woolworths Group Limited and Coles

Group. Another common key audit matter in these companies are accounting under AASB 16

Lease due to the adoption of this lease standards. Inventory is another key audit matter in

most of these companies because of the nature of goods and huge amount of sales. Lastly,

another common key audit matter in most of these companies are IT system because of the

dependence of these companies on advanced technology for daily business operations. All

these facets indicate towards the auditors’ effectiveness to report the key audit matters by

taking into consideration all the required factors in the company and the industry.

Conclusion and Recommendations

The above analysis displays the importance of ASA 701 and ASA 570 in the auditing

profession which help in increasing the audit quality by ensuring the disclosure of additional

contextual information about the companies’ financial aspects. Since there were major faults

from the auditors’ side in the collapse of Lehman Brothers, these two auditing standards have

been introduced to ensure that the same errors do not repeat. ASA 701 ensures the disclosure

of risk factors in the company’s financial aspects and ASA 570 ensures the disclosure of

additional information on the going concern position of the businesses. The auditors of the

selected five companies operating in the Australian consumer staples industry have correctly

disclosed the key audit matters along with the audit steps taken.

Based on the above discussion, the recommendation to the Australian auditors is to

ensure taking into consideration the auditing standards of ASA 701 and ASA 570 while

carrying out the audit works. This will help them in identifying the risk areas in the audit

clients’ financial statements and they will be able in assessing whether there is any material

doubt that casts key doubts on their capability to continue as going concerns. All these

together would help in enhancing the overall audit quality in Australia.

(asx.com.au, 2020).

The above table shows that there are certain similarities among the reported key audit

matters in these five companies. Most of these companies have certain key audit matters in

common. For example, accounting for rebate is a common key audit matter in this industry

that can be seen in Treasury Wine Estate, The A2 Mil Company and Coca Cola Amatil as the

companies have to provide discount to the customers in the industry. Impairment of assets is

another common key audit matter that can be seen Woolworths Group Limited and Coles

Group. Another common key audit matter in these companies are accounting under AASB 16

Lease due to the adoption of this lease standards. Inventory is another key audit matter in

most of these companies because of the nature of goods and huge amount of sales. Lastly,

another common key audit matter in most of these companies are IT system because of the

dependence of these companies on advanced technology for daily business operations. All

these facets indicate towards the auditors’ effectiveness to report the key audit matters by

taking into consideration all the required factors in the company and the industry.

Conclusion and Recommendations

The above analysis displays the importance of ASA 701 and ASA 570 in the auditing

profession which help in increasing the audit quality by ensuring the disclosure of additional

contextual information about the companies’ financial aspects. Since there were major faults

from the auditors’ side in the collapse of Lehman Brothers, these two auditing standards have

been introduced to ensure that the same errors do not repeat. ASA 701 ensures the disclosure

of risk factors in the company’s financial aspects and ASA 570 ensures the disclosure of

additional information on the going concern position of the businesses. The auditors of the

selected five companies operating in the Australian consumer staples industry have correctly

disclosed the key audit matters along with the audit steps taken.

Based on the above discussion, the recommendation to the Australian auditors is to

ensure taking into consideration the auditing standards of ASA 701 and ASA 570 while

carrying out the audit works. This will help them in identifying the risk areas in the audit

clients’ financial statements and they will be able in assessing whether there is any material

doubt that casts key doubts on their capability to continue as going concerns. All these

together would help in enhancing the overall audit quality in Australia.

8AUDITING AND ASSURANCE

References

Asx.com.au. 2020. Annual Report 2018. [online] Available at:

https://www.asx.com.au/asxpdf/20190410/pdf/4446672z94vgfh.pdf [Accessed 20 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 570 Going Concern. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 20 Jan.

2020].

Auasb.gov.au. 2020. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed 20 Jan. 2020].

Azadinamin, A., 2013. The bankruptcy of Lehman brothers: causes of failure &

recommendations going forward. Swiss Management Center (SMC) University.

Azim, M.I., 2013. Independent Auditors Report: Australian Trends From 1996 to

2010. Journal of Modern Accounting and Auditing, 9(3), p.356.

Brunelli, S., 2018. The Firm’Going Concern in the Contemporary Era. In Audit Reporting for

Going Concern Uncertainty (pp. 1-25). Springer, Cham.

Colesgroup.com.au. 2020. 2019 Annual Report. [online] Available at:

https://www.colesgroup.com.au/FormBuilder/_Resource/_module/ir5sKeTxxEOndzdh00hW

Jw/file/Coles_Annual_Report_2019.pdf [Accessed 20 Jan. 2020].

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Cordoş, G.S., 2015. Implications of the current exposure draft on audit

reporting. Management Intercultural, (33), pp.61-70.

Legislation.gov.au. 2020. ASA 701 - Communicating Key Audit Matters in the Independent

Auditor’s Report - December 2015 . [online] Available at:

https://www.legislation.gov.au/Details/F2015L02016/Explanatory%20Statement/Text

[Accessed 20 Jan. 2020].

Lewis, M., 2015. The Fall of the Lehman Brothers Could IT Have Been Avoided?. Available

at SSRN 2572716.

Mawutor, J.K.M., 2014. The failure of Lehman Brothers: causes, preventive measures and

recommendations. Research Journal of Finance and Accounting, 5(4).

Quax, R., Kandhai, D. and Sloot, P.M., 2013. Information dissipation as an early-warning

signal for the Lehman Brothers collapse in financial time series. Scientific reports, 3, p.1898.

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-

162.

Thea2milkcompany.com. 2020. 2019 Annual Report. [online] Available at:

https://thea2milkcompany.com/wp-content/uploads/The-a2-Milk-Company_FY19-Annual-

Report_double-pages-1.pdf [Accessed 20 Jan. 2020].

References

Asx.com.au. 2020. Annual Report 2018. [online] Available at:

https://www.asx.com.au/asxpdf/20190410/pdf/4446672z94vgfh.pdf [Accessed 20 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 570 Going Concern. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 20 Jan.

2020].

Auasb.gov.au. 2020. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed 20 Jan. 2020].

Azadinamin, A., 2013. The bankruptcy of Lehman brothers: causes of failure &

recommendations going forward. Swiss Management Center (SMC) University.

Azim, M.I., 2013. Independent Auditors Report: Australian Trends From 1996 to

2010. Journal of Modern Accounting and Auditing, 9(3), p.356.

Brunelli, S., 2018. The Firm’Going Concern in the Contemporary Era. In Audit Reporting for

Going Concern Uncertainty (pp. 1-25). Springer, Cham.

Colesgroup.com.au. 2020. 2019 Annual Report. [online] Available at:

https://www.colesgroup.com.au/FormBuilder/_Resource/_module/ir5sKeTxxEOndzdh00hW

Jw/file/Coles_Annual_Report_2019.pdf [Accessed 20 Jan. 2020].

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Cordoş, G.S., 2015. Implications of the current exposure draft on audit

reporting. Management Intercultural, (33), pp.61-70.

Legislation.gov.au. 2020. ASA 701 - Communicating Key Audit Matters in the Independent

Auditor’s Report - December 2015 . [online] Available at:

https://www.legislation.gov.au/Details/F2015L02016/Explanatory%20Statement/Text

[Accessed 20 Jan. 2020].

Lewis, M., 2015. The Fall of the Lehman Brothers Could IT Have Been Avoided?. Available

at SSRN 2572716.

Mawutor, J.K.M., 2014. The failure of Lehman Brothers: causes, preventive measures and

recommendations. Research Journal of Finance and Accounting, 5(4).

Quax, R., Kandhai, D. and Sloot, P.M., 2013. Information dissipation as an early-warning

signal for the Lehman Brothers collapse in financial time series. Scientific reports, 3, p.1898.

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-

162.

Thea2milkcompany.com. 2020. 2019 Annual Report. [online] Available at:

https://thea2milkcompany.com/wp-content/uploads/The-a2-Milk-Company_FY19-Annual-

Report_double-pages-1.pdf [Accessed 20 Jan. 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Tweglobal.com. 2020. ANNUAL REPORT 2019. [online] Available at:

https://www.tweglobal.com/-/media/Files/Global/Annual-Reports/2019-Annual-Report.ashx

[Accessed 20 Jan. 2020].

Woolworthsgroup.com.au. 2020. 2019 ANNUAL REPORT. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf [Accessed

20 Jan. 2020].

Xu, Y., Carson, E., Fargher, N. and Jiang, L., 2013. Responses by Australian auditors to the

global financial crisis. Accounting & Finance, 53(1), pp.301-338.

Tweglobal.com. 2020. ANNUAL REPORT 2019. [online] Available at:

https://www.tweglobal.com/-/media/Files/Global/Annual-Reports/2019-Annual-Report.ashx

[Accessed 20 Jan. 2020].

Woolworthsgroup.com.au. 2020. 2019 ANNUAL REPORT. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf [Accessed

20 Jan. 2020].

Xu, Y., Carson, E., Fargher, N. and Jiang, L., 2013. Responses by Australian auditors to the

global financial crisis. Accounting & Finance, 53(1), pp.301-338.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

Appendix

Key Audit Matters of Woolworths Group Limited

Appendix

Key Audit Matters of Woolworths Group Limited

11AUDITING AND ASSURANCE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.