Auditing Report: Risk Assessment of Medibank Private Limited - Finance

VerifiedAdded on 2020/05/28

|13

|3119

|33

Report

AI Summary

This auditing report provides an in-depth analysis of Medibank Private Limited, Australia's largest private health insurance provider. The report begins with an executive summary and an introduction to the company, including its regulatory environment, applicable financial framework, and operational structure. It then delves into the entity's objectives, assessing related business and financial risks such as competition, healthcare costs, regulatory changes, and investment risks. A significant portion of the report focuses on identifying account balances susceptible to material misstatement, specifically addressing liquidity risk, credit risk, and price risk. For each risk, the report explains the potential for misstatement and the key assertions at risk. The report highlights the importance of understanding the company's internal controls and applying appropriate audit procedures to mitigate these risks, with references to Australian Auditing Standards and relevant financial data from Medibank's annual reports. The report concludes with a synthesis of the key findings and implications for auditing Medibank Private Limited.

Running head: Auditing

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 1

Executive Summary

As per Australian Auditing Standard ASA 315, it deals with the auditor’s accountability to recognize and

evaluate the risks of substantial misstatements in the financial reports of the company. It is done

through comprehending the organization and its atmosphere, including its internal control. The aim of

the auditor is to recognize the threats of substantial mismanagement, occurred as a result of deception

or mistake.

The risk evaluation methods shall comprise of enquiring the managerial personnel, whether they have

any information which would help them in the evaluation of risk of substantial misstatements. The

others include analytical procedures and examination. The business risk comprises of the risk resulting

from certain circumstances, which could affect the organization’s ability to achieve its goals.

In this report, Medibank Private Limited, the largest provider of health insurance in Australia, would be

assessed to recognize and evaluate the risk of substantial mismanagement, by PricewaterhouseCoopers.

Also, the audit procedures applied to assert the risk and internal control methods to lessen it ,would be

reflected upon.

Executive Summary

As per Australian Auditing Standard ASA 315, it deals with the auditor’s accountability to recognize and

evaluate the risks of substantial misstatements in the financial reports of the company. It is done

through comprehending the organization and its atmosphere, including its internal control. The aim of

the auditor is to recognize the threats of substantial mismanagement, occurred as a result of deception

or mistake.

The risk evaluation methods shall comprise of enquiring the managerial personnel, whether they have

any information which would help them in the evaluation of risk of substantial misstatements. The

others include analytical procedures and examination. The business risk comprises of the risk resulting

from certain circumstances, which could affect the organization’s ability to achieve its goals.

In this report, Medibank Private Limited, the largest provider of health insurance in Australia, would be

assessed to recognize and evaluate the risk of substantial mismanagement, by PricewaterhouseCoopers.

Also, the audit procedures applied to assert the risk and internal control methods to lessen it ,would be

reflected upon.

Auditing 2

Table of Contents

Executive Summary.....................................................................................................................................1

1. Report on the knowledge gained of this entity and its environment..................................................3

Introduction to the company...................................................................................................................3

Regulatory Authority of the private health insurance sector in Australia................................................3

Applicable Financial Framework on Medibank Private Limited...............................................................3

Nature of Company’s Operations, its governance structures and its investments..................................3

Application of Accounting Policies in Medibank Private Limited.............................................................4

2. Entity’s Objectives and Assessment of related Business Risks.............................................................5

Entity’s Objectives...................................................................................................................................5

Assessment of related Business and Financial Risks................................................................................5

3. Identification of Account Balances Subjected to Risk of Material Misstatement................................7

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

Table of Contents

Executive Summary.....................................................................................................................................1

1. Report on the knowledge gained of this entity and its environment..................................................3

Introduction to the company...................................................................................................................3

Regulatory Authority of the private health insurance sector in Australia................................................3

Applicable Financial Framework on Medibank Private Limited...............................................................3

Nature of Company’s Operations, its governance structures and its investments..................................3

Application of Accounting Policies in Medibank Private Limited.............................................................4

2. Entity’s Objectives and Assessment of related Business Risks.............................................................5

Entity’s Objectives...................................................................................................................................5

Assessment of related Business and Financial Risks................................................................................5

3. Identification of Account Balances Subjected to Risk of Material Misstatement................................7

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 3

1. Report on the knowledge gained of this entity and its environment

Introduction to the company

Medibank Private Limited is the largest private health insurance provider in Australia. It operates in the

health insurance industry. It insures and sells its policies under the brand names: Medibank and AHM. It

has around 3.8 Million members and covers 29.1% of the market share. It operates as a public listed

company on ASX. It also deals in assisting the health insurance business, thereby earning income from

its ‘Complimentary Services’. Resources are also retained to compensate its regulatory reserves, which

generates monetary benefits from its portfolio of investment assets.

Regulatory Authority of the private health insurance sector in Australia

The private health insurance sector is regulated by Australian Prudential Regulation Authority (APRA) in

Australia (APRA, 2018). The organizations operating in the private health insurance sector in Australia

have to comply with the ‘APRA rules’ and ‘Prudential Standards ’. Also it is mandatory for the private

health insurers to provide information under the Financial Sector (Collection of Data) Act, 2001 and its

reporting standard to APRA. The organizations have to submit certain forms and follow directions of

APRA in this regard (Kokobe & Gemechu, 2016).

Applicable Financial Framework on Medibank Private Limited

The applicable laws and legislations on the ‘Medibank Private Limited ‘are:

Auditing and Assurance Standards Board

1. Australian Accounting Standards Board

2. Australian Prudential Regulation Authority

3. Australian Securities and Investment Commission

4. Financial Reporting Council

5. Financial System Inquiry

6. Standard Business Reporting

Nature of Company’s Operations, its governance structures and its investments

The company operates in the private health insurance sector in which it provides health insurance to the

people. Along with this, it also provides consultancies for health management and telehealth services

for the government and corporate consumers. It also trades in the travel, life and pet insurance products

and services.

1. Report on the knowledge gained of this entity and its environment

Introduction to the company

Medibank Private Limited is the largest private health insurance provider in Australia. It operates in the

health insurance industry. It insures and sells its policies under the brand names: Medibank and AHM. It

has around 3.8 Million members and covers 29.1% of the market share. It operates as a public listed

company on ASX. It also deals in assisting the health insurance business, thereby earning income from

its ‘Complimentary Services’. Resources are also retained to compensate its regulatory reserves, which

generates monetary benefits from its portfolio of investment assets.

Regulatory Authority of the private health insurance sector in Australia

The private health insurance sector is regulated by Australian Prudential Regulation Authority (APRA) in

Australia (APRA, 2018). The organizations operating in the private health insurance sector in Australia

have to comply with the ‘APRA rules’ and ‘Prudential Standards ’. Also it is mandatory for the private

health insurers to provide information under the Financial Sector (Collection of Data) Act, 2001 and its

reporting standard to APRA. The organizations have to submit certain forms and follow directions of

APRA in this regard (Kokobe & Gemechu, 2016).

Applicable Financial Framework on Medibank Private Limited

The applicable laws and legislations on the ‘Medibank Private Limited ‘are:

Auditing and Assurance Standards Board

1. Australian Accounting Standards Board

2. Australian Prudential Regulation Authority

3. Australian Securities and Investment Commission

4. Financial Reporting Council

5. Financial System Inquiry

6. Standard Business Reporting

Nature of Company’s Operations, its governance structures and its investments

The company operates in the private health insurance sector in which it provides health insurance to the

people. Along with this, it also provides consultancies for health management and telehealth services

for the government and corporate consumers. It also trades in the travel, life and pet insurance products

and services.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 4

The health insurance business granted 91.6 % of the group’s revenue and 95.4 % of the segment

operating profit in 2016 (Medibank, 2016). The amount of revenue amounted to 91.9 % whereas the

segment operating profit decreased to 93.3 % in 2017 (Medibank, 2017). From the overall income

earned by the group in 2016 and 2017, the resident health insurance policies sold to the retail and

corporate consumers contributed to 97.8 %.

In 2016 and 2017, the investment portfolio was $2.5 Billion comprising of cash and other investments. It

provides sufficient cash to cover the insurance obligations and the mandatory reserves to meet claims

related to the Health Insurance business (Medibank, 2017).

The governance structure of Medibank Private Limited is as follows:

1. Audit committee- It supervises the financial reporting

2. Risk Management Committee- It assesses the organization’s present and future risk

management.

3. Investment and Capital Committee- It controls the investments and capital management events.

4. People and Remuneration Committee- It supervise the policies related to remuneration and

people.

5. Nomination Committee- It controls the overall board and committee membership and hierarchy

of the organization.

Apart from the committees, the Chief Executive Officer and Executive Leadership Team are

accountable for the performance of the company.

According to the Medibank (2016) the net income after tax in 2016 amounted to $417 Million while

in 2017 it was $ 452 Million. The total assets amounted to $ 3266.2 Million in 2016, while in 2017 it

was $ 3462.5 Million (Medibank, 2017).The total liabilities amounted to $ 1578.7 Million in 2016

while in 2017, it was $ 1742.7 Million. The total equity which comprises of Contributed Equity,

Reserves and Retained Earnings amounted to $1578.7 Million in 2016 while in 2017; it amounted to

$ 1719.8 Million. The organization’s investment portfolio comprises of 25 % /75% for growth and

defensive assets respectively. The company invests in listed and unlisted securities which are

quoted at their fair value.

The health insurance business granted 91.6 % of the group’s revenue and 95.4 % of the segment

operating profit in 2016 (Medibank, 2016). The amount of revenue amounted to 91.9 % whereas the

segment operating profit decreased to 93.3 % in 2017 (Medibank, 2017). From the overall income

earned by the group in 2016 and 2017, the resident health insurance policies sold to the retail and

corporate consumers contributed to 97.8 %.

In 2016 and 2017, the investment portfolio was $2.5 Billion comprising of cash and other investments. It

provides sufficient cash to cover the insurance obligations and the mandatory reserves to meet claims

related to the Health Insurance business (Medibank, 2017).

The governance structure of Medibank Private Limited is as follows:

1. Audit committee- It supervises the financial reporting

2. Risk Management Committee- It assesses the organization’s present and future risk

management.

3. Investment and Capital Committee- It controls the investments and capital management events.

4. People and Remuneration Committee- It supervise the policies related to remuneration and

people.

5. Nomination Committee- It controls the overall board and committee membership and hierarchy

of the organization.

Apart from the committees, the Chief Executive Officer and Executive Leadership Team are

accountable for the performance of the company.

According to the Medibank (2016) the net income after tax in 2016 amounted to $417 Million while

in 2017 it was $ 452 Million. The total assets amounted to $ 3266.2 Million in 2016, while in 2017 it

was $ 3462.5 Million (Medibank, 2017).The total liabilities amounted to $ 1578.7 Million in 2016

while in 2017, it was $ 1742.7 Million. The total equity which comprises of Contributed Equity,

Reserves and Retained Earnings amounted to $1578.7 Million in 2016 while in 2017; it amounted to

$ 1719.8 Million. The organization’s investment portfolio comprises of 25 % /75% for growth and

defensive assets respectively. The company invests in listed and unlisted securities which are

quoted at their fair value.

Auditing 5

Application of Accounting Policies in Medibank Private Limited

The financial statements of the entity are authorized to be issued according to the resolution of the

directors. They are prepared for the consolidated entity (Group) comprising of Medibank and its

subsidiaries. The statement of accounts has been prepared according to the ‘Historical Cost Convention’

except the financial assets, land and building and liabilities quoted at their fair value or market price.

Also it follows different accounting policies according to its various segments.

2. Entity’s Objectives and Assessment of related Business Risks

Entity’s Objectives

The organization has set the following objectives for achieving better health for the human community

as a whole:

1. It aims to diversify the Medibank and AHM products to distribute the best services and

consultancy to its consumers.

2. It focuses on developing and offering the leading services to its customers.

3. Also as a part of its corporate social responsibility, it invests $ 4 Million towards childhood

obesity.

4. The Medibank Better Health Foundation focuses to develop health awareness in the society.

5. It has evolved ecofriendly policies as it believes that a healthy environment can create healthy

humans. It has endeavored to develop the green space in urban areas up to 20% by

2020(Medibank, 2018).

Assessment of related Business and Financial Risks

The substantial business risk which could influence Medibank’s business activities are as follows

(Auditing and Assurance Standards Board, 2013):

1. Competition and retaining of consumers: The emergence of new firms, with their partnership

with the existing firms can pose a threat to company’s existence in the market. The private

health insurers and assessment websites compete to retain the consumers regarding price,

products, service and channels which results in the diversion of the customers.

2. Health care prices and utilization: The increase in the health care costs can have an impact on

product margins. This can lead to reduction in the value of products.

Application of Accounting Policies in Medibank Private Limited

The financial statements of the entity are authorized to be issued according to the resolution of the

directors. They are prepared for the consolidated entity (Group) comprising of Medibank and its

subsidiaries. The statement of accounts has been prepared according to the ‘Historical Cost Convention’

except the financial assets, land and building and liabilities quoted at their fair value or market price.

Also it follows different accounting policies according to its various segments.

2. Entity’s Objectives and Assessment of related Business Risks

Entity’s Objectives

The organization has set the following objectives for achieving better health for the human community

as a whole:

1. It aims to diversify the Medibank and AHM products to distribute the best services and

consultancy to its consumers.

2. It focuses on developing and offering the leading services to its customers.

3. Also as a part of its corporate social responsibility, it invests $ 4 Million towards childhood

obesity.

4. The Medibank Better Health Foundation focuses to develop health awareness in the society.

5. It has evolved ecofriendly policies as it believes that a healthy environment can create healthy

humans. It has endeavored to develop the green space in urban areas up to 20% by

2020(Medibank, 2018).

Assessment of related Business and Financial Risks

The substantial business risk which could influence Medibank’s business activities are as follows

(Auditing and Assurance Standards Board, 2013):

1. Competition and retaining of consumers: The emergence of new firms, with their partnership

with the existing firms can pose a threat to company’s existence in the market. The private

health insurers and assessment websites compete to retain the consumers regarding price,

products, service and channels which results in the diversion of the customers.

2. Health care prices and utilization: The increase in the health care costs can have an impact on

product margins. This can lead to reduction in the value of products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 6

3. Change in the legislations: The change in the government policy and legislations may affect the

regulatory incentives, resulting in the decrease in the number of members.

4. Product pricing and design: The products design and prices are subject to government’s

approval. So, if there is a change in the government’s policies, it can pose a threat to the

product’s value.

5. Inappropriate claims: Inappropriate claims may arise due to frauds or errors resulting in the

entity’s outflow.

6. Capital Management and Investment Returns: The portfolio is subject to market risks which can

influence the value of the investment and income volatility.

7. Loss of Healthcare Agreements: Non-fulfillment of the health care agreements may result in

poor consumer experiences, loss of brand value and market share.

8. Loss of data: There may be loss of data, procedures and mechanisms in the organization. Also, it

may be influenced by cyber-attack (Ridha & Alnaji ,2015)

The Financial Risk comprises of the following risks:

1. Market rate risk: It comprises of the risk resulting from the variations of fair value or future

cash flows of the financial instruments, resulting from the variations in the market prices. It

has the following parts:

(a) Interest rate risk: The fluctuations in the market interest rates resulting in the variations in

the future cash flows is the risk of interest rates. The company is facing the risk of variations

in the interest rates in the cash and cash equivalents and fixed income investments. In 2016,

$1883.5 Million of the financial assets were exposed to Australian variable interest rate risks

(Medibank, 2016). In 2017, the number increased to $ 2167.1 Million (Medibank, 2017).

(b) Foreign currency risk: The risk influencing the variations in the foreign exchange rates results

in the foreign currency risk. The company’s is facing transaction currency exposures,

emerging from the purchase in foreign currencies. They comprise of dealings from

operational cost within the business and purchase of foreign currency denominated

instruments .In 2016, the financial instruments exposed to foreign currency risk amounted

to $ 91.6 Million (Medibank, 2016). In 2017, the number decreased to $ 76.4 Million

(Medibank, 2017).

(c) Price Risk: The risk resulting from the variations of the market prices of the fair value of

future cash flows of financial instruments is price risk. The entity is subjected to equity price

3. Change in the legislations: The change in the government policy and legislations may affect the

regulatory incentives, resulting in the decrease in the number of members.

4. Product pricing and design: The products design and prices are subject to government’s

approval. So, if there is a change in the government’s policies, it can pose a threat to the

product’s value.

5. Inappropriate claims: Inappropriate claims may arise due to frauds or errors resulting in the

entity’s outflow.

6. Capital Management and Investment Returns: The portfolio is subject to market risks which can

influence the value of the investment and income volatility.

7. Loss of Healthcare Agreements: Non-fulfillment of the health care agreements may result in

poor consumer experiences, loss of brand value and market share.

8. Loss of data: There may be loss of data, procedures and mechanisms in the organization. Also, it

may be influenced by cyber-attack (Ridha & Alnaji ,2015)

The Financial Risk comprises of the following risks:

1. Market rate risk: It comprises of the risk resulting from the variations of fair value or future

cash flows of the financial instruments, resulting from the variations in the market prices. It

has the following parts:

(a) Interest rate risk: The fluctuations in the market interest rates resulting in the variations in

the future cash flows is the risk of interest rates. The company is facing the risk of variations

in the interest rates in the cash and cash equivalents and fixed income investments. In 2016,

$1883.5 Million of the financial assets were exposed to Australian variable interest rate risks

(Medibank, 2016). In 2017, the number increased to $ 2167.1 Million (Medibank, 2017).

(b) Foreign currency risk: The risk influencing the variations in the foreign exchange rates results

in the foreign currency risk. The company’s is facing transaction currency exposures,

emerging from the purchase in foreign currencies. They comprise of dealings from

operational cost within the business and purchase of foreign currency denominated

instruments .In 2016, the financial instruments exposed to foreign currency risk amounted

to $ 91.6 Million (Medibank, 2016). In 2017, the number decreased to $ 76.4 Million

(Medibank, 2017).

(c) Price Risk: The risk resulting from the variations of the market prices of the fair value of

future cash flows of financial instruments is price risk. The entity is subjected to equity price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 7

risk comprising of investments in the infrastructure, property and Australian and

international equities (Otieno & Nyangechi , 2013).

2. Credit risk: The risk arising from the possible defaults of counterparty is termed as credit

risk. The company is facing the credit risk to the amounts equal to its financial assets

consisting of cash and cash equivalents and the financial assets at a fair value.

3. Liquidity Risk: The risk faced by the company where it confronts the problems in arranging

funds to fulfill its commitments associated with financial instruments. It may result from

incapability to sell the financial assets at their fair value, failure of the counter party to repay

its contractual liabilities or the company is unable to arrange the funds or an unexpected

insurance liability due for payment (Deloitte, 2017).

In the overall liquidity risk, the financial assets consist of property, plant and machinery and

investments in working capital (OECD, 2014).

3. Identification of Account Balances Subjected to Risk of Material Misstatement

Specific account balance

(i) (ii) (iii)

Name of the

account balance

Liquidity Risk Credit Risk Price Risk

(a) Explain why

the account

balance is at

significant risk of

material

misstatement.

The firm is facing the

risk of raising funds to

fulfil the obligations

concerned with

financial instruments.

So, it may manipulate

the accounts

receivables by

liquidating them and

thereby increasing the

amounts of cash and

cash equivalents (PWC,

The firm is facing the risk

of possible defaults by

counterparty, thus it is

subjected to the risk of

material misstatements.

The firm does not have

any financial mechanisms

to lessen the credit

risk .Also all the

instruments are

unsecured. The

management can alter

The firm is facing the risk

of fluctuations in the fair

value of the financial

instruments .It occurs due

to variations in the

market prices. As the firm

is subjected to price risk

in the fixed income

investments due to

changes in its credit

spreads. The

management can falsify

risk comprising of investments in the infrastructure, property and Australian and

international equities (Otieno & Nyangechi , 2013).

2. Credit risk: The risk arising from the possible defaults of counterparty is termed as credit

risk. The company is facing the credit risk to the amounts equal to its financial assets

consisting of cash and cash equivalents and the financial assets at a fair value.

3. Liquidity Risk: The risk faced by the company where it confronts the problems in arranging

funds to fulfill its commitments associated with financial instruments. It may result from

incapability to sell the financial assets at their fair value, failure of the counter party to repay

its contractual liabilities or the company is unable to arrange the funds or an unexpected

insurance liability due for payment (Deloitte, 2017).

In the overall liquidity risk, the financial assets consist of property, plant and machinery and

investments in working capital (OECD, 2014).

3. Identification of Account Balances Subjected to Risk of Material Misstatement

Specific account balance

(i) (ii) (iii)

Name of the

account balance

Liquidity Risk Credit Risk Price Risk

(a) Explain why

the account

balance is at

significant risk of

material

misstatement.

The firm is facing the

risk of raising funds to

fulfil the obligations

concerned with

financial instruments.

So, it may manipulate

the accounts

receivables by

liquidating them and

thereby increasing the

amounts of cash and

cash equivalents (PWC,

The firm is facing the risk

of possible defaults by

counterparty, thus it is

subjected to the risk of

material misstatements.

The firm does not have

any financial mechanisms

to lessen the credit

risk .Also all the

instruments are

unsecured. The

management can alter

The firm is facing the risk

of fluctuations in the fair

value of the financial

instruments .It occurs due

to variations in the

market prices. As the firm

is subjected to price risk

in the fixed income

investments due to

changes in its credit

spreads. The

management can falsify

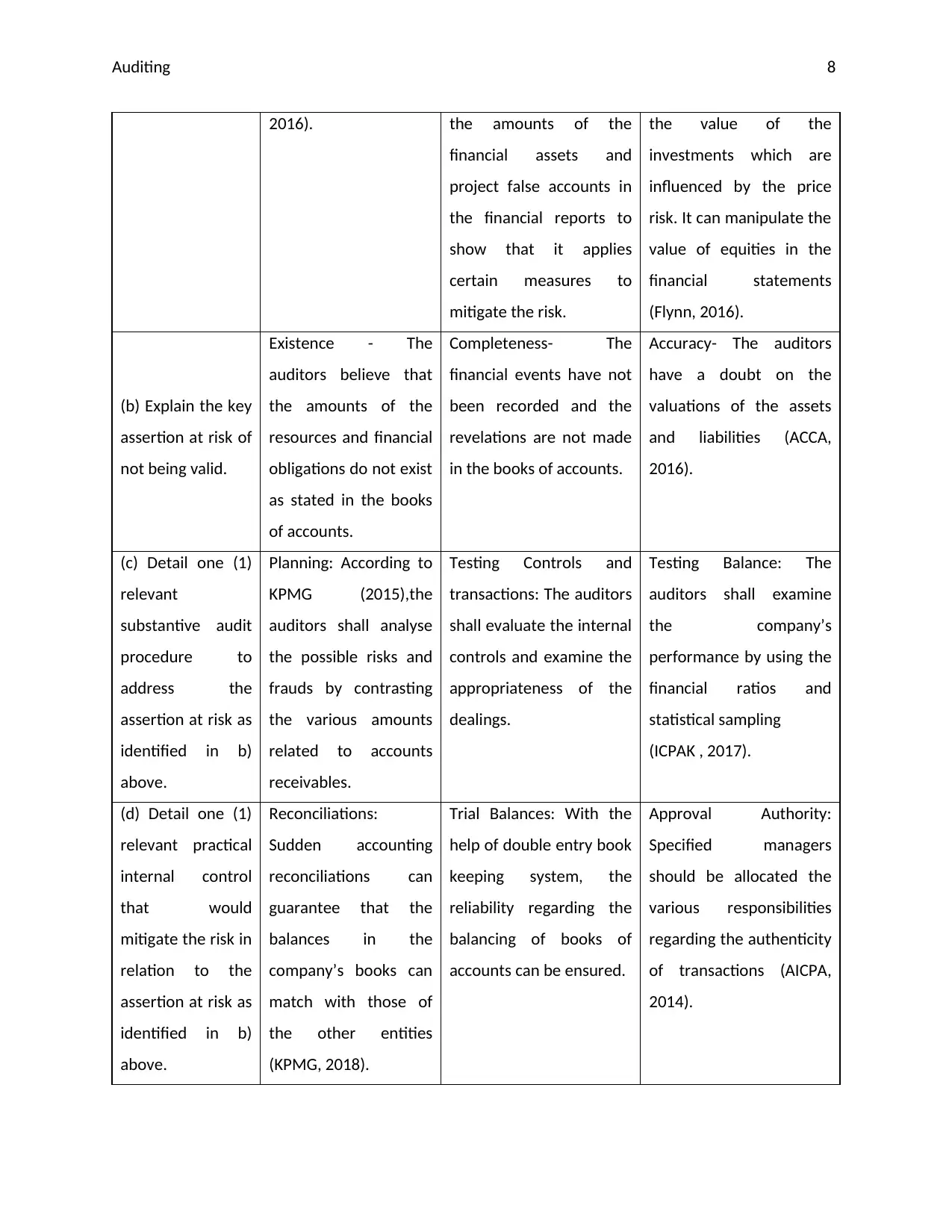

Auditing 8

2016). the amounts of the

financial assets and

project false accounts in

the financial reports to

show that it applies

certain measures to

mitigate the risk.

the value of the

investments which are

influenced by the price

risk. It can manipulate the

value of equities in the

financial statements

(Flynn, 2016).

(b) Explain the key

assertion at risk of

not being valid.

Existence - The

auditors believe that

the amounts of the

resources and financial

obligations do not exist

as stated in the books

of accounts.

Completeness- The

financial events have not

been recorded and the

revelations are not made

in the books of accounts.

Accuracy- The auditors

have a doubt on the

valuations of the assets

and liabilities (ACCA,

2016).

(c) Detail one (1)

relevant

substantive audit

procedure to

address the

assertion at risk as

identified in b)

above.

Planning: According to

KPMG (2015),the

auditors shall analyse

the possible risks and

frauds by contrasting

the various amounts

related to accounts

receivables.

Testing Controls and

transactions: The auditors

shall evaluate the internal

controls and examine the

appropriateness of the

dealings.

Testing Balance: The

auditors shall examine

the company’s

performance by using the

financial ratios and

statistical sampling

(ICPAK , 2017).

(d) Detail one (1)

relevant practical

internal control

that would

mitigate the risk in

relation to the

assertion at risk as

identified in b)

above.

Reconciliations:

Sudden accounting

reconciliations can

guarantee that the

balances in the

company’s books can

match with those of

the other entities

(KPMG, 2018).

Trial Balances: With the

help of double entry book

keeping system, the

reliability regarding the

balancing of books of

accounts can be ensured.

Approval Authority:

Specified managers

should be allocated the

various responsibilities

regarding the authenticity

of transactions (AICPA,

2014).

2016). the amounts of the

financial assets and

project false accounts in

the financial reports to

show that it applies

certain measures to

mitigate the risk.

the value of the

investments which are

influenced by the price

risk. It can manipulate the

value of equities in the

financial statements

(Flynn, 2016).

(b) Explain the key

assertion at risk of

not being valid.

Existence - The

auditors believe that

the amounts of the

resources and financial

obligations do not exist

as stated in the books

of accounts.

Completeness- The

financial events have not

been recorded and the

revelations are not made

in the books of accounts.

Accuracy- The auditors

have a doubt on the

valuations of the assets

and liabilities (ACCA,

2016).

(c) Detail one (1)

relevant

substantive audit

procedure to

address the

assertion at risk as

identified in b)

above.

Planning: According to

KPMG (2015),the

auditors shall analyse

the possible risks and

frauds by contrasting

the various amounts

related to accounts

receivables.

Testing Controls and

transactions: The auditors

shall evaluate the internal

controls and examine the

appropriateness of the

dealings.

Testing Balance: The

auditors shall examine

the company’s

performance by using the

financial ratios and

statistical sampling

(ICPAK , 2017).

(d) Detail one (1)

relevant practical

internal control

that would

mitigate the risk in

relation to the

assertion at risk as

identified in b)

above.

Reconciliations:

Sudden accounting

reconciliations can

guarantee that the

balances in the

company’s books can

match with those of

the other entities

(KPMG, 2018).

Trial Balances: With the

help of double entry book

keeping system, the

reliability regarding the

balancing of books of

accounts can be ensured.

Approval Authority:

Specified managers

should be allocated the

various responsibilities

regarding the authenticity

of transactions (AICPA,

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

10

Conclusion

To, conclude, the auditors PricewaterhouseCoopers have conducted an analysis of the financial

statements of Medibank Private Limited regarding the assessment of its environment and business risks.

It has evaluated its various account balances and stated the results pertaining to its study. They have

identified the various risks of substantial mismanagement which can be minimized with the help of key

audit procedures (PWC, 2017).

The auditors have reviewed various audit policies and procedures complied by the firm with respect to

the rules and regulations of the APRA and other legislations as mentioned in the above paragraphs. Also

the firm follows the ‘Corporate Governance Principles’ and has formed various committees for better

administration and accomplishment of its strategies and objectives.

Also, the environment in which the organization operates is full of vulnerabilities and market

fluctuations. So, the auditors have observed all the accounting policies of the organization and with the

help of various audit procedures and assertions; they tried to regulate the risks of material

misstatements.

10

Conclusion

To, conclude, the auditors PricewaterhouseCoopers have conducted an analysis of the financial

statements of Medibank Private Limited regarding the assessment of its environment and business risks.

It has evaluated its various account balances and stated the results pertaining to its study. They have

identified the various risks of substantial mismanagement which can be minimized with the help of key

audit procedures (PWC, 2017).

The auditors have reviewed various audit policies and procedures complied by the firm with respect to

the rules and regulations of the APRA and other legislations as mentioned in the above paragraphs. Also

the firm follows the ‘Corporate Governance Principles’ and has formed various committees for better

administration and accomplishment of its strategies and objectives.

Also, the environment in which the organization operates is full of vulnerabilities and market

fluctuations. So, the auditors have observed all the accounting policies of the organization and with the

help of various audit procedures and assertions; they tried to regulate the risks of material

misstatements.

Auditing

11

References

ACCA(2016). The Audit of Financial Statement Assertions. Retrieved from

http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-

study-resources/f8/technical-articles/assertions.html#

AICPA(2014). The Importance of Internal Control in Financial Reporting and Safeguarding Plan Assets.

Retrieved from

https://www.aicpa.org/content/dam/aicpa/interestareas/employeebenefitplanauditquality/

resources/planadvisories/downloadabledocuments/plan-advisoryinternalcontrol-hires.pdf

APRA(2018). About APRA. Retrieved from http://www.apra.gov.au/AboutAPRA/Pages/Default.

Auditing and Assurance Standards Board (2013). Auditing Standard ASA 315 Identifying and Assessing

the Risks of Material Misstatement through Understanding the Entity and Its Environment.

Retrieved from

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA

_315.pdf

Deloitte(2017). 2017 Insurance Regulatory Trends. The Wall Street Journal. Retrieved from

http://deloitte.wsj.com/riskandcompliance/2017/03/21/2017-insurance-regulatory-trends/

Flynn, K.(2016). Financial fraud in the private health insurance sector in Australia: perspectives from the

industry. Journal of Financial Crime. 23(1).143-158.

ICPAK (2017).Conducting Risk Assessment & Auditing the Internal Control System. Retrieved from

https://www.icpak.com/wp-content/uploads/2017/03/RISK-ASSESSMENT-AUDITING-ICS1.pdf

Kokobe, S.A.& Gemechu, D.(2016). Risk Management Techniques and Financial Performance of

Insurance Companies. International Journal of Accounting Research.4(1).

KPMG(2015). Audit quality . Retrieved from

https://assets.kpmg.com/content/dam/kpmg/pdf/2016/03/audit-quality-report-2015.pdf

11

References

ACCA(2016). The Audit of Financial Statement Assertions. Retrieved from

http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-

study-resources/f8/technical-articles/assertions.html#

AICPA(2014). The Importance of Internal Control in Financial Reporting and Safeguarding Plan Assets.

Retrieved from

https://www.aicpa.org/content/dam/aicpa/interestareas/employeebenefitplanauditquality/

resources/planadvisories/downloadabledocuments/plan-advisoryinternalcontrol-hires.pdf

APRA(2018). About APRA. Retrieved from http://www.apra.gov.au/AboutAPRA/Pages/Default.

Auditing and Assurance Standards Board (2013). Auditing Standard ASA 315 Identifying and Assessing

the Risks of Material Misstatement through Understanding the Entity and Its Environment.

Retrieved from

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA

_315.pdf

Deloitte(2017). 2017 Insurance Regulatory Trends. The Wall Street Journal. Retrieved from

http://deloitte.wsj.com/riskandcompliance/2017/03/21/2017-insurance-regulatory-trends/

Flynn, K.(2016). Financial fraud in the private health insurance sector in Australia: perspectives from the

industry. Journal of Financial Crime. 23(1).143-158.

ICPAK (2017).Conducting Risk Assessment & Auditing the Internal Control System. Retrieved from

https://www.icpak.com/wp-content/uploads/2017/03/RISK-ASSESSMENT-AUDITING-ICS1.pdf

Kokobe, S.A.& Gemechu, D.(2016). Risk Management Techniques and Financial Performance of

Insurance Companies. International Journal of Accounting Research.4(1).

KPMG(2015). Audit quality . Retrieved from

https://assets.kpmg.com/content/dam/kpmg/pdf/2016/03/audit-quality-report-2015.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.