Auditing Case Study: Legal and Ethical Issues for OEV and Framed Ltd.

VerifiedAdded on 2022/08/26

|10

|2144

|13

Report

AI Summary

This report analyzes an auditing case involving OEV, an accounting firm, and Framed Ltd., a client company that experienced financial fraud. The case explores the tort of negligence by the auditor, specifically highlighting the failure to detect fraudulent activities committed by Framed Ltd.'s sales representatives. The report discusses the auditor's responsibilities, the concept of 'due professional care,' and the actions that can be taken against OEV for its negligence. The case also delves into an ethical dilemma faced by an OEV senior auditor, applying the American Accounting Association's decision-making process to evaluate alternative courses of action. The report concludes by emphasizing the importance of ethical decision-making in auditing and the potential consequences of failing to uphold professional standards, affecting stakeholders like the liquidator and a bank that relied on the audited financial reports. The report also discusses the ethical issues involved and the consequences of different actions.

Running Head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Question 1..................................................................................................................................2

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Tort of Negligence.................................................................................................................2

Action against OEV...............................................................................................................3

Reduction of Liability............................................................................................................3

Success in Action against OEV..............................................................................................4

Conclusion..................................................................................................................................4

Question 2..................................................................................................................................5

Reference....................................................................................................................................8

Table of Contents

Question 1..................................................................................................................................2

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Tort of Negligence.................................................................................................................2

Action against OEV...............................................................................................................3

Reduction of Liability............................................................................................................3

Success in Action against OEV..............................................................................................4

Conclusion..................................................................................................................................4

Question 2..................................................................................................................................5

Reference....................................................................................................................................8

2AUDITING

Question 1

Introduction

Auditing is the process of examining financial records of the entity for determining

that whether they are accurate as well as according to the applicable laws, regulations and

laws. It is used for providing confidence for all the stakeholders that accounting reports of

organization are accurate. Hence, this report aims to outline all elements of tort of negligence

by auditor and the actions that can be taken against them for their negligence to detect fraud

in client company.

Discussion

Tort of Negligence

Framed was wholesaler of the supplies of office, who was engaged in selling all its

products to retailers all through out of NSW. The company was not able to earn profit rather

it was at break-even situation for last two years. The key issue was of the management of

cash flow and the other issue includes reasonable revenue and creeping up of the accounts

payable and receivables. The most recent audit was completed by the auditing firm, OEV and

they provided unmodified set of opinion. Within couple of the months of end of year, framed

limited went into the liquidation and they become incapable for paying their outstanding

debts. Framed liquidator then found major fraud and manipulation committed by Framed

sales representatives. These representatives were involved in entering the falsified sales for

achieving bonuses that they get from sales. The material statement was done on sales and

receivables. Therefore, all these manipulations and fraud was neglected by auditors and

negligence has been tort by them in detecting fraud, which was going on in the Framed Ltd

(Handoko & Widuri, 2016).

Question 1

Introduction

Auditing is the process of examining financial records of the entity for determining

that whether they are accurate as well as according to the applicable laws, regulations and

laws. It is used for providing confidence for all the stakeholders that accounting reports of

organization are accurate. Hence, this report aims to outline all elements of tort of negligence

by auditor and the actions that can be taken against them for their negligence to detect fraud

in client company.

Discussion

Tort of Negligence

Framed was wholesaler of the supplies of office, who was engaged in selling all its

products to retailers all through out of NSW. The company was not able to earn profit rather

it was at break-even situation for last two years. The key issue was of the management of

cash flow and the other issue includes reasonable revenue and creeping up of the accounts

payable and receivables. The most recent audit was completed by the auditing firm, OEV and

they provided unmodified set of opinion. Within couple of the months of end of year, framed

limited went into the liquidation and they become incapable for paying their outstanding

debts. Framed liquidator then found major fraud and manipulation committed by Framed

sales representatives. These representatives were involved in entering the falsified sales for

achieving bonuses that they get from sales. The material statement was done on sales and

receivables. Therefore, all these manipulations and fraud was neglected by auditors and

negligence has been tort by them in detecting fraud, which was going on in the Framed Ltd

(Handoko & Widuri, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

The standard of auditing that fits in case of Framed Limited is “due professional

care”. The exercise of “due professional care” is done in planning, performance as well as

preparation of the audit. It involves the independent auditor for the planning and then

performing their work with the “due professional care”. Moreover, this imposes

responsibility upon each professional in the entity of the independent auditor for observance

of standards of reporting and the field work (Pcaobus.org. 2020). It is assumed from the

auditors that they should successfully perform their task. Further, without any kind of fault or

error, they should undertake their task with good faith as well as integrity. The auditors hold

the responsibility for any kind of dishonesty and negligence (Quadackers, Groot & Wright,

2014).

Action against OEV

Liquidator of the Framed limited are likely to get success in the action against audit

firm, OEV. It was discovered by the liquidators of Framed ltd. that key fraud was carried out

by two sales representatives of the Framed ltd. These representatives of sales were engaged in

entering false sales for getting sales bonus. Moreover, audit division’s junior member was

involved in material misstatement of the receivables and sales. Further, liquidator acting on

Framed Limited’s behalf has claimed the audit firm OEV that they were quite negligent in the

conducting of audits as well as detection of fraud, which were committed in Framed Ltd.

Although, Framed Limited’s unethical act cannot be neglected due to manipulating sales,

however, OEV is still held responsible due to failure of auditing firm in the detection of fraud

and because of breaching of due professional care (Omidfar & Moradi, 2015).

Reduction of Liability

OEV should lessen their liability to the liquidators of Framed Ltd. The OEV auditors

cannot escape from their liability of failing in detecting manipulations. Liquidators of the

Framed ltd. has thrown out the claim of negligence, which was brought against OEV for

The standard of auditing that fits in case of Framed Limited is “due professional

care”. The exercise of “due professional care” is done in planning, performance as well as

preparation of the audit. It involves the independent auditor for the planning and then

performing their work with the “due professional care”. Moreover, this imposes

responsibility upon each professional in the entity of the independent auditor for observance

of standards of reporting and the field work (Pcaobus.org. 2020). It is assumed from the

auditors that they should successfully perform their task. Further, without any kind of fault or

error, they should undertake their task with good faith as well as integrity. The auditors hold

the responsibility for any kind of dishonesty and negligence (Quadackers, Groot & Wright,

2014).

Action against OEV

Liquidator of the Framed limited are likely to get success in the action against audit

firm, OEV. It was discovered by the liquidators of Framed ltd. that key fraud was carried out

by two sales representatives of the Framed ltd. These representatives of sales were engaged in

entering false sales for getting sales bonus. Moreover, audit division’s junior member was

involved in material misstatement of the receivables and sales. Further, liquidator acting on

Framed Limited’s behalf has claimed the audit firm OEV that they were quite negligent in the

conducting of audits as well as detection of fraud, which were committed in Framed Ltd.

Although, Framed Limited’s unethical act cannot be neglected due to manipulating sales,

however, OEV is still held responsible due to failure of auditing firm in the detection of fraud

and because of breaching of due professional care (Omidfar & Moradi, 2015).

Reduction of Liability

OEV should lessen their liability to the liquidators of Framed Ltd. The OEV auditors

cannot escape from their liability of failing in detecting manipulations. Liquidators of the

Framed ltd. has thrown out the claim of negligence, which was brought against OEV for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

failing in detecting serious manipulation and fraud at the Framed Ltd. Further, liquidator

argued that company’s auditors are responsible and liable for detecting fraud because they are

being hired for fulfilling their responsibilities against the company. The company’s auditors

need to be aware of things going on the financial statements of the client’s company. It’s

auditor duty to keep check on changes occurring in the financial reports and they should take

initiative to bring this to the notice of company’s management (Ray, 2015).

Success in Action against OEV

VicBank is expected to get success against the OEV. It has extended the terms of

overdraft to the Framed Ltd. VicBank trusted on the audited financial reports of the Framed

Ltd. that was provided by the auditing firm. This has resulted into claiming of VicBank to

OEV for damages done because of negligence of their duty. Although, it is quite difficult to

succeed against the claim regarding the auditor’s negligence to detect fraud, but it is clear in

this case that OEV has failed in discovering the overstatement. Therefore, VicBank can

succeed against OEV and it can be sued due to their failure and negligence for spotting fraud

against the Fraud Limited (Endaya, 2014).

Conclusion

Therefore, this report concludes that the sales representatives of Framed Ltd. has

committed fraud in the sales and receivables for getting bonus. In this concern, the biggest

failure and tort of negligence of the auditing firm OEV was failure of their due professional

care. Hence, their failure as audit professional may leads towards taking adverse action

against them by liquidators and VicBank.

failing in detecting serious manipulation and fraud at the Framed Ltd. Further, liquidator

argued that company’s auditors are responsible and liable for detecting fraud because they are

being hired for fulfilling their responsibilities against the company. The company’s auditors

need to be aware of things going on the financial statements of the client’s company. It’s

auditor duty to keep check on changes occurring in the financial reports and they should take

initiative to bring this to the notice of company’s management (Ray, 2015).

Success in Action against OEV

VicBank is expected to get success against the OEV. It has extended the terms of

overdraft to the Framed Ltd. VicBank trusted on the audited financial reports of the Framed

Ltd. that was provided by the auditing firm. This has resulted into claiming of VicBank to

OEV for damages done because of negligence of their duty. Although, it is quite difficult to

succeed against the claim regarding the auditor’s negligence to detect fraud, but it is clear in

this case that OEV has failed in discovering the overstatement. Therefore, VicBank can

succeed against OEV and it can be sued due to their failure and negligence for spotting fraud

against the Fraud Limited (Endaya, 2014).

Conclusion

Therefore, this report concludes that the sales representatives of Framed Ltd. has

committed fraud in the sales and receivables for getting bonus. In this concern, the biggest

failure and tort of negligence of the auditing firm OEV was failure of their due professional

care. Hence, their failure as audit professional may leads towards taking adverse action

against them by liquidators and VicBank.

5AUDITING

Question 2

American

Accounting

Association Model

Decision-making process

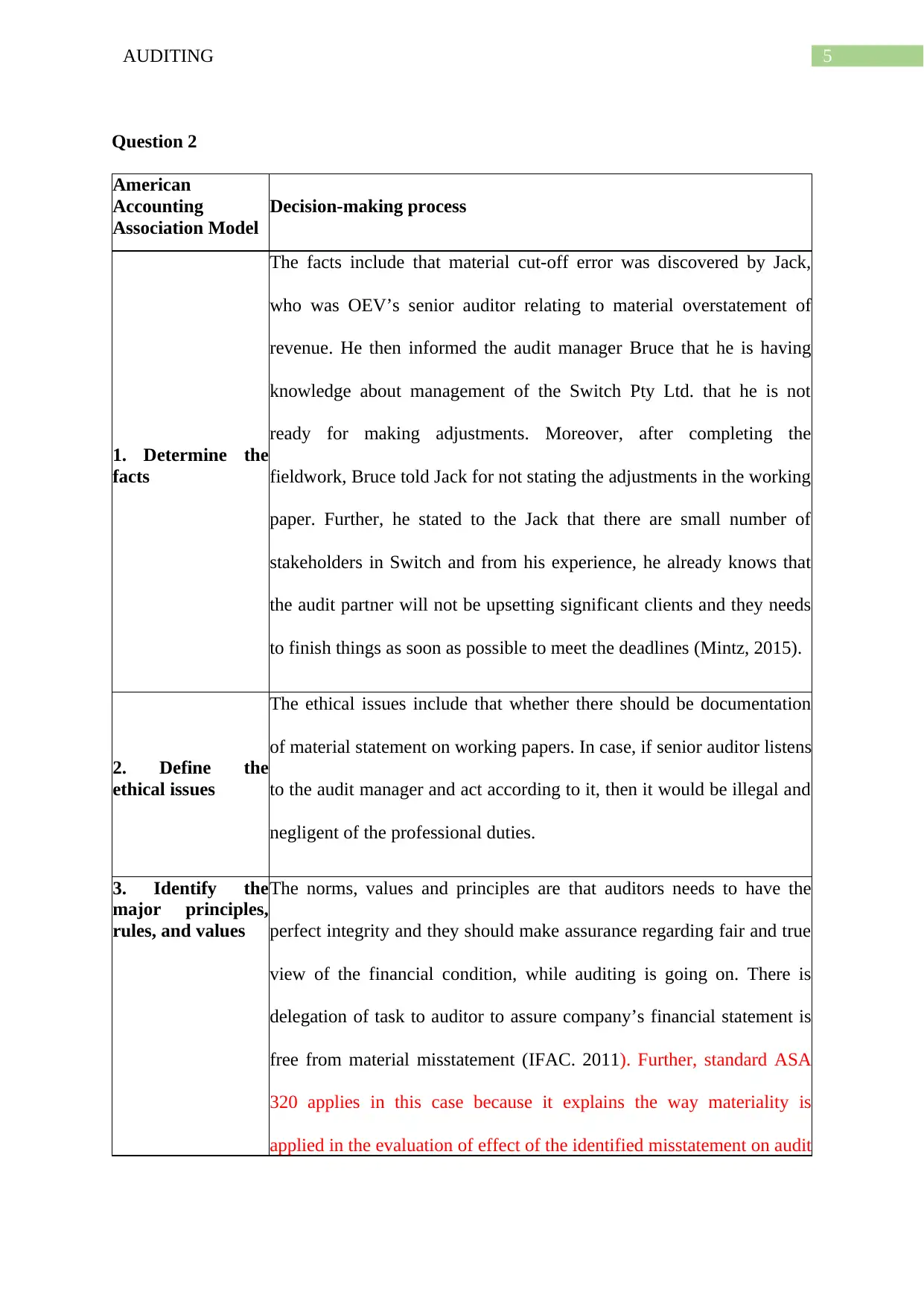

1. Determine the

facts

The facts include that material cut-off error was discovered by Jack,

who was OEV’s senior auditor relating to material overstatement of

revenue. He then informed the audit manager Bruce that he is having

knowledge about management of the Switch Pty Ltd. that he is not

ready for making adjustments. Moreover, after completing the

fieldwork, Bruce told Jack for not stating the adjustments in the working

paper. Further, he stated to the Jack that there are small number of

stakeholders in Switch and from his experience, he already knows that

the audit partner will not be upsetting significant clients and they needs

to finish things as soon as possible to meet the deadlines (Mintz, 2015).

2. Define the

ethical issues

The ethical issues include that whether there should be documentation

of material statement on working papers. In case, if senior auditor listens

to the audit manager and act according to it, then it would be illegal and

negligent of the professional duties.

3. Identify the

major principles,

rules, and values

The norms, values and principles are that auditors needs to have the

perfect integrity and they should make assurance regarding fair and true

view of the financial condition, while auditing is going on. There is

delegation of task to auditor to assure company’s financial statement is

free from material misstatement (IFAC. 2011). Further, standard ASA

320 applies in this case because it explains the way materiality is

applied in the evaluation of effect of the identified misstatement on audit

Question 2

American

Accounting

Association Model

Decision-making process

1. Determine the

facts

The facts include that material cut-off error was discovered by Jack,

who was OEV’s senior auditor relating to material overstatement of

revenue. He then informed the audit manager Bruce that he is having

knowledge about management of the Switch Pty Ltd. that he is not

ready for making adjustments. Moreover, after completing the

fieldwork, Bruce told Jack for not stating the adjustments in the working

paper. Further, he stated to the Jack that there are small number of

stakeholders in Switch and from his experience, he already knows that

the audit partner will not be upsetting significant clients and they needs

to finish things as soon as possible to meet the deadlines (Mintz, 2015).

2. Define the

ethical issues

The ethical issues include that whether there should be documentation

of material statement on working papers. In case, if senior auditor listens

to the audit manager and act according to it, then it would be illegal and

negligent of the professional duties.

3. Identify the

major principles,

rules, and values

The norms, values and principles are that auditors needs to have the

perfect integrity and they should make assurance regarding fair and true

view of the financial condition, while auditing is going on. There is

delegation of task to auditor to assure company’s financial statement is

free from material misstatement (IFAC. 2011). Further, standard ASA

320 applies in this case because it explains the way materiality is

applied in the evaluation of effect of the identified misstatement on audit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

American

Accounting

Association Model

Decision-making process

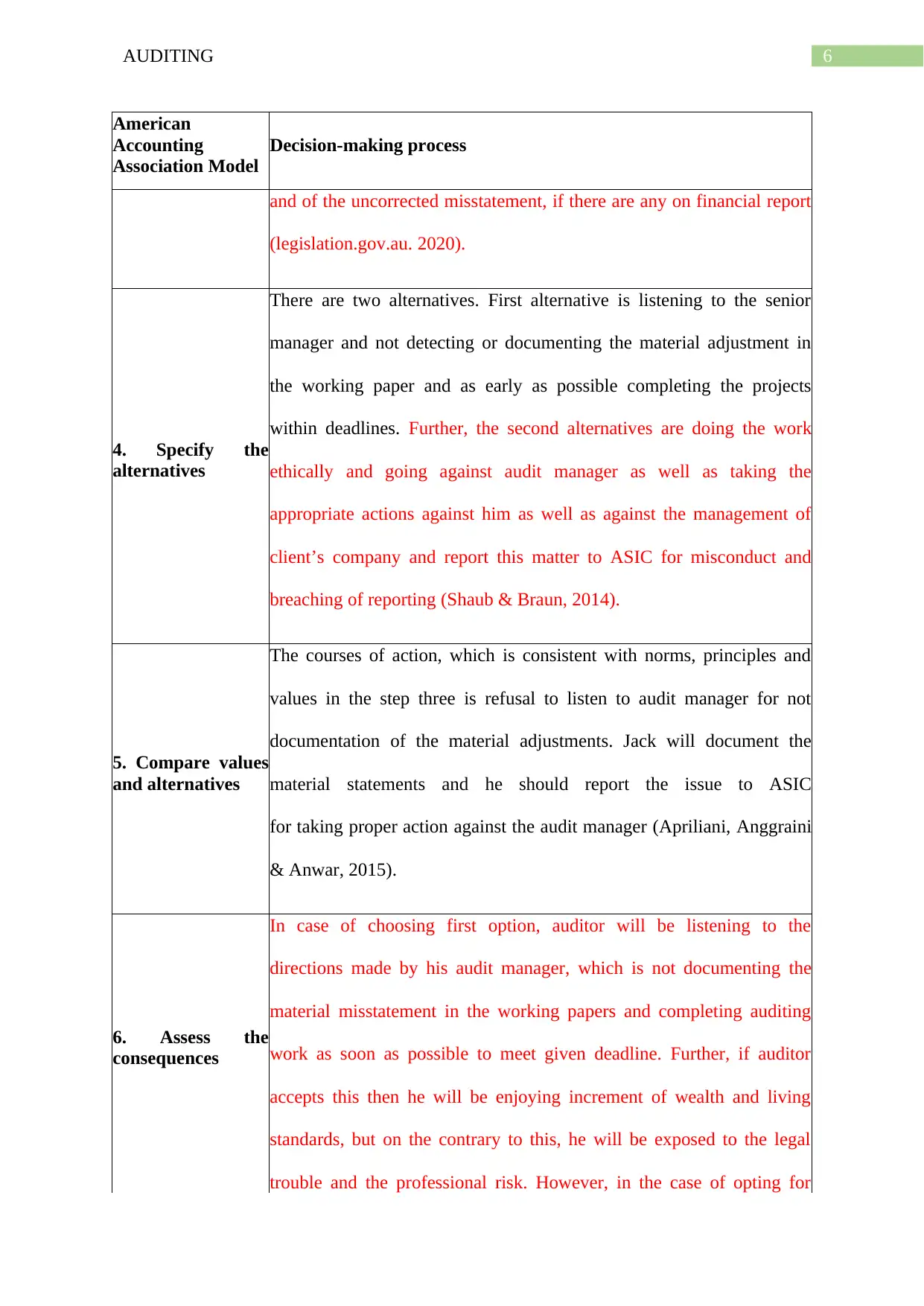

and of the uncorrected misstatement, if there are any on financial report

(legislation.gov.au. 2020).

4. Specify the

alternatives

There are two alternatives. First alternative is listening to the senior

manager and not detecting or documenting the material adjustment in

the working paper and as early as possible completing the projects

within deadlines. Further, the second alternatives are doing the work

ethically and going against audit manager as well as taking the

appropriate actions against him as well as against the management of

client’s company and report this matter to ASIC for misconduct and

breaching of reporting (Shaub & Braun, 2014).

5. Compare values

and alternatives

The courses of action, which is consistent with norms, principles and

values in the step three is refusal to listen to audit manager for not

documentation of the material adjustments. Jack will document the

material statements and he should report the issue to ASIC

for taking proper action against the audit manager (Apriliani, Anggraini

& Anwar, 2015).

6. Assess the

consequences

In case of choosing first option, auditor will be listening to the

directions made by his audit manager, which is not documenting the

material misstatement in the working papers and completing auditing

work as soon as possible to meet given deadline. Further, if auditor

accepts this then he will be enjoying increment of wealth and living

standards, but on the contrary to this, he will be exposed to the legal

trouble and the professional risk. However, in the case of opting for

American

Accounting

Association Model

Decision-making process

and of the uncorrected misstatement, if there are any on financial report

(legislation.gov.au. 2020).

4. Specify the

alternatives

There are two alternatives. First alternative is listening to the senior

manager and not detecting or documenting the material adjustment in

the working paper and as early as possible completing the projects

within deadlines. Further, the second alternatives are doing the work

ethically and going against audit manager as well as taking the

appropriate actions against him as well as against the management of

client’s company and report this matter to ASIC for misconduct and

breaching of reporting (Shaub & Braun, 2014).

5. Compare values

and alternatives

The courses of action, which is consistent with norms, principles and

values in the step three is refusal to listen to audit manager for not

documentation of the material adjustments. Jack will document the

material statements and he should report the issue to ASIC

for taking proper action against the audit manager (Apriliani, Anggraini

& Anwar, 2015).

6. Assess the

consequences

In case of choosing first option, auditor will be listening to the

directions made by his audit manager, which is not documenting the

material misstatement in the working papers and completing auditing

work as soon as possible to meet given deadline. Further, if auditor

accepts this then he will be enjoying increment of wealth and living

standards, but on the contrary to this, he will be exposed to the legal

trouble and the professional risk. However, in the case of opting for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

American

Accounting

Association Model

Decision-making process

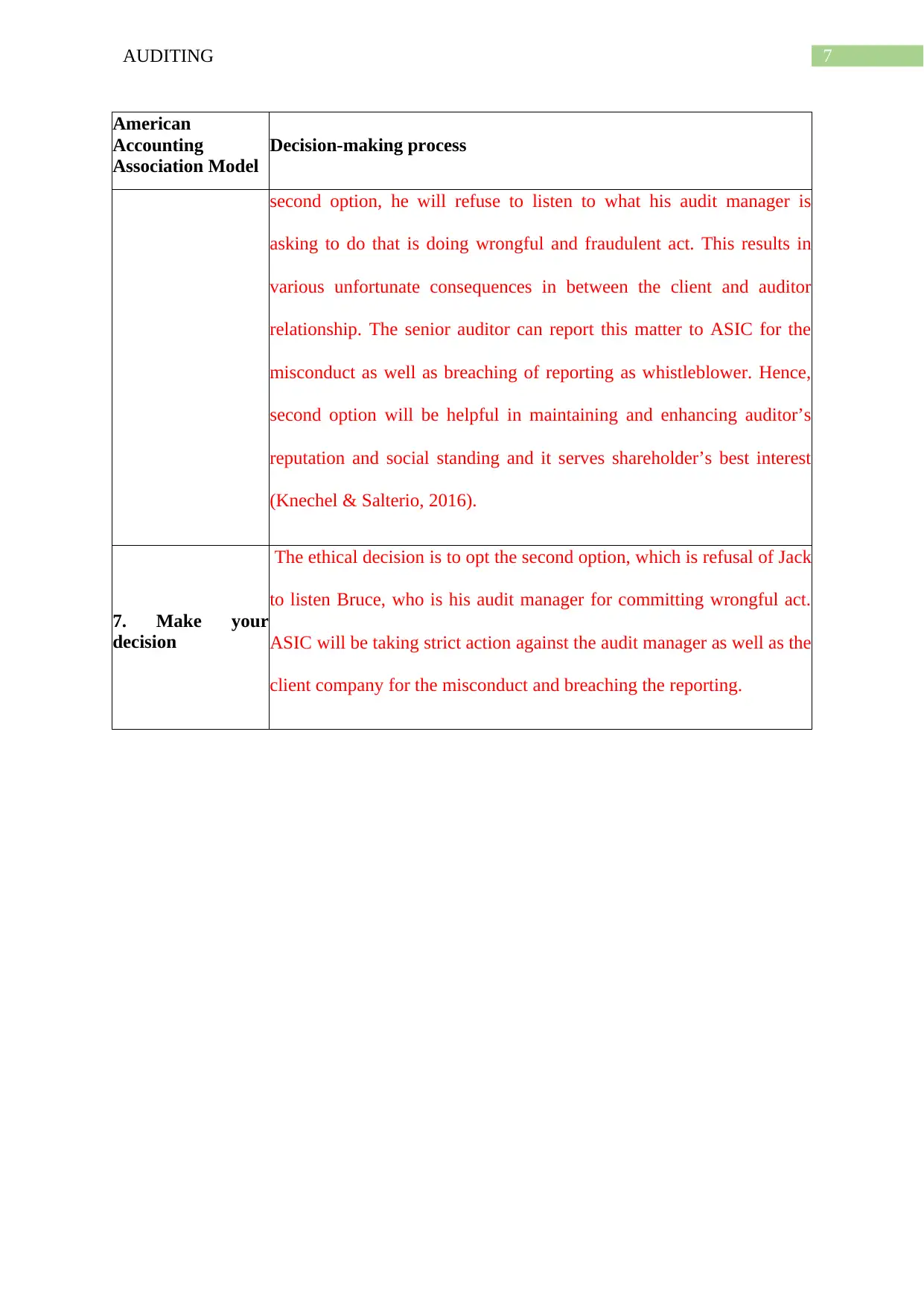

second option, he will refuse to listen to what his audit manager is

asking to do that is doing wrongful and fraudulent act. This results in

various unfortunate consequences in between the client and auditor

relationship. The senior auditor can report this matter to ASIC for the

misconduct as well as breaching of reporting as whistleblower. Hence,

second option will be helpful in maintaining and enhancing auditor’s

reputation and social standing and it serves shareholder’s best interest

(Knechel & Salterio, 2016).

7. Make your

decision

The ethical decision is to opt the second option, which is refusal of Jack

to listen Bruce, who is his audit manager for committing wrongful act.

ASIC will be taking strict action against the audit manager as well as the

client company for the misconduct and breaching the reporting.

American

Accounting

Association Model

Decision-making process

second option, he will refuse to listen to what his audit manager is

asking to do that is doing wrongful and fraudulent act. This results in

various unfortunate consequences in between the client and auditor

relationship. The senior auditor can report this matter to ASIC for the

misconduct as well as breaching of reporting as whistleblower. Hence,

second option will be helpful in maintaining and enhancing auditor’s

reputation and social standing and it serves shareholder’s best interest

(Knechel & Salterio, 2016).

7. Make your

decision

The ethical decision is to opt the second option, which is refusal of Jack

to listen Bruce, who is his audit manager for committing wrongful act.

ASIC will be taking strict action against the audit manager as well as the

client company for the misconduct and breaching the reporting.

8AUDITING

Reference

Apriliani, D., Anggraini, R. Z., & Anwar, C. (2015). The effect of organization ethical culture

and ethical climate on ethical decision making of auditor with self efficacy as

moderating. Review of Integrative Business and Economics Research, 4(1), 226.

Endaya, K. A. (2014). Coordination and cooperation between internal and external

auditors. Research Journal of Finance and Accounting, 5(9), 76-80.

IFAC. (2011). Revised Code of Ethics - Completed. Retrieved 11 March 2020, from

https://www.ethicsboard.org/projects/revised-code-ethics-completed

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Mintz, S. (2015). Whistleblowing considerations for external auditors under Dodd-Frank: A

blueprint for future research. In Research on professional responsibility and ethics in

accounting. Emerald Group Publishing Limited.

Omidfar, M., & Moradi, M., (2015). The effects of industry specialization on auditor's

opinion in Iran. Mediterranean Journal of Social Sciences, 6(1), pp.399-399.

Pcaobus.org. (2020). AU 230 Due Professional Care in the Performance of Work. Retrieved

11 March 2020, from

https://pcaobus.org/Standards/Archived/PreReorgStandards/Pages/AU230.aspx

Quadackers, L., Groot, T., & Wright, A. (2014). Auditors’ professional skepticism: Neutrality

versus presumptive doubt. Contemporary accounting research, 31(3), 639-657.

Ray, T., (2015). Auditors Still Challenged by Professional. The CPA Journal, 85(1), p.20.

Shaub, M. K., & Braun, R. L. (2014). Call of duty: A framework for auditors’ ethical

decisions. In Accounting for the Public Interest (pp. 3-25). Springer, Dordrecht.

Reference

Apriliani, D., Anggraini, R. Z., & Anwar, C. (2015). The effect of organization ethical culture

and ethical climate on ethical decision making of auditor with self efficacy as

moderating. Review of Integrative Business and Economics Research, 4(1), 226.

Endaya, K. A. (2014). Coordination and cooperation between internal and external

auditors. Research Journal of Finance and Accounting, 5(9), 76-80.

IFAC. (2011). Revised Code of Ethics - Completed. Retrieved 11 March 2020, from

https://www.ethicsboard.org/projects/revised-code-ethics-completed

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Mintz, S. (2015). Whistleblowing considerations for external auditors under Dodd-Frank: A

blueprint for future research. In Research on professional responsibility and ethics in

accounting. Emerald Group Publishing Limited.

Omidfar, M., & Moradi, M., (2015). The effects of industry specialization on auditor's

opinion in Iran. Mediterranean Journal of Social Sciences, 6(1), pp.399-399.

Pcaobus.org. (2020). AU 230 Due Professional Care in the Performance of Work. Retrieved

11 March 2020, from

https://pcaobus.org/Standards/Archived/PreReorgStandards/Pages/AU230.aspx

Quadackers, L., Groot, T., & Wright, A. (2014). Auditors’ professional skepticism: Neutrality

versus presumptive doubt. Contemporary accounting research, 31(3), 639-657.

Ray, T., (2015). Auditors Still Challenged by Professional. The CPA Journal, 85(1), p.20.

Shaub, M. K., & Braun, R. L. (2014). Call of duty: A framework for auditors’ ethical

decisions. In Accounting for the Public Interest (pp. 3-25). Springer, Dordrecht.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

Handoko, B. L., & Widuri, R. (2016, November). The impact of auditor communication and

due professional care on client responses to inquiries for successful audit process.

In 2016 International Conference on Information Management and Technology

(ICIMTech) (pp. 296-300). IEEE.

legislation.gov.au (2020). Retrieved 23 March 2020, from

https://www.legislation.gov.au/Details/F2006L01375/88b15cc7-1c10-4b6b-aa3a-

3a57f1778cab

Handoko, B. L., & Widuri, R. (2016, November). The impact of auditor communication and

due professional care on client responses to inquiries for successful audit process.

In 2016 International Conference on Information Management and Technology

(ICIMTech) (pp. 296-300). IEEE.

legislation.gov.au (2020). Retrieved 23 March 2020, from

https://www.legislation.gov.au/Details/F2006L01375/88b15cc7-1c10-4b6b-aa3a-

3a57f1778cab

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.