Semester 2 BAO5524 Auditing Report: Probiotec Limited Audit Analysis

VerifiedAdded on 2022/10/19

|16

|3955

|119

Report

AI Summary

This report analyzes the auditing procedures applied to Probiotec Limited, an Australian pharmaceutical company. It examines the nature of the company, its audit program, and the concept of materiality in financial statements, including planning materiality. The report identifies potential material misstatements in accounts like cash, receivables, and intangible assets, along with the associated risks. It also outlines the audit procedures used to assess these risks, considering inherent and control risks. The analysis covers substantive procedures and the auditor's approach to forming an opinion on the financial statements, offering a comprehensive overview of the audit process and its application to a specific company.

Running head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Executive Summary

The report shows the auditing procedure that is carried by the auditor upon different entity

report. It deals with a company name Probiotec which an Australian based company. It shows

the different account that can have material misstatement and also show the planning

materiality which is being calculated by the auditor in the initial stage of audit process.

Lastly, it states the risk that has been associated with different account and the procedure

which is carried upon the account and based on which auditor gives its opinion upon the

same.

AUDITING

Executive Summary

The report shows the auditing procedure that is carried by the auditor upon different entity

report. It deals with a company name Probiotec which an Australian based company. It shows

the different account that can have material misstatement and also show the planning

materiality which is being calculated by the auditor in the initial stage of audit process.

Lastly, it states the risk that has been associated with different account and the procedure

which is carried upon the account and based on which auditor gives its opinion upon the

same.

2

AUDITING

Table of Contents

Introduction................................................................................................................................3

Nature of the Company..............................................................................................................3

Audit Program............................................................................................................................4

Materiality in financial statement...............................................................................................5

Planning Materiality...................................................................................................................6

Risk Associated in Above mentioned Accounts........................................................................7

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

AUDITING

Table of Contents

Introduction................................................................................................................................3

Nature of the Company..............................................................................................................3

Audit Program............................................................................................................................4

Materiality in financial statement...............................................................................................5

Planning Materiality...................................................................................................................6

Risk Associated in Above mentioned Accounts........................................................................7

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

Introduction

An audit is the evaluation of the entity report as whether the entity has followed all

the norms that are laid in accounting standard while preparing their books of accounts (Chen

et al., 2015). This process can be carried by both external and internal ways as if the internal

employee carries the audit process than it termed as internal auditing and if the external

auditor carries the audit than it termed as statutory audit. It has to check the financial report

by carrying different procedure in the entity operation. Each organisation must have proper

internal control system as this system helps them to reduce the risk associated in their

business activities (De Simone, Ege and Stomberg 2014). As if the entity is having lack of

proper internal control in their business activity than it increase risk associated in the

business, auditor has to figure out the risk which is being associated in internal control and on

the evidence gather by the auditor it has to form a proper opinion upon the report of the

entity. The report shows the entity Probiotec Limited and states the amount of risk that is

present in entity business. It also shows the materiality in entity business and how the auditor

able to plan its audit procedure upon the planning materiality. It describes the material

misstatement that is present in a different account of the entity and how the auditor can carry

substantive procedure to know the risk of material misstatement in entity books of accounts.

Nature of the Entity

The report shows the company Probiotec Limited that is an Australian based

Pharmaceuticals organisation which carries its activities in Australia. It has many business

operations as its market, manufacture and distributes its product in the country. The company

was founded in 1997 and has it headquartered in Laverton North, VIC. It has a proper range

of health product and able to carry its business in a very cost-saving manner. Company has

proper research team, and also it has invested a considerable sum upon the advancement of its

AUDITING

Introduction

An audit is the evaluation of the entity report as whether the entity has followed all

the norms that are laid in accounting standard while preparing their books of accounts (Chen

et al., 2015). This process can be carried by both external and internal ways as if the internal

employee carries the audit process than it termed as internal auditing and if the external

auditor carries the audit than it termed as statutory audit. It has to check the financial report

by carrying different procedure in the entity operation. Each organisation must have proper

internal control system as this system helps them to reduce the risk associated in their

business activities (De Simone, Ege and Stomberg 2014). As if the entity is having lack of

proper internal control in their business activity than it increase risk associated in the

business, auditor has to figure out the risk which is being associated in internal control and on

the evidence gather by the auditor it has to form a proper opinion upon the report of the

entity. The report shows the entity Probiotec Limited and states the amount of risk that is

present in entity business. It also shows the materiality in entity business and how the auditor

able to plan its audit procedure upon the planning materiality. It describes the material

misstatement that is present in a different account of the entity and how the auditor can carry

substantive procedure to know the risk of material misstatement in entity books of accounts.

Nature of the Entity

The report shows the company Probiotec Limited that is an Australian based

Pharmaceuticals organisation which carries its activities in Australia. It has many business

operations as its market, manufacture and distributes its product in the country. The company

was founded in 1997 and has it headquartered in Laverton North, VIC. It has a proper range

of health product and able to carry its business in a very cost-saving manner. Company has

proper research team, and also it has invested a considerable sum upon the advancement of its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

technologies in their business activities (Auasb.gov.au 2019). Auditor has to apply many

auditing standards upon the company financial information to understand the business as well

as to know the amount of materiality in the entity books of accounts. It has to set the

guidelines and scope of the audit it has to comply with ASA 201 “Terms of Audit

Engagements” which shows all the norms that should be followed by the auditor while

ascertaining the scope of the audit (Auasb.gov.au 2019). ASA 250 “Consideration of Law

and Regulations in an Audit” state the law and regulation which is to be followed by the

auditor in its audit process and help it to increase the overall audit quality.

Audit Program

It is the strategy which the auditor makes upon the plan and procedure which it will

carry in the entity different activities (DeFond and Zhang 2014). These help the auditor to

know whether the entity has followed all the framework while carrying their business

activities in its respective industry. These strategies and plans are programs that are made by

auditor in the initial stage of the audit. As per ASA 300 in Para 7 it states that the auditor

should plan its strategy at the beginning of the audit, which assists the auditor to get an

overview how the things while being carried on in later stage of the business. The audit

strategy shows all the stages that will be followed by the auditor in carrying the audit process

upon the company financial information (Auasb.gov.au 2019) as it shows the process which

auditor plans to calculate the planning materiality as well the analysis of material

misstatement in different account of the entity. These also focuses upon the sampling and

other substantive methods that are used by the auditor to understand the risk of material

misstatement in the organisation (Auasb.gov.au 2019). It also states the steps that are carried

by auditor in regards of entity internal control system is working and how the organization

can manage the business risk with the risk assessment procedure in their business activities.

ASA 300 “Documentation” is also used by the auditor to know which are the vital document

AUDITING

technologies in their business activities (Auasb.gov.au 2019). Auditor has to apply many

auditing standards upon the company financial information to understand the business as well

as to know the amount of materiality in the entity books of accounts. It has to set the

guidelines and scope of the audit it has to comply with ASA 201 “Terms of Audit

Engagements” which shows all the norms that should be followed by the auditor while

ascertaining the scope of the audit (Auasb.gov.au 2019). ASA 250 “Consideration of Law

and Regulations in an Audit” state the law and regulation which is to be followed by the

auditor in its audit process and help it to increase the overall audit quality.

Audit Program

It is the strategy which the auditor makes upon the plan and procedure which it will

carry in the entity different activities (DeFond and Zhang 2014). These help the auditor to

know whether the entity has followed all the framework while carrying their business

activities in its respective industry. These strategies and plans are programs that are made by

auditor in the initial stage of the audit. As per ASA 300 in Para 7 it states that the auditor

should plan its strategy at the beginning of the audit, which assists the auditor to get an

overview how the things while being carried on in later stage of the business. The audit

strategy shows all the stages that will be followed by the auditor in carrying the audit process

upon the company financial information (Auasb.gov.au 2019) as it shows the process which

auditor plans to calculate the planning materiality as well the analysis of material

misstatement in different account of the entity. These also focuses upon the sampling and

other substantive methods that are used by the auditor to understand the risk of material

misstatement in the organisation (Auasb.gov.au 2019). It also states the steps that are carried

by auditor in regards of entity internal control system is working and how the organization

can manage the business risk with the risk assessment procedure in their business activities.

ASA 300 “Documentation” is also used by the auditor to know which are the vital document

5

AUDITING

that should be asked from the management and how the analysis of each document should do

by the auditor (DeFond and Lennox 2017). All these steps help the auditor to get an overview

of all the procedure which it should carry upon the financial report and also help to minimise

the audit risk, which is there in their activities.

Materiality in financial statement

It refers to the error or omission which happen in entity accounting books, and it

directly affects the financial information of the organisation. Financial user has an effect on

their decision making process if the entity is having materiality in their business. Auditor has

to check the management risk assessment procedure and how effective it is in its business

activities. As per the ASA 315 “Identifying and Assessing the Risks of Material Misstatement

through Understanding the Entity and Its Environment” in its para 5 states that auditor should

carry many risk assessment procedures upon the entity accounts to know whether it contains

materiality or not (Eilifsen and Messier Jr 2014). The materiality in company financial

accounts has shown below:

Cash and Cash Equivalent - The financial report of the entity for the year 2018 shows an

increase in the figure of cash, which signifies that there is specific materiality involves in the

account balance. In 2017 it was $321624, but in 2018 it is $1816089, so the difference

between the two figure is enormous due to which the auditor has ascertained that the account

is having certain misstatement and the auditor has to carry its risk assessment procedure to

know the amount of risk involved in the account.

Trade and other Receivables - The next account which is considered to have some

materiality is trade and other receivables. As it has also had a significant increase in current

due to which the auditor has consider it to having some misstatement done by the

management in the account. In 2017 it was 10822143, but in 2018 it becomes 16472056

AUDITING

that should be asked from the management and how the analysis of each document should do

by the auditor (DeFond and Lennox 2017). All these steps help the auditor to get an overview

of all the procedure which it should carry upon the financial report and also help to minimise

the audit risk, which is there in their activities.

Materiality in financial statement

It refers to the error or omission which happen in entity accounting books, and it

directly affects the financial information of the organisation. Financial user has an effect on

their decision making process if the entity is having materiality in their business. Auditor has

to check the management risk assessment procedure and how effective it is in its business

activities. As per the ASA 315 “Identifying and Assessing the Risks of Material Misstatement

through Understanding the Entity and Its Environment” in its para 5 states that auditor should

carry many risk assessment procedures upon the entity accounts to know whether it contains

materiality or not (Eilifsen and Messier Jr 2014). The materiality in company financial

accounts has shown below:

Cash and Cash Equivalent - The financial report of the entity for the year 2018 shows an

increase in the figure of cash, which signifies that there is specific materiality involves in the

account balance. In 2017 it was $321624, but in 2018 it is $1816089, so the difference

between the two figure is enormous due to which the auditor has ascertained that the account

is having certain misstatement and the auditor has to carry its risk assessment procedure to

know the amount of risk involved in the account.

Trade and other Receivables - The next account which is considered to have some

materiality is trade and other receivables. As it has also had a significant increase in current

due to which the auditor has consider it to having some misstatement done by the

management in the account. In 2017 it was 10822143, but in 2018 it becomes 16472056

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

which show a significant amount of difference so it should perform many tests of control to

know the real value of this account in the entity books of accounts

Intangible Asset – This asset shows the goodwill and brand value of the entity, increase in

the asset signifies that it able to gain more amount of popularity in their industry. As there is

an increase in the account balance, it may happen to portrait a good picture Infront of

investors and other user company has done overvaluation of the account. The auditor should

carry proper substantive procedure upon the books of account to know the real figure of the

intangible asset of the entity.

Long-term Interest-Bearing Liabilities - Auditor has also considered this account to have

certain amount of materiality as there is increase in the account which signifies that the entity

has manipulated the account to get benefit in the industry. The auditor should gather proper

audit evidence about the materiality which is involved in entity account and should state all

the matters correctly in its auditor report

Long-term Provisions – The financial report shows a rise in the level of provision in current

year which can termed as very risky for the company. If the company is increasing the

provision that denotes it having less amount of customer in the business. It should check the

reason for increase in company provisions as well whether the amount has been increased as

per the proper accounting standard or not.

Planning Materiality

Auditor has to carry many procedures in an entity book of account to ascertain

whether it has followed all the norms which preparing their financial reports. Materiality is

one of the most critical factors which the auditor has to ascertain in its audit process

(Furnham and Gunter 2015). The omission of transaction that is made by an individual and

judgement taken by them is termed as materiality. As if the entity financial books have

AUDITING

which show a significant amount of difference so it should perform many tests of control to

know the real value of this account in the entity books of accounts

Intangible Asset – This asset shows the goodwill and brand value of the entity, increase in

the asset signifies that it able to gain more amount of popularity in their industry. As there is

an increase in the account balance, it may happen to portrait a good picture Infront of

investors and other user company has done overvaluation of the account. The auditor should

carry proper substantive procedure upon the books of account to know the real figure of the

intangible asset of the entity.

Long-term Interest-Bearing Liabilities - Auditor has also considered this account to have

certain amount of materiality as there is increase in the account which signifies that the entity

has manipulated the account to get benefit in the industry. The auditor should gather proper

audit evidence about the materiality which is involved in entity account and should state all

the matters correctly in its auditor report

Long-term Provisions – The financial report shows a rise in the level of provision in current

year which can termed as very risky for the company. If the company is increasing the

provision that denotes it having less amount of customer in the business. It should check the

reason for increase in company provisions as well whether the amount has been increased as

per the proper accounting standard or not.

Planning Materiality

Auditor has to carry many procedures in an entity book of account to ascertain

whether it has followed all the norms which preparing their financial reports. Materiality is

one of the most critical factors which the auditor has to ascertain in its audit process

(Furnham and Gunter 2015). The omission of transaction that is made by an individual and

judgement taken by them is termed as materiality. As if the entity financial books have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

materiality that signifies that the entity books not made as per different accounting

frameworks and guidelines.

Auditor plans the amount of materiality at the starting stage of audit process as this

helps it to know the audit process which is being carried upon the entity accounting books

(Griffiths 2016). Planning materiality assists the auditor to understand the materiality involve

in their business activities, and with the help of which the auditor plans the amount of audit

procedure it requires to perform upon the entity activities. These also assist the auditor in

having an idea about the timing and scope of audit that is to be performed by the auditor upon

the entity operations (Groomer and Murthy 2018). The auditor can know where it has to give

more emphasis and how easily it able to gather more audit evidence in regards to fraud and

other error done by the company in that accounting year.

The ascertain which the auditor make at the begging of its audit process is solely

based upon the planning materiality (Hall 2015). The calculation of planning materiality is

done by considering any one of the three factors which are Total Assets, Sales and Equity. It

generally considers the highest amount factor which helps it to get a proper amount of

materiality in regards to entity operations (He, Zeadally and Wu 2015). As per the company

is consider auditor has taken the total asset value in consideration for the calculation of

planning materiality and the percentage is imposed is 5%. Calculation of planning materiality

is listed below:

Planning Materiality=Total Asset∗5 %

¿ $ 93657465∗5 %

¿ $ 4682873.25

The calculation shows the materiality of the entity and with the help of which the auditor can

plan its audit strategy that it will carry upon the company financial report. The auditor can

AUDITING

materiality that signifies that the entity books not made as per different accounting

frameworks and guidelines.

Auditor plans the amount of materiality at the starting stage of audit process as this

helps it to know the audit process which is being carried upon the entity accounting books

(Griffiths 2016). Planning materiality assists the auditor to understand the materiality involve

in their business activities, and with the help of which the auditor plans the amount of audit

procedure it requires to perform upon the entity activities. These also assist the auditor in

having an idea about the timing and scope of audit that is to be performed by the auditor upon

the entity operations (Groomer and Murthy 2018). The auditor can know where it has to give

more emphasis and how easily it able to gather more audit evidence in regards to fraud and

other error done by the company in that accounting year.

The ascertain which the auditor make at the begging of its audit process is solely

based upon the planning materiality (Hall 2015). The calculation of planning materiality is

done by considering any one of the three factors which are Total Assets, Sales and Equity. It

generally considers the highest amount factor which helps it to get a proper amount of

materiality in regards to entity operations (He, Zeadally and Wu 2015). As per the company

is consider auditor has taken the total asset value in consideration for the calculation of

planning materiality and the percentage is imposed is 5%. Calculation of planning materiality

is listed below:

Planning Materiality=Total Asset∗5 %

¿ $ 93657465∗5 %

¿ $ 4682873.25

The calculation shows the materiality of the entity and with the help of which the auditor can

plan its audit strategy that it will carry upon the company financial report. The auditor can

8

AUDITING

know how much time it has to give in regards of each aspect of the business activity and how

it will able to collect audit evidence with the help of test of control and different substantive

procedure in entity operations.

Risk Associated in Above mentioned Accounts

The risk that has associated in above mention account has adequately been analysis by

the auditor as the auditor has carry substantive procedure in the entity financial information

which assists it about the amount of risk involved in each type of account. The risk which can

found in a company statement is control and inherent risk.

Inherent risk is those risk which cannot be controlled by the internal control of the

entity. There is a risk which cannot be minimised by the entity while carrying their business

activities. Control risk is those type of risk which can be easily controlled by the

management. These are the error or omission which occurs in entity business, and that can

quickly be minimised if the entity has sound internal control system in their activities. The

risk and the substantive procedure that is carried by the auditor shown below:

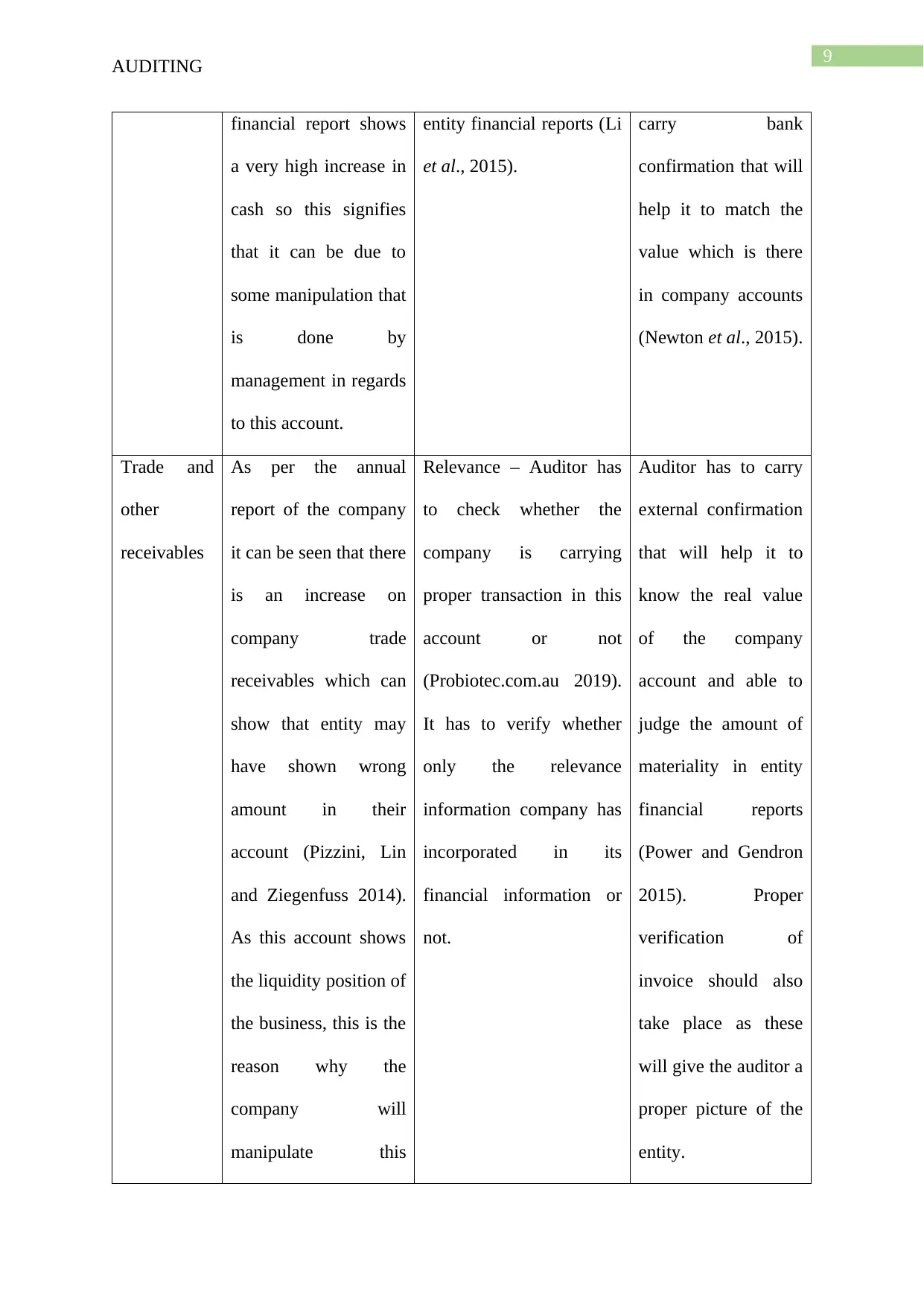

Account

Affected

Risk of Material

Misstatement

Assertions Audit Procedure

Cash and

Cash

Equivalents

The risk of material

misstatement is very

high in this account as

this is a liquid account

so the company can

easily manipulate the

account (Knechel, and

Salterio 2016). As the

Completeness – Auditor

has to check that the

entity has recorded each

transaction properly in

their financial statement

as if there is any

misstatement than it will

show an adverse effect in

Auditor has tom

verify the cash

register of the entity

to ascertain that the

entity can record each

transaction in their

financial books. The

auditor should also

AUDITING

know how much time it has to give in regards of each aspect of the business activity and how

it will able to collect audit evidence with the help of test of control and different substantive

procedure in entity operations.

Risk Associated in Above mentioned Accounts

The risk that has associated in above mention account has adequately been analysis by

the auditor as the auditor has carry substantive procedure in the entity financial information

which assists it about the amount of risk involved in each type of account. The risk which can

found in a company statement is control and inherent risk.

Inherent risk is those risk which cannot be controlled by the internal control of the

entity. There is a risk which cannot be minimised by the entity while carrying their business

activities. Control risk is those type of risk which can be easily controlled by the

management. These are the error or omission which occurs in entity business, and that can

quickly be minimised if the entity has sound internal control system in their activities. The

risk and the substantive procedure that is carried by the auditor shown below:

Account

Affected

Risk of Material

Misstatement

Assertions Audit Procedure

Cash and

Cash

Equivalents

The risk of material

misstatement is very

high in this account as

this is a liquid account

so the company can

easily manipulate the

account (Knechel, and

Salterio 2016). As the

Completeness – Auditor

has to check that the

entity has recorded each

transaction properly in

their financial statement

as if there is any

misstatement than it will

show an adverse effect in

Auditor has tom

verify the cash

register of the entity

to ascertain that the

entity can record each

transaction in their

financial books. The

auditor should also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

financial report shows

a very high increase in

cash so this signifies

that it can be due to

some manipulation that

is done by

management in regards

to this account.

entity financial reports (Li

et al., 2015).

carry bank

confirmation that will

help it to match the

value which is there

in company accounts

(Newton et al., 2015).

Trade and

other

receivables

As per the annual

report of the company

it can be seen that there

is an increase on

company trade

receivables which can

show that entity may

have shown wrong

amount in their

account (Pizzini, Lin

and Ziegenfuss 2014).

As this account shows

the liquidity position of

the business, this is the

reason why the

company will

manipulate this

Relevance – Auditor has

to check whether the

company is carrying

proper transaction in this

account or not

(Probiotec.com.au 2019).

It has to verify whether

only the relevance

information company has

incorporated in its

financial information or

not.

Auditor has to carry

external confirmation

that will help it to

know the real value

of the company

account and able to

judge the amount of

materiality in entity

financial reports

(Power and Gendron

2015). Proper

verification of

invoice should also

take place as these

will give the auditor a

proper picture of the

entity.

AUDITING

financial report shows

a very high increase in

cash so this signifies

that it can be due to

some manipulation that

is done by

management in regards

to this account.

entity financial reports (Li

et al., 2015).

carry bank

confirmation that will

help it to match the

value which is there

in company accounts

(Newton et al., 2015).

Trade and

other

receivables

As per the annual

report of the company

it can be seen that there

is an increase on

company trade

receivables which can

show that entity may

have shown wrong

amount in their

account (Pizzini, Lin

and Ziegenfuss 2014).

As this account shows

the liquidity position of

the business, this is the

reason why the

company will

manipulate this

Relevance – Auditor has

to check whether the

company is carrying

proper transaction in this

account or not

(Probiotec.com.au 2019).

It has to verify whether

only the relevance

information company has

incorporated in its

financial information or

not.

Auditor has to carry

external confirmation

that will help it to

know the real value

of the company

account and able to

judge the amount of

materiality in entity

financial reports

(Power and Gendron

2015). Proper

verification of

invoice should also

take place as these

will give the auditor a

proper picture of the

entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

account in their books

of account

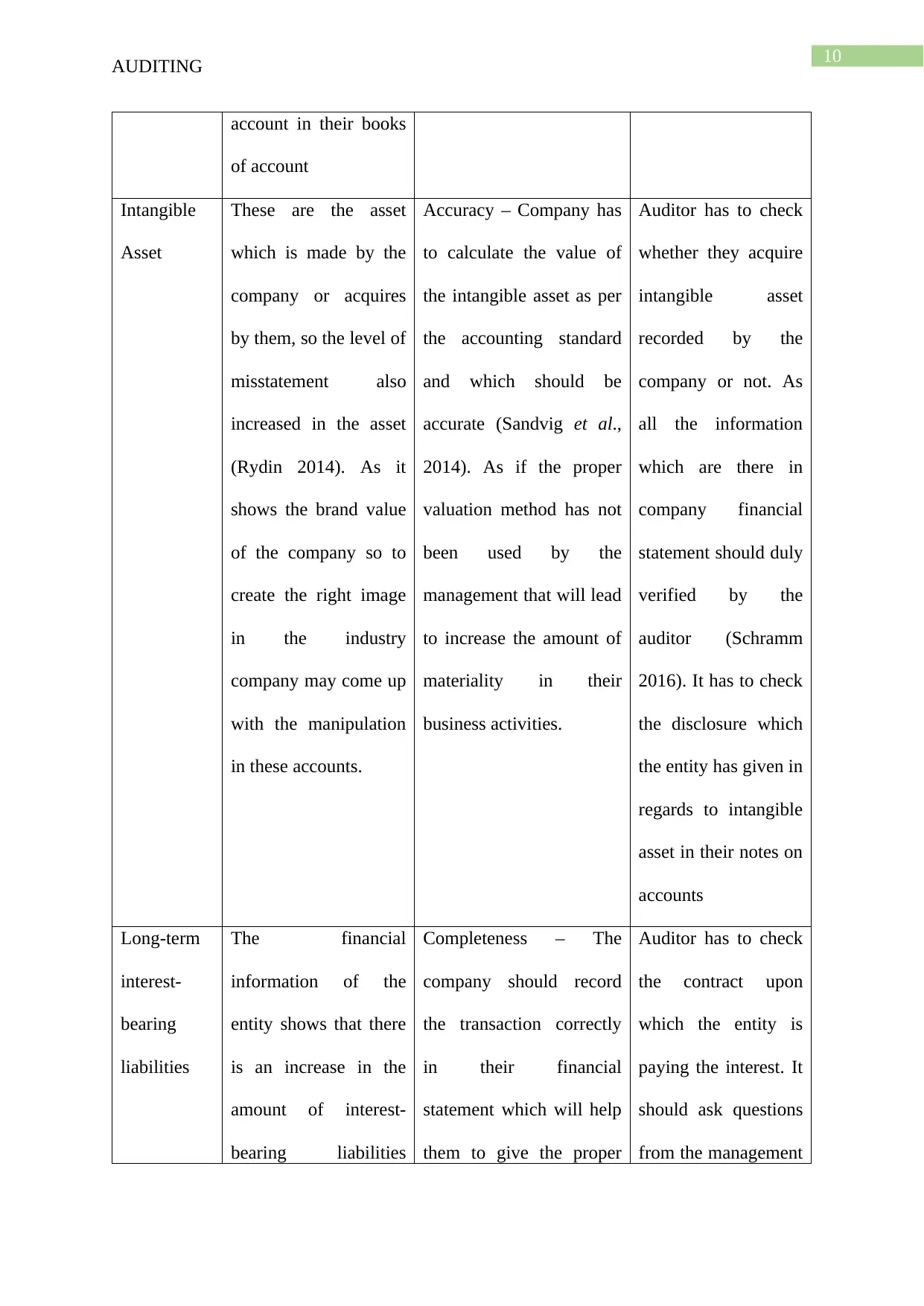

Intangible

Asset

These are the asset

which is made by the

company or acquires

by them, so the level of

misstatement also

increased in the asset

(Rydin 2014). As it

shows the brand value

of the company so to

create the right image

in the industry

company may come up

with the manipulation

in these accounts.

Accuracy – Company has

to calculate the value of

the intangible asset as per

the accounting standard

and which should be

accurate (Sandvig et al.,

2014). As if the proper

valuation method has not

been used by the

management that will lead

to increase the amount of

materiality in their

business activities.

Auditor has to check

whether they acquire

intangible asset

recorded by the

company or not. As

all the information

which are there in

company financial

statement should duly

verified by the

auditor (Schramm

2016). It has to check

the disclosure which

the entity has given in

regards to intangible

asset in their notes on

accounts

Long-term

interest-

bearing

liabilities

The financial

information of the

entity shows that there

is an increase in the

amount of interest-

bearing liabilities

Completeness – The

company should record

the transaction correctly

in their financial

statement which will help

them to give the proper

Auditor has to check

the contract upon

which the entity is

paying the interest. It

should ask questions

from the management

AUDITING

account in their books

of account

Intangible

Asset

These are the asset

which is made by the

company or acquires

by them, so the level of

misstatement also

increased in the asset

(Rydin 2014). As it

shows the brand value

of the company so to

create the right image

in the industry

company may come up

with the manipulation

in these accounts.

Accuracy – Company has

to calculate the value of

the intangible asset as per

the accounting standard

and which should be

accurate (Sandvig et al.,

2014). As if the proper

valuation method has not

been used by the

management that will lead

to increase the amount of

materiality in their

business activities.

Auditor has to check

whether they acquire

intangible asset

recorded by the

company or not. As

all the information

which are there in

company financial

statement should duly

verified by the

auditor (Schramm

2016). It has to check

the disclosure which

the entity has given in

regards to intangible

asset in their notes on

accounts

Long-term

interest-

bearing

liabilities

The financial

information of the

entity shows that there

is an increase in the

amount of interest-

bearing liabilities

Completeness – The

company should record

the transaction correctly

in their financial

statement which will help

them to give the proper

Auditor has to check

the contract upon

which the entity is

paying the interest. It

should ask questions

from the management

11

AUDITING

which signify the risk

of misstatement in the

account (Shen et al.,

2017). The entity to

show their financial

health strong may

manipulate these

account figure; as a

result, the materiality

will occur in the

company books of

accounts

amount of information to

the users. As if the entity

is not able to record the

transition correctly than

the risk of misstatement

will increase in the

business.

related to the changes

in the figure in an

accounting year.

Proper verification of

the disclosure should

also be done by the

auditor to get a

picture of how the

entity is dealing with

the account in their

business activities.

Long Term

Provisions

As there is an increase

in the amount provided

in compare to last year,

which denotes that

there can be risk of

materiality in the

business. The company

has increased the

provision which will

also give an impact

upon the overall

financial health of the

entity.

Relevance – Company

should only take relevant

information in the

financial information. It

should make provision as

per the accounting

standard, and the entity

should carry no irrelevant

information in their books

of accounts.

The auditor should

match the provision

with the accounting

standard to verify that

the entity has

followed the said

accounting standard

in their books of

account. Industry-

standard should be

analysed by the

auditor to ascertain

the level of

AUDITING

which signify the risk

of misstatement in the

account (Shen et al.,

2017). The entity to

show their financial

health strong may

manipulate these

account figure; as a

result, the materiality

will occur in the

company books of

accounts

amount of information to

the users. As if the entity

is not able to record the

transition correctly than

the risk of misstatement

will increase in the

business.

related to the changes

in the figure in an

accounting year.

Proper verification of

the disclosure should

also be done by the

auditor to get a

picture of how the

entity is dealing with

the account in their

business activities.

Long Term

Provisions

As there is an increase

in the amount provided

in compare to last year,

which denotes that

there can be risk of

materiality in the

business. The company

has increased the

provision which will

also give an impact

upon the overall

financial health of the

entity.

Relevance – Company

should only take relevant

information in the

financial information. It

should make provision as

per the accounting

standard, and the entity

should carry no irrelevant

information in their books

of accounts.

The auditor should

match the provision

with the accounting

standard to verify that

the entity has

followed the said

accounting standard

in their books of

account. Industry-

standard should be

analysed by the

auditor to ascertain

the level of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.