Auditing and Professional Practice Assignment - Financial Review

VerifiedAdded on 2023/06/04

|12

|2371

|110

Report

AI Summary

This report provides an audit plan for a small entity, including materiality determination based on the provided trial balance for 2016 and 2017. It includes a preliminary analytical review, variance analysis, and a common size income statement. The report identifies critical accounts with potential anomalies and suggests appropriate audit procedures for each. It also assesses fraud risk, highlighting the importance of professional skepticism and thorough verification of financial statements, despite initial assumptions of trustworthiness. The analysis focuses on accounts such as sales, cost of sales, superannuation expenses, and depreciation, recommending specific vouching and verification steps to ensure compliance with accounting standards and regulations. The report concludes by emphasizing the need for a comprehensive fraud risk analysis and careful examination of accounts with significant variances.

Auditing and

Professional Practice

Assignment

Professional Practice

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Conclusion & Recommendation..................................................................................................................8

References.................................................................................................................................................10

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Conclusion & Recommendation..................................................................................................................8

References.................................................................................................................................................10

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

A report has been prepared on one of the small entity for which the audit planning is to be done.

The trial balance of the company has been given from which the materiality of the entity needs to

be determined. Besides this, the preliminary analytical review of the company has been done and

variance analysis and the common size income statement has been prepared based on the input

for both the given year 2016 and 2017 (Dichev, 2017). The report highlights the critical accounts

where major anomalies can be seen and the audit procedures to be employed for each of these

accounts has been shown. At the end, the fraud risk analysis has also been done for the entity to

check the possibility of fraud, material misstatements, errors and other omissions, if any, in the

entity.

3 | P a g e

Introduction

A report has been prepared on one of the small entity for which the audit planning is to be done.

The trial balance of the company has been given from which the materiality of the entity needs to

be determined. Besides this, the preliminary analytical review of the company has been done and

variance analysis and the common size income statement has been prepared based on the input

for both the given year 2016 and 2017 (Dichev, 2017). The report highlights the critical accounts

where major anomalies can be seen and the audit procedures to be employed for each of these

accounts has been shown. At the end, the fraud risk analysis has also been done for the entity to

check the possibility of fraud, material misstatements, errors and other omissions, if any, in the

entity.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

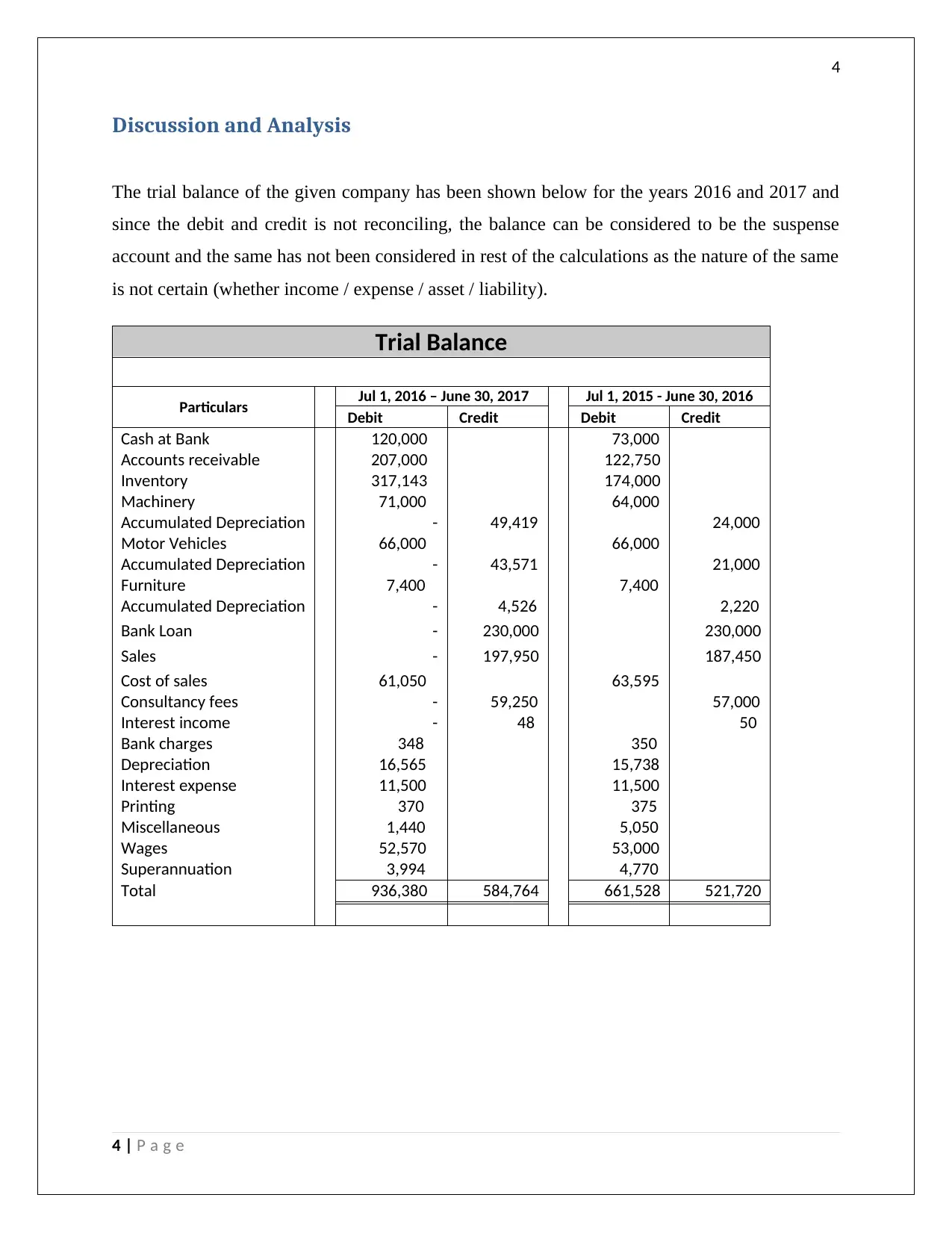

Discussion and Analysis

The trial balance of the given company has been shown below for the years 2016 and 2017 and

since the debit and credit is not reconciling, the balance can be considered to be the suspense

account and the same has not been considered in rest of the calculations as the nature of the same

is not certain (whether income / expense / asset / liability).

Trial Balance

Particulars Jul 1, 2016 – June 30, 2017 Jul 1, 2015 - June 30, 2016

Debit Credit Debit Credit

Cash at Bank 120,000 73,000

Accounts receivable 207,000 122,750

Inventory 317,143 174,000

Machinery 71,000 64,000

Accumulated Depreciation - 49,419 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation - 43,571 21,000

Furniture 7,400 7,400

Accumulated Depreciation - 4,526 2,220

Bank Loan - 230,000 230,000

Sales - 197,950 187,450

Cost of sales 61,050 63,595

Consultancy fees - 59,250 57,000

Interest income - 48 50

Bank charges 348 350

Depreciation 16,565 15,738

Interest expense 11,500 11,500

Printing 370 375

Miscellaneous 1,440 5,050

Wages 52,570 53,000

Superannuation 3,994 4,770

Total 936,380 584,764 661,528 521,720

4 | P a g e

Discussion and Analysis

The trial balance of the given company has been shown below for the years 2016 and 2017 and

since the debit and credit is not reconciling, the balance can be considered to be the suspense

account and the same has not been considered in rest of the calculations as the nature of the same

is not certain (whether income / expense / asset / liability).

Trial Balance

Particulars Jul 1, 2016 – June 30, 2017 Jul 1, 2015 - June 30, 2016

Debit Credit Debit Credit

Cash at Bank 120,000 73,000

Accounts receivable 207,000 122,750

Inventory 317,143 174,000

Machinery 71,000 64,000

Accumulated Depreciation - 49,419 24,000

Motor Vehicles 66,000 66,000

Accumulated Depreciation - 43,571 21,000

Furniture 7,400 7,400

Accumulated Depreciation - 4,526 2,220

Bank Loan - 230,000 230,000

Sales - 197,950 187,450

Cost of sales 61,050 63,595

Consultancy fees - 59,250 57,000

Interest income - 48 50

Bank charges 348 350

Depreciation 16,565 15,738

Interest expense 11,500 11,500

Printing 370 375

Miscellaneous 1,440 5,050

Wages 52,570 53,000

Superannuation 3,994 4,770

Total 936,380 584,764 661,528 521,720

4 | P a g e

5

1. In the first place, the materiality level is to be determined for the given entity as it will

help in ascertaining which is the extent to which the checking needs to be done and what

can be ignored. Anything is said to be material if it has the ability to change the economic

or financial decision of the end user or the relevant stakeholder. It gives the auditor an

idea as to what is the value limit until which the audit is to be restrained. It is one of the

essential tools in the audit planning (Belton, 2017). In the given case, the materiality

level, which has been determined by the head auditor of the consulting firm, is $ 15000

but the same is too high considering the values in the trial balance. There has been

various iterations and the limits, which have been suggested by the accounting boards

over the globe like those including IASB and several other top consulting and auditing

companies. Some of these limits are 0.5%-1% of the gross sales or the total assets, 1-2%

of the gross profit or the fixed assets or the shareholder’s equity or 5-10% of the net

profit. Based on these percentages, the materiality limit for the given company can be

worked out to $ 1686.6 to $ 1979.5 (Jefferson, 2017). The benefit of choosing this limit is

some accounts like Interest expenses, superannuation and depreciation and furniture

account would also be covered by audit, which would have been ignored as per earlier

limits.

(in $)

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 197,950 989.75 to 1979.5

1% to 2% of the total assets Total Assets 691,027 6910.27 to 13820.54

1% to 2% of the gross profit Gross Profit 84,330 843.3 to 1686.6

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 109,411 5470.60 to 10941.10

5 | P a g e

1. In the first place, the materiality level is to be determined for the given entity as it will

help in ascertaining which is the extent to which the checking needs to be done and what

can be ignored. Anything is said to be material if it has the ability to change the economic

or financial decision of the end user or the relevant stakeholder. It gives the auditor an

idea as to what is the value limit until which the audit is to be restrained. It is one of the

essential tools in the audit planning (Belton, 2017). In the given case, the materiality

level, which has been determined by the head auditor of the consulting firm, is $ 15000

but the same is too high considering the values in the trial balance. There has been

various iterations and the limits, which have been suggested by the accounting boards

over the globe like those including IASB and several other top consulting and auditing

companies. Some of these limits are 0.5%-1% of the gross sales or the total assets, 1-2%

of the gross profit or the fixed assets or the shareholder’s equity or 5-10% of the net

profit. Based on these percentages, the materiality limit for the given company can be

worked out to $ 1686.6 to $ 1979.5 (Jefferson, 2017). The benefit of choosing this limit is

some accounts like Interest expenses, superannuation and depreciation and furniture

account would also be covered by audit, which would have been ignored as per earlier

limits.

(in $)

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 197,950 989.75 to 1979.5

1% to 2% of the total assets Total Assets 691,027 6910.27 to 13820.54

1% to 2% of the gross profit Gross Profit 84,330 843.3 to 1686.6

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 109,411 5470.60 to 10941.10

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

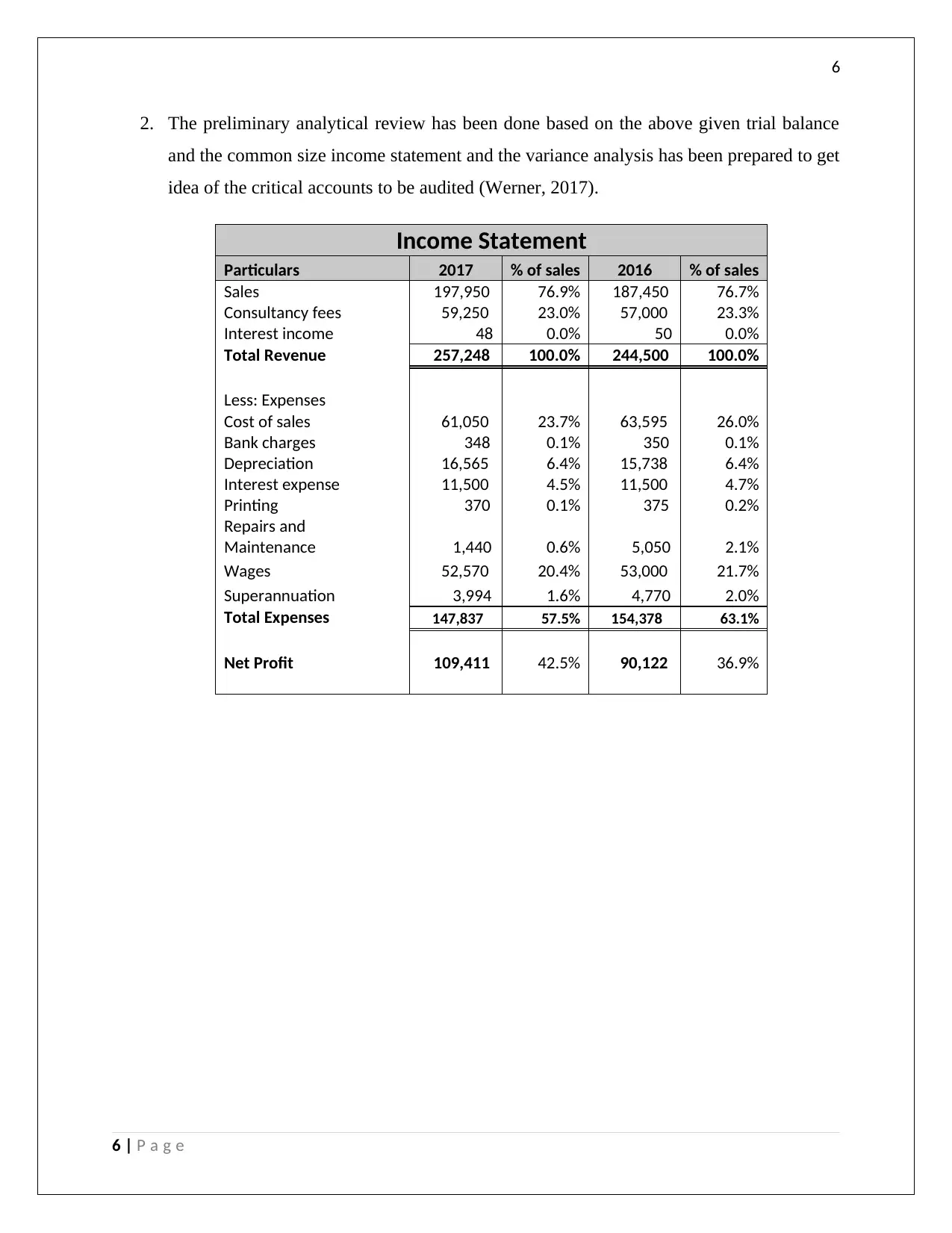

2. The preliminary analytical review has been done based on the above given trial balance

and the common size income statement and the variance analysis has been prepared to get

idea of the critical accounts to be audited (Werner, 2017).

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 197,950 76.9% 187,450 76.7%

Consultancy fees 59,250 23.0% 57,000 23.3%

Interest income 48 0.0% 50 0.0%

Total Revenue 257,248 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 61,050 23.7% 63,595 26.0%

Bank charges 348 0.1% 350 0.1%

Depreciation 16,565 6.4% 15,738 6.4%

Interest expense 11,500 4.5% 11,500 4.7%

Printing 370 0.1% 375 0.2%

Repairs and

Maintenance 1,440 0.6% 5,050 2.1%

Wages 52,570 20.4% 53,000 21.7%

Superannuation 3,994 1.6% 4,770 2.0%

Total Expenses 147,837 57.5% 154,378 63.1%

Net Profit 109,411 42.5% 90,122 36.9%

6 | P a g e

2. The preliminary analytical review has been done based on the above given trial balance

and the common size income statement and the variance analysis has been prepared to get

idea of the critical accounts to be audited (Werner, 2017).

Income Statement

Particulars 2017 % of sales 2016 % of sales

Sales 197,950 76.9% 187,450 76.7%

Consultancy fees 59,250 23.0% 57,000 23.3%

Interest income 48 0.0% 50 0.0%

Total Revenue 257,248 100.0% 244,500 100.0%

Less: Expenses

Cost of sales 61,050 23.7% 63,595 26.0%

Bank charges 348 0.1% 350 0.1%

Depreciation 16,565 6.4% 15,738 6.4%

Interest expense 11,500 4.5% 11,500 4.7%

Printing 370 0.1% 375 0.2%

Repairs and

Maintenance 1,440 0.6% 5,050 2.1%

Wages 52,570 20.4% 53,000 21.7%

Superannuation 3,994 1.6% 4,770 2.0%

Total Expenses 147,837 57.5% 154,378 63.1%

Net Profit 109,411 42.5% 90,122 36.9%

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

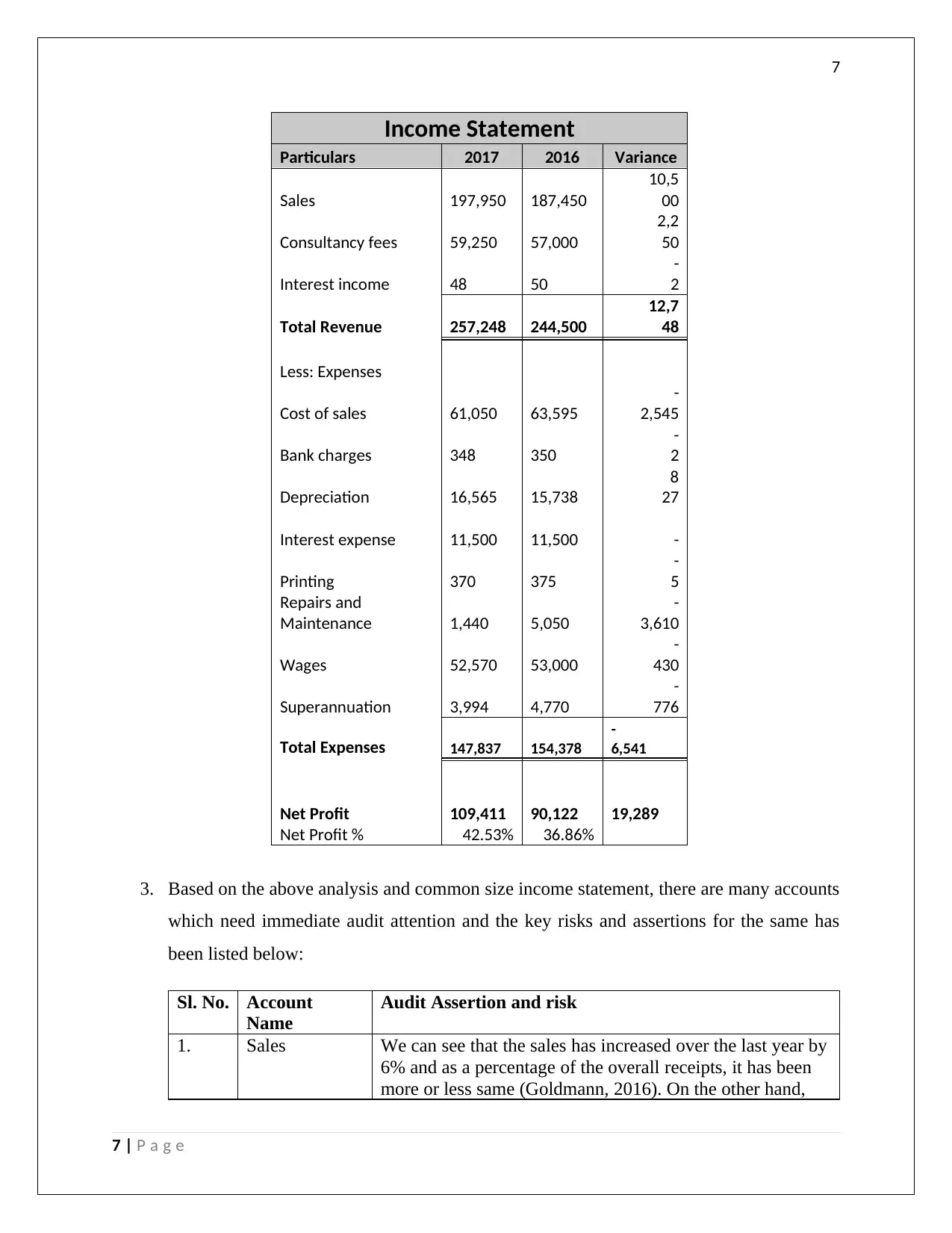

Income Statement

Particulars 2017 2016 Variance

Sales 197,950 187,450

10,5

00

Consultancy fees 59,250 57,000

2,2

50

Interest income 48 50

-

2

Total Revenue 257,248 244,500

12,7

48

Less: Expenses

Cost of sales 61,050 63,595

-

2,545

Bank charges 348 350

-

2

Depreciation 16,565 15,738

8

27

Interest expense 11,500 11,500 -

Printing 370 375

-

5

Repairs and

Maintenance 1,440 5,050

-

3,610

Wages 52,570 53,000

-

430

Superannuation 3,994 4,770

-

776

Total Expenses 147,837 154,378

-

6,541

Net Profit 109,411 90,122 19,289

Net Profit % 42.53% 36.86%

3. Based on the above analysis and common size income statement, there are many accounts

which need immediate audit attention and the key risks and assertions for the same has

been listed below:

Sl. No. Account

Name

Audit Assertion and risk

1. Sales We can see that the sales has increased over the last year by

6% and as a percentage of the overall receipts, it has been

more or less same (Goldmann, 2016). On the other hand,

7 | P a g e

Income Statement

Particulars 2017 2016 Variance

Sales 197,950 187,450

10,5

00

Consultancy fees 59,250 57,000

2,2

50

Interest income 48 50

-

2

Total Revenue 257,248 244,500

12,7

48

Less: Expenses

Cost of sales 61,050 63,595

-

2,545

Bank charges 348 350

-

2

Depreciation 16,565 15,738

8

27

Interest expense 11,500 11,500 -

Printing 370 375

-

5

Repairs and

Maintenance 1,440 5,050

-

3,610

Wages 52,570 53,000

-

430

Superannuation 3,994 4,770

-

776

Total Expenses 147,837 154,378

-

6,541

Net Profit 109,411 90,122 19,289

Net Profit % 42.53% 36.86%

3. Based on the above analysis and common size income statement, there are many accounts

which need immediate audit attention and the key risks and assertions for the same has

been listed below:

Sl. No. Account

Name

Audit Assertion and risk

1. Sales We can see that the sales has increased over the last year by

6% and as a percentage of the overall receipts, it has been

more or less same (Goldmann, 2016). On the other hand,

7 | P a g e

8

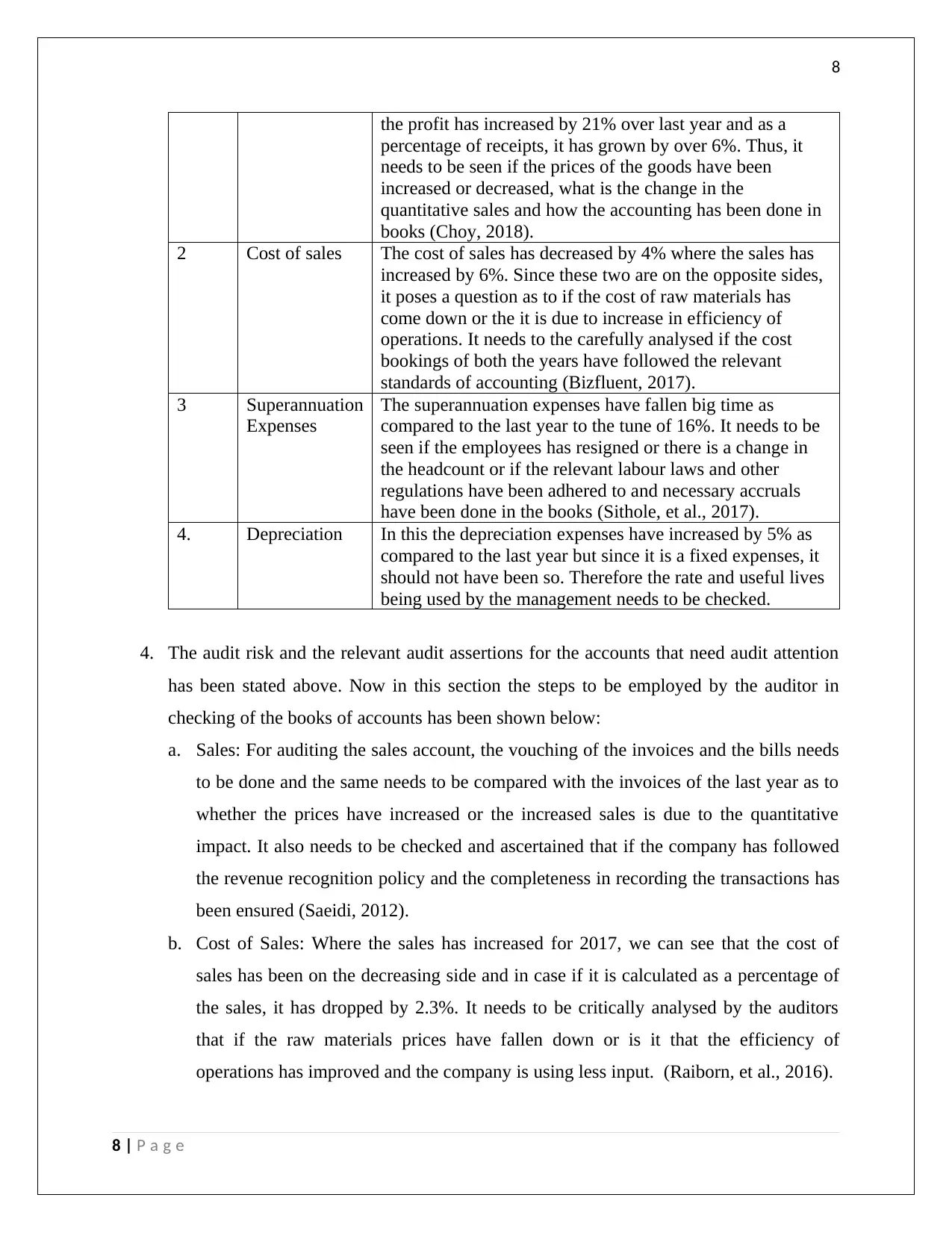

the profit has increased by 21% over last year and as a

percentage of receipts, it has grown by over 6%. Thus, it

needs to be seen if the prices of the goods have been

increased or decreased, what is the change in the

quantitative sales and how the accounting has been done in

books (Choy, 2018).

2 Cost of sales The cost of sales has decreased by 4% where the sales has

increased by 6%. Since these two are on the opposite sides,

it poses a question as to if the cost of raw materials has

come down or the it is due to increase in efficiency of

operations. It needs to the carefully analysed if the cost

bookings of both the years have followed the relevant

standards of accounting (Bizfluent, 2017).

3 Superannuation

Expenses

The superannuation expenses have fallen big time as

compared to the last year to the tune of 16%. It needs to be

seen if the employees has resigned or there is a change in

the headcount or if the relevant labour laws and other

regulations have been adhered to and necessary accruals

have been done in the books (Sithole, et al., 2017).

4. Depreciation In this the depreciation expenses have increased by 5% as

compared to the last year but since it is a fixed expenses, it

should not have been so. Therefore the rate and useful lives

being used by the management needs to be checked.

4. The audit risk and the relevant audit assertions for the accounts that need audit attention

has been stated above. Now in this section the steps to be employed by the auditor in

checking of the books of accounts has been shown below:

a. Sales: For auditing the sales account, the vouching of the invoices and the bills needs

to be done and the same needs to be compared with the invoices of the last year as to

whether the prices have increased or the increased sales is due to the quantitative

impact. It also needs to be checked and ascertained that if the company has followed

the revenue recognition policy and the completeness in recording the transactions has

been ensured (Saeidi, 2012).

b. Cost of Sales: Where the sales has increased for 2017, we can see that the cost of

sales has been on the decreasing side and in case if it is calculated as a percentage of

the sales, it has dropped by 2.3%. It needs to be critically analysed by the auditors

that if the raw materials prices have fallen down or is it that the efficiency of

operations has improved and the company is using less input. (Raiborn, et al., 2016).

8 | P a g e

the profit has increased by 21% over last year and as a

percentage of receipts, it has grown by over 6%. Thus, it

needs to be seen if the prices of the goods have been

increased or decreased, what is the change in the

quantitative sales and how the accounting has been done in

books (Choy, 2018).

2 Cost of sales The cost of sales has decreased by 4% where the sales has

increased by 6%. Since these two are on the opposite sides,

it poses a question as to if the cost of raw materials has

come down or the it is due to increase in efficiency of

operations. It needs to the carefully analysed if the cost

bookings of both the years have followed the relevant

standards of accounting (Bizfluent, 2017).

3 Superannuation

Expenses

The superannuation expenses have fallen big time as

compared to the last year to the tune of 16%. It needs to be

seen if the employees has resigned or there is a change in

the headcount or if the relevant labour laws and other

regulations have been adhered to and necessary accruals

have been done in the books (Sithole, et al., 2017).

4. Depreciation In this the depreciation expenses have increased by 5% as

compared to the last year but since it is a fixed expenses, it

should not have been so. Therefore the rate and useful lives

being used by the management needs to be checked.

4. The audit risk and the relevant audit assertions for the accounts that need audit attention

has been stated above. Now in this section the steps to be employed by the auditor in

checking of the books of accounts has been shown below:

a. Sales: For auditing the sales account, the vouching of the invoices and the bills needs

to be done and the same needs to be compared with the invoices of the last year as to

whether the prices have increased or the increased sales is due to the quantitative

impact. It also needs to be checked and ascertained that if the company has followed

the revenue recognition policy and the completeness in recording the transactions has

been ensured (Saeidi, 2012).

b. Cost of Sales: Where the sales has increased for 2017, we can see that the cost of

sales has been on the decreasing side and in case if it is calculated as a percentage of

the sales, it has dropped by 2.3%. It needs to be critically analysed by the auditors

that if the raw materials prices have fallen down or is it that the efficiency of

operations has improved and the company is using less input. (Raiborn, et al., 2016).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

c. Superannuation expenses: In the superannuation expenses, there has been the major

decrease of 16% as compared to the last year and it needs to be checked from the

employee register if the employees have left or the wages and salaries have been

lowered. Besides checking the completeness in the recording of all the expenses, the

auditor also needs to check the statutory requirements (Knechel & Salterio, 2016).

d. Depreciation: The auditor needs to check All the management estimates and

judgements needs to be taken into account and it also needs to be checked if the

company has recorded all the costs and not shifted them to the future years. The

useful lives, the depreciation rates and the asset class used by the company also needs

to be checked by the auditor.

Conclusion & Recommendation

5. In the given case, the audit partner has suggested that the fraud risk analysis need not be

done for the client as it is trustworthy and it can be assumed that there would be no fraud.

However, as per the principles laid down in APES 110 and the other statutes of

professional scepticism this is not acceptable and the auditor needs to check every given

client for fraud risk factors as mentioned in the auditing standards. The auditors are one

who give reasonable assurance on the financial statements being produced by the entities

and therefore it needs be verified (Linden & Freeman, 2017). Few of the accounts, which

hint that there can be fraud, are those of cost of sales and superannuation for reasons

stated above, and depreciation since the same has increased but the gross block of the

assets has remained the same. Also, it should be checked why the entity is keeping such a

high stock balance, the receivables balance and the cash balance as it is leading to

blockage of funds (Defond & Lennox, 2017).

9 | P a g e

c. Superannuation expenses: In the superannuation expenses, there has been the major

decrease of 16% as compared to the last year and it needs to be checked from the

employee register if the employees have left or the wages and salaries have been

lowered. Besides checking the completeness in the recording of all the expenses, the

auditor also needs to check the statutory requirements (Knechel & Salterio, 2016).

d. Depreciation: The auditor needs to check All the management estimates and

judgements needs to be taken into account and it also needs to be checked if the

company has recorded all the costs and not shifted them to the future years. The

useful lives, the depreciation rates and the asset class used by the company also needs

to be checked by the auditor.

Conclusion & Recommendation

5. In the given case, the audit partner has suggested that the fraud risk analysis need not be

done for the client as it is trustworthy and it can be assumed that there would be no fraud.

However, as per the principles laid down in APES 110 and the other statutes of

professional scepticism this is not acceptable and the auditor needs to check every given

client for fraud risk factors as mentioned in the auditing standards. The auditors are one

who give reasonable assurance on the financial statements being produced by the entities

and therefore it needs be verified (Linden & Freeman, 2017). Few of the accounts, which

hint that there can be fraud, are those of cost of sales and superannuation for reasons

stated above, and depreciation since the same has increased but the gross block of the

assets has remained the same. Also, it should be checked why the entity is keeping such a

high stock balance, the receivables balance and the cash balance as it is leading to

blockage of funds (Defond & Lennox, 2017).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 07 december 2017].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Defond, M. & Lennox, C., 2017. Do PCAOB Inspections Improve the Quality of Internal Control Audits?.

Journal of Accounting Research, 55(3), pp. 591-627.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

10 | P a g e

References

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 07 december 2017].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Defond, M. & Lennox, C., 2017. Do PCAOB Inspections Improve the Quality of Internal Control Audits?.

Journal of Accounting Research, 55(3), pp. 591-627.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

10 | P a g e

11

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. fourth ed. New York: Routledge.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Saeidi, F., 2012. Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), pp. 7031-41.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Knechel, W. & Salterio, S., 2016. Auditing:Assurance and Risk. fourth ed. New York: Routledge.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Saeidi, F., 2012. Audit expectations gap and corporate fraud: Empirical evidence from Iran. African

Journal of Business Management, 6(23), pp. 7031-41.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.