Auditing Professional Practice Report - Finance Module, Semester 1

VerifiedAdded on 2021/05/27

|5

|535

|52

Report

AI Summary

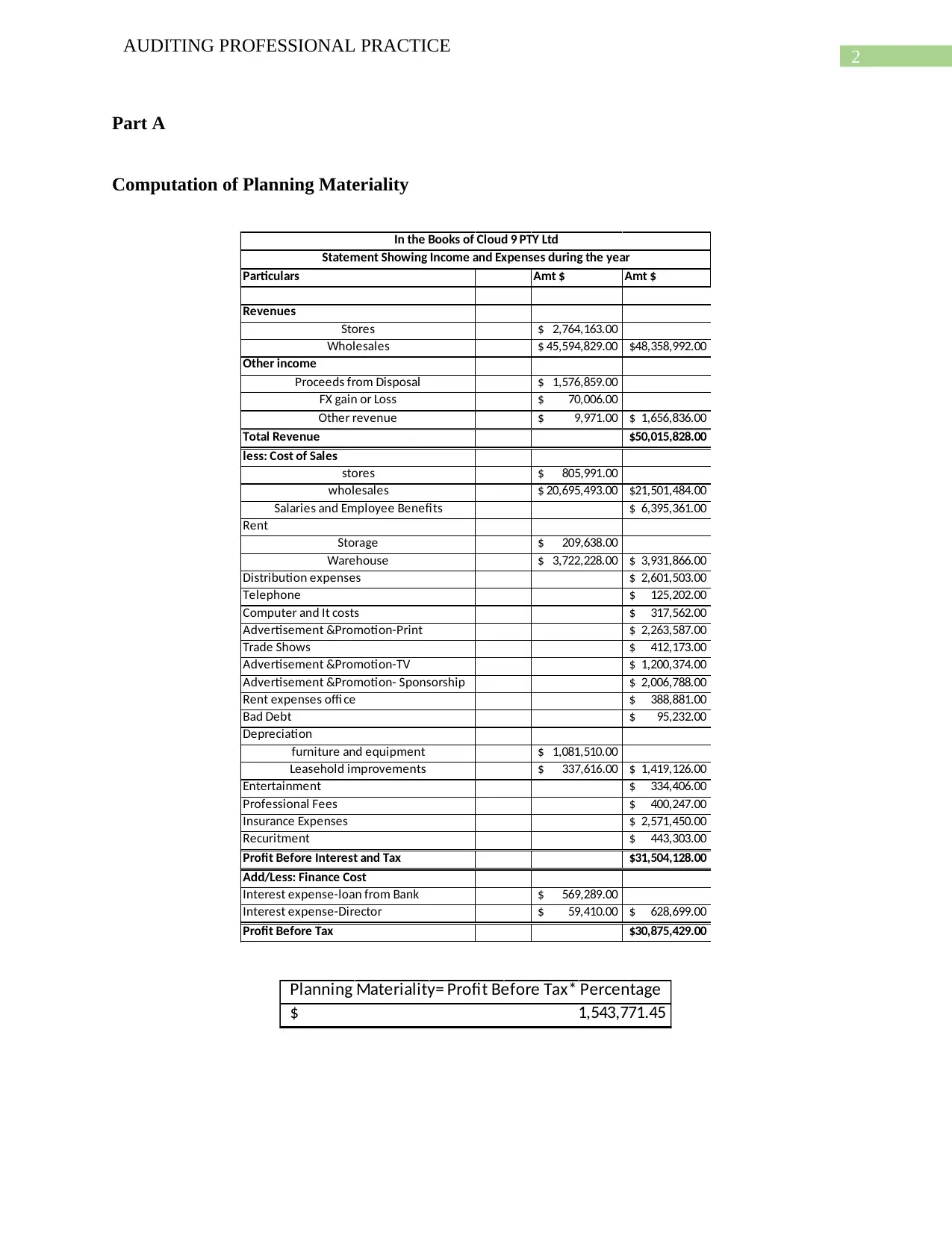

This report, focused on auditing professional practice, delves into key concepts such as planning materiality and its calculation, and the importance of materiality to auditors. The report computes planning materiality based on a business's profit before tax, highlighting the auditor's flexibility in choosing estimates. It emphasizes the significance of materiality as defined by International Standards of Auditing (ISA) 320, underscoring its role in identifying material misstatements and influencing stakeholder decisions. The report also discusses how auditors use materiality at the planning stage to identify potential misstatements and ensure financial statements accurately reflect a company's financial position. The role of materiality in the judgment of the auditor is also highlighted.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.