Auditing and Professional Practices Report for Chamoisee Enterprises

VerifiedAdded on 2023/06/06

|16

|2186

|105

Report

AI Summary

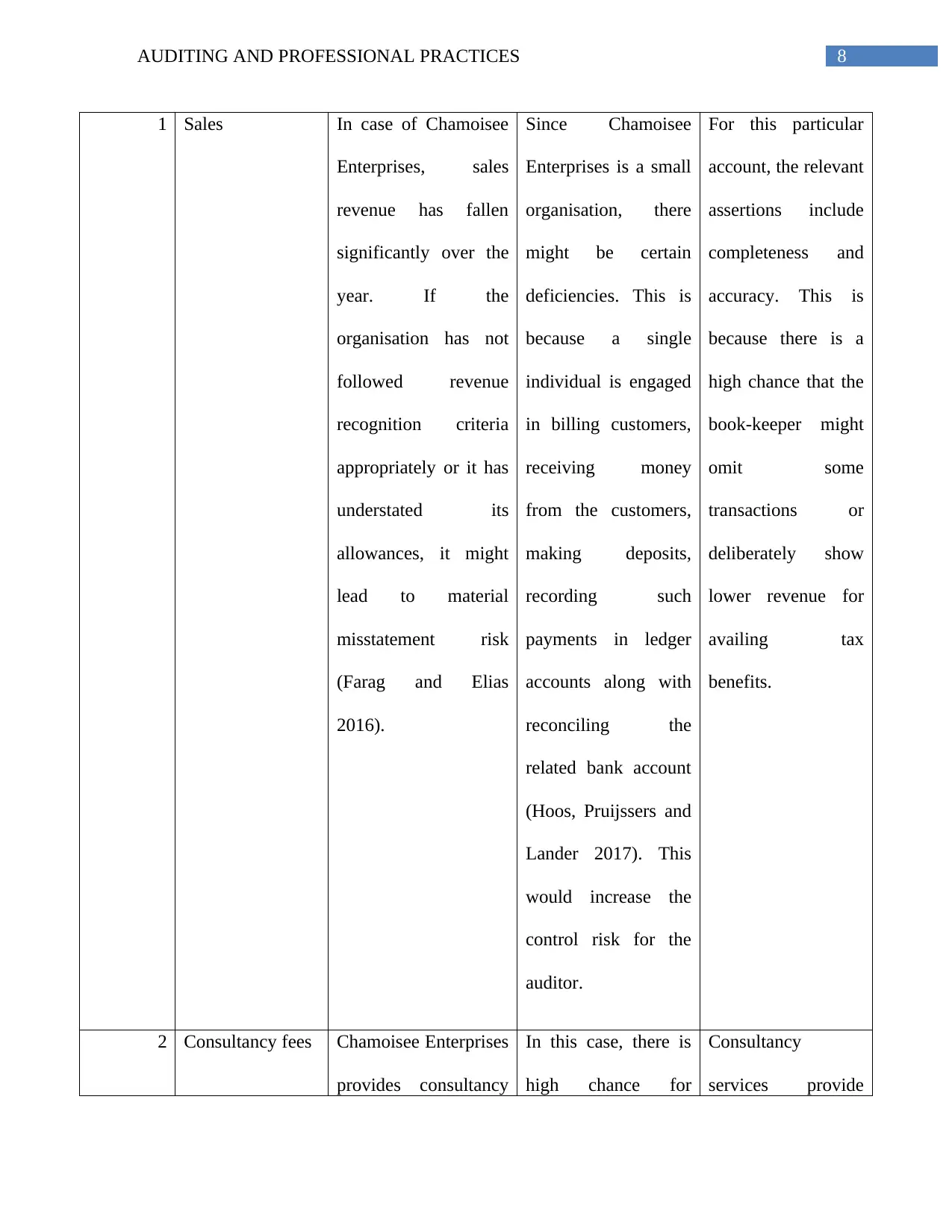

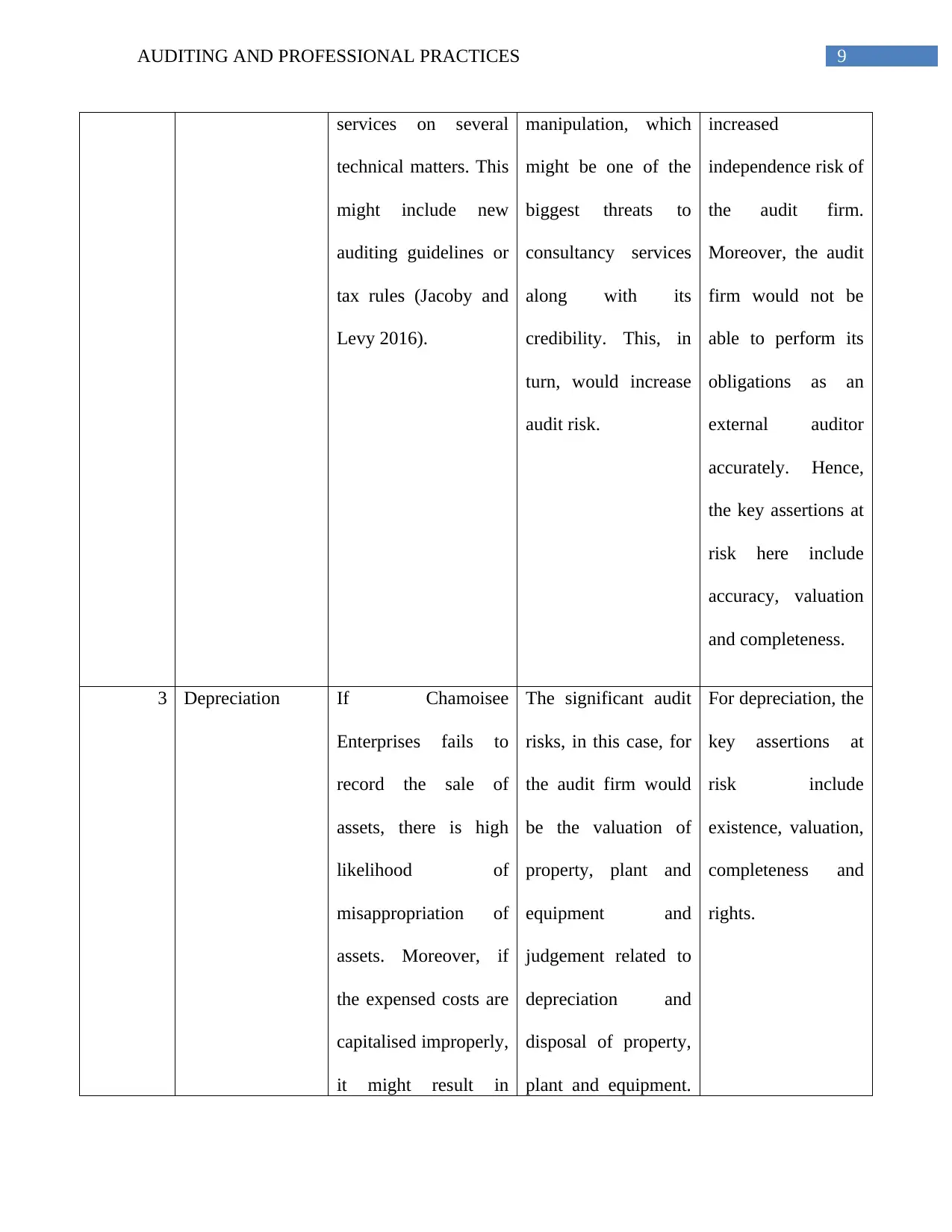

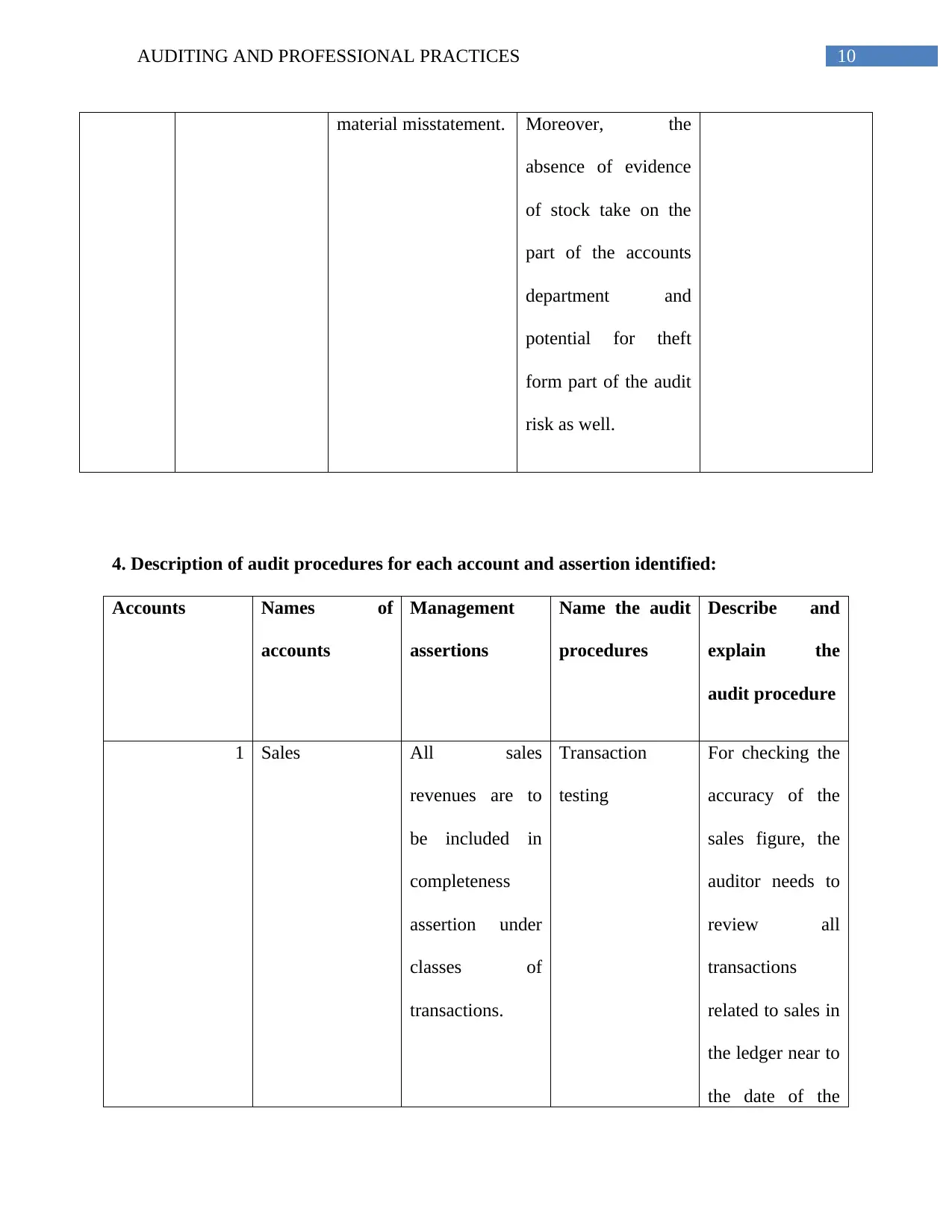

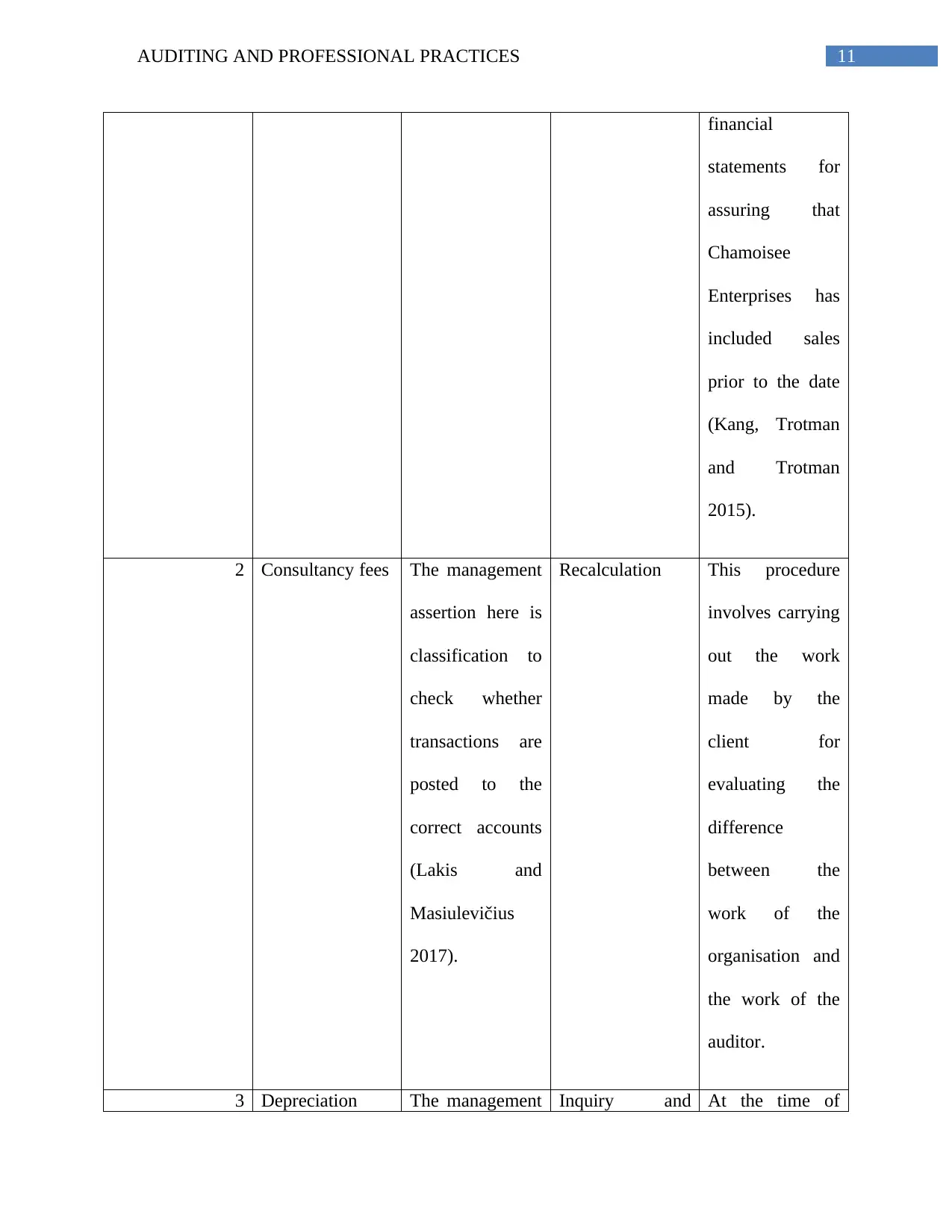

This report provides an in-depth analysis of the audit planning stage for Chamoisee Enterprises, a small audit client. The report begins by assessing the appropriateness of the materiality figure and its impact on the audit budget. It then performs an analytical review of income statement items using trend analysis. The core of the report identifies three income statement accounts at risk of material misstatement – sales, consultancy fees, and depreciation – and details the associated audit risks and relevant assertions for each. Specific audit procedures are recommended for each account and assertion. Finally, the report addresses the issue of fraud risk, evaluating the audit partner's suggestion to maintain professional skepticism. The report emphasizes the importance of considering professional skepticism in the audit process, especially in the context of potential fraud.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.