Auditing QEM Limited: Business Risks, Analytical Procedures, and Audit

VerifiedAdded on 2022/11/29

|12

|2123

|219

Report

AI Summary

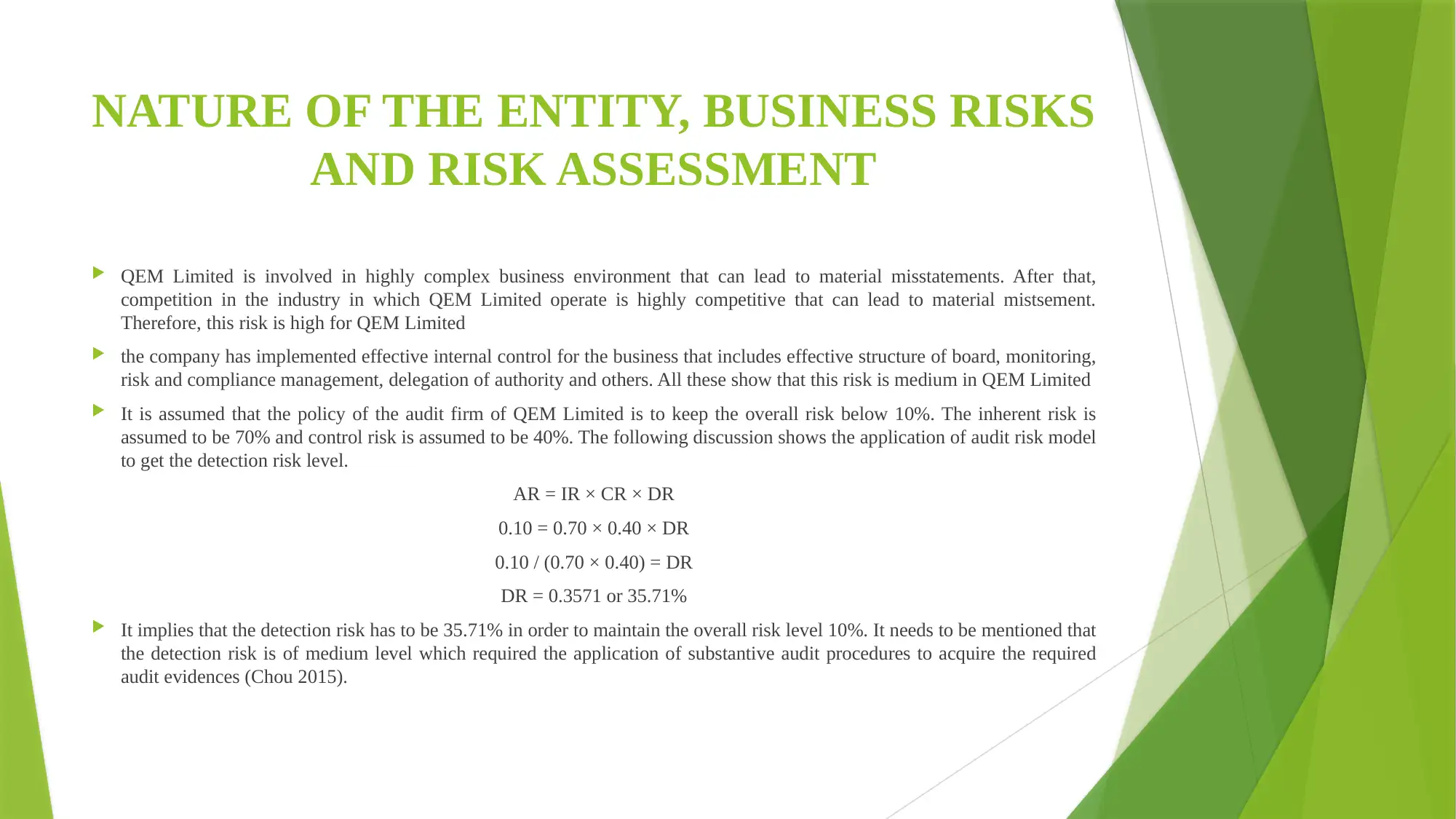

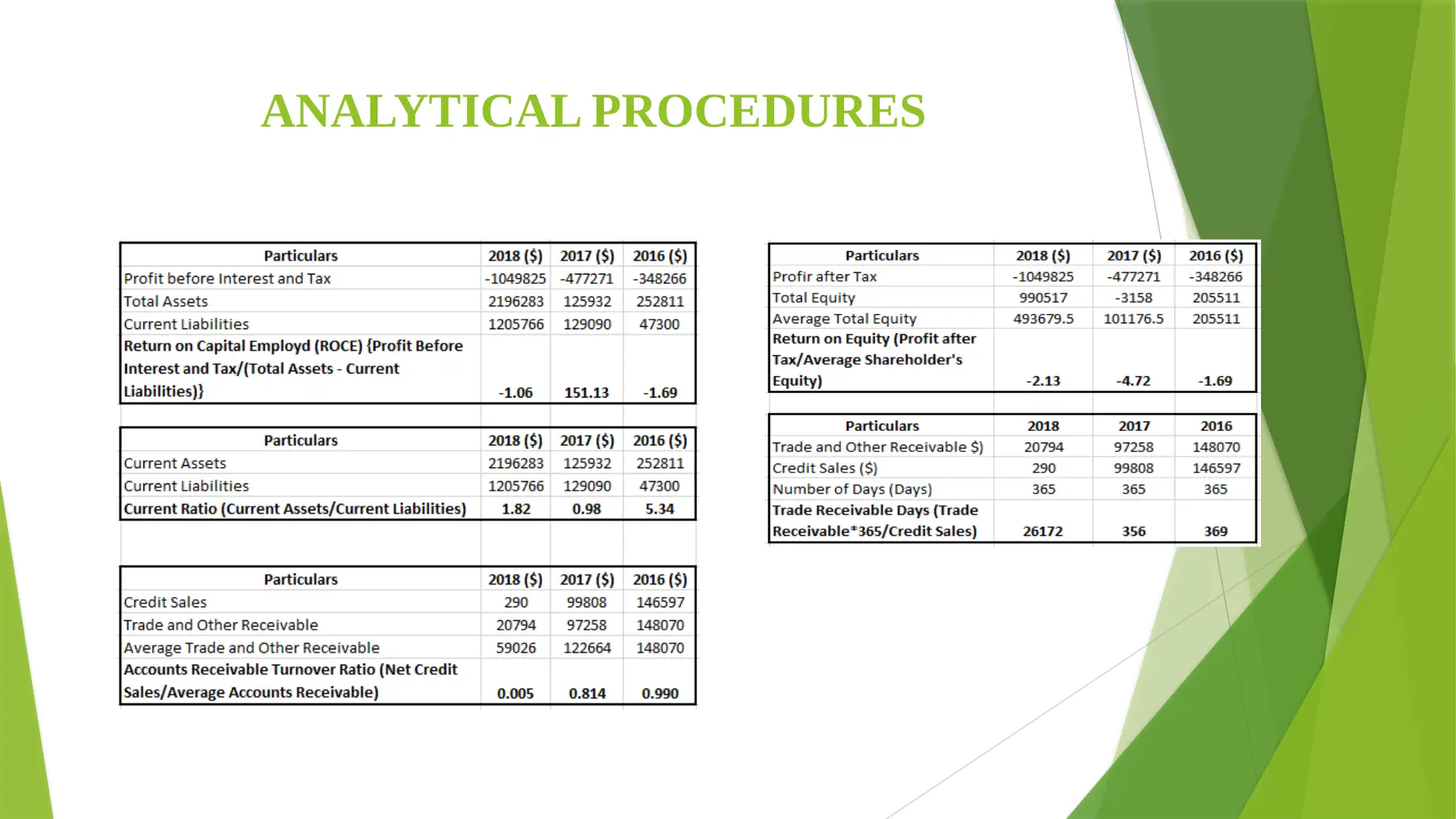

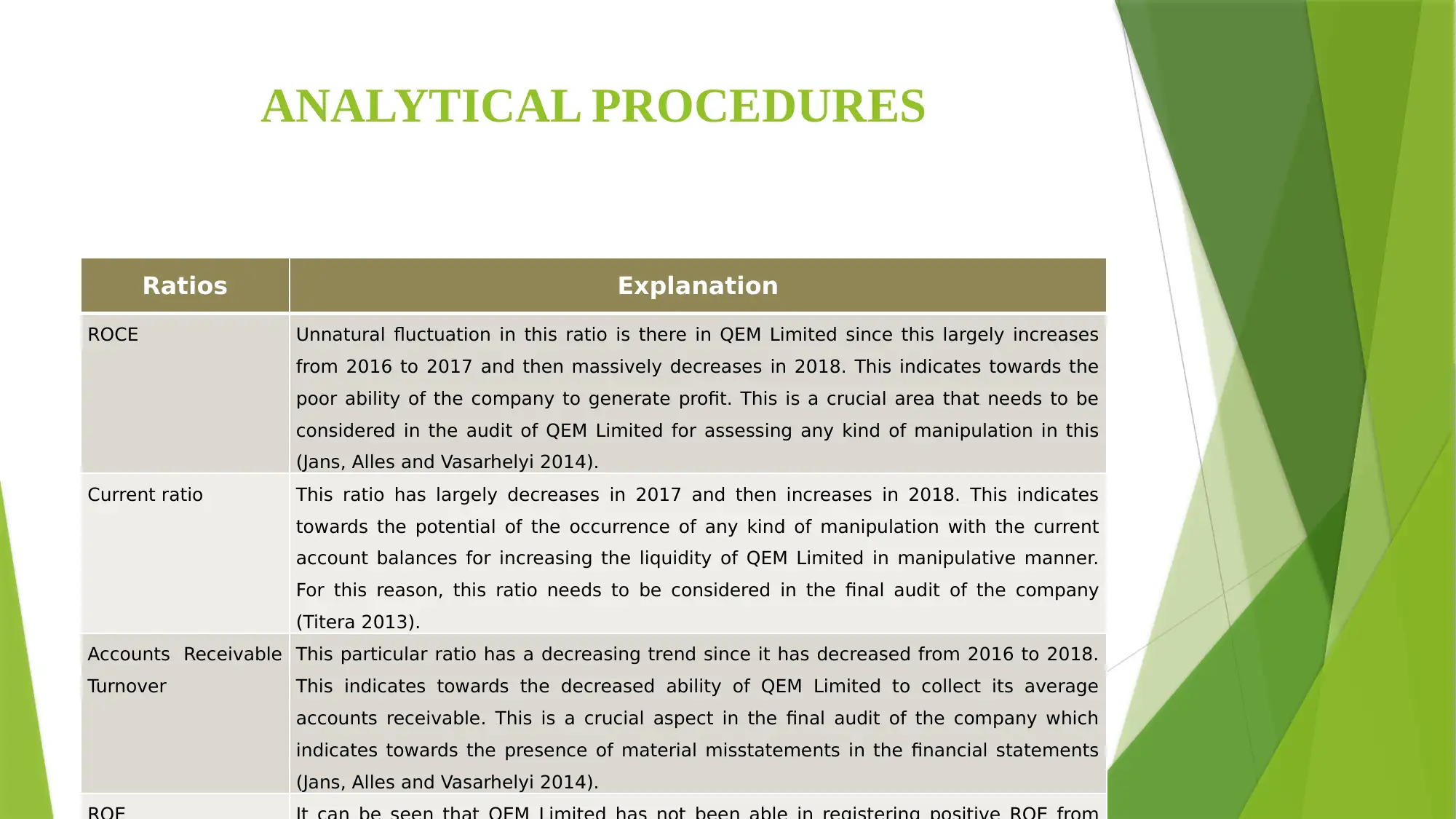

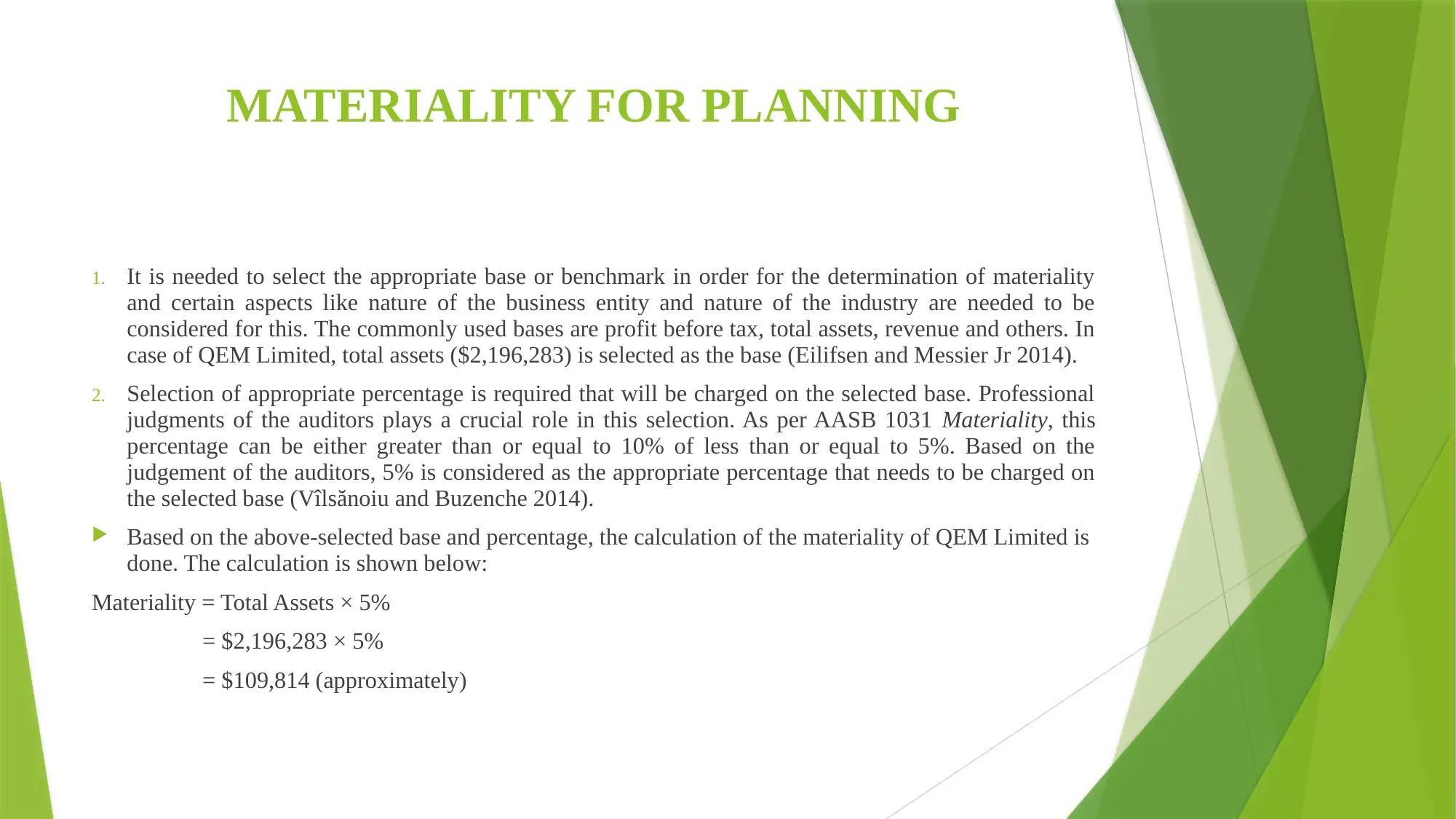

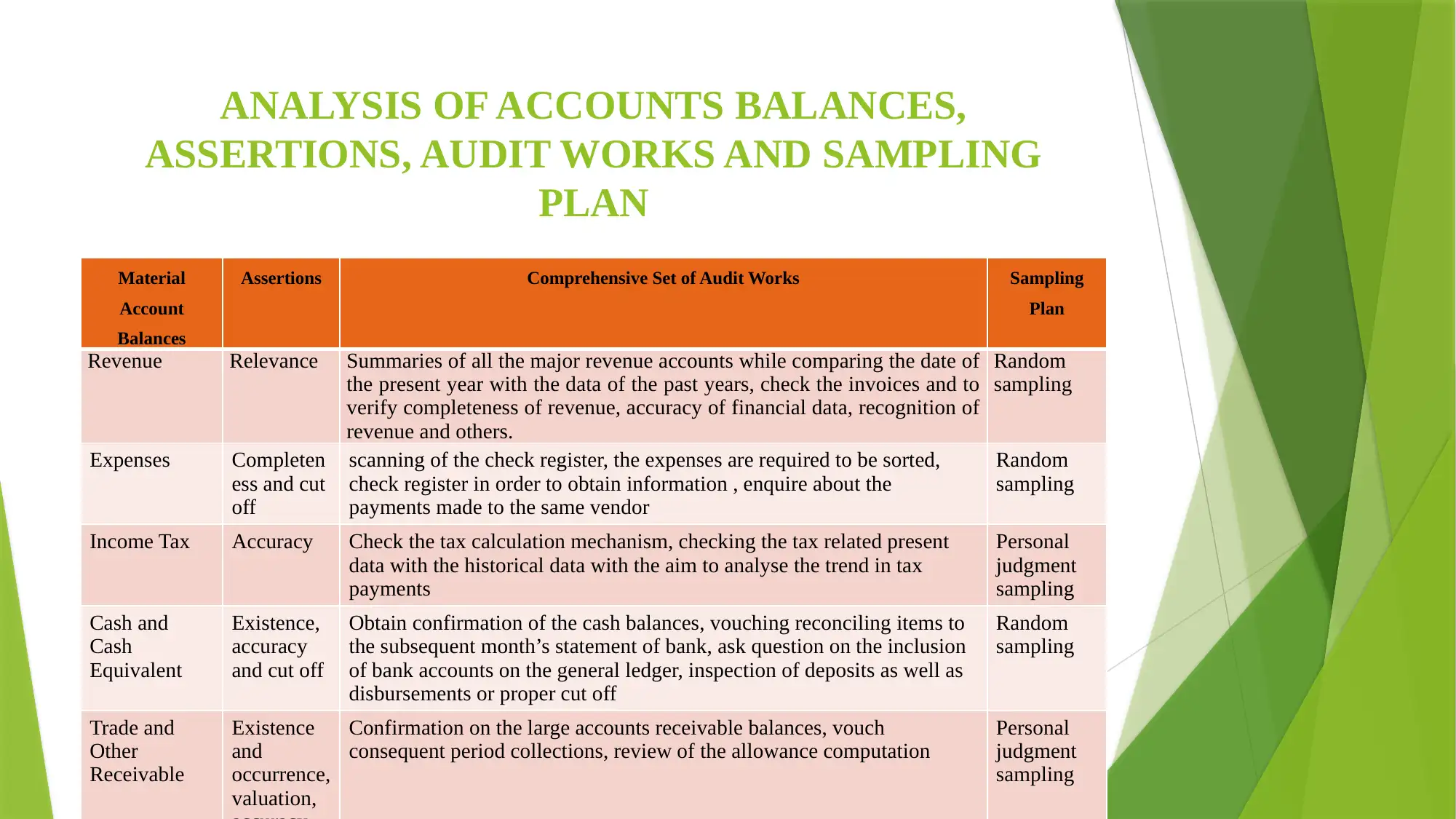

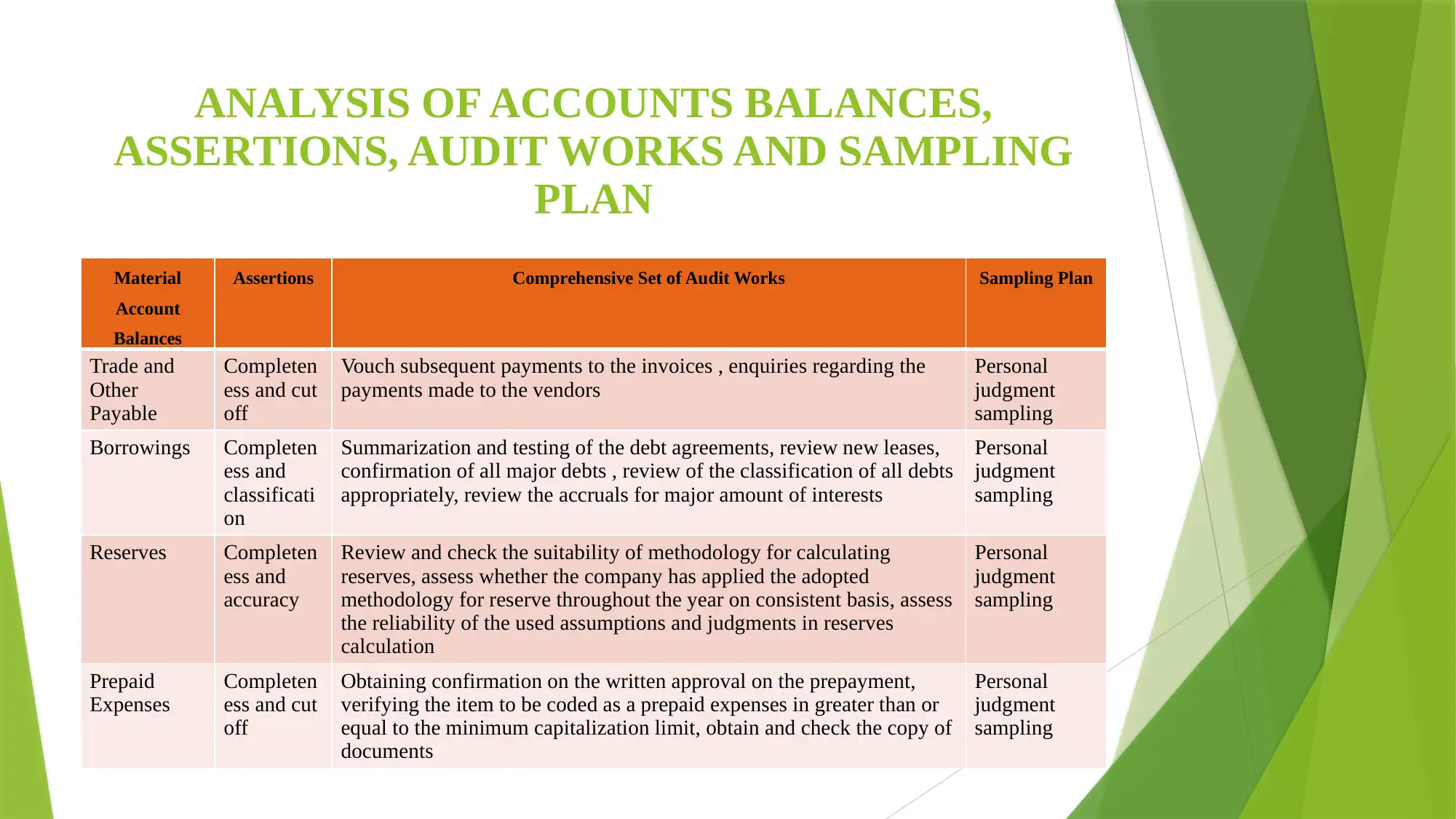

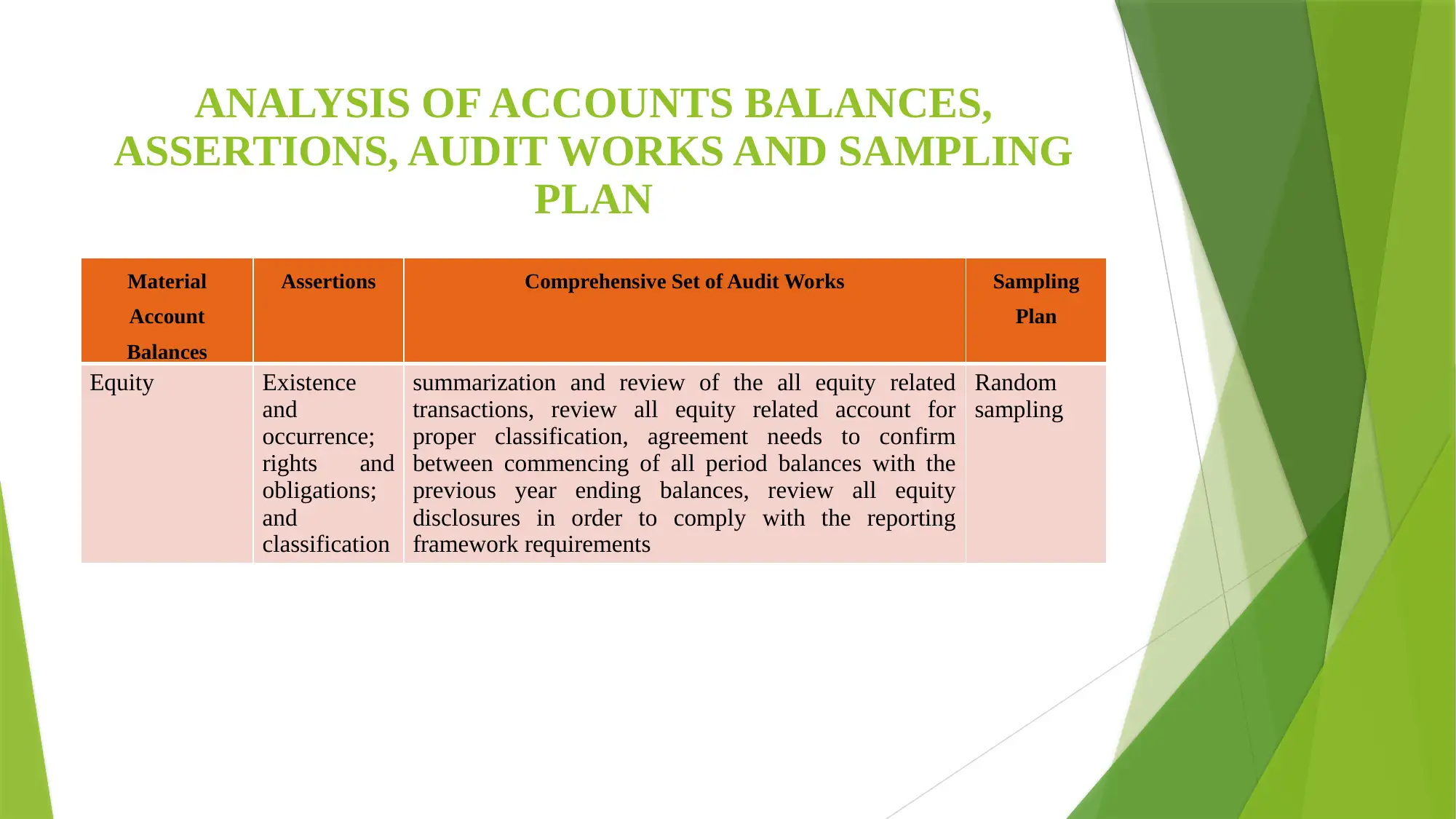

This report provides a comprehensive analysis of the auditing process for QEM Limited, an ASX-listed company in the energy sector. It begins with an introduction to auditing, emphasizing risk assessment and analytical procedures. The report then delves into the nature of QEM Limited, its business risks (operational, financial reporting, and compliance), and the application of the audit risk model to determine detection risk. Analytical procedures, including ratio analysis (ROCE, Current Ratio, Accounts Receivable Turnover, and ROE), are examined to identify potential material misstatements. The report also covers the determination of materiality, the selection of appropriate bases and percentages, and the calculation of materiality. Finally, it presents an analysis of account balances, audit assertions, audit works, and sampling plans for various accounts, including revenue, expenses, income tax, cash, receivables, payables, borrowings, reserves, prepaid expenses, and equity. The conclusion highlights the importance of understanding the audit client, applying audit risk models, and utilizing audit assertions and sampling processes to obtain sufficient audit evidence. The report references various auditing research papers to support its analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.