Auditing and Assurance: Analysis of Risk Factors at CBA Ltd. Bank

VerifiedAdded on 2020/05/28

|8

|1136

|48

Report

AI Summary

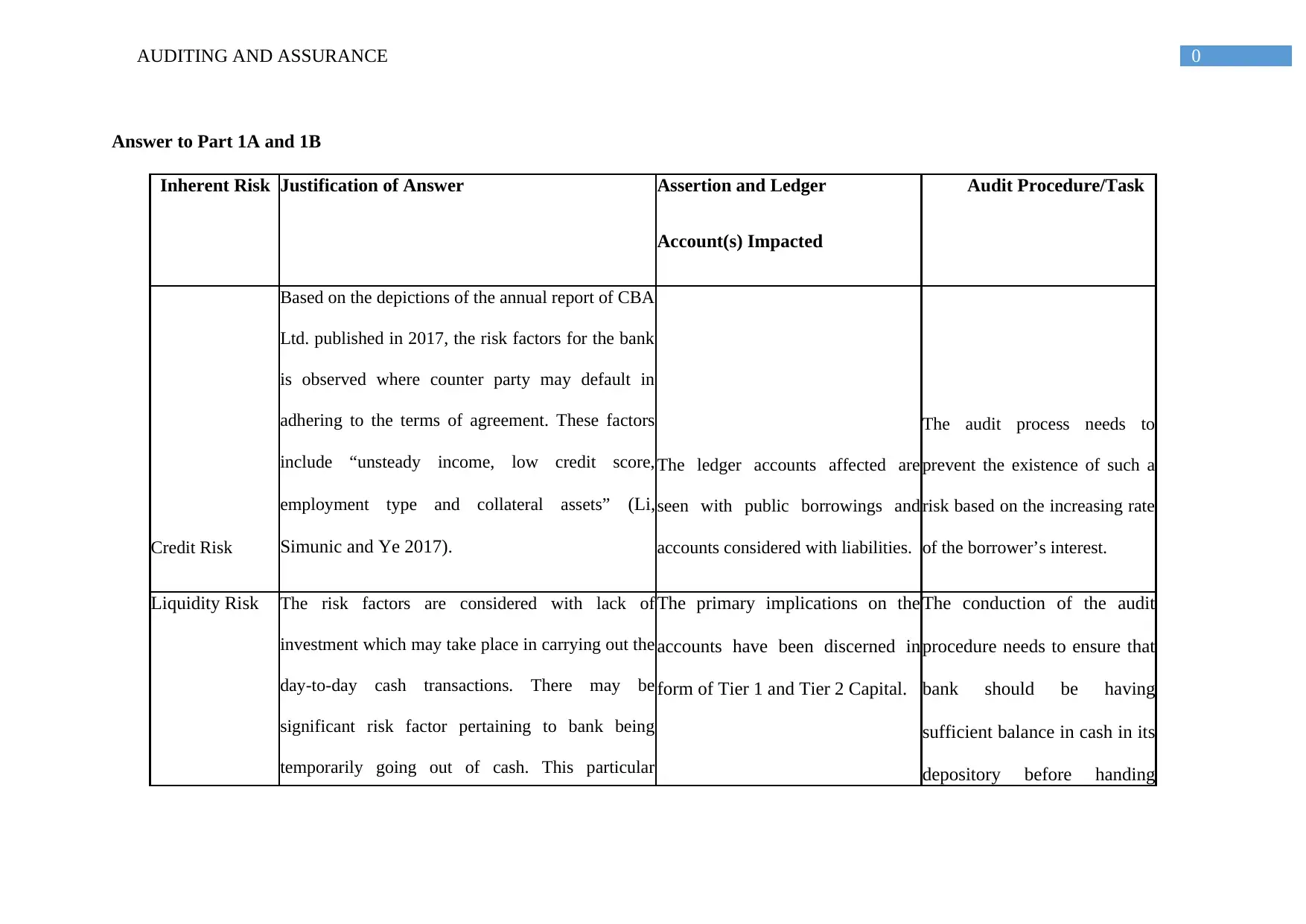

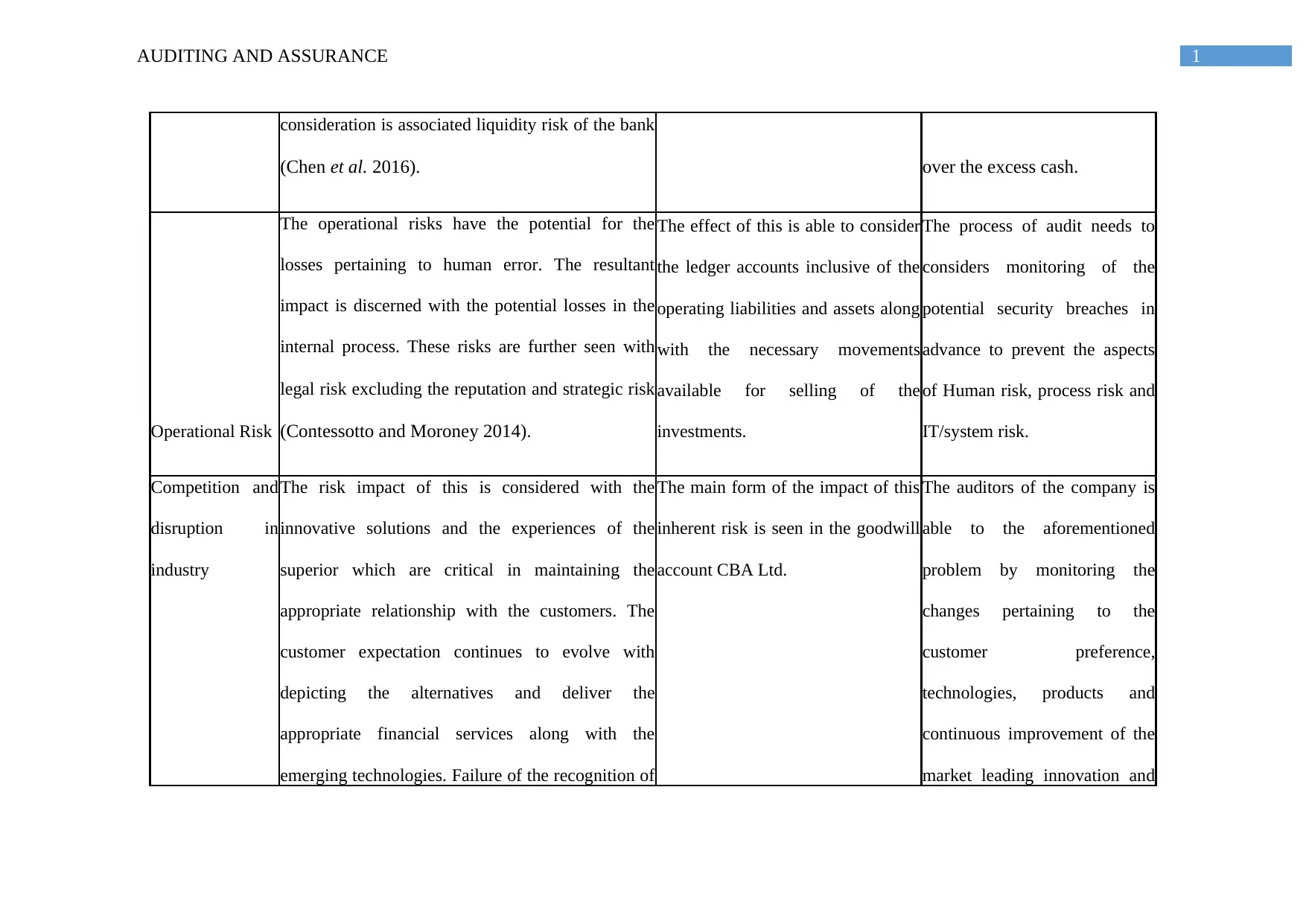

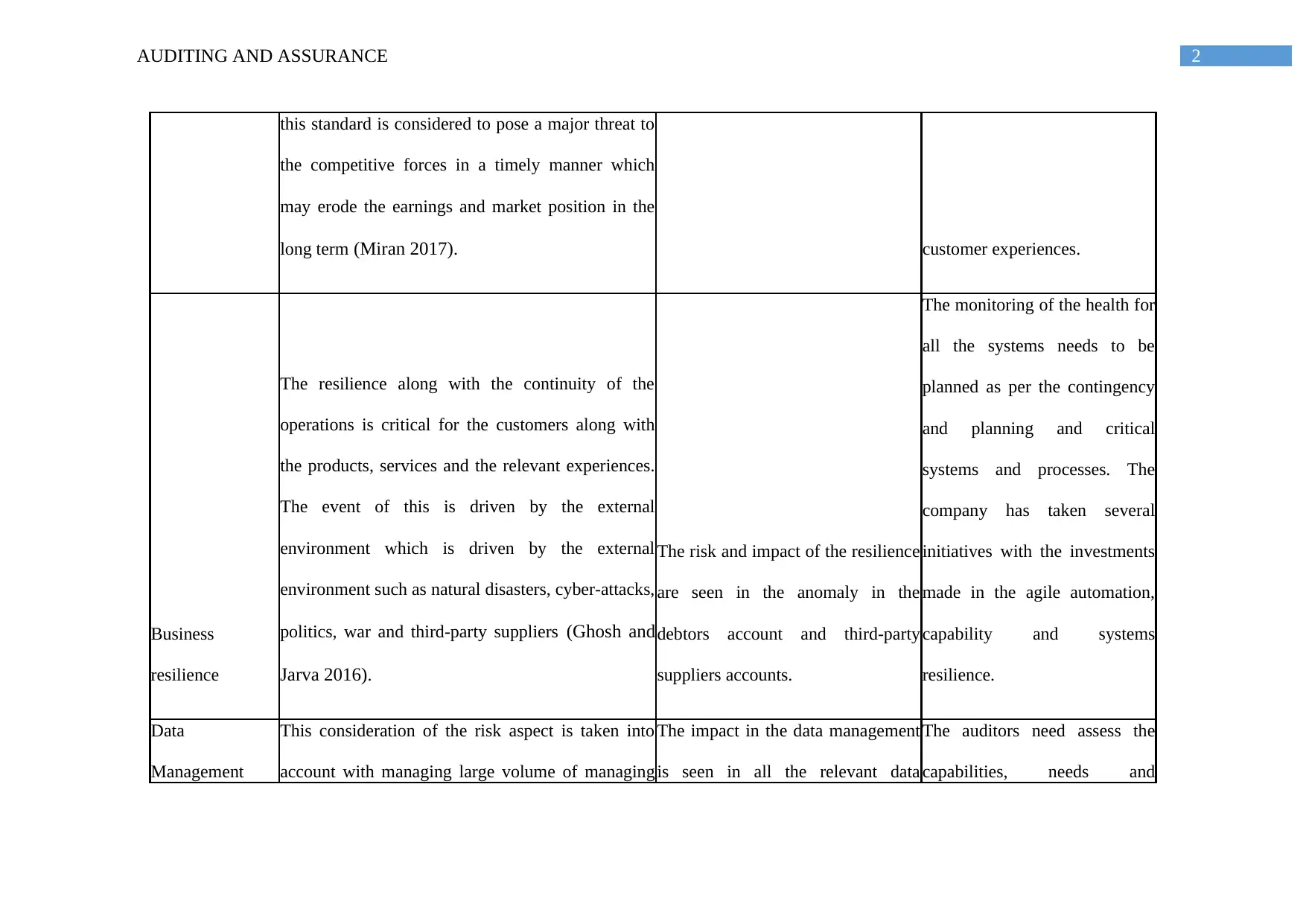

This report presents an analysis of the risk factors affecting CBA Ltd., focusing on key areas within auditing and assurance. The report identifies and explains various inherent risks, including credit risk, liquidity risk, operational risk, competition and disruption, business resilience, data management, and people capability. For each risk, the report outlines its potential impact on the bank's financial accounts, the relevant audit procedures, and the ledger accounts affected. The report also references several academic sources to support its analysis. The aim is to provide a comprehensive assessment of the risks faced by the bank and the corresponding audit strategies needed to mitigate these risks. This report offers insights into the auditing process and risk management within a financial institution.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.