ACCT 3004 Auditing Assessment Task Two: Crest Outfitters Audit Report

VerifiedAdded on 2023/06/08

|11

|2408

|494

Report

AI Summary

This report presents an auditing assessment for ACCT 3004, focusing on the preliminary risk assessment of Crest Outfitters. It delves into the client's background, organizational structure, and the use of foreign currency and leases. The report addresses inherent risks, including industry and economic factors, and assesses the client's financial performance measures. It examines the entity's internal control systems, including IT systems and documented business processes, and highlights the use of analytical procedures. The report further explores materiality, risk factors affecting the audit model, and the impact of opening a physical store in another country on the company's accounts. It details the components of internal control, including the control environment, risk assessment processes, control activities, and substantive audit procedures. The report also provides an overview of the audit evidence, including external confirmations, documentary, verbal, computational, physical, electronic, and data analytics evidence and details the audit procedures used for lease accounts.

ACCT 3004 Auditing

Assessment Task Two

Assessment Task Two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part 1: Preliminary risk assessment.................................................................................................3

Part 2: Materiality............................................................................................................................4

Risk factors affecting risk model & audit strategy......................................................................5

Part 3................................................................................................................................................6

Part 4................................................................................................................................................7

Part 5................................................................................................................................................7

Part 6................................................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

Part 1: Preliminary risk assessment.................................................................................................3

Part 2: Materiality............................................................................................................................4

Risk factors affecting risk model & audit strategy......................................................................5

Part 3................................................................................................................................................6

Part 4................................................................................................................................................7

Part 5................................................................................................................................................7

Part 6................................................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

Part 1: Preliminary risk assessment

Work paper ref: _A-002__

Prepared by: Tia

__RJ_____Hallafi_

Date prepared: 16/4/2020

Crest Outfitters

Audit for the year ending 30 June 2020

Preliminary assessment of risks of material misstatement

OBJECTIVES

Gaining an understanding of the client to determine the potential risk factors associated with material

misstatement due to error or fraud at the time of developing audit strategy.

Identification of risks associated with Crest Outfitters foreign currency and lease account.

CLIENT BACKGROUND INFORMATION

Organisational structure, ownership and governance

Who is the owner of the company? What type of corporate governance have been adopted by the

client (membership of board of directors, agency relationships or ownership concentration)?

Are there any board of directors who are independent, if Yes, how many?

How foreign currency is being used in the business what are the type of transactions and their volume

that are accomplished in foreign currency?

What is the model of the business? Does the business use leases extensively and whether there is any

security that has been kept on account of leases?

The Entity and Its Environment giving rise to inherent risk

Industry, regulatory and other factors

What are the government regulations applicable on the firm?

The industry from which the firm is associated with and the level of competition in it? Are there any

global standards required to be satisfied for this industry?

The current economic condition of the firm’s economy and how this could affect the firm?

How the foreign currency and movements therein could affect the performance of entity?

The item in which the entity is dealing, the nature of demand (trend or dependent), the nature of item

(luxury or essential)?

The possibility of occurrence of theft or fraud?

Work paper ref: _A-002__

Prepared by: Tia

__RJ_____Hallafi_

Date prepared: 16/4/2020

Crest Outfitters

Audit for the year ending 30 June 2020

Preliminary assessment of risks of material misstatement

OBJECTIVES

Gaining an understanding of the client to determine the potential risk factors associated with material

misstatement due to error or fraud at the time of developing audit strategy.

Identification of risks associated with Crest Outfitters foreign currency and lease account.

CLIENT BACKGROUND INFORMATION

Organisational structure, ownership and governance

Who is the owner of the company? What type of corporate governance have been adopted by the

client (membership of board of directors, agency relationships or ownership concentration)?

Are there any board of directors who are independent, if Yes, how many?

How foreign currency is being used in the business what are the type of transactions and their volume

that are accomplished in foreign currency?

What is the model of the business? Does the business use leases extensively and whether there is any

security that has been kept on account of leases?

The Entity and Its Environment giving rise to inherent risk

Industry, regulatory and other factors

What are the government regulations applicable on the firm?

The industry from which the firm is associated with and the level of competition in it? Are there any

global standards required to be satisfied for this industry?

The current economic condition of the firm’s economy and how this could affect the firm?

How the foreign currency and movements therein could affect the performance of entity?

The item in which the entity is dealing, the nature of demand (trend or dependent), the nature of item

(luxury or essential)?

The possibility of occurrence of theft or fraud?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Measures to assess financial performance

What information is required to be disclosed publicly?

What is the position of entity among other players of the industry?

What procedures or policies have been adopted with respect to the remuneration of staff?

What is the level of training and qualification does the accounting staff hold?

The Applicable Financial Reporting Framework

What are the estimates and policies used by the entity in its accounting procedure could affect its

audit risk?

What else accounting standards must be complied to by the entity?

Does the company trades publicly in one or more jurisdiction?

Obtaining an Understanding of the Entity’s System of Internal Control

What IT systems are used to support the entity’s business?

Does the entity have documented business processes and procedures?

The reasons for which the analytical procedures are used during risk assessment involves the

following:

These procedures are considered to be more effective as well as efficient as compared to tests

concerning the reduction of risk of material misstatements both at the assertion and

acceptably low level. It further facilitates the determination of the cause of risk of material

misstatement that is, whether it has happened due to fraud or error (Voss and Carter, 2021).

Part 2: Materiality

The preliminary assessment which is also referred to as the risk assessment phase involves

involve one of the initial step while conducting audit. Therefore, it has a significant relationship

with the identification of risk associated with materiality because the background information

concerning the client could be obtained only through preliminary assessment and this in turn

could facilitate the determination of materiality thresholds in order to ensure reasonable

What information is required to be disclosed publicly?

What is the position of entity among other players of the industry?

What procedures or policies have been adopted with respect to the remuneration of staff?

What is the level of training and qualification does the accounting staff hold?

The Applicable Financial Reporting Framework

What are the estimates and policies used by the entity in its accounting procedure could affect its

audit risk?

What else accounting standards must be complied to by the entity?

Does the company trades publicly in one or more jurisdiction?

Obtaining an Understanding of the Entity’s System of Internal Control

What IT systems are used to support the entity’s business?

Does the entity have documented business processes and procedures?

The reasons for which the analytical procedures are used during risk assessment involves the

following:

These procedures are considered to be more effective as well as efficient as compared to tests

concerning the reduction of risk of material misstatements both at the assertion and

acceptably low level. It further facilitates the determination of the cause of risk of material

misstatement that is, whether it has happened due to fraud or error (Voss and Carter, 2021).

Part 2: Materiality

The preliminary assessment which is also referred to as the risk assessment phase involves

involve one of the initial step while conducting audit. Therefore, it has a significant relationship

with the identification of risk associated with materiality because the background information

concerning the client could be obtained only through preliminary assessment and this in turn

could facilitate the determination of materiality thresholds in order to ensure reasonable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assurance. This is turn indicates that there is no significant impact of material misstatement over

the usability of Crest outfitters financial statements.

Risks of material misstatement

Risk can be found to be materially misstated both on financial statement level as well as the

assertion level (O'Connell and et.al., 2020). The risk of material misstatement arising at financial

statement level involves certain risks that could affect the entire financial statement or potentially

having effect over several assertions. It has the potentiality of hindering auditor’s ability in

giving unqualified audit opinion.

The factors due to which risk of material misstatement arises at financial statement level are as

follows:

Improper oversight by the BODs.

Incompetency of management

Inadequacy of records & accounting systems

Poor economic and industrial conditions.

GAAP makes it necessary for the auditor to assess the risk associated with material misstatement

at the assertion level which is composed of control and inherent risk.

With respect to the Crest outfitters, the risk of material misstatement could arise at the time of

foreign currency transactions while recognizing or exchanging gains or losses associated with it.

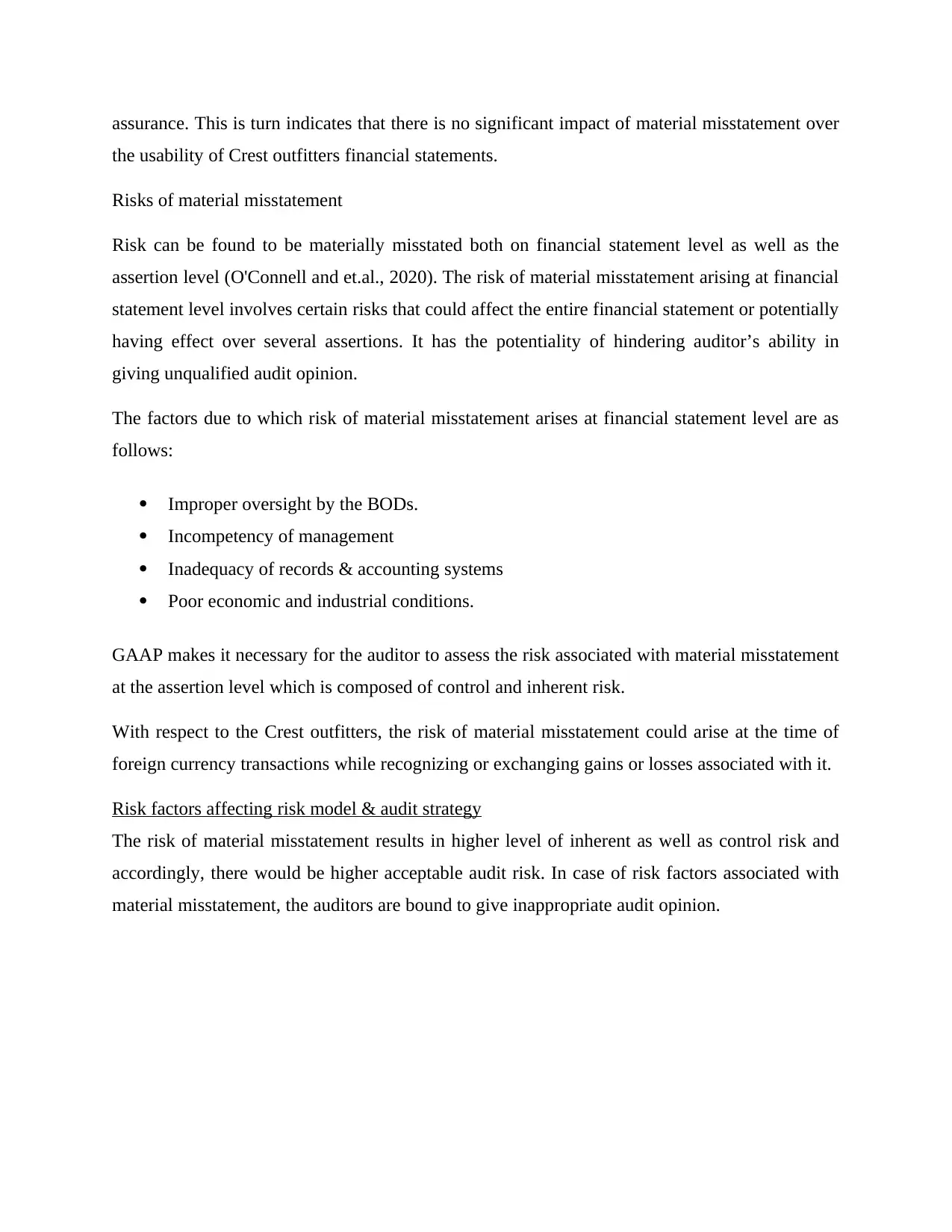

Risk factors affecting risk model & audit strategy

The risk of material misstatement results in higher level of inherent as well as control risk and

accordingly, there would be higher acceptable audit risk. In case of risk factors associated with

material misstatement, the auditors are bound to give inappropriate audit opinion.

the usability of Crest outfitters financial statements.

Risks of material misstatement

Risk can be found to be materially misstated both on financial statement level as well as the

assertion level (O'Connell and et.al., 2020). The risk of material misstatement arising at financial

statement level involves certain risks that could affect the entire financial statement or potentially

having effect over several assertions. It has the potentiality of hindering auditor’s ability in

giving unqualified audit opinion.

The factors due to which risk of material misstatement arises at financial statement level are as

follows:

Improper oversight by the BODs.

Incompetency of management

Inadequacy of records & accounting systems

Poor economic and industrial conditions.

GAAP makes it necessary for the auditor to assess the risk associated with material misstatement

at the assertion level which is composed of control and inherent risk.

With respect to the Crest outfitters, the risk of material misstatement could arise at the time of

foreign currency transactions while recognizing or exchanging gains or losses associated with it.

Risk factors affecting risk model & audit strategy

The risk of material misstatement results in higher level of inherent as well as control risk and

accordingly, there would be higher acceptable audit risk. In case of risk factors associated with

material misstatement, the auditors are bound to give inappropriate audit opinion.

Part 3

With regards to the case of Crest Outfitters there will be an effect being created on the

accounts and business then they decided to open the physical store. This will be created by the

company because of the reason that when the company will be going to another country then all

the accounting requirements will be changed and so the auditing will also be changed. In case the

company will be selling its products and services in another country then they will be treated in

different manner (Byrne, Anda and Ho, 2019). This is particularly because of the reason that

Crest Outfitters will have to comply with the accounting and auditing standard of that country

only. The major effect of this on the income and the accounts of Crest Outfitters will be on the

recording of the business transaction. This is particularly because of the reason that when the

company will not be complying with the requirement of accounting and auditing standard of

every country is different and it takes a lot of time in managing the work in better and effective

manner. In case the goods and services are being sold at the beginning of the year then it will be

recorded in the same manner and this will be audited along with the other account at the end of

the year.

With regards to the case of Crest Outfitters there will be an effect being created on the

accounts and business then they decided to open the physical store. This will be created by the

company because of the reason that when the company will be going to another country then all

the accounting requirements will be changed and so the auditing will also be changed. In case the

company will be selling its products and services in another country then they will be treated in

different manner (Byrne, Anda and Ho, 2019). This is particularly because of the reason that

Crest Outfitters will have to comply with the accounting and auditing standard of that country

only. The major effect of this on the income and the accounts of Crest Outfitters will be on the

recording of the business transaction. This is particularly because of the reason that when the

company will not be complying with the requirement of accounting and auditing standard of

every country is different and it takes a lot of time in managing the work in better and effective

manner. In case the goods and services are being sold at the beginning of the year then it will be

recorded in the same manner and this will be audited along with the other account at the end of

the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 4

Sufficient appropriate evidence must be present at the time of auditing. Sufficiency can be

described in terms of appropriateness as well as the quantity of evidences.

External confirmations: here confirmation is obtained from third party with regards to the matter

included in confirmation letter. For instance, bank reconciliation statement.

Documentary evidences: It includes invoices, minutes of meetings, supplier’s and bank

statement, etc. these are third party generated evidences used during auditing (Malone and et.al.,

2018).

Representations: Specific consideration for claims as well as litigation required auditor to gather

representation letter from the lawyers of the client as an audit evidence.

Verbal evidence: It is required while gaining an understanding of the client itself or its internal

control system.

Computational evidence: It is required for checking the mathematical accuracy of the financial

reports. In case of Crest outfitters, it could be used to determine whether the translation has been

done accurately.

Physical evidence: Such evidence is obtained through the inspection of tangible assets held with

the client.

Electronic evidence: It involves evidences generated through accounting software and other

electronic transactions giving rise to financial event.

Data analytics: It is the evidence obtained by the auditor through analyzing financial records of

the client.

All these are the sources of evidences that auditor evaluates while performing control and

substantive testing. They perform evaluation by taking sample of evidences where the size of

sample depends on several factors such as the extent of control that the auditor establishes,

tolerance for deviation or misstatement, etc. all this led to increase or decrease in the size of

sample (Eltweri, 2021).

Sufficient appropriate evidence must be present at the time of auditing. Sufficiency can be

described in terms of appropriateness as well as the quantity of evidences.

External confirmations: here confirmation is obtained from third party with regards to the matter

included in confirmation letter. For instance, bank reconciliation statement.

Documentary evidences: It includes invoices, minutes of meetings, supplier’s and bank

statement, etc. these are third party generated evidences used during auditing (Malone and et.al.,

2018).

Representations: Specific consideration for claims as well as litigation required auditor to gather

representation letter from the lawyers of the client as an audit evidence.

Verbal evidence: It is required while gaining an understanding of the client itself or its internal

control system.

Computational evidence: It is required for checking the mathematical accuracy of the financial

reports. In case of Crest outfitters, it could be used to determine whether the translation has been

done accurately.

Physical evidence: Such evidence is obtained through the inspection of tangible assets held with

the client.

Electronic evidence: It involves evidences generated through accounting software and other

electronic transactions giving rise to financial event.

Data analytics: It is the evidence obtained by the auditor through analyzing financial records of

the client.

All these are the sources of evidences that auditor evaluates while performing control and

substantive testing. They perform evaluation by taking sample of evidences where the size of

sample depends on several factors such as the extent of control that the auditor establishes,

tolerance for deviation or misstatement, etc. all this led to increase or decrease in the size of

sample (Eltweri, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 5

Components of internal control

At the time of control risk assessment, auditor is required to evaluate risks of material

misstatement, enquiry of individuals and management personnel involved in internal audit

function, analytical procedures, etc (Hoque and Thiagarajah, 2022).

Control environment must be evaluated that is associated with the preparation of financial report.

Management communicates & enforces integrity & ethical values –

reduce incentives, pressures & opportunity that tempt staff to act dishonestly, illegally

Management set example by following code of good conduct

Commitment to competence – continued staff training

Participation of those charged with governance (CEO / Board/Audit committee)

Management philosophy & operating style – are they risk takers?

Assignment of authority & responsibility

Organisational structure

Human resources policy

Entity risk assessment process: It involves identification of risks associated with foreign currency

& leases, significance of that risk and addressing that risk.

Entity’s process to monitor the quality of control: It involves identification of effectiveness of

controls and remediation of control deficiencies.

IT & related processes and communication in business: It involves activities related to

information processing in entity and resources, policies & disclosures associated with it.

Control activities: It involves authorization, performance reviews, information processing,

physical controls and segregation of duties.

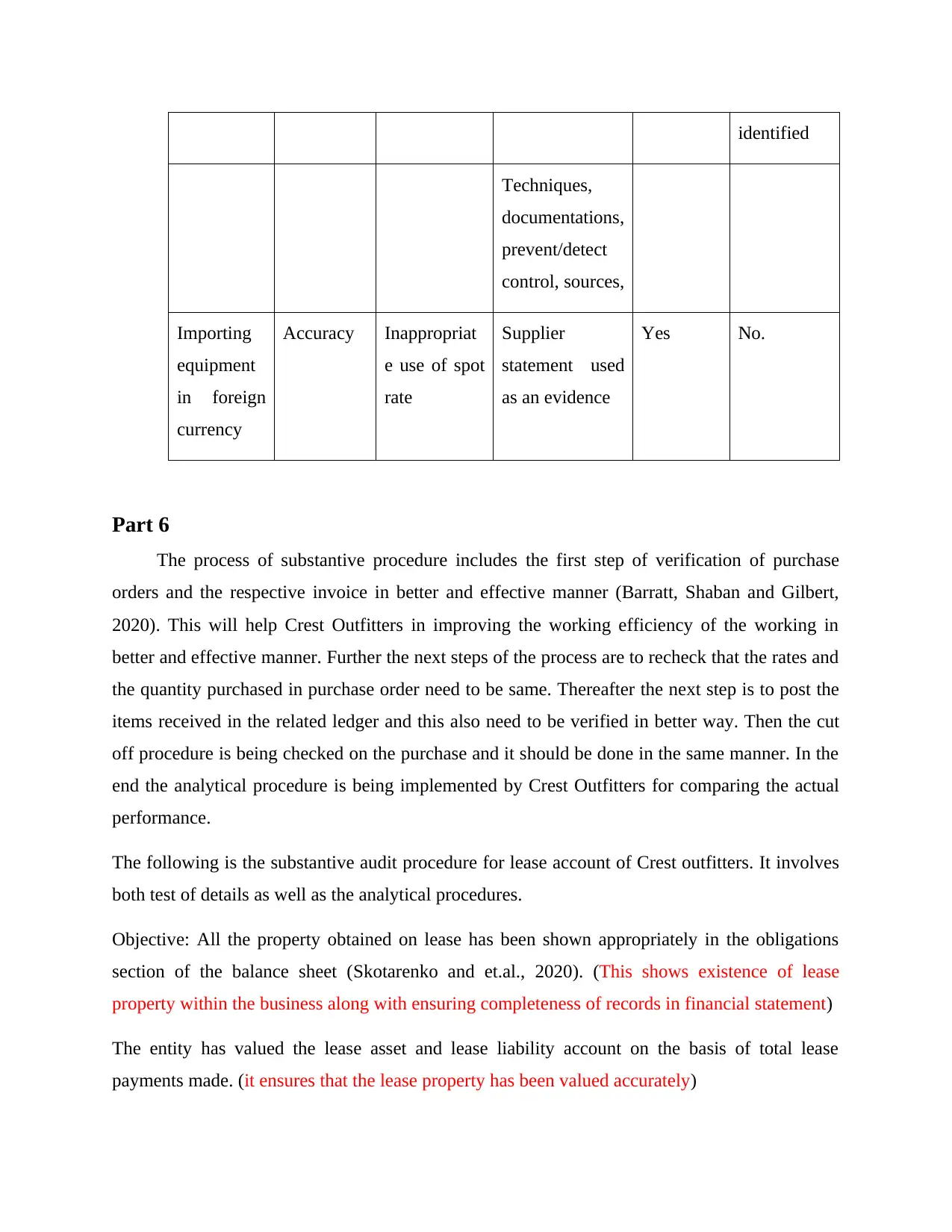

With reference to Crest outfitters, the following would be done for testing controls:

transaction

s

Objectives

/assertions

WCGW Controls/steps Performed

Y/N

Has fraud

been

Components of internal control

At the time of control risk assessment, auditor is required to evaluate risks of material

misstatement, enquiry of individuals and management personnel involved in internal audit

function, analytical procedures, etc (Hoque and Thiagarajah, 2022).

Control environment must be evaluated that is associated with the preparation of financial report.

Management communicates & enforces integrity & ethical values –

reduce incentives, pressures & opportunity that tempt staff to act dishonestly, illegally

Management set example by following code of good conduct

Commitment to competence – continued staff training

Participation of those charged with governance (CEO / Board/Audit committee)

Management philosophy & operating style – are they risk takers?

Assignment of authority & responsibility

Organisational structure

Human resources policy

Entity risk assessment process: It involves identification of risks associated with foreign currency

& leases, significance of that risk and addressing that risk.

Entity’s process to monitor the quality of control: It involves identification of effectiveness of

controls and remediation of control deficiencies.

IT & related processes and communication in business: It involves activities related to

information processing in entity and resources, policies & disclosures associated with it.

Control activities: It involves authorization, performance reviews, information processing,

physical controls and segregation of duties.

With reference to Crest outfitters, the following would be done for testing controls:

transaction

s

Objectives

/assertions

WCGW Controls/steps Performed

Y/N

Has fraud

been

identified

Techniques,

documentations,

prevent/detect

control, sources,

Importing

equipment

in foreign

currency

Accuracy Inappropriat

e use of spot

rate

Supplier

statement used

as an evidence

Yes No.

Part 6

The process of substantive procedure includes the first step of verification of purchase

orders and the respective invoice in better and effective manner (Barratt, Shaban and Gilbert,

2020). This will help Crest Outfitters in improving the working efficiency of the working in

better and effective manner. Further the next steps of the process are to recheck that the rates and

the quantity purchased in purchase order need to be same. Thereafter the next step is to post the

items received in the related ledger and this also need to be verified in better way. Then the cut

off procedure is being checked on the purchase and it should be done in the same manner. In the

end the analytical procedure is being implemented by Crest Outfitters for comparing the actual

performance.

The following is the substantive audit procedure for lease account of Crest outfitters. It involves

both test of details as well as the analytical procedures.

Objective: All the property obtained on lease has been shown appropriately in the obligations

section of the balance sheet (Skotarenko and et.al., 2020). (This shows existence of lease

property within the business along with ensuring completeness of records in financial statement)

The entity has valued the lease asset and lease liability account on the basis of total lease

payments made. (it ensures that the lease property has been valued accurately)

Techniques,

documentations,

prevent/detect

control, sources,

Importing

equipment

in foreign

currency

Accuracy Inappropriat

e use of spot

rate

Supplier

statement used

as an evidence

Yes No.

Part 6

The process of substantive procedure includes the first step of verification of purchase

orders and the respective invoice in better and effective manner (Barratt, Shaban and Gilbert,

2020). This will help Crest Outfitters in improving the working efficiency of the working in

better and effective manner. Further the next steps of the process are to recheck that the rates and

the quantity purchased in purchase order need to be same. Thereafter the next step is to post the

items received in the related ledger and this also need to be verified in better way. Then the cut

off procedure is being checked on the purchase and it should be done in the same manner. In the

end the analytical procedure is being implemented by Crest Outfitters for comparing the actual

performance.

The following is the substantive audit procedure for lease account of Crest outfitters. It involves

both test of details as well as the analytical procedures.

Objective: All the property obtained on lease has been shown appropriately in the obligations

section of the balance sheet (Skotarenko and et.al., 2020). (This shows existence of lease

property within the business along with ensuring completeness of records in financial statement)

The entity has valued the lease asset and lease liability account on the basis of total lease

payments made. (it ensures that the lease property has been valued accurately)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Crest outfitters has the right to use to use the leased asset on an agreed term. (By ensuring

so, it could be determined that Crest outfitters have rights & obligations to use the asset)

Disclosures related to the leases account have been appropriately made in the notes on the basis

of applicable accounting principles. (Auditors here ensures that the assets & liabilities associated

with leases have been appropriately classified and detailed explanation for their treatment and

recognition have been given).

It is all about substantive procedure with reference to the lease account of Crest outfitters

through which test of details and analytical procedures are being done by the auditor of several

financial records.

so, it could be determined that Crest outfitters have rights & obligations to use the asset)

Disclosures related to the leases account have been appropriately made in the notes on the basis

of applicable accounting principles. (Auditors here ensures that the assets & liabilities associated

with leases have been appropriately classified and detailed explanation for their treatment and

recognition have been given).

It is all about substantive procedure with reference to the lease account of Crest outfitters

through which test of details and analytical procedures are being done by the auditor of several

financial records.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Barratt, R., Shaban, R.Z. and Gilbert, G.L., 2020. Characteristics of personal protective

equipment training programs in Australia and New Zealand hospitals: A survey. Infection,

disease & health, 25(4), pp.253-261.

Byrne, J.J., Anda, M. and Ho, G.E., 2019. Water sustainable house: Water auditing of 3 case

studies in Perth, Western Australia. Water Practice and Technology, 14(2), pp.435-443.

Eltweri, A., 2021. The Blockchain Impact on the Current Auditing Standards.

Hoque, Z. and Thiagarajah, T., 2022. Local Government Auditing in Australia. In Auditing

Practices in Local Governments: An International Comparison (pp. 13-26). Emerald

Publishing Limited.

Malone, B., and et.al., 2018. Auditing on-farm soil carbon stocks using downscaled national

mapping products: Examples from Australia and New Zealand. Geoderma regional, 13,

pp.1-14.

O'Connell, B.T., and et.al., 2020. Impact of research assessment exercises on research

approaches and foci of accounting disciplines in Australia. Accounting, Auditing &

Accountability Journal, 33(6), pp.1277-1302.

Skotarenko, O., and et.al., 2020. The application of auditing internal standards for strengthen

positions in the accounting outsourcing services market. European Journal of Molecular

& Clinical Medicine, 7(2), p.2020.

Voss, B. and Carter, D., Regulation of auditing in Australia.

Books and Journals

Barratt, R., Shaban, R.Z. and Gilbert, G.L., 2020. Characteristics of personal protective

equipment training programs in Australia and New Zealand hospitals: A survey. Infection,

disease & health, 25(4), pp.253-261.

Byrne, J.J., Anda, M. and Ho, G.E., 2019. Water sustainable house: Water auditing of 3 case

studies in Perth, Western Australia. Water Practice and Technology, 14(2), pp.435-443.

Eltweri, A., 2021. The Blockchain Impact on the Current Auditing Standards.

Hoque, Z. and Thiagarajah, T., 2022. Local Government Auditing in Australia. In Auditing

Practices in Local Governments: An International Comparison (pp. 13-26). Emerald

Publishing Limited.

Malone, B., and et.al., 2018. Auditing on-farm soil carbon stocks using downscaled national

mapping products: Examples from Australia and New Zealand. Geoderma regional, 13,

pp.1-14.

O'Connell, B.T., and et.al., 2020. Impact of research assessment exercises on research

approaches and foci of accounting disciplines in Australia. Accounting, Auditing &

Accountability Journal, 33(6), pp.1277-1302.

Skotarenko, O., and et.al., 2020. The application of auditing internal standards for strengthen

positions in the accounting outsourcing services market. European Journal of Molecular

& Clinical Medicine, 7(2), p.2020.

Voss, B. and Carter, D., Regulation of auditing in Australia.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.