Auditing Report: ISA 260 Communication, Audit Risks in Tuck Co.

VerifiedAdded on 2020/11/23

|10

|2427

|74

Report

AI Summary

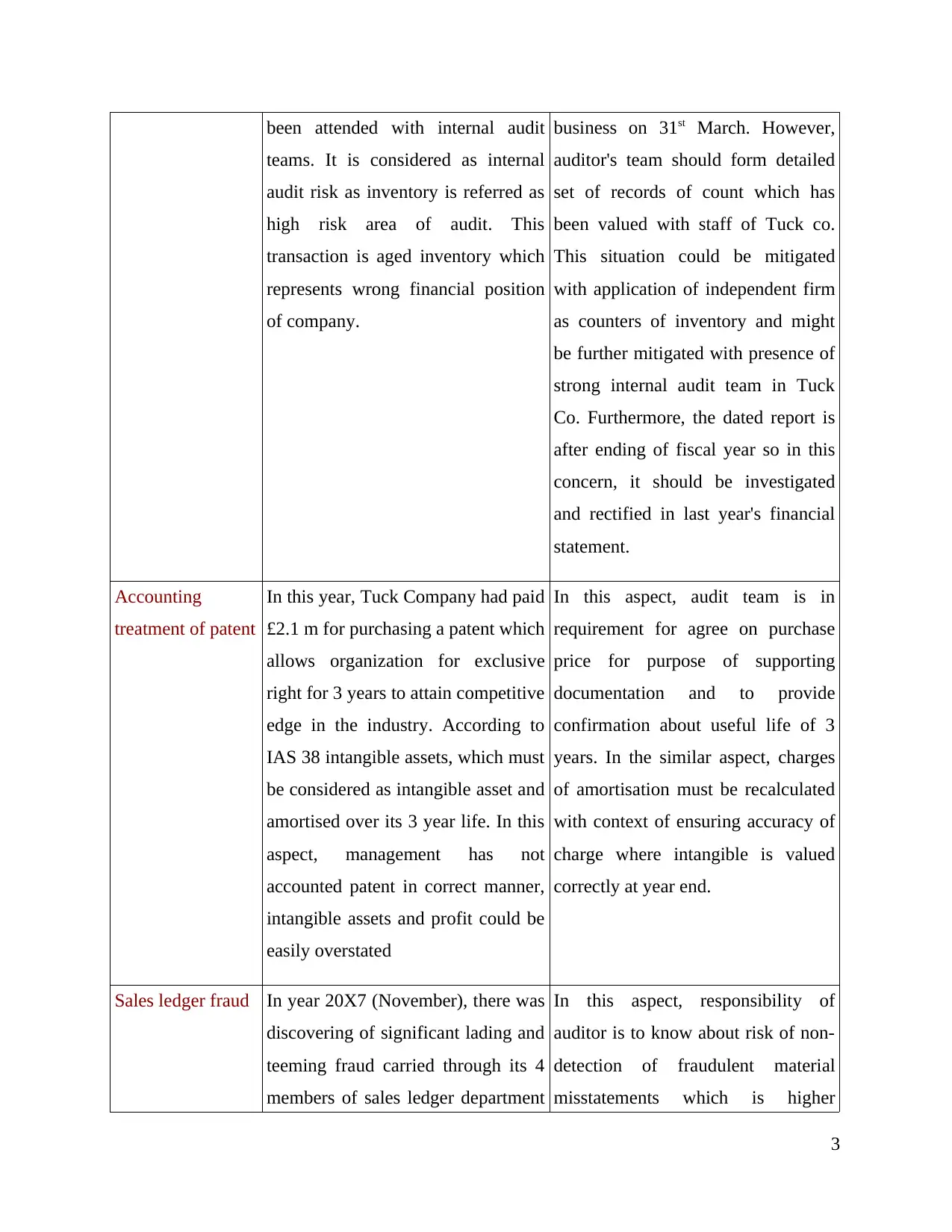

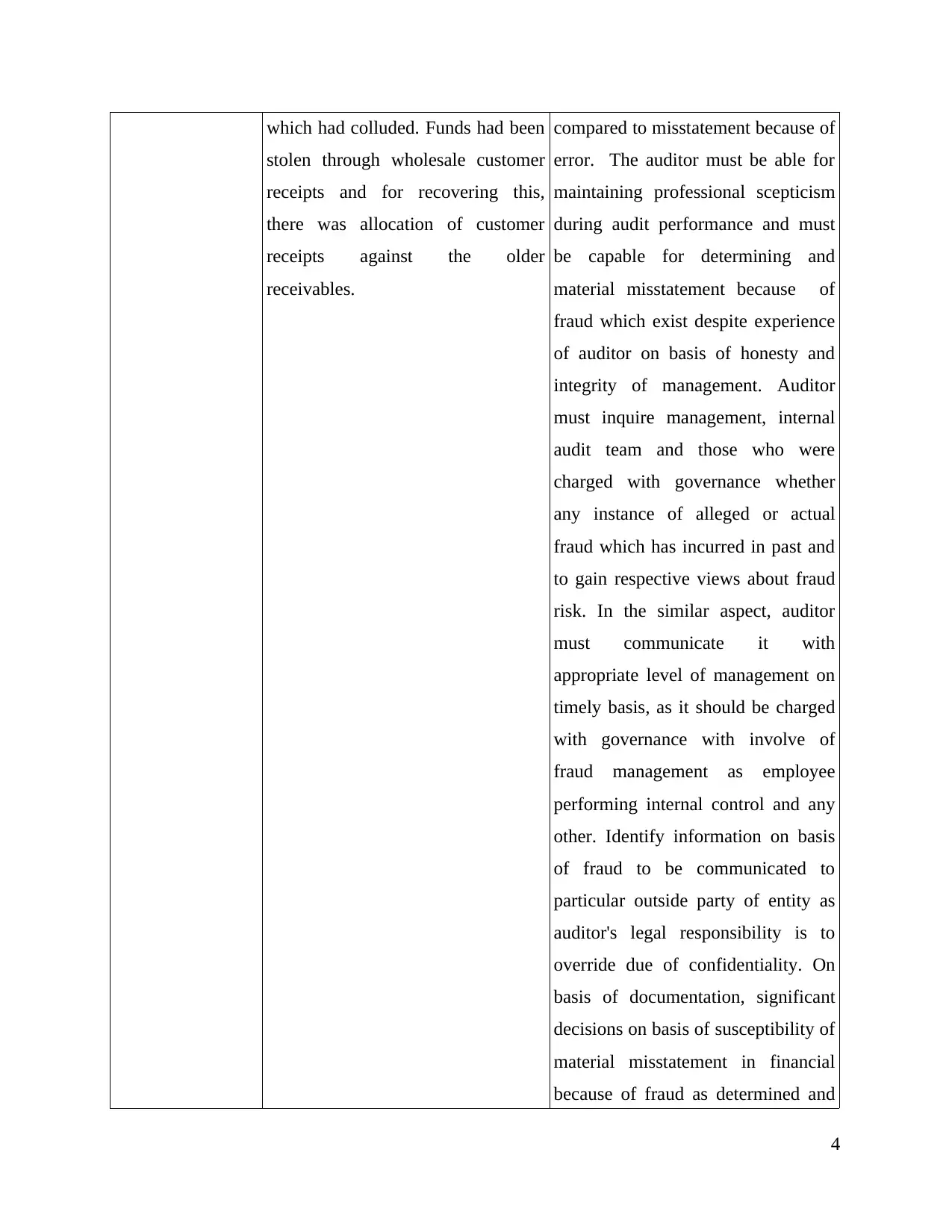

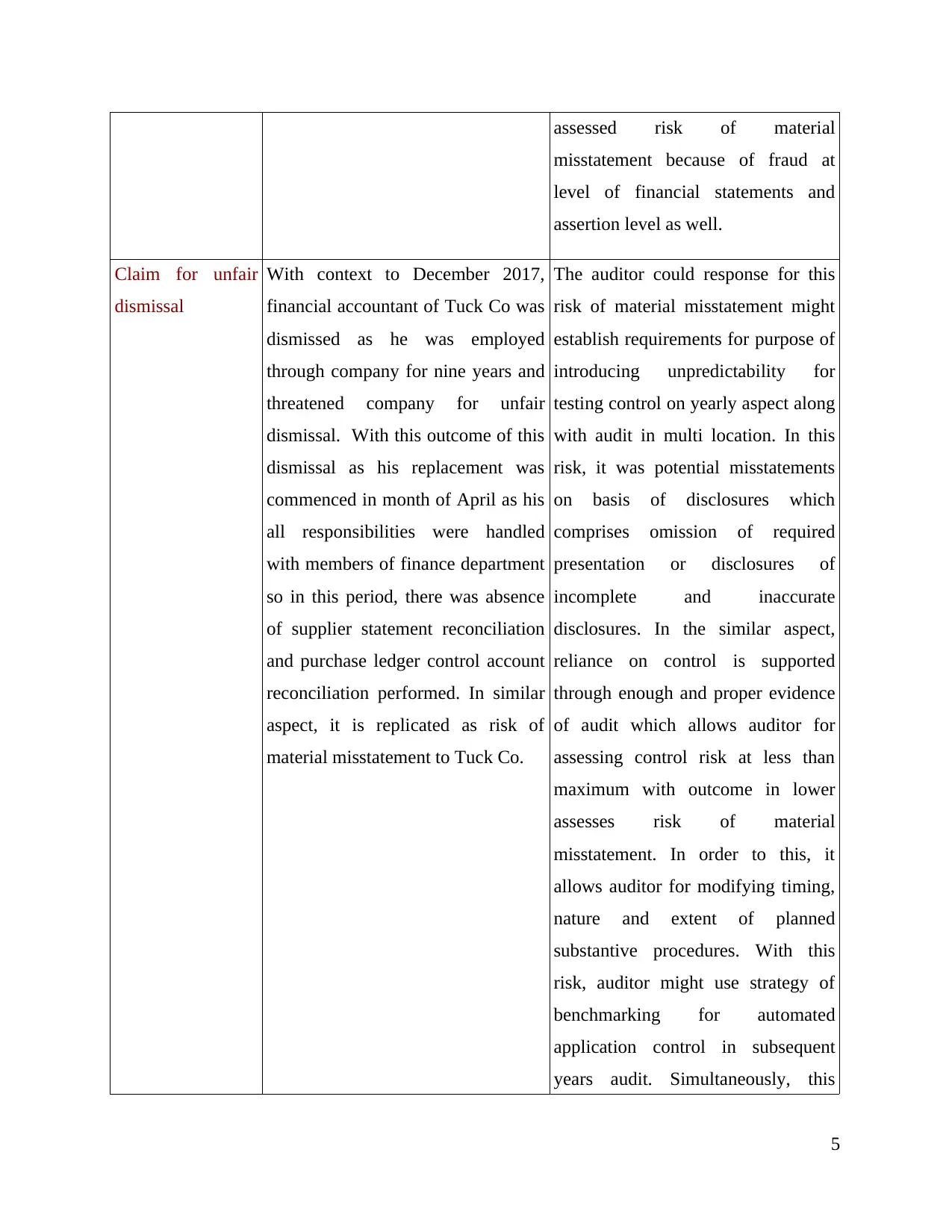

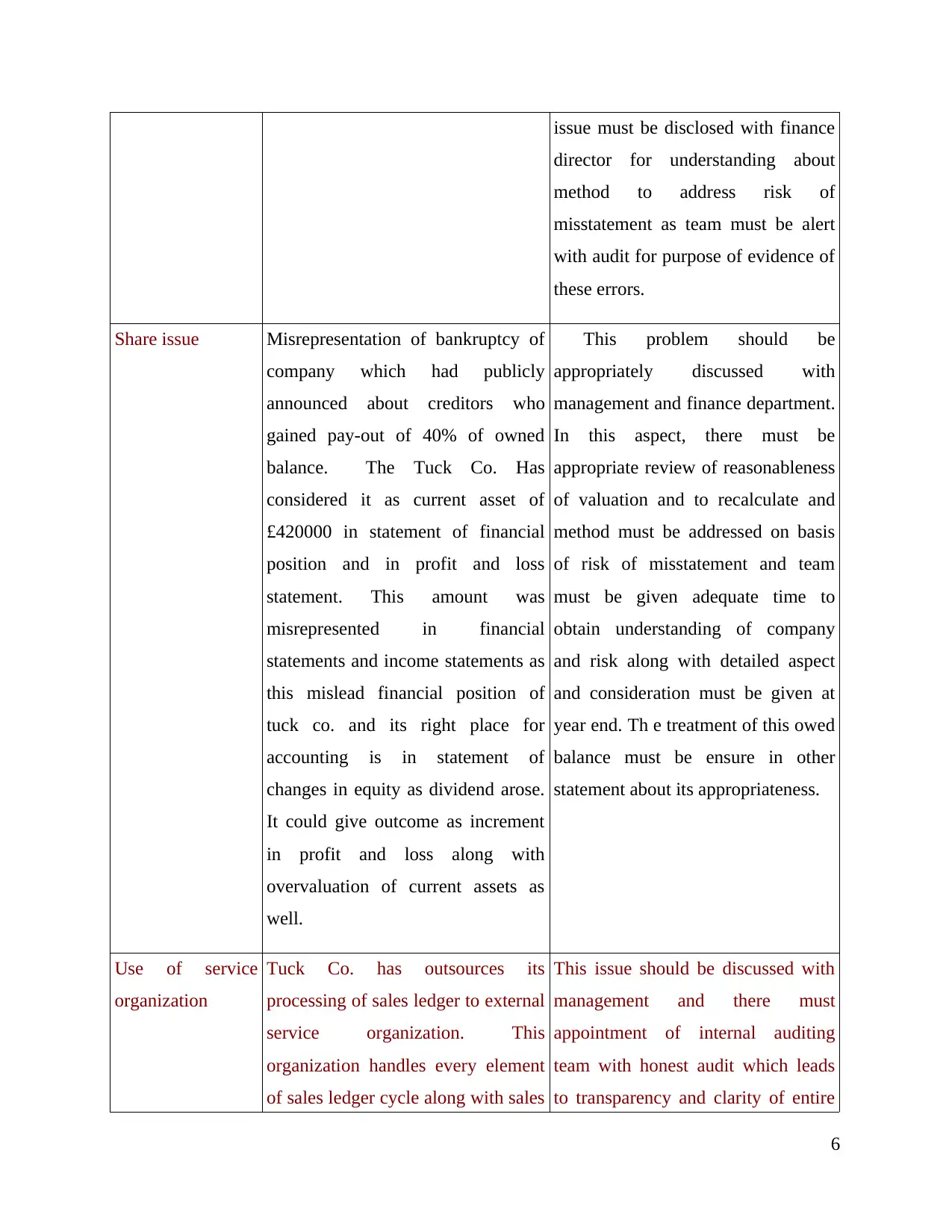

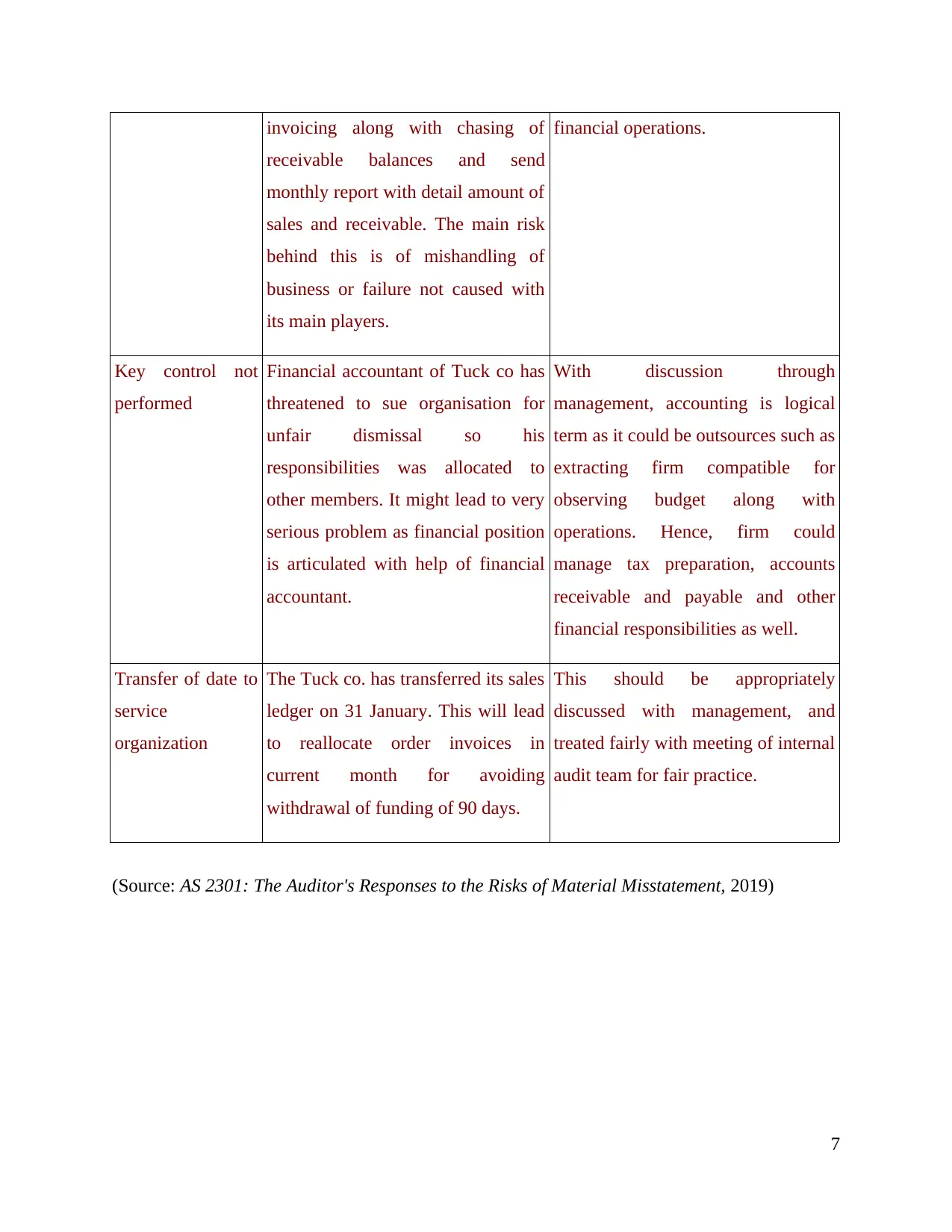

This report delves into the core principles of auditing, focusing on International Standard on Auditing (ISA) 260, which addresses the auditor's responsibility for communicating with those charged with governance. The report emphasizes the importance of effective communication throughout the audit process, outlining how it facilitates a constructive working relationship, aids in understanding matters arising from the audit, and helps in the oversight of financial reporting. Furthermore, the report analyzes specific audit risks within the context of Tuck Co., including inventory valuation, accounting treatment of a patent, sales ledger fraud, claims for unfair dismissal, and share issue misrepresentation. For each risk, the report describes the potential for material misstatement and proposes appropriate auditor responses, such as enhanced inventory counts, scrutiny of intangible asset amortization, investigation of fraudulent activities, and verification of financial disclosures. The report underscores the significance of professional skepticism, internal controls, and proactive communication in mitigating audit risks and ensuring the accuracy and reliability of financial statements. The document highlights the importance of accurate financial reporting in the context of the Tuck Co. case study.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.