Auditing Report: Audit Evidence, Financial Ratios, and Risk Analysis

VerifiedAdded on 2023/01/06

|12

|3700

|32

Report

AI Summary

This auditing report presents a comprehensive analysis of key auditing concepts. It begins with an introduction to auditing and then delves into the importance of sufficient and appropriate audit evidence, supported by a case study. The report examines the implications of financial ratios in auditing, analyzing ratios like current ratio, quick ratio, inventory turnover, and net profit margin. Internal control weaknesses within a case study are identified, focusing on segregation of duties and authorization processes. The report evaluates the appropriateness of conclusions drawn by auditors and discusses the risks associated with related party transactions, including material misstatement and fraud. Finally, it explores procedures for managing assertions and compares the roles of internal and external auditors. The report draws conclusions and provides references to support its findings.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Sufficient appropriate audit evidence..........................................................................................3

Sufficient appropriate audit evidence based on case study.........................................................3

QUESTION 2...................................................................................................................................4

Implication of financial ratios in auditing...................................................................................4

QUESTION 3...................................................................................................................................5

Internal control weaknesses........................................................................................................5

QUESTION 4...................................................................................................................................6

Arrival to appropriate conclusion................................................................................................6

Risk associated with related party transaction............................................................................6

QUESTION 5...................................................................................................................................8

Procedures for managing assertions............................................................................................8

QUESTION 6...................................................................................................................................8

Difference and similarities of internal and external auditor........................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Sufficient appropriate audit evidence..........................................................................................3

Sufficient appropriate audit evidence based on case study.........................................................3

QUESTION 2...................................................................................................................................4

Implication of financial ratios in auditing...................................................................................4

QUESTION 3...................................................................................................................................5

Internal control weaknesses........................................................................................................5

QUESTION 4...................................................................................................................................6

Arrival to appropriate conclusion................................................................................................6

Risk associated with related party transaction............................................................................6

QUESTION 5...................................................................................................................................8

Procedures for managing assertions............................................................................................8

QUESTION 6...................................................................................................................................8

Difference and similarities of internal and external auditor........................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Auditing is defined as the verification of the different activities and transaction taking

place in the business. This includes hiring a person for inspecting the company and the working

of company along with financial statements of company. Audit is applied all over the business

and within every aspect of business and other related activities of business. Auditing is very

important for businesses to comply with because this includes analysis of financial statements of

company by an independent auditor and try to communicate all the details relating to the

financial position of the company. This auditing will assist the company in improving its

financial position of company as auditor will provide their expertise relating to the use and

compliance of accounting principles by company at time of making financial accounts of

company.

In the present report the different aspect of auditing will be discussed like the sufficient

appropriate audit evidence with respect to a case study. Further the different types financial

ratios will be discussed and its implication in audit will be analysed. In addition to that the

different internal control weakness will discussed and further the various risk associated with the

related party transaction will be analysed. Moreover, the discussion will lead to procedure

relating to assertion of occurrence, completeness and accuracy relating to the case study. In the

end the different and similarities among the internal and external auditor will be discussed.

QUESTION 1

Sufficient appropriate audit evidence

Sufficient appropriate audit evidence is basically referring to the quantity of the evidence

collected in respect to the audit. Sufficiency accounts for the relevance and the reliability of the

audit evidence in order to provide support to the auditor's opinion (Lessambo, 2018). It includes

the information on the books of accounts along with the various other sources through which

information is gathered. Auditor expresses opinion on the financial statements of the company in

respect to whether they are depicting true and fair view or not and this is all dependent upon the

audit evidence gathered by the auditor.

Sufficient appropriate audit evidence based on case study

In the matter 1, the Raymond has not obtained sufficient audit evidence, he has

considered the error amounting to $185000 to be immaterial and has not proceeded further with

Auditing is defined as the verification of the different activities and transaction taking

place in the business. This includes hiring a person for inspecting the company and the working

of company along with financial statements of company. Audit is applied all over the business

and within every aspect of business and other related activities of business. Auditing is very

important for businesses to comply with because this includes analysis of financial statements of

company by an independent auditor and try to communicate all the details relating to the

financial position of the company. This auditing will assist the company in improving its

financial position of company as auditor will provide their expertise relating to the use and

compliance of accounting principles by company at time of making financial accounts of

company.

In the present report the different aspect of auditing will be discussed like the sufficient

appropriate audit evidence with respect to a case study. Further the different types financial

ratios will be discussed and its implication in audit will be analysed. In addition to that the

different internal control weakness will discussed and further the various risk associated with the

related party transaction will be analysed. Moreover, the discussion will lead to procedure

relating to assertion of occurrence, completeness and accuracy relating to the case study. In the

end the different and similarities among the internal and external auditor will be discussed.

QUESTION 1

Sufficient appropriate audit evidence

Sufficient appropriate audit evidence is basically referring to the quantity of the evidence

collected in respect to the audit. Sufficiency accounts for the relevance and the reliability of the

audit evidence in order to provide support to the auditor's opinion (Lessambo, 2018). It includes

the information on the books of accounts along with the various other sources through which

information is gathered. Auditor expresses opinion on the financial statements of the company in

respect to whether they are depicting true and fair view or not and this is all dependent upon the

audit evidence gathered by the auditor.

Sufficient appropriate audit evidence based on case study

In the matter 1, the Raymond has not obtained sufficient audit evidence, he has

considered the error amounting to $185000 to be immaterial and has not proceeded further with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the investigation. The auditor should have further investigated the shareholding having market

value below $200,000 as there were chances of such errors as well which might make the total

amount material to the company. Therefore, Raymond has not carried out the appropriate audit

procedure in an effective manner.

In the other case, Raymond has found some discrepancies while conducting the count

test, but he has taken them to be immaterial and also with the same the client also identified five

discrepancies in respect to actual quantity in hand and what the perpetual record is showing. But

no adjustment is being made is regard to the discrepancies in the perpetual records since the

amount was just $50000 and is considered to be immaterial. Under this matter as well, even

though the amount was not large but it was the duty of the auditor to obtain sufficient evidence in

respect to where the counting gets wrong or the cause of this error. Also, relevant entry or

adjustment should be made in the records as well.

QUESTION 2

Implication of financial ratios in auditing

The current ratio has increased in comparison to the previous year and budgeted

outcomes and is also more than the industry average as well. Also, the quick ratio has remained

same but is slower than the industry average. This might be because the company is having large

amount of inventory which has blocked it cash. The inventory turnover ratio is has reduced from

the last year and is lower than the budgeted outcome and the industry result. This means that the

company is not able make sales of product and the stock is lying on the shelf for long and is

ineffective in managing its inventory. Along with that the net profit margin ratio is very low even

though it is greater than the industry average and the budgeted results.

The auditor is required to determine what is making the inventory going slowly or does it

creating any sort of alarm in respect to the going concern of the business (Zainudin and Hashim,

2016). The inventory turnover ratio implies that auditor requires to carefully verify the existence,

quantity and the valuation of the inventory on a continuous basis in order to determine the right

amount and accurate result. Also, to determine whether the fall is deliberate or accidental. In

respect to the net profit margin, the auditor is required to access the operating expenses incurred

for attaining the profit and verifying the same with the vouchers or bills. Therefore, the auditor

requires to evaluate the cause of change in the figures.

value below $200,000 as there were chances of such errors as well which might make the total

amount material to the company. Therefore, Raymond has not carried out the appropriate audit

procedure in an effective manner.

In the other case, Raymond has found some discrepancies while conducting the count

test, but he has taken them to be immaterial and also with the same the client also identified five

discrepancies in respect to actual quantity in hand and what the perpetual record is showing. But

no adjustment is being made is regard to the discrepancies in the perpetual records since the

amount was just $50000 and is considered to be immaterial. Under this matter as well, even

though the amount was not large but it was the duty of the auditor to obtain sufficient evidence in

respect to where the counting gets wrong or the cause of this error. Also, relevant entry or

adjustment should be made in the records as well.

QUESTION 2

Implication of financial ratios in auditing

The current ratio has increased in comparison to the previous year and budgeted

outcomes and is also more than the industry average as well. Also, the quick ratio has remained

same but is slower than the industry average. This might be because the company is having large

amount of inventory which has blocked it cash. The inventory turnover ratio is has reduced from

the last year and is lower than the budgeted outcome and the industry result. This means that the

company is not able make sales of product and the stock is lying on the shelf for long and is

ineffective in managing its inventory. Along with that the net profit margin ratio is very low even

though it is greater than the industry average and the budgeted results.

The auditor is required to determine what is making the inventory going slowly or does it

creating any sort of alarm in respect to the going concern of the business (Zainudin and Hashim,

2016). The inventory turnover ratio implies that auditor requires to carefully verify the existence,

quantity and the valuation of the inventory on a continuous basis in order to determine the right

amount and accurate result. Also, to determine whether the fall is deliberate or accidental. In

respect to the net profit margin, the auditor is required to access the operating expenses incurred

for attaining the profit and verifying the same with the vouchers or bills. Therefore, the auditor

requires to evaluate the cause of change in the figures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

Internal control weaknesses

The internal control is mainly the policies and the procedures which are implemented by

the management with the core objective of accomplishing the business objectives by ensuring the

orderly and proper conduct of the business (Harp and Barnes, 2018). The internal control

weaknesses of the Everyday supplies for the cash receipts and the billing functions are stated

below.

In the given case, there is no segregation of duties among the personnel preparing the

invoices, verifying the same and posting it on the ledger a/c which might result into

incurring of unreliable records caused due to the errors.

The a/c receivable supervisor carries out the billing process but does not involves any

verification of the same either manually or through computer and along with that has the

ability to alter the details.

Another weakness is that the pre-listed cheques should be supported with the verified

deposit slips received from the bank at the time of bank reconciliation by a clerk for

carrying the activity independently instead of cashier.

The remittance information which is being transmitted by the bookkeeper electronically

to the account receivable supervisor for further updating should be backed up along with

the supporting documents which includes the pre-listed cheques and slips related to

deposits.

There is lack of effective internal control system which entails carrying the

comprehensive background check on the customers before providing credit and affecting

the credit sale and exposing the company to the rise in the uncollectible a/c incidents.

Explanation for weakness 2 and 5 are given below.

The billing process by account receivable supervisor was a weakness as this includes no

verification process by the manager. Hence, there were high chances of fraud which can

take place in the accounting and billing process. This is a weakness as supervisor not

involves use of computers or manual checking of every transaction being recorded by the

supervisor and this affects the working capacity of the company.

The bookkeeper has the authority to write off the uncollectible a/cs without undertaking

any investigation in order to find out the reasons and the details pertaining to each of such

Internal control weaknesses

The internal control is mainly the policies and the procedures which are implemented by

the management with the core objective of accomplishing the business objectives by ensuring the

orderly and proper conduct of the business (Harp and Barnes, 2018). The internal control

weaknesses of the Everyday supplies for the cash receipts and the billing functions are stated

below.

In the given case, there is no segregation of duties among the personnel preparing the

invoices, verifying the same and posting it on the ledger a/c which might result into

incurring of unreliable records caused due to the errors.

The a/c receivable supervisor carries out the billing process but does not involves any

verification of the same either manually or through computer and along with that has the

ability to alter the details.

Another weakness is that the pre-listed cheques should be supported with the verified

deposit slips received from the bank at the time of bank reconciliation by a clerk for

carrying the activity independently instead of cashier.

The remittance information which is being transmitted by the bookkeeper electronically

to the account receivable supervisor for further updating should be backed up along with

the supporting documents which includes the pre-listed cheques and slips related to

deposits.

There is lack of effective internal control system which entails carrying the

comprehensive background check on the customers before providing credit and affecting

the credit sale and exposing the company to the rise in the uncollectible a/c incidents.

Explanation for weakness 2 and 5 are given below.

The billing process by account receivable supervisor was a weakness as this includes no

verification process by the manager. Hence, there were high chances of fraud which can

take place in the accounting and billing process. This is a weakness as supervisor not

involves use of computers or manual checking of every transaction being recorded by the

supervisor and this affects the working capacity of the company.

The bookkeeper has the authority to write off the uncollectible a/cs without undertaking

any investigation in order to find out the reasons and the details pertaining to each of such

overdue a/c. The current criteria for treating the overdue account is mere 6 months for

writing it off and is also considered to be very inflexible and does not render for the

prevention of the further granting of the credit to the contractor at an initial date or at the

time when such account becomes overdue for the very first time. The bookkeeper has the

ability to grant additional credit in an indirect way and even by not notifying the credit

manager even in case where the contractor's account has been written off. Along with

that, the bookkeeper has the incompatible authorities in respect to authorizing the writing

off of the overdue accounts and the recording of the journal entries. Therefore, this

weakness has the potential to expose the company to a greater risk on account of the

credit risk to the contractors who are unable or having inability to pay back back the

amount on the due date.

QUESTION 4

Arrival to appropriate conclusion

With reference to the conclusion drawn by John was not appropriate and correct. The

major reason underlying this fact is that with help of the analytical procedure of auditing the

company can try to assess the unusual fact relating to company or any other transaction (Rozario

and Vasarhelyi, 2018). Thus, in the present case of Taxon Ltd the auditor was not having proof

of the other four Electronic Fund Transfer (EFT) forms. Thus, with help of the analytical process

of auditing the company can record the transaction that remaining four EFT forms has not been

approved in writing. Hence, the conclusion drawn by John was not appropriate and effective.

The major reason underlying this fact is that auditor John has recorded the six samples which

was having written approval of CFO of company. But they have also recorded remaining four

transaction assuming to have verbal approval.

Risk associated with related party transaction

Auditing of related party transaction is very important to be performed at time of

analysing and auditing financial statements (Moffitt, Rozario and Vasarhelyi, 2018). The related

party transactions are the transaction which involves various stakeholders of company such as

executives, directors and other stakeholders of company. There are different types of risk which

writing it off and is also considered to be very inflexible and does not render for the

prevention of the further granting of the credit to the contractor at an initial date or at the

time when such account becomes overdue for the very first time. The bookkeeper has the

ability to grant additional credit in an indirect way and even by not notifying the credit

manager even in case where the contractor's account has been written off. Along with

that, the bookkeeper has the incompatible authorities in respect to authorizing the writing

off of the overdue accounts and the recording of the journal entries. Therefore, this

weakness has the potential to expose the company to a greater risk on account of the

credit risk to the contractors who are unable or having inability to pay back back the

amount on the due date.

QUESTION 4

Arrival to appropriate conclusion

With reference to the conclusion drawn by John was not appropriate and correct. The

major reason underlying this fact is that with help of the analytical procedure of auditing the

company can try to assess the unusual fact relating to company or any other transaction (Rozario

and Vasarhelyi, 2018). Thus, in the present case of Taxon Ltd the auditor was not having proof

of the other four Electronic Fund Transfer (EFT) forms. Thus, with help of the analytical process

of auditing the company can record the transaction that remaining four EFT forms has not been

approved in writing. Hence, the conclusion drawn by John was not appropriate and effective.

The major reason underlying this fact is that auditor John has recorded the six samples which

was having written approval of CFO of company. But they have also recorded remaining four

transaction assuming to have verbal approval.

Risk associated with related party transaction

Auditing of related party transaction is very important to be performed at time of

analysing and auditing financial statements (Moffitt, Rozario and Vasarhelyi, 2018). The related

party transactions are the transaction which involves various stakeholders of company such as

executives, directors and other stakeholders of company. There are different types of risk which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

are associated with the related party transaction and is present in case of Taxon Ltd as well.

These related party risk are as follows-

Material misstatement- In case of risk associated with related parties the major risk faced

is the risk of material misstatement (Kotsanopoulos and Arvanitoyannis, 2017). This is a type of

risk which the related party faces in order to manage the transaction with the related party and

the company itself. The risk of material misstatement is defined as a risk which is encountered

by company at time of entering in transaction with company. Under this risk some important

information is not being communicated with the related party. Hence, some of the material

information is not being shared and this is the risk which is present in related party transaction.

With reference to the case of Tyson Ltd. is clear that the auditor has not highlighted the fact that

remaining of the four EFT transaction are not having written approval of CFO of company.

Risk of fraud- this is another major type of risk which is associated at time of related

party transaction. Under this the risk is fraud is intentionally doing a wrong thing even after the

fact that person is having knowledge that they are doing wrong. But then also people act in the

same manner and this affects the integrity of the company and the related parties attached with

company. It is the duty and liability of auditor that they try to outline the fraud taking place in

company and try to take some actions in order to minimize the risk of fraud which is taking in

company (Groomer and Murthy, 2018). With reference to case study of Taxon Ltd the risk of

fraud was also present. This was in form that auditor included the four remaining EFT forms as

well by stating that the remaining four EFT forms was having verbal consent of CFO which was

not having any proof relating to the verbal consent.

The reliability of the control at Taxon is not much effective as the control system was not

good. The auditor was not providing reliable information after the auditing as the information

available at the company was not complete. The four EFT form was not having the written

approval of CFO and because of this the data was not reliable and this affected the whole of the

reliability of the control system (Seethamraju and Hecimovic, 2020). The control system

reliability was affected as the company was not having proof or records that whether approval

was provided to the remaining four of the EFT forms and this affected the reliability of the

control system.

These related party risk are as follows-

Material misstatement- In case of risk associated with related parties the major risk faced

is the risk of material misstatement (Kotsanopoulos and Arvanitoyannis, 2017). This is a type of

risk which the related party faces in order to manage the transaction with the related party and

the company itself. The risk of material misstatement is defined as a risk which is encountered

by company at time of entering in transaction with company. Under this risk some important

information is not being communicated with the related party. Hence, some of the material

information is not being shared and this is the risk which is present in related party transaction.

With reference to the case of Tyson Ltd. is clear that the auditor has not highlighted the fact that

remaining of the four EFT transaction are not having written approval of CFO of company.

Risk of fraud- this is another major type of risk which is associated at time of related

party transaction. Under this the risk is fraud is intentionally doing a wrong thing even after the

fact that person is having knowledge that they are doing wrong. But then also people act in the

same manner and this affects the integrity of the company and the related parties attached with

company. It is the duty and liability of auditor that they try to outline the fraud taking place in

company and try to take some actions in order to minimize the risk of fraud which is taking in

company (Groomer and Murthy, 2018). With reference to case study of Taxon Ltd the risk of

fraud was also present. This was in form that auditor included the four remaining EFT forms as

well by stating that the remaining four EFT forms was having verbal consent of CFO which was

not having any proof relating to the verbal consent.

The reliability of the control at Taxon is not much effective as the control system was not

good. The auditor was not providing reliable information after the auditing as the information

available at the company was not complete. The four EFT form was not having the written

approval of CFO and because of this the data was not reliable and this affected the whole of the

reliability of the control system (Seethamraju and Hecimovic, 2020). The control system

reliability was affected as the company was not having proof or records that whether approval

was provided to the remaining four of the EFT forms and this affected the reliability of the

control system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 5

Procedures for managing assertions

Occurrence- this assertion is related to the fact that whether the transaction which was

recorded actually took place or not (Management assertion in auditing, 2019). With

respect to the case of Magi Chen of Sun Construction Pty Ltd. For managing occurrence

assertion, the process to be followed by company is that they have to check all the

transaction being recorded with help of vouchers that they have actually being performed

or not. For this Sun Construction Pty Ltd. Will check the receipt book and all transaction

in actual.

Completeness- this assertion deals with the fact that whether transaction or event of

business has been recorded or not. Hence, for this Sun Construction Pty Ltd. follows the

procedures of reconciling the journals and ledger with final accounts. The major reason

underlying this fact is that all the transactions are recorded in journal and from their

posted in ledger and then in final accounts. Hence, with this process company will be

able to tally all transaction.

Accuracy- present assertion is related with fact that all transactions are recorded in full

amount in accurate manner. Thus, for this Sun Construction Pty Ltd. Must check and

reconcile all the transaction with the voucher and bills. The major reason is that in

voucher and bill all transaction is present including the amount.

QUESTION 6

Difference and similarities of internal and external auditor

The internal auditor is a person who are responsible for taking the view of governance,

control system of company and all other related risk of business. the major work of the internal

auditor is to manage and monitor the routine activities of business and provides for suggestion is

any required. On the flip side the external auditor is a person or entity being hired by company to

analyse the financial statements of company and comment on financial position of company

(Byrne, Anda and Ho, 2019). Both the internal and external auditor has different role within the

management and running of company. In addition to this both internal and external auditor are

necessary for business to be recruited as this manages the performance and working of company

to a great extent.

Procedures for managing assertions

Occurrence- this assertion is related to the fact that whether the transaction which was

recorded actually took place or not (Management assertion in auditing, 2019). With

respect to the case of Magi Chen of Sun Construction Pty Ltd. For managing occurrence

assertion, the process to be followed by company is that they have to check all the

transaction being recorded with help of vouchers that they have actually being performed

or not. For this Sun Construction Pty Ltd. Will check the receipt book and all transaction

in actual.

Completeness- this assertion deals with the fact that whether transaction or event of

business has been recorded or not. Hence, for this Sun Construction Pty Ltd. follows the

procedures of reconciling the journals and ledger with final accounts. The major reason

underlying this fact is that all the transactions are recorded in journal and from their

posted in ledger and then in final accounts. Hence, with this process company will be

able to tally all transaction.

Accuracy- present assertion is related with fact that all transactions are recorded in full

amount in accurate manner. Thus, for this Sun Construction Pty Ltd. Must check and

reconcile all the transaction with the voucher and bills. The major reason is that in

voucher and bill all transaction is present including the amount.

QUESTION 6

Difference and similarities of internal and external auditor

The internal auditor is a person who are responsible for taking the view of governance,

control system of company and all other related risk of business. the major work of the internal

auditor is to manage and monitor the routine activities of business and provides for suggestion is

any required. On the flip side the external auditor is a person or entity being hired by company to

analyse the financial statements of company and comment on financial position of company

(Byrne, Anda and Ho, 2019). Both the internal and external auditor has different role within the

management and running of company. In addition to this both internal and external auditor are

necessary for business to be recruited as this manages the performance and working of company

to a great extent.

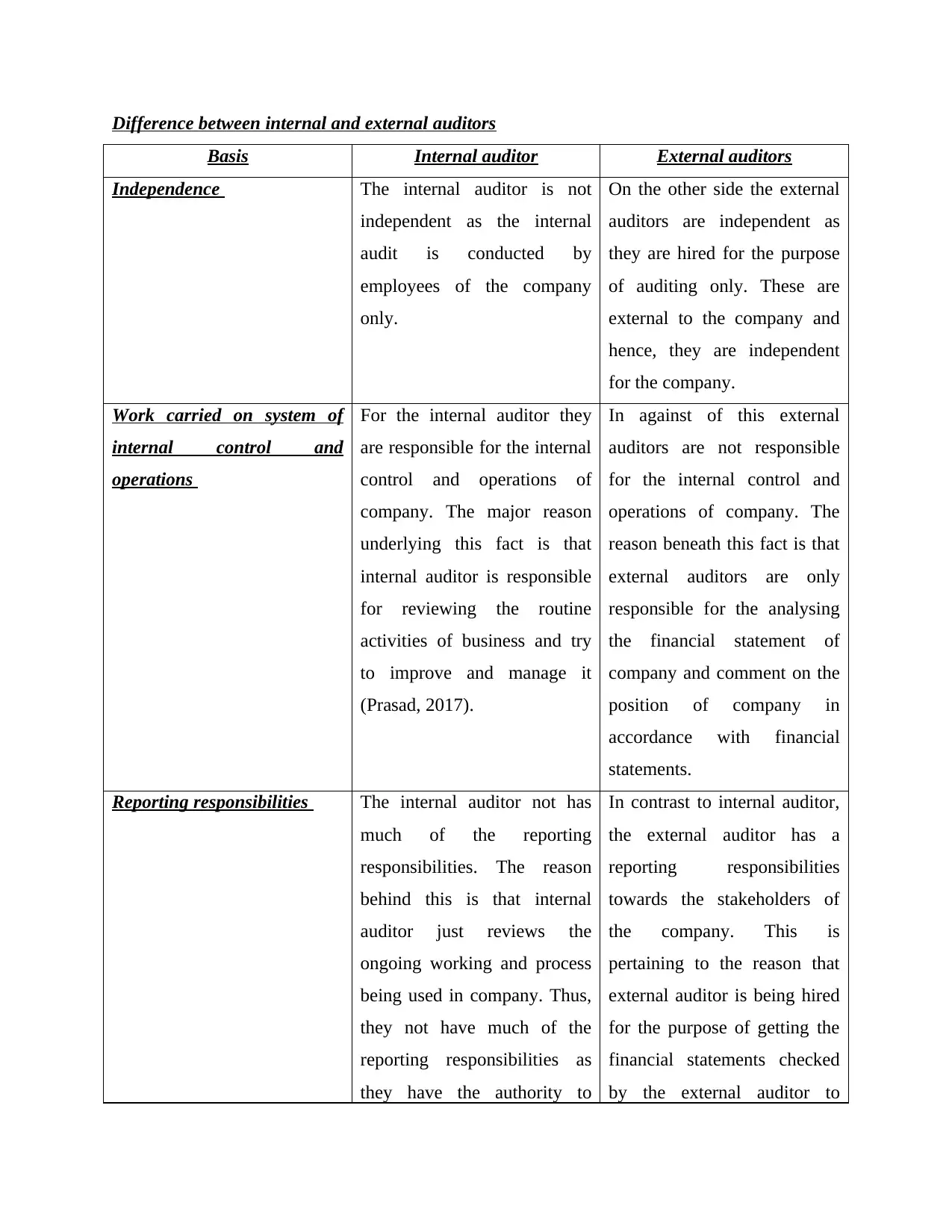

Difference between internal and external auditors

Basis Internal auditor External auditors

Independence The internal auditor is not

independent as the internal

audit is conducted by

employees of the company

only.

On the other side the external

auditors are independent as

they are hired for the purpose

of auditing only. These are

external to the company and

hence, they are independent

for the company.

Work carried on system of

internal control and

operations

For the internal auditor they

are responsible for the internal

control and operations of

company. The major reason

underlying this fact is that

internal auditor is responsible

for reviewing the routine

activities of business and try

to improve and manage it

(Prasad, 2017).

In against of this external

auditors are not responsible

for the internal control and

operations of company. The

reason beneath this fact is that

external auditors are only

responsible for the analysing

the financial statement of

company and comment on the

position of company in

accordance with financial

statements.

Reporting responsibilities The internal auditor not has

much of the reporting

responsibilities. The reason

behind this is that internal

auditor just reviews the

ongoing working and process

being used in company. Thus,

they not have much of the

reporting responsibilities as

they have the authority to

In contrast to internal auditor,

the external auditor has a

reporting responsibilities

towards the stakeholders of

the company. This is

pertaining to the reason that

external auditor is being hired

for the purpose of getting the

financial statements checked

by the external auditor to

Basis Internal auditor External auditors

Independence The internal auditor is not

independent as the internal

audit is conducted by

employees of the company

only.

On the other side the external

auditors are independent as

they are hired for the purpose

of auditing only. These are

external to the company and

hence, they are independent

for the company.

Work carried on system of

internal control and

operations

For the internal auditor they

are responsible for the internal

control and operations of

company. The major reason

underlying this fact is that

internal auditor is responsible

for reviewing the routine

activities of business and try

to improve and manage it

(Prasad, 2017).

In against of this external

auditors are not responsible

for the internal control and

operations of company. The

reason beneath this fact is that

external auditors are only

responsible for the analysing

the financial statement of

company and comment on the

position of company in

accordance with financial

statements.

Reporting responsibilities The internal auditor not has

much of the reporting

responsibilities. The reason

behind this is that internal

auditor just reviews the

ongoing working and process

being used in company. Thus,

they not have much of the

reporting responsibilities as

they have the authority to

In contrast to internal auditor,

the external auditor has a

reporting responsibilities

towards the stakeholders of

the company. This is

pertaining to the reason that

external auditor is being hired

for the purpose of getting the

financial statements checked

by the external auditor to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

suggest and implement the

changes which they think is

essential in the management of

business. Here the internal

auditors are responsible for

reporting all their work to the

management of company. The

major reason pertaining to the

fact is that internal auditor is

responsible for managing

performance of company.

check the fairness and

truthfulness of the statements

of company. Here the

responsibility of external

auditor is responsible for

stakeholders of company as

financial statements are of

interest of stakeholders of

company.

Similarity among internal and external auditors

The similarity between the internal and external auditor is that both the parties are hired

for the benefit of company and work in the direction of protecting the company. The internal

auditor is responsible for the managing the working of the company and try to improve the

performance and attain goals of company. In the similar manner, external auditor also evaluates

the financial statements of company and try to comment on financial position of company that is

whether it is correct or not. Further both internal and external auditor ensures that all ethical and

financial principles are being followed by both auditors (Hay, Stewart and Botica Redmayne,

2017). Another major similarity between internal and external auditor is that both of them work

in direction of attainment of goals and objectives of business and try to achieve them in any

condition. Furthermore, the report of both internal and external auditors assist management and

stakeholder in deciding better policies for company and work in direction of developing the

business to a great extent.

CONCLUSION

From the above whole study, it is clearly evaluated that auditing is defined as a process

through which an auditor analysed the financial statements of company and comment of

financial position of company. Under auditing company hires an auditor who thoroughly checks

and analyses the financial statement of company in accordance with all the financial and

accounting principles and ethics. If the company has not prepared accounts in accordance with

changes which they think is

essential in the management of

business. Here the internal

auditors are responsible for

reporting all their work to the

management of company. The

major reason pertaining to the

fact is that internal auditor is

responsible for managing

performance of company.

check the fairness and

truthfulness of the statements

of company. Here the

responsibility of external

auditor is responsible for

stakeholders of company as

financial statements are of

interest of stakeholders of

company.

Similarity among internal and external auditors

The similarity between the internal and external auditor is that both the parties are hired

for the benefit of company and work in the direction of protecting the company. The internal

auditor is responsible for the managing the working of the company and try to improve the

performance and attain goals of company. In the similar manner, external auditor also evaluates

the financial statements of company and try to comment on financial position of company that is

whether it is correct or not. Further both internal and external auditor ensures that all ethical and

financial principles are being followed by both auditors (Hay, Stewart and Botica Redmayne,

2017). Another major similarity between internal and external auditor is that both of them work

in direction of attainment of goals and objectives of business and try to achieve them in any

condition. Furthermore, the report of both internal and external auditors assist management and

stakeholder in deciding better policies for company and work in direction of developing the

business to a great extent.

CONCLUSION

From the above whole study, it is clearly evaluated that auditing is defined as a process

through which an auditor analysed the financial statements of company and comment of

financial position of company. Under auditing company hires an auditor who thoroughly checks

and analyses the financial statement of company in accordance with all the financial and

accounting principles and ethics. If the company has not prepared accounts in accordance with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

these principles, then it is the responsibility of auditor to highlight this and bring in notice of

company.

This is essential as this will assist the company in managing the accounts in accordance

to the principles which are being highlighted in auditing by the auditor. Further from the above

study it was analysed that auditing is very essential for company as it highlighted the appropriate

audit evidence and implication of different financial ratios in auditing. Further it discussed the

different risk associated with related transaction like risk of fraud, material misstatement and

many others.

company.

This is essential as this will assist the company in managing the accounts in accordance

to the principles which are being highlighted in auditing by the auditor. Further from the above

study it was analysed that auditing is very essential for company as it highlighted the appropriate

audit evidence and implication of different financial ratios in auditing. Further it discussed the

different risk associated with related transaction like risk of fraud, material misstatement and

many others.

REFERENCES

Books and Journals

Byrne, J.J., Anda, M. and Ho, G.E., 2019. Water sustainable house: water auditing of 3 case

studies in Perth, Western Australia. Water Practice and Technology. 14(2). pp.435-443.

Groomer, S.M. and Murthy, U.S., 2018. Continuous Auditing of Database Applications: An

Embedded Audit Module Approach1. In Continuous auditing. Emerald Publishing

Limited.

Harp, N. L. and Barnes, B. G., 2018. Internal control weaknesses and acquisition

performance. The Accounting Review. 93(1). pp.235-258.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The role of auditing in corporate

governance in Australia and New Zealand: A research synthesis. Australian Accounting

Review. 27(4). pp.457-479.

Kotsanopoulos, K.V. and Arvanitoyannis, I.S., 2017. The role of auditing, food safety, and food

quality standards in the food industry: A review. Comprehensive Reviews in Food

Science and Food Safety. 16(5). pp.760-775.

Lessambo, F. I., 2018. Audit Evidence and Documentation. In Auditing, Assurance Services, and

Forensics (pp. 155-182). Palgrave Macmillan, Cham.

Moffitt, K.C., Rozario, A.M. and Vasarhelyi, M.A., 2018. Robotic process automation for

auditing. Journal of Emerging Technologies in Accounting. 15(1). pp.1-10.

Prasad, A., 2017. Environmental performance auditing in Australia, Canada and

India. International Journal of Government Auditing. 44(2). p.24.

Rozario, A.M. and Vasarhelyi, M.A., 2018. Auditing with Smart Contracts. International

Journal of Digital Accounting Research. 18.

Seethamraju, R.C. and Hecimovic, A., 2020. Impact of Artificial Intelligence on Auditing-An

Exploratory Study.

Zainudin, E. F. and Hashim, H. A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting.

Online

Management assertion in auditing. 2019. [Online]. Available through: <

https://www.accountingtools.com/articles/what-are-management-assertions-in-

auditing.html>

Books and Journals

Byrne, J.J., Anda, M. and Ho, G.E., 2019. Water sustainable house: water auditing of 3 case

studies in Perth, Western Australia. Water Practice and Technology. 14(2). pp.435-443.

Groomer, S.M. and Murthy, U.S., 2018. Continuous Auditing of Database Applications: An

Embedded Audit Module Approach1. In Continuous auditing. Emerald Publishing

Limited.

Harp, N. L. and Barnes, B. G., 2018. Internal control weaknesses and acquisition

performance. The Accounting Review. 93(1). pp.235-258.

Hay, D., Stewart, J. and Botica Redmayne, N., 2017. The role of auditing in corporate

governance in Australia and New Zealand: A research synthesis. Australian Accounting

Review. 27(4). pp.457-479.

Kotsanopoulos, K.V. and Arvanitoyannis, I.S., 2017. The role of auditing, food safety, and food

quality standards in the food industry: A review. Comprehensive Reviews in Food

Science and Food Safety. 16(5). pp.760-775.

Lessambo, F. I., 2018. Audit Evidence and Documentation. In Auditing, Assurance Services, and

Forensics (pp. 155-182). Palgrave Macmillan, Cham.

Moffitt, K.C., Rozario, A.M. and Vasarhelyi, M.A., 2018. Robotic process automation for

auditing. Journal of Emerging Technologies in Accounting. 15(1). pp.1-10.

Prasad, A., 2017. Environmental performance auditing in Australia, Canada and

India. International Journal of Government Auditing. 44(2). p.24.

Rozario, A.M. and Vasarhelyi, M.A., 2018. Auditing with Smart Contracts. International

Journal of Digital Accounting Research. 18.

Seethamraju, R.C. and Hecimovic, A., 2020. Impact of Artificial Intelligence on Auditing-An

Exploratory Study.

Zainudin, E. F. and Hashim, H. A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting.

Online

Management assertion in auditing. 2019. [Online]. Available through: <

https://www.accountingtools.com/articles/what-are-management-assertions-in-

auditing.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.