Auditing and Assurance: Financial Analysis and Risk Assessment Report

VerifiedAdded on 2022/08/26

|15

|3462

|16

Report

AI Summary

This report provides a comprehensive analysis of auditing and assurance principles, focusing on risk assessment and financial analysis. It examines factors that increase or decrease the risk of material misstatements, considering the case of Homes South Ltd (HS). The report identifies specific audit risks and recommends appropriate audit procedures. Additionally, the report analyzes financial information from Darfield Electronics, identifying mismatches in financial data and assessing potential audit risks, such as overstatement of revenue, misallocation of costs, and insufficient provisions for doubtful debts and outdated inventories. The report highlights the importance of understanding financial statement analysis and risk management within an auditing context.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

Introduction................................................................................................................................2

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................6

Analysis of the Information...................................................................................................6

Identification of Audit Risks..................................................................................................8

Audit Response......................................................................................................................9

Conclusion and Recommendations..........................................................................................10

References................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................6

Analysis of the Information...................................................................................................6

Identification of Audit Risks..................................................................................................8

Audit Response......................................................................................................................9

Conclusion and Recommendations..........................................................................................10

References................................................................................................................................11

2AUDITING AND ASSURANCE

Introduction

Auditing refers to the process to examine the financial records of an organizations in

order to determine that whether they are correct and they are recorded in accordance with the

applicable accounting rules and principles (Leung et al. 2015). External auditors come from

outside companies for examining the financial and accounting records of the client

organizations in order to provide independent audit opinion on these financial and accounting

records. Law puts the obligation on the listed companies to have their financial reports

audited by external auditors. External auditors have the prime responsibility to gather all

information of the audit clients that are required to conduct the audit. After that collection of

all the required information and facts, it is needed for the auditors to analyse the factors that

would create impacts on the material misstatements. At the same time, external auditors are

also required to analyse the draft financial information of the clients in order to identify the

audit risks in them. After identifying the audit risks, the external auditors are accountable to

undertake appropriate audit procedures in respond to the risks identified (William Jr, Glover

and Prawitt 2016). There are two parts of this report. The first part of the report involves in

indicating the factors that would affect the risks of material misstatements along with reasons.

The second part involves in analysing the draft financial information for the identification of

audit risks along with the required respond from the auditors.

Answer to Question 1

Consideration of the provided information Homes South Ltd (HS) shows that there

are two types of factors in the company; one would likely to increase the risks of material

misstatements and the other would probably decrease the risks of material misstatements.

Both these types of factors are discussed below:

Introduction

Auditing refers to the process to examine the financial records of an organizations in

order to determine that whether they are correct and they are recorded in accordance with the

applicable accounting rules and principles (Leung et al. 2015). External auditors come from

outside companies for examining the financial and accounting records of the client

organizations in order to provide independent audit opinion on these financial and accounting

records. Law puts the obligation on the listed companies to have their financial reports

audited by external auditors. External auditors have the prime responsibility to gather all

information of the audit clients that are required to conduct the audit. After that collection of

all the required information and facts, it is needed for the auditors to analyse the factors that

would create impacts on the material misstatements. At the same time, external auditors are

also required to analyse the draft financial information of the clients in order to identify the

audit risks in them. After identifying the audit risks, the external auditors are accountable to

undertake appropriate audit procedures in respond to the risks identified (William Jr, Glover

and Prawitt 2016). There are two parts of this report. The first part of the report involves in

indicating the factors that would affect the risks of material misstatements along with reasons.

The second part involves in analysing the draft financial information for the identification of

audit risks along with the required respond from the auditors.

Answer to Question 1

Consideration of the provided information Homes South Ltd (HS) shows that there

are two types of factors in the company; one would likely to increase the risks of material

misstatements and the other would probably decrease the risks of material misstatements.

Both these types of factors are discussed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

Factors Contributing to the Increase in Risk of Material Misstatements

1. It can be seen from the provided situation that there is a major volatility in the interest

rate and this interest rate is a major factor for the mortgage business of HS. This

volatility in the interest rate is continuously increasing and decreasing in short

intervals which is affecting the mortgage business of the company. For this reason,

the price of mortgage is being affected and this can lead to the risk of material

misstatements (Hosseinniakani, Inacio and Mota 2014).

2. George Watson is the majority shareholder of HS whereas he is also the Chief

Executive Officer and is responsible for controlling the Board of Directors of the

company. It indicates that George Watson has the large amount of power and can

influence the decision making process of the company. This increases the chances of

fraud in the key accounts of the financial statements by him that can lead to material

misstatements in the financial reports of HS (Bhattacharjee, Maletta and Moreno

2016).

3. It is mentioned in the provided case of HS that the management of the company is

compensated based on the profitability of branches. This increases the chance of

fraudulent activities around the profitability of the branches by deliberately

overstating the profits or understating the expenses in order to increase the

profitability of the branches. This incentive or motivation of the management of HS to

increase the profitability for getting higher compensation increases the chance of

material misstatements in the financial statements of the company (Ruhnke and

Schmidt 2014).

4. As per the provided information, the formula of HS that is the accounting estimation

has failed in correctly estimating the allowance amount for loan losses. It indicates

towards the presence of key uncertainty in the accounting estimates and assumptions

Factors Contributing to the Increase in Risk of Material Misstatements

1. It can be seen from the provided situation that there is a major volatility in the interest

rate and this interest rate is a major factor for the mortgage business of HS. This

volatility in the interest rate is continuously increasing and decreasing in short

intervals which is affecting the mortgage business of the company. For this reason,

the price of mortgage is being affected and this can lead to the risk of material

misstatements (Hosseinniakani, Inacio and Mota 2014).

2. George Watson is the majority shareholder of HS whereas he is also the Chief

Executive Officer and is responsible for controlling the Board of Directors of the

company. It indicates that George Watson has the large amount of power and can

influence the decision making process of the company. This increases the chances of

fraud in the key accounts of the financial statements by him that can lead to material

misstatements in the financial reports of HS (Bhattacharjee, Maletta and Moreno

2016).

3. It is mentioned in the provided case of HS that the management of the company is

compensated based on the profitability of branches. This increases the chance of

fraudulent activities around the profitability of the branches by deliberately

overstating the profits or understating the expenses in order to increase the

profitability of the branches. This incentive or motivation of the management of HS to

increase the profitability for getting higher compensation increases the chance of

material misstatements in the financial statements of the company (Ruhnke and

Schmidt 2014).

4. As per the provided information, the formula of HS that is the accounting estimation

has failed in correctly estimating the allowance amount for loan losses. It indicates

towards the presence of key uncertainty in the accounting estimates and assumptions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

used by the management of HS in the accounting for allowance for loan losses. This is

a crucial aspect that can increase the risk of material misstatements (Abdullatif 2013).

5. In the year 2019, a new branch office was opened by HS in a metropolitan area that is

30 kilometres from the principal business place and this branch has not been able in

producing profitability yet. This increases the fraud risk of manipulating the amount

of revenues and expenses of the branch for increasing the profit of the branch.

Therefore, this needs to be considered as a crucial factor that can increase the risk of

material misstatements in HS (LópezPuertas‐Lamy, Desender and Epure 2017).

6. A new computer system has been installed by HS in 2019 in order to increase the

operational efficiency. However, certain negatives are associated with this new

accounting system. In case there is any types of errors in the new system and in case

the new system shows errors in collecting data, there can be material misstatement in

the financial statement of the company (Lobo and Zhao 2013).

Factors Contributing to the Decrease in Risk of Material Misstatements

1. HS operates in the finance industry that is governed as well as regulated by extensive

legislations and regulations imposed by the government. Compliance with these

extensive legislations and regulations reduces the scope of fraudulent activities in the

financial statements of the companies operating under this industry. This is a crucial

factor that reduces the risk of material misstatements in HS (Askary, Arnaout and

Abughazaleh 2018).

2. It can be seen that the main operations of HS are in the prosperous rural area that has

experienced significant growth in the recent year. When a company is already

profitable, there is not much incentive or motivation for its management to

manipulatively increase the profitability. This factor reduces the risk of material

misstatement (Al-Khaddash, Al Nawas and Ramadan 2013).

used by the management of HS in the accounting for allowance for loan losses. This is

a crucial aspect that can increase the risk of material misstatements (Abdullatif 2013).

5. In the year 2019, a new branch office was opened by HS in a metropolitan area that is

30 kilometres from the principal business place and this branch has not been able in

producing profitability yet. This increases the fraud risk of manipulating the amount

of revenues and expenses of the branch for increasing the profit of the branch.

Therefore, this needs to be considered as a crucial factor that can increase the risk of

material misstatements in HS (LópezPuertas‐Lamy, Desender and Epure 2017).

6. A new computer system has been installed by HS in 2019 in order to increase the

operational efficiency. However, certain negatives are associated with this new

accounting system. In case there is any types of errors in the new system and in case

the new system shows errors in collecting data, there can be material misstatement in

the financial statement of the company (Lobo and Zhao 2013).

Factors Contributing to the Decrease in Risk of Material Misstatements

1. HS operates in the finance industry that is governed as well as regulated by extensive

legislations and regulations imposed by the government. Compliance with these

extensive legislations and regulations reduces the scope of fraudulent activities in the

financial statements of the companies operating under this industry. This is a crucial

factor that reduces the risk of material misstatements in HS (Askary, Arnaout and

Abughazaleh 2018).

2. It can be seen that the main operations of HS are in the prosperous rural area that has

experienced significant growth in the recent year. When a company is already

profitable, there is not much incentive or motivation for its management to

manipulatively increase the profitability. This factor reduces the risk of material

misstatement (Al-Khaddash, Al Nawas and Ramadan 2013).

5AUDITING AND ASSURANCE

3. It can be observed from the facts of the case that there is a considerable growth of the

products in which HS deals which increases the scope of the company to deliver more

products for increasing the sales and profitability. This is a crucial aspect that

decreases the risk of material misstatements.

4. It can be seen from the provided information of HS that there is a favourable

availability of funds for the business of HS for the additional mortgages. The

company has been able to continuously sell their mortgages as a source of new

lendable funds. Therefore, the presence of adequate funds decreases the risk of

material misstatements (Al-Khaddash, Al Nawas and Ramadan 2013).

5. It is provided in the case that there has been very little turnover of employees in HS’s

accounting department which indicates towards superior knowledge and skillset of the

employees under this department. Therefore, long-standing employees with effective

accounting skills and knowledge decreases the risk of material misstatements.

6. It can be seen that the internal auditor of HS uses to directly report to the audit

committee chairman who is a minority shareholder instead of George Watson. This

helps in retaining the integrity and honesty of the internal audit team and this keeps

informing the minority shareholders about the internal affairs of HS. This factor

decreases the risk of material misstatements (Vaicekauskas and Mackevičius 2014).

7. It is mentioned in the provided case of HS that J Audrey Pearce has been auditing the

financial statements of HS for last five years and it means that he is well aware of the

trends of the financial performance and position of HS along with the industry.

Therefore, this is tough for the management of HS to manipulate the financial

accounts in the presence of the auditor that ultimately decreases the risk of material

misstatements.

3. It can be observed from the facts of the case that there is a considerable growth of the

products in which HS deals which increases the scope of the company to deliver more

products for increasing the sales and profitability. This is a crucial aspect that

decreases the risk of material misstatements.

4. It can be seen from the provided information of HS that there is a favourable

availability of funds for the business of HS for the additional mortgages. The

company has been able to continuously sell their mortgages as a source of new

lendable funds. Therefore, the presence of adequate funds decreases the risk of

material misstatements (Al-Khaddash, Al Nawas and Ramadan 2013).

5. It is provided in the case that there has been very little turnover of employees in HS’s

accounting department which indicates towards superior knowledge and skillset of the

employees under this department. Therefore, long-standing employees with effective

accounting skills and knowledge decreases the risk of material misstatements.

6. It can be seen that the internal auditor of HS uses to directly report to the audit

committee chairman who is a minority shareholder instead of George Watson. This

helps in retaining the integrity and honesty of the internal audit team and this keeps

informing the minority shareholders about the internal affairs of HS. This factor

decreases the risk of material misstatements (Vaicekauskas and Mackevičius 2014).

7. It is mentioned in the provided case of HS that J Audrey Pearce has been auditing the

financial statements of HS for last five years and it means that he is well aware of the

trends of the financial performance and position of HS along with the industry.

Therefore, this is tough for the management of HS to manipulate the financial

accounts in the presence of the auditor that ultimately decreases the risk of material

misstatements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

8. It is clearly mentioned in the case that the management of HS has always been

receptive to the suggestion of the auditors on different aspects. This implies the

presence of effective internal control within HS as per the suggestion of the auditor.

This is a crucial fact that reduces the risk of material misstatements in the financial

statements of HS (Vaicekauskas and Mackevičius 2014).

Answer to Question 2

Analysis of the Information

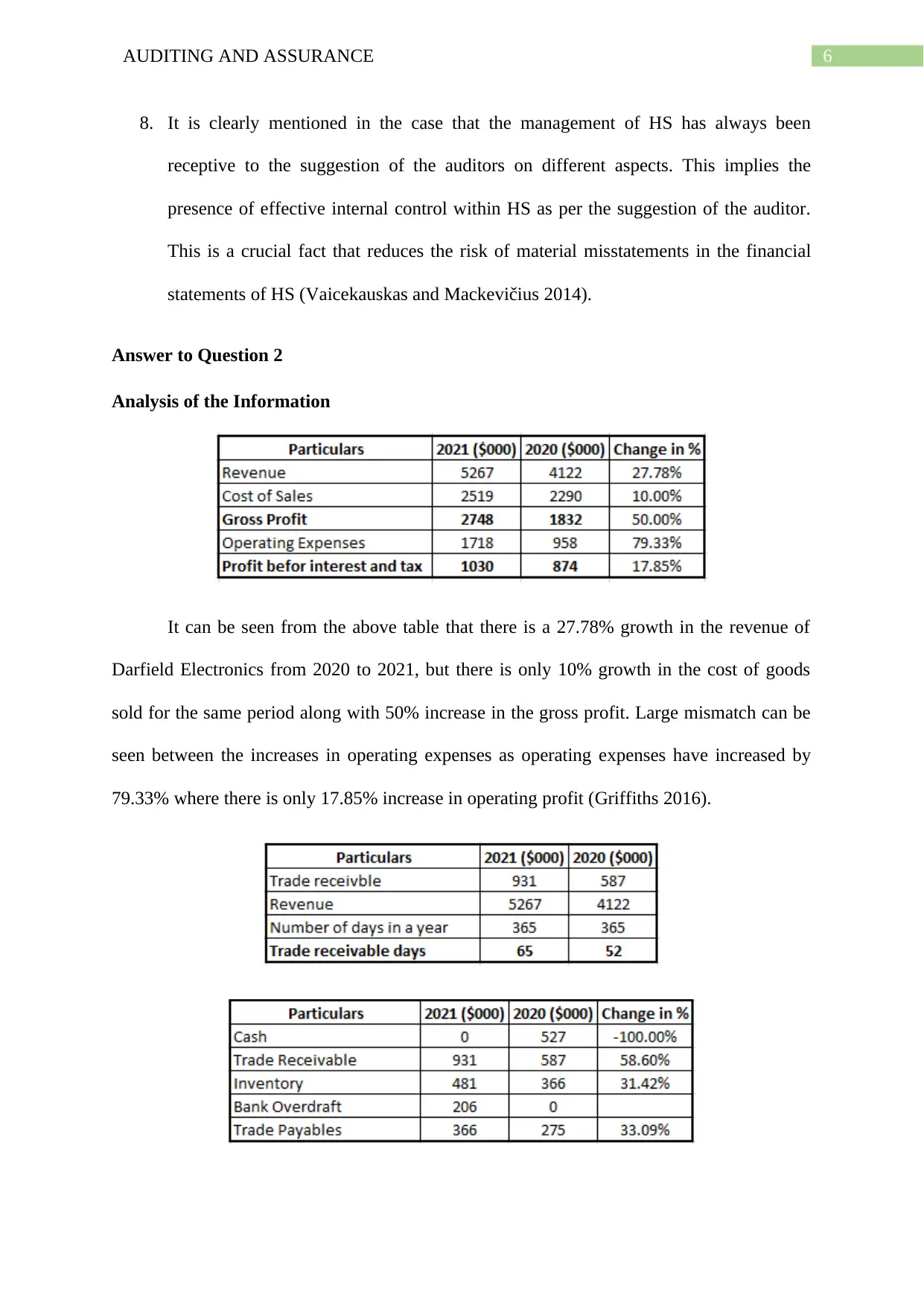

It can be seen from the above table that there is a 27.78% growth in the revenue of

Darfield Electronics from 2020 to 2021, but there is only 10% growth in the cost of goods

sold for the same period along with 50% increase in the gross profit. Large mismatch can be

seen between the increases in operating expenses as operating expenses have increased by

79.33% where there is only 17.85% increase in operating profit (Griffiths 2016).

8. It is clearly mentioned in the case that the management of HS has always been

receptive to the suggestion of the auditors on different aspects. This implies the

presence of effective internal control within HS as per the suggestion of the auditor.

This is a crucial fact that reduces the risk of material misstatements in the financial

statements of HS (Vaicekauskas and Mackevičius 2014).

Answer to Question 2

Analysis of the Information

It can be seen from the above table that there is a 27.78% growth in the revenue of

Darfield Electronics from 2020 to 2021, but there is only 10% growth in the cost of goods

sold for the same period along with 50% increase in the gross profit. Large mismatch can be

seen between the increases in operating expenses as operating expenses have increased by

79.33% where there is only 17.85% increase in operating profit (Griffiths 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

As per the above table, there is an increase in the trade receivable days from 52 days

in 2020 to 65 days in 2021. Large disparity can be seen between the increase in revenue and

receivables as revenue of Darfield Electronics has increased by 27.78% where receivables

have increased by 58.60% that is more than double of revenue (Titera 2013).

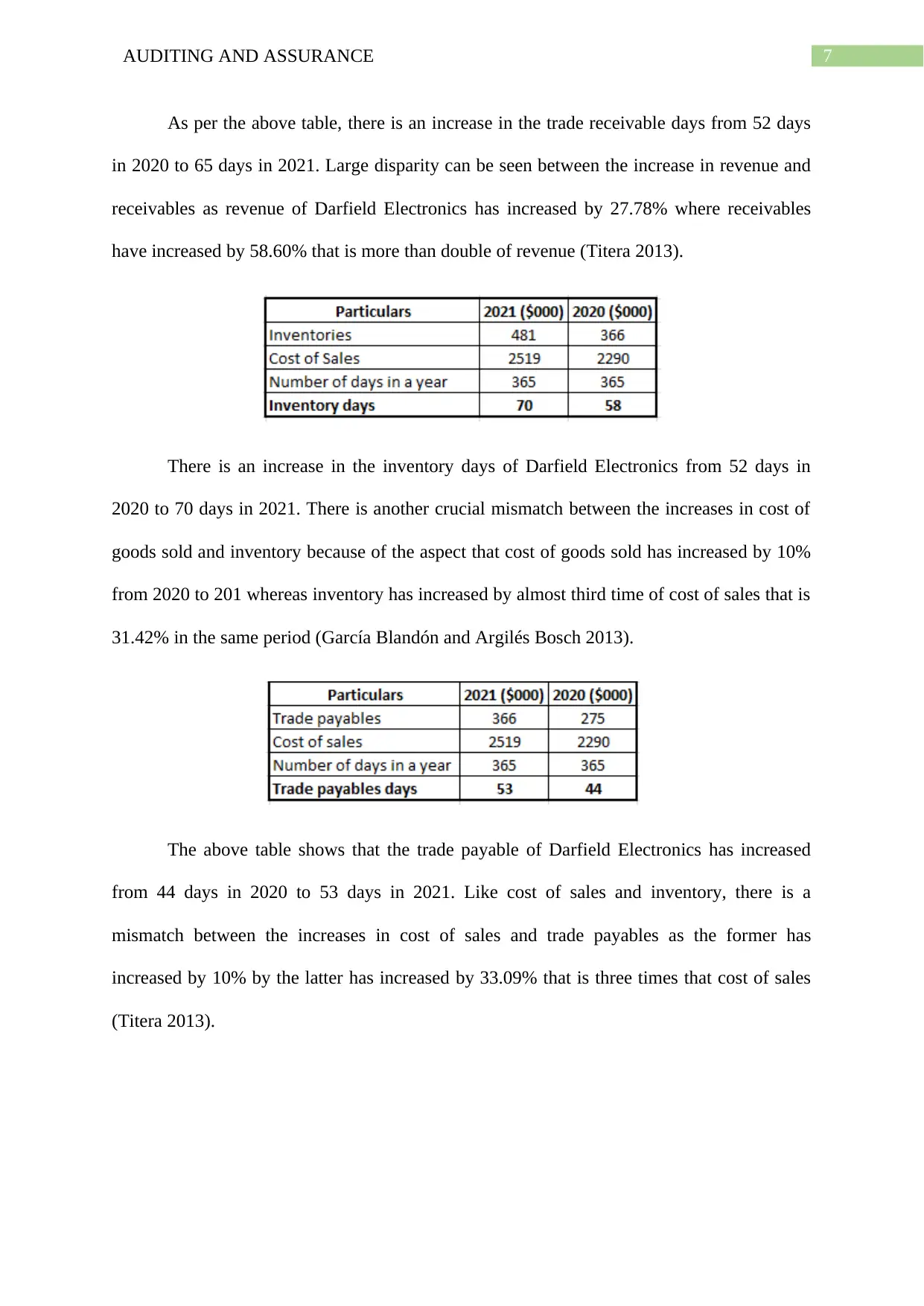

There is an increase in the inventory days of Darfield Electronics from 52 days in

2020 to 70 days in 2021. There is another crucial mismatch between the increases in cost of

goods sold and inventory because of the aspect that cost of goods sold has increased by 10%

from 2020 to 201 whereas inventory has increased by almost third time of cost of sales that is

31.42% in the same period (García Blandón and Argilés Bosch 2013).

The above table shows that the trade payable of Darfield Electronics has increased

from 44 days in 2020 to 53 days in 2021. Like cost of sales and inventory, there is a

mismatch between the increases in cost of sales and trade payables as the former has

increased by 10% by the latter has increased by 33.09% that is three times that cost of sales

(Titera 2013).

As per the above table, there is an increase in the trade receivable days from 52 days

in 2020 to 65 days in 2021. Large disparity can be seen between the increase in revenue and

receivables as revenue of Darfield Electronics has increased by 27.78% where receivables

have increased by 58.60% that is more than double of revenue (Titera 2013).

There is an increase in the inventory days of Darfield Electronics from 52 days in

2020 to 70 days in 2021. There is another crucial mismatch between the increases in cost of

goods sold and inventory because of the aspect that cost of goods sold has increased by 10%

from 2020 to 201 whereas inventory has increased by almost third time of cost of sales that is

31.42% in the same period (García Blandón and Argilés Bosch 2013).

The above table shows that the trade payable of Darfield Electronics has increased

from 44 days in 2020 to 53 days in 2021. Like cost of sales and inventory, there is a

mismatch between the increases in cost of sales and trade payables as the former has

increased by 10% by the latter has increased by 33.09% that is three times that cost of sales

(Titera 2013).

8AUDITING AND ASSURANCE

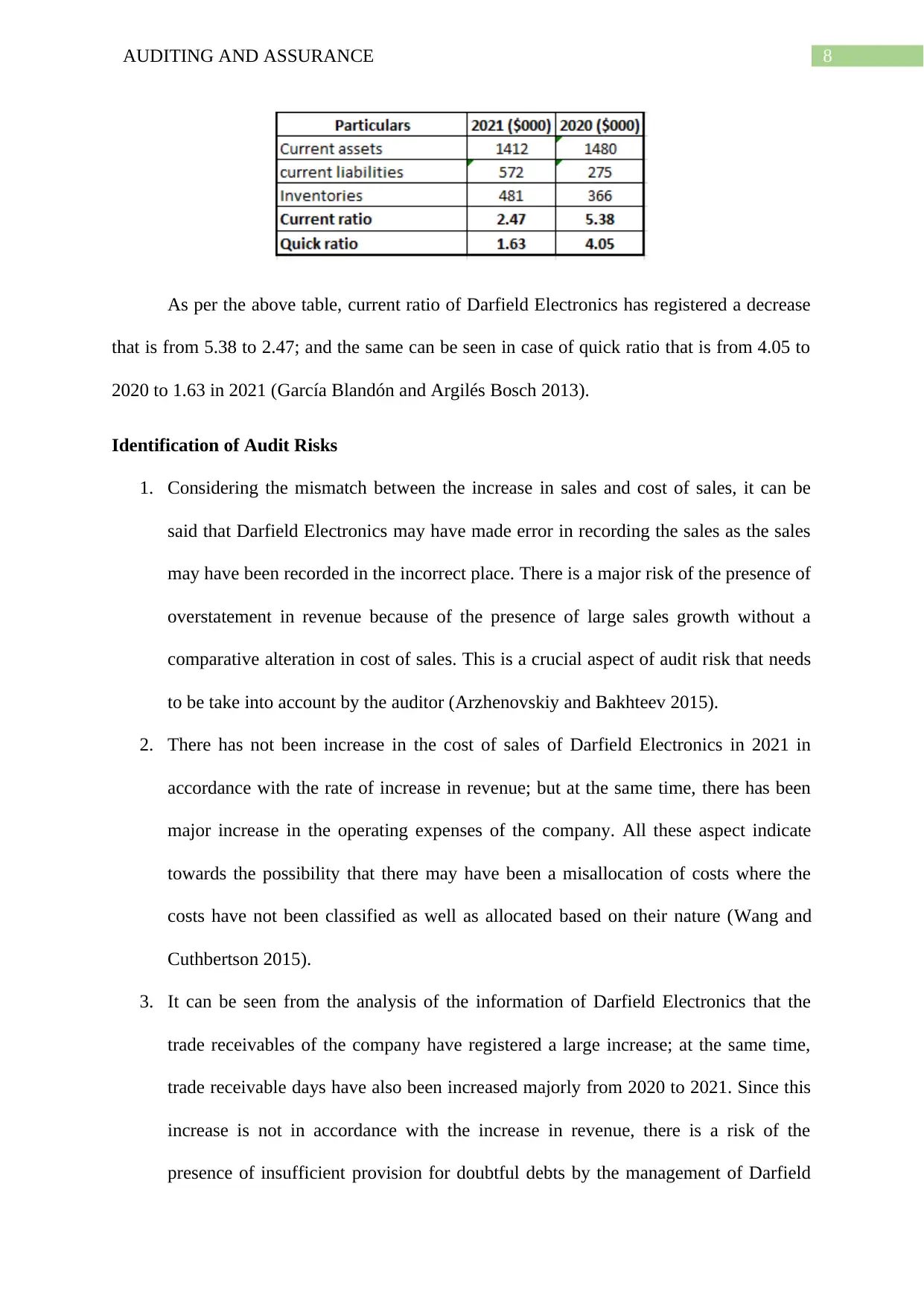

As per the above table, current ratio of Darfield Electronics has registered a decrease

that is from 5.38 to 2.47; and the same can be seen in case of quick ratio that is from 4.05 to

2020 to 1.63 in 2021 (García Blandón and Argilés Bosch 2013).

Identification of Audit Risks

1. Considering the mismatch between the increase in sales and cost of sales, it can be

said that Darfield Electronics may have made error in recording the sales as the sales

may have been recorded in the incorrect place. There is a major risk of the presence of

overstatement in revenue because of the presence of large sales growth without a

comparative alteration in cost of sales. This is a crucial aspect of audit risk that needs

to be take into account by the auditor (Arzhenovskiy and Bakhteev 2015).

2. There has not been increase in the cost of sales of Darfield Electronics in 2021 in

accordance with the rate of increase in revenue; but at the same time, there has been

major increase in the operating expenses of the company. All these aspect indicate

towards the possibility that there may have been a misallocation of costs where the

costs have not been classified as well as allocated based on their nature (Wang and

Cuthbertson 2015).

3. It can be seen from the analysis of the information of Darfield Electronics that the

trade receivables of the company have registered a large increase; at the same time,

trade receivable days have also been increased majorly from 2020 to 2021. Since this

increase is not in accordance with the increase in revenue, there is a risk of the

presence of insufficient provision for doubtful debts by the management of Darfield

As per the above table, current ratio of Darfield Electronics has registered a decrease

that is from 5.38 to 2.47; and the same can be seen in case of quick ratio that is from 4.05 to

2020 to 1.63 in 2021 (García Blandón and Argilés Bosch 2013).

Identification of Audit Risks

1. Considering the mismatch between the increase in sales and cost of sales, it can be

said that Darfield Electronics may have made error in recording the sales as the sales

may have been recorded in the incorrect place. There is a major risk of the presence of

overstatement in revenue because of the presence of large sales growth without a

comparative alteration in cost of sales. This is a crucial aspect of audit risk that needs

to be take into account by the auditor (Arzhenovskiy and Bakhteev 2015).

2. There has not been increase in the cost of sales of Darfield Electronics in 2021 in

accordance with the rate of increase in revenue; but at the same time, there has been

major increase in the operating expenses of the company. All these aspect indicate

towards the possibility that there may have been a misallocation of costs where the

costs have not been classified as well as allocated based on their nature (Wang and

Cuthbertson 2015).

3. It can be seen from the analysis of the information of Darfield Electronics that the

trade receivables of the company have registered a large increase; at the same time,

trade receivable days have also been increased majorly from 2020 to 2021. Since this

increase is not in accordance with the increase in revenue, there is a risk of the

presence of insufficient provision for doubtful debts by the management of Darfield

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Electronics in order to increase the total current liabilities for showing a goods short-

term liquidity position. This needs to be considered by the auditor (Hooda, Bawa and

Rana 2018).

4. Darfield Electronics has registered an increase in the inventory days along with

inventory in 2020 as compared to 2021. Given the large mismatch between the

increases in inventory and cost of sales, it can be said that there is a risk due to the

potential presence of insufficient provision for outdated inventories by the

management of Darfield Electronics. Another possibility is that the management of

Darfield Electronics has not transfer the inventories to the cost of sales that should

have been done. This needs to be considered by the auditor (Wang and Cuthbertson

2015).

5. Earlier analysis shows that both the current ratio as well as quick ratio of Darfield

Electronics have largely fallen in 2021 as compared to 2020. This indicates that

Darfield Electronics is facing major issues in paying off the current business

obligations in the absence of adequate current assets and quick assets. This aspect is

in line with the large increase in trade payable and trade payable days. All these

aspects indicate towards the presence of going concern risk in Darfield Electronics

(Hooda, Bawa and Rana 2018).

Audit Response

1. It is needed for the auditor to undertake cut-off test of sales through obtaining and

acknowledging sales invoices issued by Darfield Electronics in order to check the

customers’ dates of acknowledgement so that it can be assured that the sales invoices

are of same accounting period when the company has recognized the sales (Byrnes et

al. 2018).

Electronics in order to increase the total current liabilities for showing a goods short-

term liquidity position. This needs to be considered by the auditor (Hooda, Bawa and

Rana 2018).

4. Darfield Electronics has registered an increase in the inventory days along with

inventory in 2020 as compared to 2021. Given the large mismatch between the

increases in inventory and cost of sales, it can be said that there is a risk due to the

potential presence of insufficient provision for outdated inventories by the

management of Darfield Electronics. Another possibility is that the management of

Darfield Electronics has not transfer the inventories to the cost of sales that should

have been done. This needs to be considered by the auditor (Wang and Cuthbertson

2015).

5. Earlier analysis shows that both the current ratio as well as quick ratio of Darfield

Electronics have largely fallen in 2021 as compared to 2020. This indicates that

Darfield Electronics is facing major issues in paying off the current business

obligations in the absence of adequate current assets and quick assets. This aspect is

in line with the large increase in trade payable and trade payable days. All these

aspects indicate towards the presence of going concern risk in Darfield Electronics

(Hooda, Bawa and Rana 2018).

Audit Response

1. It is needed for the auditor to undertake cut-off test of sales through obtaining and

acknowledging sales invoices issued by Darfield Electronics in order to check the

customers’ dates of acknowledgement so that it can be assured that the sales invoices

are of same accounting period when the company has recognized the sales (Byrnes et

al. 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

2. Darfield Electronics uses certain valuation process for inventory in order to determine

the values of inventories. It is required for the auditor to verify the fact that the

method mentioned in the financial statements has been followed by the accounting

system of the company. This also helps in determining associated costs with

inventory.

3. In case of trade receivables, the auditor needs to compare trade receivable days to the

last year’s data, review the appropriateness of allowance for doubtful debts by

discussing with the management. Moreover, the auditor is required to examine the

large customer accounts in trade receivables while comparing them with previous

year’s balance (Abdullatif 2013).

4. It is needed for the auditor of Darfield Electronics to test the allocation assertion of

expenses. This requires the auditor to verify whether the expenses have been properly

classified as well as presented in the financial reports of the company.

5. The auditor of Darfield Electronics is needed to assess that whether there is any

material uncertainty in the company that can cast significant doubt on the ability of

the company to continue as a going concern in future. Moreover, the auditor is also

needed to undertake analysing the management’s assessment on the presence of any

material uncertainty, events or circumstances (Daniela and Attila 2013).

Conclusion and Recommendations

The above analysis shows that business organizations have certain factors that

increase the risk of material misstatements and there are certain factors that reduce the

possibility of the risk of material misstatements in the financial statements. For example, high

competitiveness of industry, complex accounting judgment, less profitability and others are

the factors that increase the risk of material misstatements; and factors like effective internal

control, governance mechanism and others reduce the risk of material misstatement. The

2. Darfield Electronics uses certain valuation process for inventory in order to determine

the values of inventories. It is required for the auditor to verify the fact that the

method mentioned in the financial statements has been followed by the accounting

system of the company. This also helps in determining associated costs with

inventory.

3. In case of trade receivables, the auditor needs to compare trade receivable days to the

last year’s data, review the appropriateness of allowance for doubtful debts by

discussing with the management. Moreover, the auditor is required to examine the

large customer accounts in trade receivables while comparing them with previous

year’s balance (Abdullatif 2013).

4. It is needed for the auditor of Darfield Electronics to test the allocation assertion of

expenses. This requires the auditor to verify whether the expenses have been properly

classified as well as presented in the financial reports of the company.

5. The auditor of Darfield Electronics is needed to assess that whether there is any

material uncertainty in the company that can cast significant doubt on the ability of

the company to continue as a going concern in future. Moreover, the auditor is also

needed to undertake analysing the management’s assessment on the presence of any

material uncertainty, events or circumstances (Daniela and Attila 2013).

Conclusion and Recommendations

The above analysis shows that business organizations have certain factors that

increase the risk of material misstatements and there are certain factors that reduce the

possibility of the risk of material misstatements in the financial statements. For example, high

competitiveness of industry, complex accounting judgment, less profitability and others are

the factors that increase the risk of material misstatements; and factors like effective internal

control, governance mechanism and others reduce the risk of material misstatement. The

11AUDITING AND ASSURANCE

above discussion also shows that analysis of financial information helps the auditors in

identifying the audit risk which is required to undertake the appropriate audit procedures by

them.

On the basis of whole discussion, it is recommended to the auditors that they should

design the audit based on the outcome of the analysis of the unaudited financial statements of

the clients. This is helpful for the auditors in identifying the areas that are of high audit risk

and require additional audit attention. Moreover, the auditors are recommended to consider

both types of factors responsible for increasing and decreasing the risk of material

misstatements.

above discussion also shows that analysis of financial information helps the auditors in

identifying the audit risk which is required to undertake the appropriate audit procedures by

them.

On the basis of whole discussion, it is recommended to the auditors that they should

design the audit based on the outcome of the analysis of the unaudited financial statements of

the clients. This is helpful for the auditors in identifying the areas that are of high audit risk

and require additional audit attention. Moreover, the auditors are recommended to consider

both types of factors responsible for increasing and decreasing the risk of material

misstatements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.