Auditing and Assurance: AGL Limited Risk Assessment Report

VerifiedAdded on 2020/05/16

|14

|2475

|64

Report

AI Summary

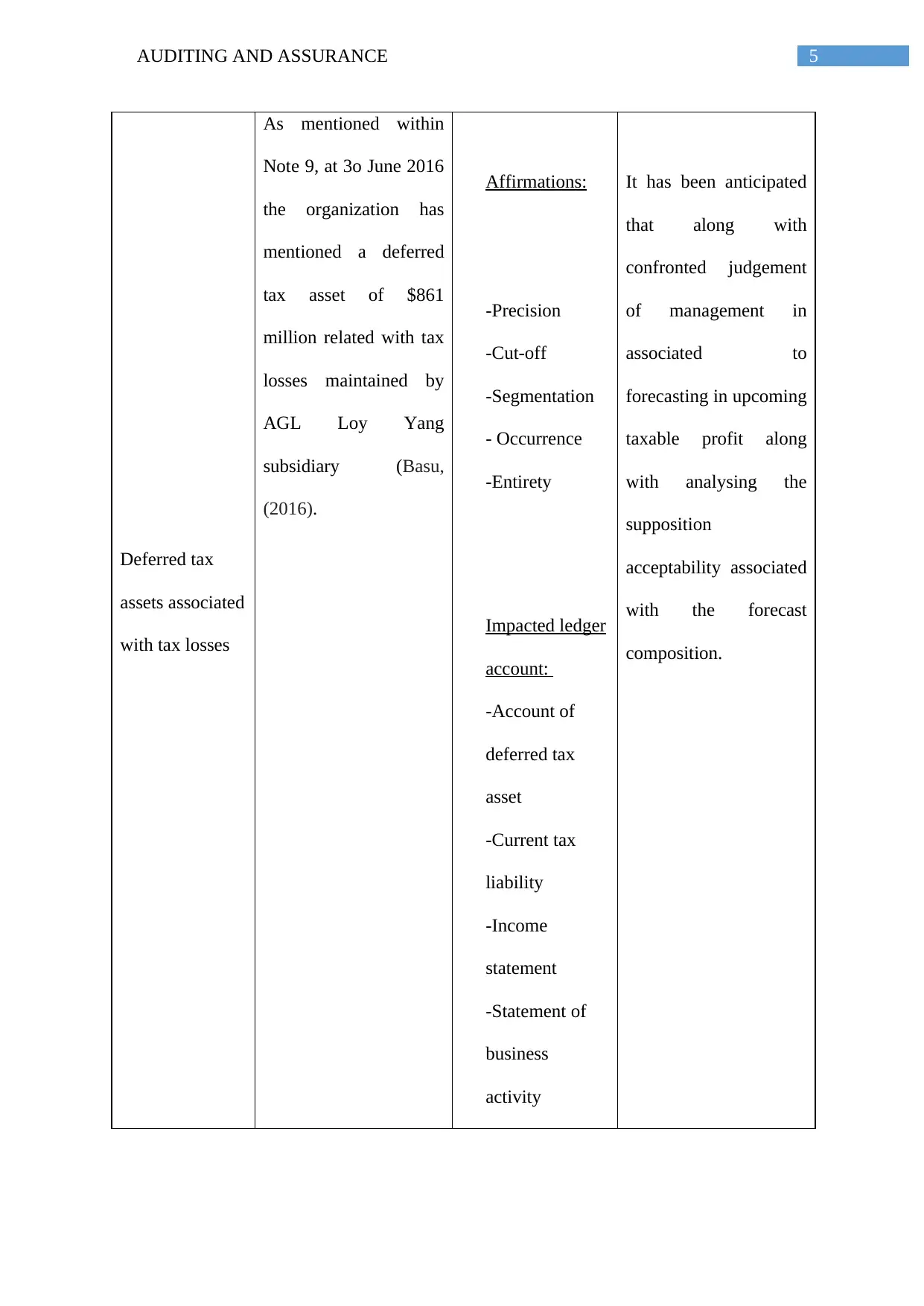

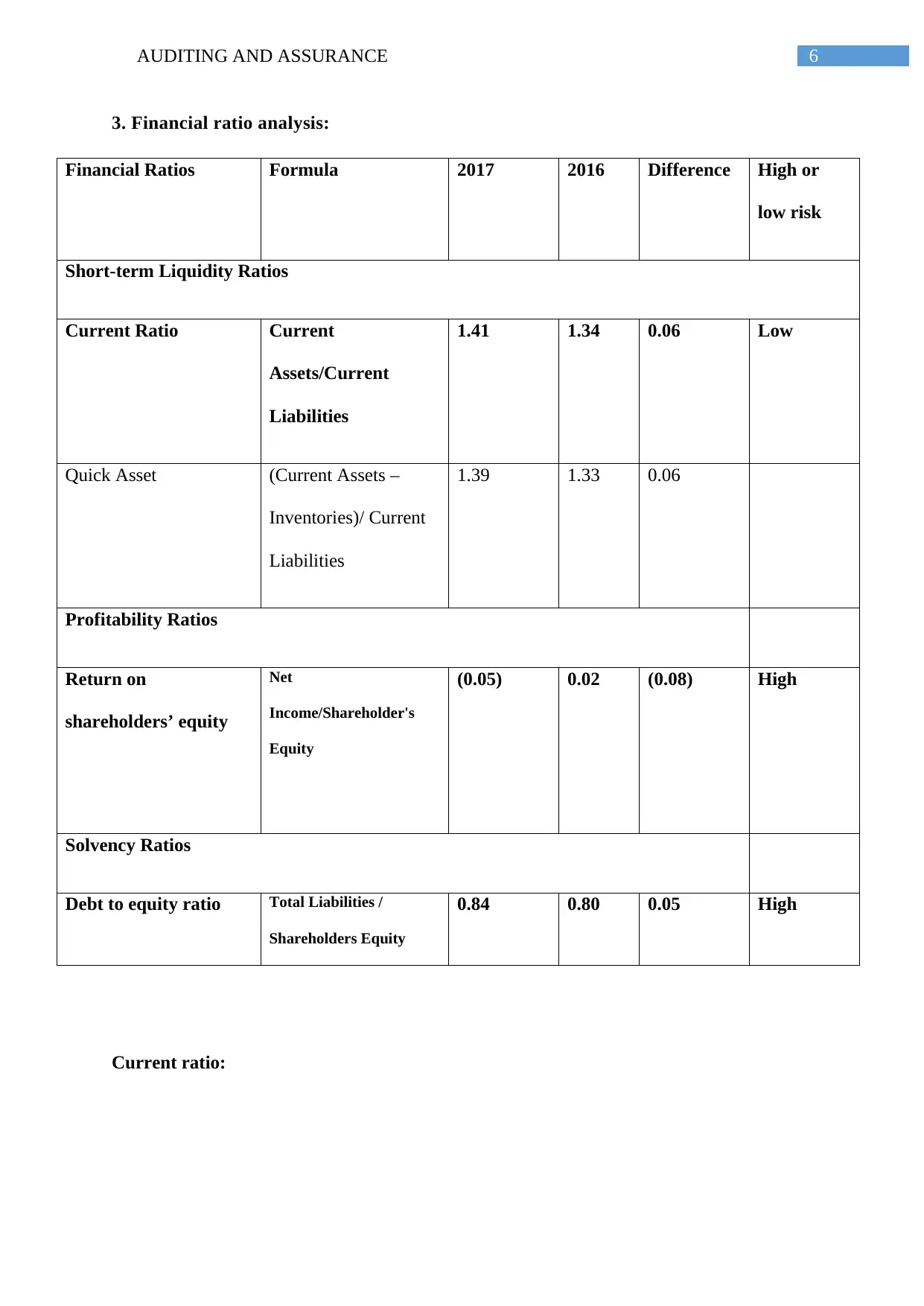

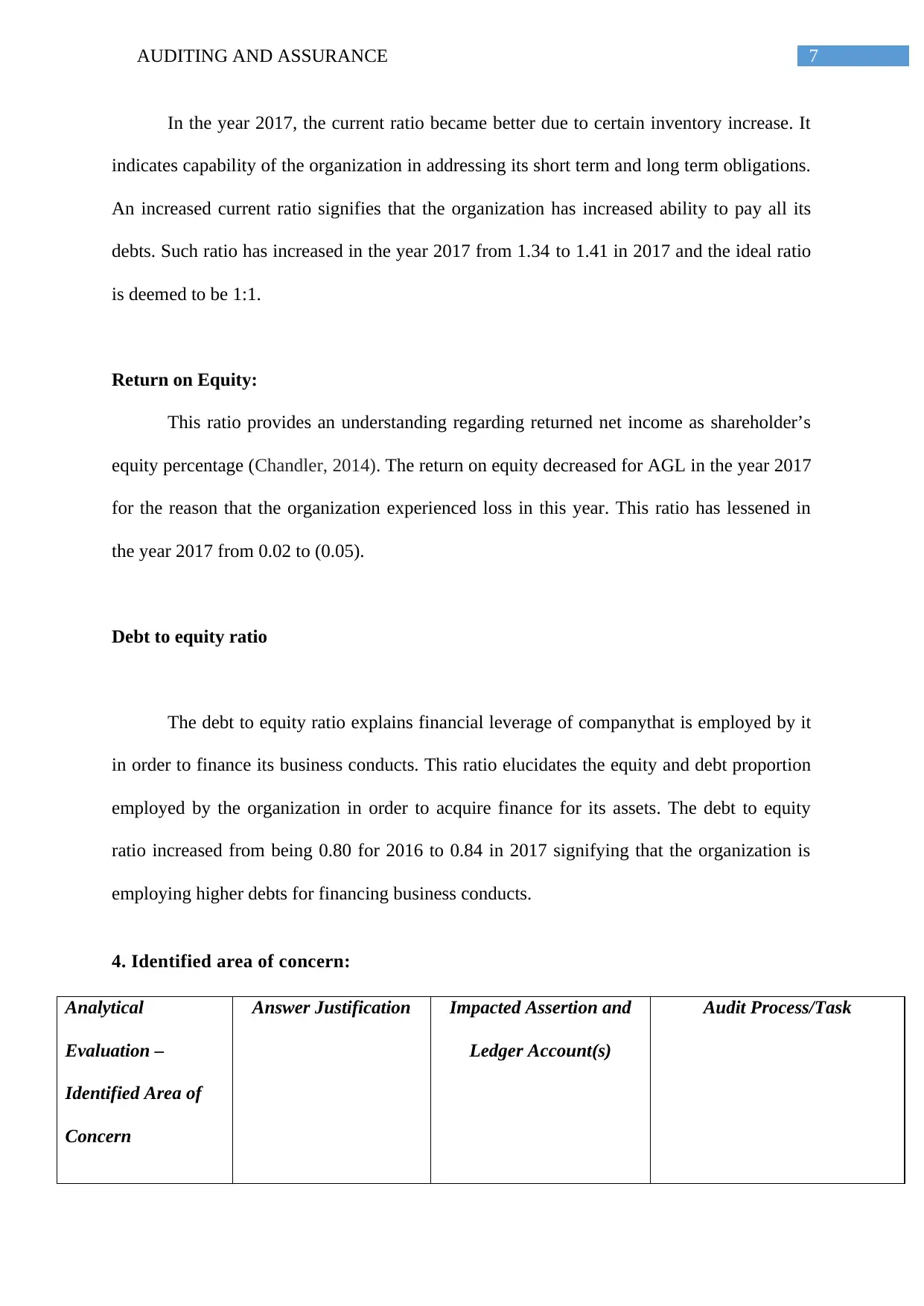

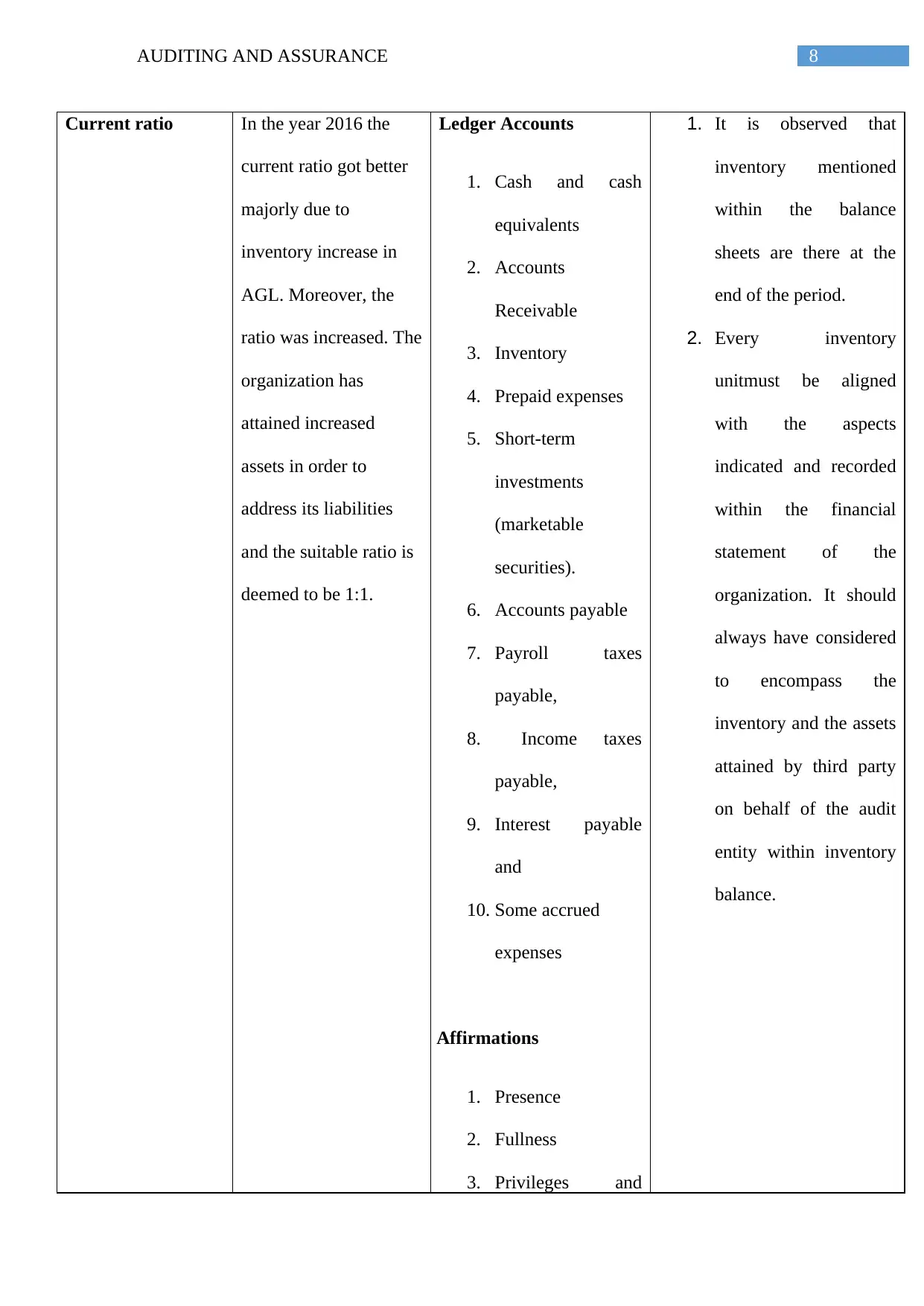

This report presents a risk assessment of AGL Limited, a new client, focusing on developing a thorough risk assessment procedure and suggesting necessary control elements. The report examines inherent risks, impacted ledger accounts, and the audit process, including unbilled revenue, unbilled distribution costs, and deferred tax assets. Financial ratio analysis, including current ratio, return on equity, and debt-to-equity ratio, are evaluated to identify areas of concern. The analysis highlights the importance of the audit committee, its responsibilities, and the nomination of an effective external auditor. The report concludes by emphasizing the significance of professional judgment in auditing and the role of the audit committee in ensuring fair financial reporting, providing valuable insights for shareholders. The report also discusses the control elements and the role of the audit report, audit documentation, and professional skepticism in the audit process.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.