Auditing and Assurance: ASA 315, ASA 520 and Analytical Procedures

VerifiedAdded on 2021/05/31

|7

|1314

|53

Report

AI Summary

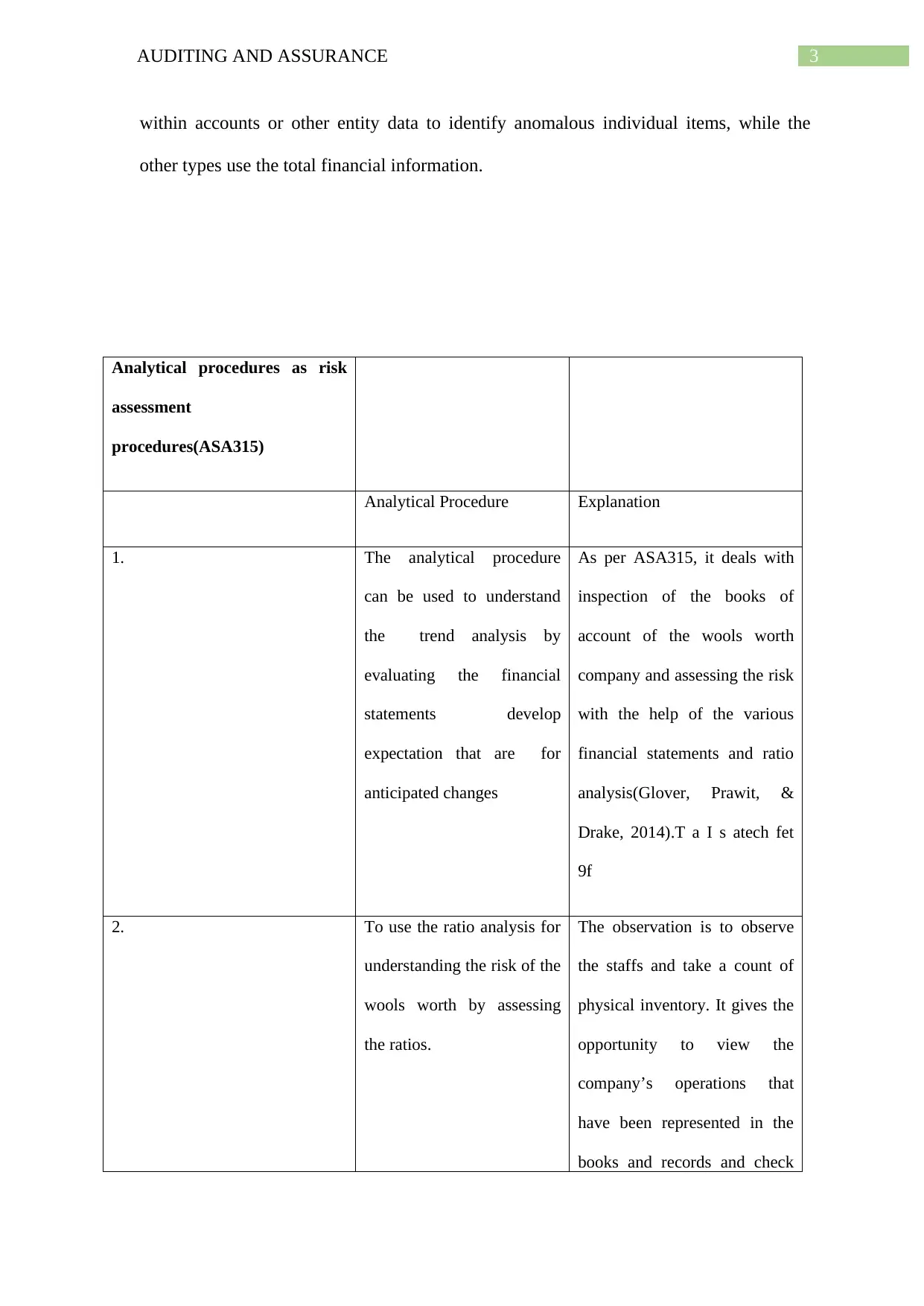

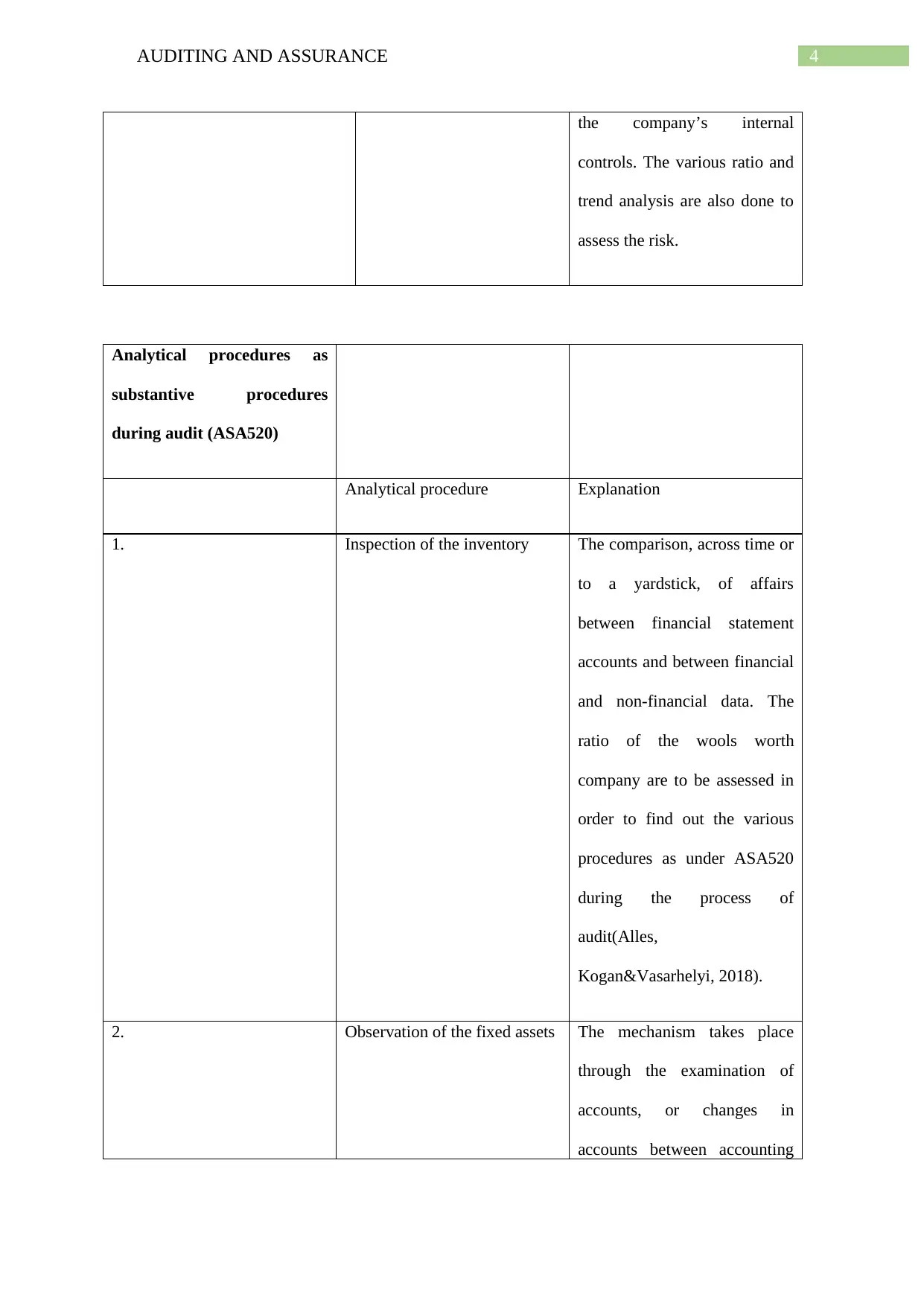

This report provides a comprehensive overview of auditing and assurance, specifically focusing on Australian Accounting Standards ASA 315 and ASA 520. ASA 315 addresses the auditor's responsibility in identifying and assessing the risk of material misstatement in a company's financial reports, considering the company's environment and internal controls. ASA 520 focuses on the auditor's use of analytical procedures as substantive procedures to form an overall conclusion on financial statements. The report details how analytical procedures are used in both risk assessment and substantive procedures, including ratio analysis, trend analysis, and reasonableness testing. It also explores specific examples like inspection of inventory and observation of fixed assets. The report emphasizes the importance of selecting appropriate analytical procedures based on the desired level of assurance and professional judgment. References to relevant literature support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.