Comprehensive Auditing Report: Financial Review of SECOS Group Limited

VerifiedAdded on 2020/12/29

|15

|3477

|394

Report

AI Summary

This report presents an audit analysis of SECOS Group Limited, a manufacturer and distributor of packaging materials. It begins with an introduction to auditing and the chosen company. The report then details the company's business, including its market capitalization and ownership structure. It examines business risk, risk of material misstatement (inherent, control, and detection risks), and the audit risk model. Analytical procedures, including key ratio calculations (current ratio, inventory turnover, gross margin, and debt-to-equity ratio) are presented and interpreted. The report also covers materiality, outlining account balances and related audit procedures for cash and cash equivalents, and receivables. Finally, it includes audit work steps for cash and cash equivalents, and receivables. This report is contributed by a student to be published on the website Desklib.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................7

TASK 5............................................................................................................................................9

TASK 6..........................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERECNES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................7

TASK 5............................................................................................................................................9

TASK 6..........................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERECNES..............................................................................................................................15

INTRODUCTION

Audit is an inspection of various books of accounts of an entity with a view to ascertain a

fair and true picture of financial position. It is conducted by an auditor and he can be an external

party or an employee of the company. It helps in finding the material risk or error that could

affect the company to a great extent. The investors rely on the audited annual report for making

investment decisions (Chen and et. al., 2012). Therefore, it is important to conduct audit. Audit

can be compulsory or voluntary. There are two types of audit i.e. financial audit and management

audit. The chosen company in the project report is SECOS Group. The report covers, the

material account balances that may affect the company, audit work for addressing such balances

along with its respective assertions for gathering evidence to prove the materiality.

TASK 1

SECOS Group Limited is a manufacturer and distributor of packaging material across the

world. Its headquarters are situated at Mount Waverley, Australia. It was a result of merger of

Cardia Bioplastic and Stellar Films Group in April 2015. it produces and sells its high quality

cast films and provides renewable sustainable plastic materials for packaging and plastic

products industries. The company holds a robust patent portfolio and it is following a business

trend by going global through sustainable packaging. It has a Product Development Centre and

manufacturing plant of its own finished products and resins in China and the manufacturing unit

of cast films is located in Australia and Malaysia. Along with this, it has sales and distribution

channels in across the globe.

Audit is an inspection of various books of accounts of an entity with a view to ascertain a

fair and true picture of financial position. It is conducted by an auditor and he can be an external

party or an employee of the company. It helps in finding the material risk or error that could

affect the company to a great extent. The investors rely on the audited annual report for making

investment decisions (Chen and et. al., 2012). Therefore, it is important to conduct audit. Audit

can be compulsory or voluntary. There are two types of audit i.e. financial audit and management

audit. The chosen company in the project report is SECOS Group. The report covers, the

material account balances that may affect the company, audit work for addressing such balances

along with its respective assertions for gathering evidence to prove the materiality.

TASK 1

SECOS Group Limited is a manufacturer and distributor of packaging material across the

world. Its headquarters are situated at Mount Waverley, Australia. It was a result of merger of

Cardia Bioplastic and Stellar Films Group in April 2015. it produces and sells its high quality

cast films and provides renewable sustainable plastic materials for packaging and plastic

products industries. The company holds a robust patent portfolio and it is following a business

trend by going global through sustainable packaging. It has a Product Development Centre and

manufacturing plant of its own finished products and resins in China and the manufacturing unit

of cast films is located in Australia and Malaysia. Along with this, it has sales and distribution

channels in across the globe.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Business Risk- are non-financial risk, that assesses company's industry, its applicable

regulations and use of technology. An entity may have lower profits than the estimated profits

for the year. The factors included in this risk are input costs, competition, sales-volume, per unit

cost, climate affecting the economic stability and government regulations. Further, it includes an

internal review of company's survival in the future. The auditor will form an understanding

about the SECOS' business, the environment that is it operating in and its internal control.

SECOS Group Ltd. Is a small capital stock company that has a market capitalization of USD $8

Million. Since the company does not have huge market capitalization, there is a threat on its

survival because of its financial viability. The ownership structure of the company may affect its

short- term and long-term performance.

Risk of material misstatement- The risk that occurs due to the errors in financial

statements of an organization. Such situation arise when there is a difference between the figures

recorded and the estimated figures that will be included in financial statement to provide a fair

view of the company. It calculate the degree of material risk and is calculated at the assertion

level. It is subdivided into two categories viz. Inherent risk and control risk.

Inherent risk- refers to the possibility of incorrect or misleading data in accounting

records due to reasons other than failure of controls. It is the risk involved in the critical

transactions of the company. The inherent risk of SECOS Group limited is low, as the company

has been established in 2015 only, therefore it review and manages its internal control

effectively. Also, the auditors conduct the audit of the company, which reduces this risk as there

are low chances of errors in the transactions done during the year.

Control risk- occurs when there is material misstatement in the financial statements and

the reason for such misstatement is due to the failure of controls and practices used by the entity.

The factors affecting these risks range from industry practices, non-routine transactions, previous

audit results, audit decision regarding the recorded balances and transactions, related parties

transactions, misappropriation of assets etc.

Detection risk- It is the risk that assumes that auditor will not be able to assess or detect

a misstatement that subsist in an assertion of financial statements that could materially affect the

company. This means there are very high chances that the auditor will fail to find material

Business Risk- are non-financial risk, that assesses company's industry, its applicable

regulations and use of technology. An entity may have lower profits than the estimated profits

for the year. The factors included in this risk are input costs, competition, sales-volume, per unit

cost, climate affecting the economic stability and government regulations. Further, it includes an

internal review of company's survival in the future. The auditor will form an understanding

about the SECOS' business, the environment that is it operating in and its internal control.

SECOS Group Ltd. Is a small capital stock company that has a market capitalization of USD $8

Million. Since the company does not have huge market capitalization, there is a threat on its

survival because of its financial viability. The ownership structure of the company may affect its

short- term and long-term performance.

Risk of material misstatement- The risk that occurs due to the errors in financial

statements of an organization. Such situation arise when there is a difference between the figures

recorded and the estimated figures that will be included in financial statement to provide a fair

view of the company. It calculate the degree of material risk and is calculated at the assertion

level. It is subdivided into two categories viz. Inherent risk and control risk.

Inherent risk- refers to the possibility of incorrect or misleading data in accounting

records due to reasons other than failure of controls. It is the risk involved in the critical

transactions of the company. The inherent risk of SECOS Group limited is low, as the company

has been established in 2015 only, therefore it review and manages its internal control

effectively. Also, the auditors conduct the audit of the company, which reduces this risk as there

are low chances of errors in the transactions done during the year.

Control risk- occurs when there is material misstatement in the financial statements and

the reason for such misstatement is due to the failure of controls and practices used by the entity.

The factors affecting these risks range from industry practices, non-routine transactions, previous

audit results, audit decision regarding the recorded balances and transactions, related parties

transactions, misappropriation of assets etc.

Detection risk- It is the risk that assumes that auditor will not be able to assess or detect

a misstatement that subsist in an assertion of financial statements that could materially affect the

company. This means there are very high chances that the auditor will fail to find material

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

misstatement even through substantive test and analysis. The audit report will provide that no

material errors are present in the data.

Audit risk- This risk is also known as residual risk. It means that an auditor will present

an unqualified report because of the failure to detect material misstatement due to fraud or error.

In this risk, the financial statements provided are free of any material misstatement. The

disclosure of the risk may have a impact on the decision making of the investors. The company

may calculate the overall risk by applying Audit Risk Model. The formula is :

AR = ƒ[IR*CR*DR]

Where, AR = Audit Risk

IR = Inherent Risk

CR= Control Risk

DR = Detection Risk

The inherent and control risk could affect the company as wrong opinion of auditor

formed on the basis of the recorded transaction will provide a negative image in the eyes of

investors. The judgement of the auditor is important at the time of disclosing the financial

position of the entity. The detection risk greatly depends on these two risks as the auditor should

find out the misleading information and the audit risk is the product of inherent, control and

detection risk.

TASK 3

Analytical procedures of SECOS by using various ratios:

Analytical procedures- The auditor use these procedures in the financial audit to assess

the potential risk exist in the business operations of the company. After identification of the

risks, they are required to be addressed by taking proper audit actions and plans. For applying the

actions, the auditor must understand the finances of the organization, the environment it is

operating in and history. The procedure starts from preliminary analytical review then

substantive analytical review and lastly, the final analytical review.

Key Ratios Calculation of SECOS Group Limited:

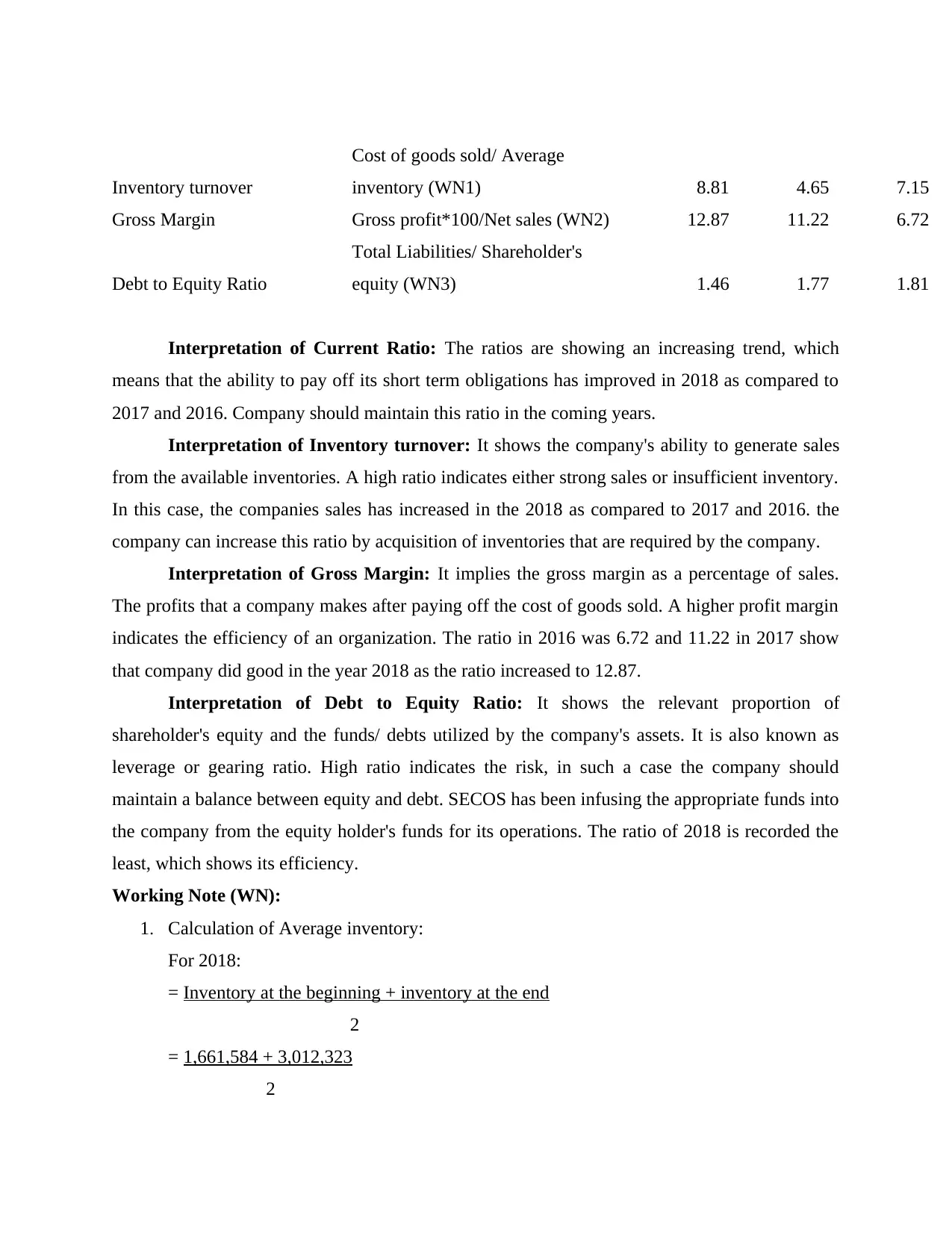

Ratios formula 2018 2017 2016

Current ratio Current Assets/ Current Liabilities 1.78 0.94 0.87

material errors are present in the data.

Audit risk- This risk is also known as residual risk. It means that an auditor will present

an unqualified report because of the failure to detect material misstatement due to fraud or error.

In this risk, the financial statements provided are free of any material misstatement. The

disclosure of the risk may have a impact on the decision making of the investors. The company

may calculate the overall risk by applying Audit Risk Model. The formula is :

AR = ƒ[IR*CR*DR]

Where, AR = Audit Risk

IR = Inherent Risk

CR= Control Risk

DR = Detection Risk

The inherent and control risk could affect the company as wrong opinion of auditor

formed on the basis of the recorded transaction will provide a negative image in the eyes of

investors. The judgement of the auditor is important at the time of disclosing the financial

position of the entity. The detection risk greatly depends on these two risks as the auditor should

find out the misleading information and the audit risk is the product of inherent, control and

detection risk.

TASK 3

Analytical procedures of SECOS by using various ratios:

Analytical procedures- The auditor use these procedures in the financial audit to assess

the potential risk exist in the business operations of the company. After identification of the

risks, they are required to be addressed by taking proper audit actions and plans. For applying the

actions, the auditor must understand the finances of the organization, the environment it is

operating in and history. The procedure starts from preliminary analytical review then

substantive analytical review and lastly, the final analytical review.

Key Ratios Calculation of SECOS Group Limited:

Ratios formula 2018 2017 2016

Current ratio Current Assets/ Current Liabilities 1.78 0.94 0.87

Inventory turnover

Cost of goods sold/ Average

inventory (WN1) 8.81 4.65 7.15

Gross Margin Gross profit*100/Net sales (WN2) 12.87 11.22 6.72

Debt to Equity Ratio

Total Liabilities/ Shareholder's

equity (WN3) 1.46 1.77 1.81

Interpretation of Current Ratio: The ratios are showing an increasing trend, which

means that the ability to pay off its short term obligations has improved in 2018 as compared to

2017 and 2016. Company should maintain this ratio in the coming years.

Interpretation of Inventory turnover: It shows the company's ability to generate sales

from the available inventories. A high ratio indicates either strong sales or insufficient inventory.

In this case, the companies sales has increased in the 2018 as compared to 2017 and 2016. the

company can increase this ratio by acquisition of inventories that are required by the company.

Interpretation of Gross Margin: It implies the gross margin as a percentage of sales.

The profits that a company makes after paying off the cost of goods sold. A higher profit margin

indicates the efficiency of an organization. The ratio in 2016 was 6.72 and 11.22 in 2017 show

that company did good in the year 2018 as the ratio increased to 12.87.

Interpretation of Debt to Equity Ratio: It shows the relevant proportion of

shareholder's equity and the funds/ debts utilized by the company's assets. It is also known as

leverage or gearing ratio. High ratio indicates the risk, in such a case the company should

maintain a balance between equity and debt. SECOS has been infusing the appropriate funds into

the company from the equity holder's funds for its operations. The ratio of 2018 is recorded the

least, which shows its efficiency.

Working Note (WN):

1. Calculation of Average inventory:

For 2018:

= Inventory at the beginning + inventory at the end

2

= 1,661,584 + 3,012,323

2

Cost of goods sold/ Average

inventory (WN1) 8.81 4.65 7.15

Gross Margin Gross profit*100/Net sales (WN2) 12.87 11.22 6.72

Debt to Equity Ratio

Total Liabilities/ Shareholder's

equity (WN3) 1.46 1.77 1.81

Interpretation of Current Ratio: The ratios are showing an increasing trend, which

means that the ability to pay off its short term obligations has improved in 2018 as compared to

2017 and 2016. Company should maintain this ratio in the coming years.

Interpretation of Inventory turnover: It shows the company's ability to generate sales

from the available inventories. A high ratio indicates either strong sales or insufficient inventory.

In this case, the companies sales has increased in the 2018 as compared to 2017 and 2016. the

company can increase this ratio by acquisition of inventories that are required by the company.

Interpretation of Gross Margin: It implies the gross margin as a percentage of sales.

The profits that a company makes after paying off the cost of goods sold. A higher profit margin

indicates the efficiency of an organization. The ratio in 2016 was 6.72 and 11.22 in 2017 show

that company did good in the year 2018 as the ratio increased to 12.87.

Interpretation of Debt to Equity Ratio: It shows the relevant proportion of

shareholder's equity and the funds/ debts utilized by the company's assets. It is also known as

leverage or gearing ratio. High ratio indicates the risk, in such a case the company should

maintain a balance between equity and debt. SECOS has been infusing the appropriate funds into

the company from the equity holder's funds for its operations. The ratio of 2018 is recorded the

least, which shows its efficiency.

Working Note (WN):

1. Calculation of Average inventory:

For 2018:

= Inventory at the beginning + inventory at the end

2

= 1,661,584 + 3,012,323

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 2,337,082

For 2017:

= 1661584+2606413/2 = 2133999

For 2016:

= 2606413+2940902/2 = 2773657.5

2. Revenue has been taken as Net sales.

3. Shareholder's equity has been calculated by deducting Total Liabilities from Total Assets.

For 2018:

= Total Assets – Total Liabilities

= 17,791,313 - 10,567,363

= 7,223,950

For 2017:

= 15684378-10030321

= 5654057

For 2016:

= 13570997-8747256

= 4823741

TASK 4

Materiality implies the impact of an omission or misstatement of an information in an

entity's financial statements. It affects the decision of investors. The material balances includes

those assets and liabilities, which if increased or decreased will impact the data stated in financial

statements. The account balance is the amount recorded in the financial statement. The

materiality in such balances mean the error or omission in the figures at the time preparing the

financial statements of a company. No company shall take such materiality easy. The auditor

should find the error while preparing the statements as the decision of investors will be based on

that report. For this purpose, the auditor shall plan the complete procedure as per the requirement

of the organization and also the transaction done by it in the year. The planning also depends on

the future proposals of the company. Usually, the chances of materiality is high in big companies

as huge number of transactions are being carried by the company during the year, hence a proper

For 2017:

= 1661584+2606413/2 = 2133999

For 2016:

= 2606413+2940902/2 = 2773657.5

2. Revenue has been taken as Net sales.

3. Shareholder's equity has been calculated by deducting Total Liabilities from Total Assets.

For 2018:

= Total Assets – Total Liabilities

= 17,791,313 - 10,567,363

= 7,223,950

For 2017:

= 15684378-10030321

= 5654057

For 2016:

= 13570997-8747256

= 4823741

TASK 4

Materiality implies the impact of an omission or misstatement of an information in an

entity's financial statements. It affects the decision of investors. The material balances includes

those assets and liabilities, which if increased or decreased will impact the data stated in financial

statements. The account balance is the amount recorded in the financial statement. The

materiality in such balances mean the error or omission in the figures at the time preparing the

financial statements of a company. No company shall take such materiality easy. The auditor

should find the error while preparing the statements as the decision of investors will be based on

that report. For this purpose, the auditor shall plan the complete procedure as per the requirement

of the organization and also the transaction done by it in the year. The planning also depends on

the future proposals of the company. Usually, the chances of materiality is high in big companies

as huge number of transactions are being carried by the company during the year, hence a proper

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

plan will help the auditor to conduct the audit and provide a report which will depict true

financial position of the company.

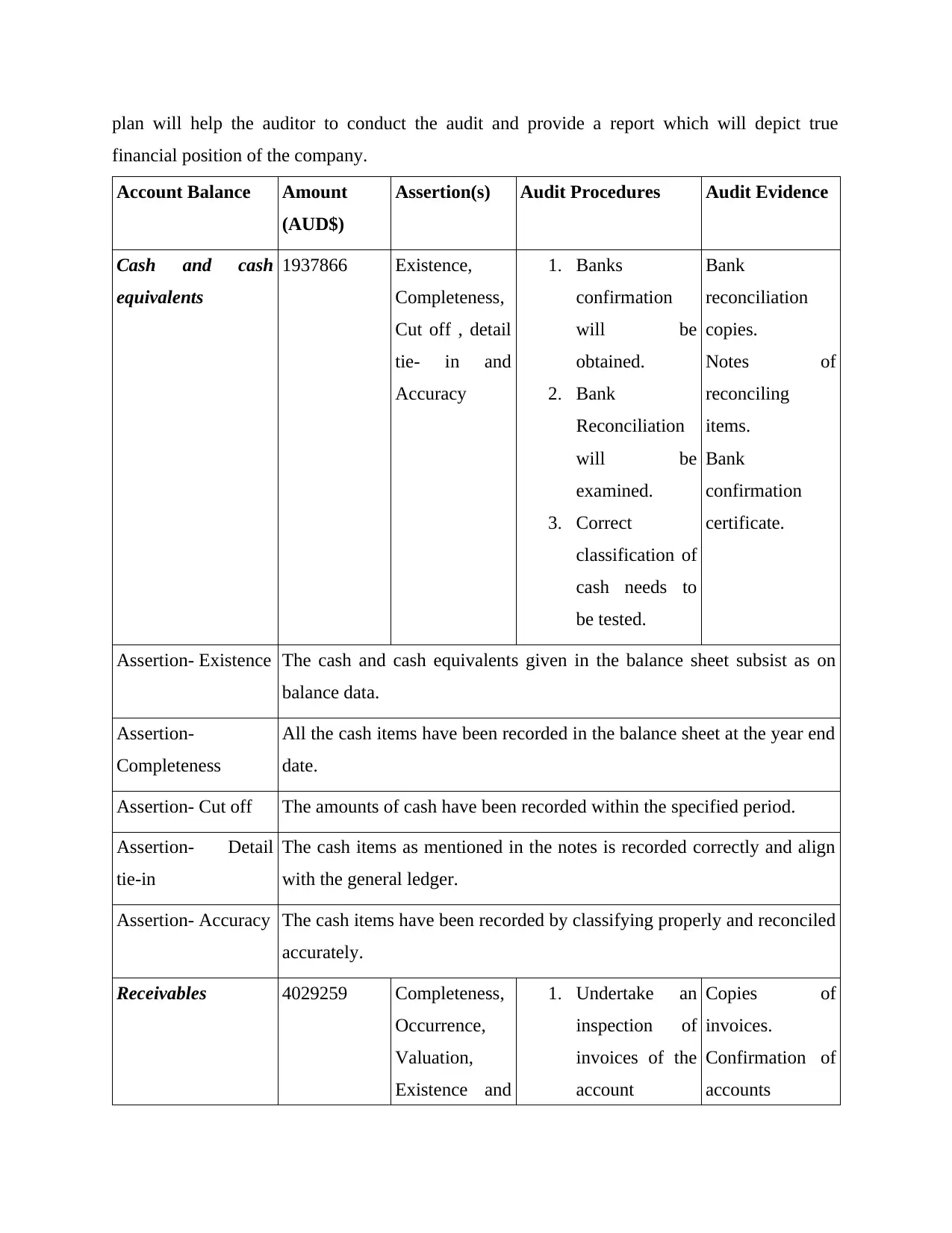

Account Balance Amount

(AUD$)

Assertion(s) Audit Procedures Audit Evidence

Cash and cash

equivalents

1937866 Existence,

Completeness,

Cut off , detail

tie- in and

Accuracy

1. Banks

confirmation

will be

obtained.

2. Bank

Reconciliation

will be

examined.

3. Correct

classification of

cash needs to

be tested.

Bank

reconciliation

copies.

Notes of

reconciling

items.

Bank

confirmation

certificate.

Assertion- Existence The cash and cash equivalents given in the balance sheet subsist as on

balance data.

Assertion-

Completeness

All the cash items have been recorded in the balance sheet at the year end

date.

Assertion- Cut off The amounts of cash have been recorded within the specified period.

Assertion- Detail

tie-in

The cash items as mentioned in the notes is recorded correctly and align

with the general ledger.

Assertion- Accuracy The cash items have been recorded by classifying properly and reconciled

accurately.

Receivables 4029259 Completeness,

Occurrence,

Valuation,

Existence and

1. Undertake an

inspection of

invoices of the

account

Copies of

invoices.

Confirmation of

accounts

financial position of the company.

Account Balance Amount

(AUD$)

Assertion(s) Audit Procedures Audit Evidence

Cash and cash

equivalents

1937866 Existence,

Completeness,

Cut off , detail

tie- in and

Accuracy

1. Banks

confirmation

will be

obtained.

2. Bank

Reconciliation

will be

examined.

3. Correct

classification of

cash needs to

be tested.

Bank

reconciliation

copies.

Notes of

reconciling

items.

Bank

confirmation

certificate.

Assertion- Existence The cash and cash equivalents given in the balance sheet subsist as on

balance data.

Assertion-

Completeness

All the cash items have been recorded in the balance sheet at the year end

date.

Assertion- Cut off The amounts of cash have been recorded within the specified period.

Assertion- Detail

tie-in

The cash items as mentioned in the notes is recorded correctly and align

with the general ledger.

Assertion- Accuracy The cash items have been recorded by classifying properly and reconciled

accurately.

Receivables 4029259 Completeness,

Occurrence,

Valuation,

Existence and

1. Undertake an

inspection of

invoices of the

account

Copies of

invoices.

Confirmation of

accounts

disclosure. receivables.

2. Test the

reconciliation

of receivable

with general

ledger.

3. Contact the

customers to

confirm the

accounts

receivables.

4. Asses the bad

debts written

off during the

period.

receivables.

Receivables

report.

Cash receipts.

Assertion-

Completeness

The receivables amount shown in the balance sheet is the

TASK 5

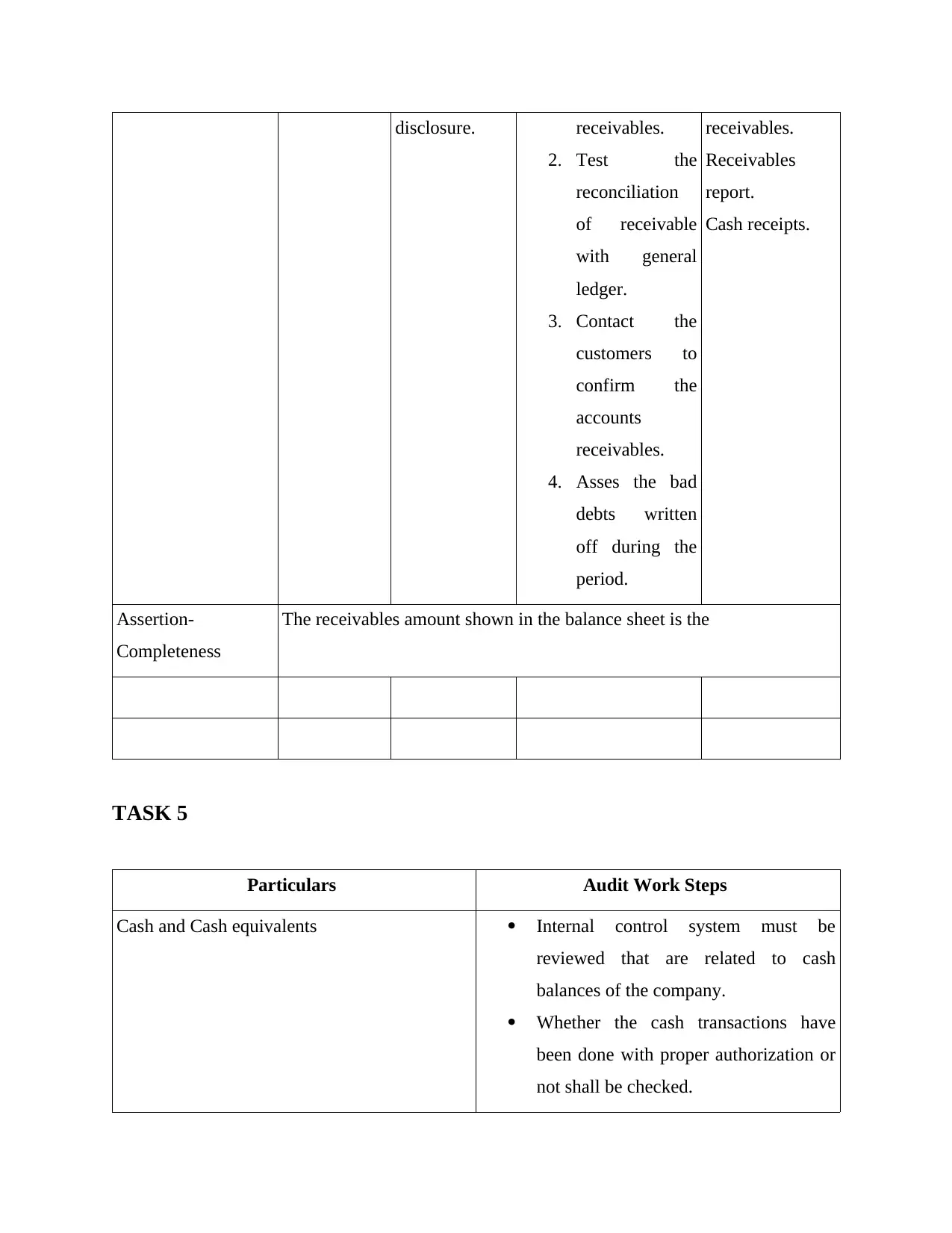

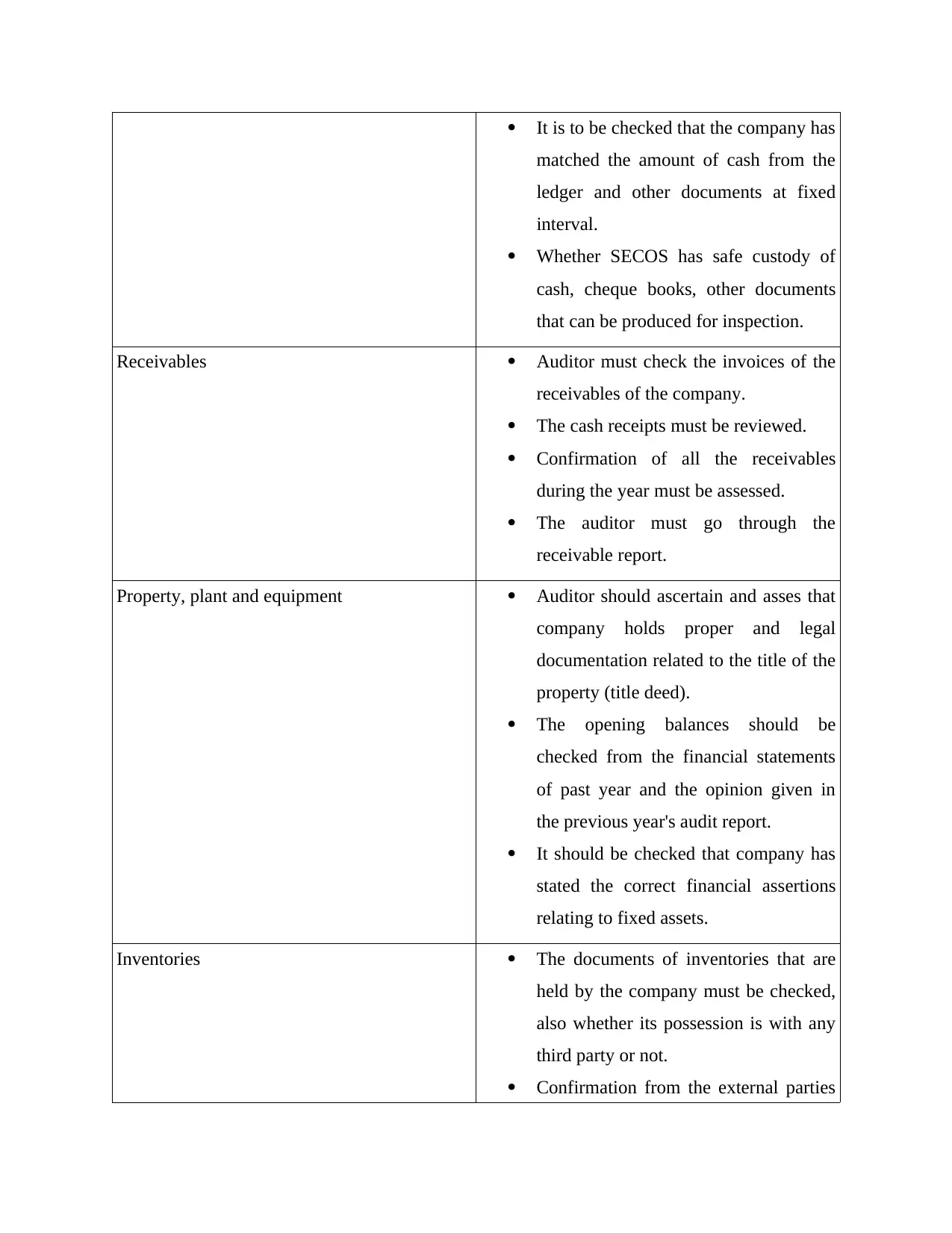

Particulars Audit Work Steps

Cash and Cash equivalents Internal control system must be

reviewed that are related to cash

balances of the company.

Whether the cash transactions have

been done with proper authorization or

not shall be checked.

2. Test the

reconciliation

of receivable

with general

ledger.

3. Contact the

customers to

confirm the

accounts

receivables.

4. Asses the bad

debts written

off during the

period.

receivables.

Receivables

report.

Cash receipts.

Assertion-

Completeness

The receivables amount shown in the balance sheet is the

TASK 5

Particulars Audit Work Steps

Cash and Cash equivalents Internal control system must be

reviewed that are related to cash

balances of the company.

Whether the cash transactions have

been done with proper authorization or

not shall be checked.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is to be checked that the company has

matched the amount of cash from the

ledger and other documents at fixed

interval.

Whether SECOS has safe custody of

cash, cheque books, other documents

that can be produced for inspection.

Receivables Auditor must check the invoices of the

receivables of the company.

The cash receipts must be reviewed.

Confirmation of all the receivables

during the year must be assessed.

The auditor must go through the

receivable report.

Property, plant and equipment Auditor should ascertain and asses that

company holds proper and legal

documentation related to the title of the

property (title deed).

The opening balances should be

checked from the financial statements

of past year and the opinion given in

the previous year's audit report.

It should be checked that company has

stated the correct financial assertions

relating to fixed assets.

Inventories The documents of inventories that are

held by the company must be checked,

also whether its possession is with any

third party or not.

Confirmation from the external parties

matched the amount of cash from the

ledger and other documents at fixed

interval.

Whether SECOS has safe custody of

cash, cheque books, other documents

that can be produced for inspection.

Receivables Auditor must check the invoices of the

receivables of the company.

The cash receipts must be reviewed.

Confirmation of all the receivables

during the year must be assessed.

The auditor must go through the

receivable report.

Property, plant and equipment Auditor should ascertain and asses that

company holds proper and legal

documentation related to the title of the

property (title deed).

The opening balances should be

checked from the financial statements

of past year and the opinion given in

the previous year's audit report.

It should be checked that company has

stated the correct financial assertions

relating to fixed assets.

Inventories The documents of inventories that are

held by the company must be checked,

also whether its possession is with any

third party or not.

Confirmation from the external parties

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

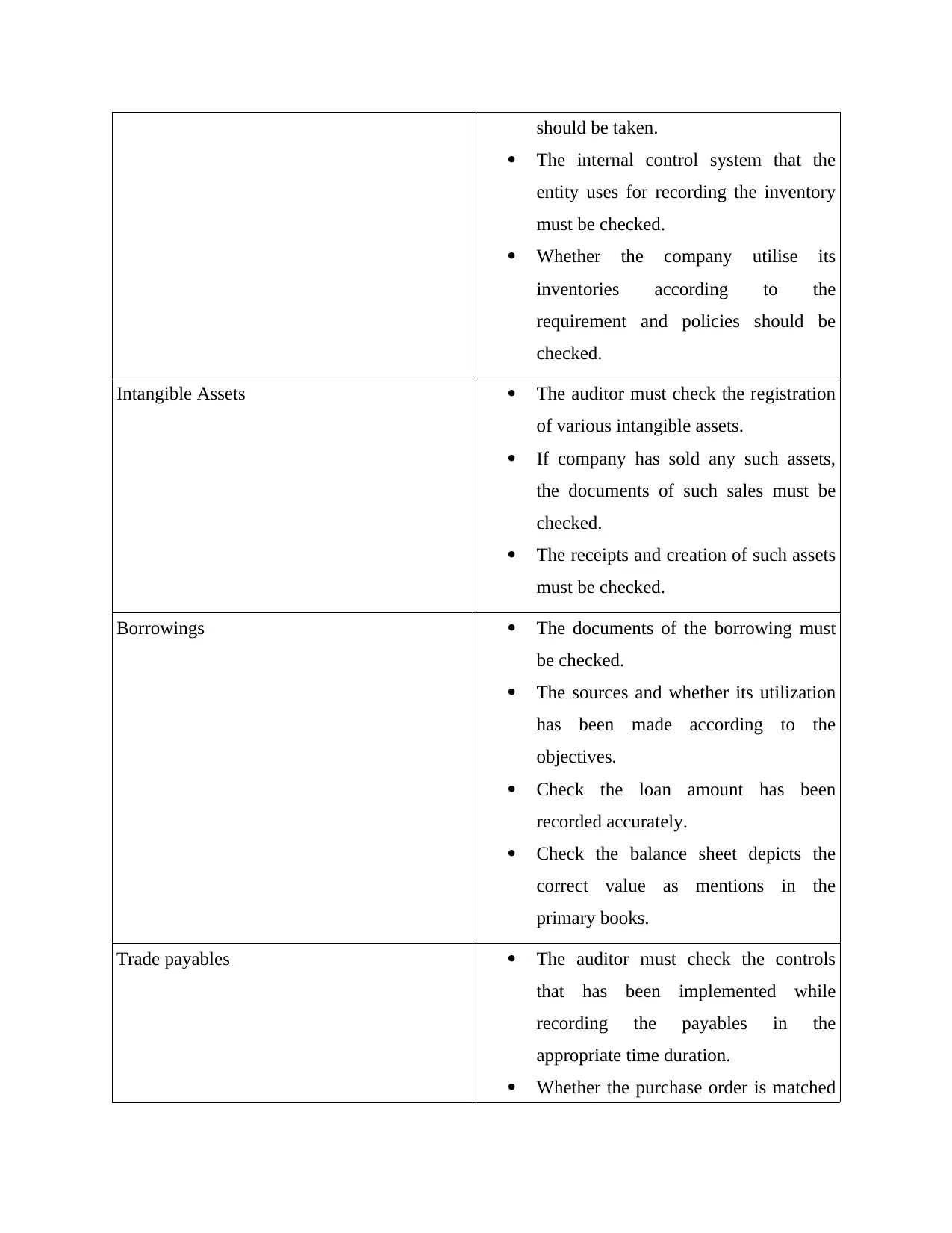

should be taken.

The internal control system that the

entity uses for recording the inventory

must be checked.

Whether the company utilise its

inventories according to the

requirement and policies should be

checked.

Intangible Assets The auditor must check the registration

of various intangible assets.

If company has sold any such assets,

the documents of such sales must be

checked.

The receipts and creation of such assets

must be checked.

Borrowings The documents of the borrowing must

be checked.

The sources and whether its utilization

has been made according to the

objectives.

Check the loan amount has been

recorded accurately.

Check the balance sheet depicts the

correct value as mentions in the

primary books.

Trade payables The auditor must check the controls

that has been implemented while

recording the payables in the

appropriate time duration.

Whether the purchase order is matched

The internal control system that the

entity uses for recording the inventory

must be checked.

Whether the company utilise its

inventories according to the

requirement and policies should be

checked.

Intangible Assets The auditor must check the registration

of various intangible assets.

If company has sold any such assets,

the documents of such sales must be

checked.

The receipts and creation of such assets

must be checked.

Borrowings The documents of the borrowing must

be checked.

The sources and whether its utilization

has been made according to the

objectives.

Check the loan amount has been

recorded accurately.

Check the balance sheet depicts the

correct value as mentions in the

primary books.

Trade payables The auditor must check the controls

that has been implemented while

recording the payables in the

appropriate time duration.

Whether the purchase order is matched

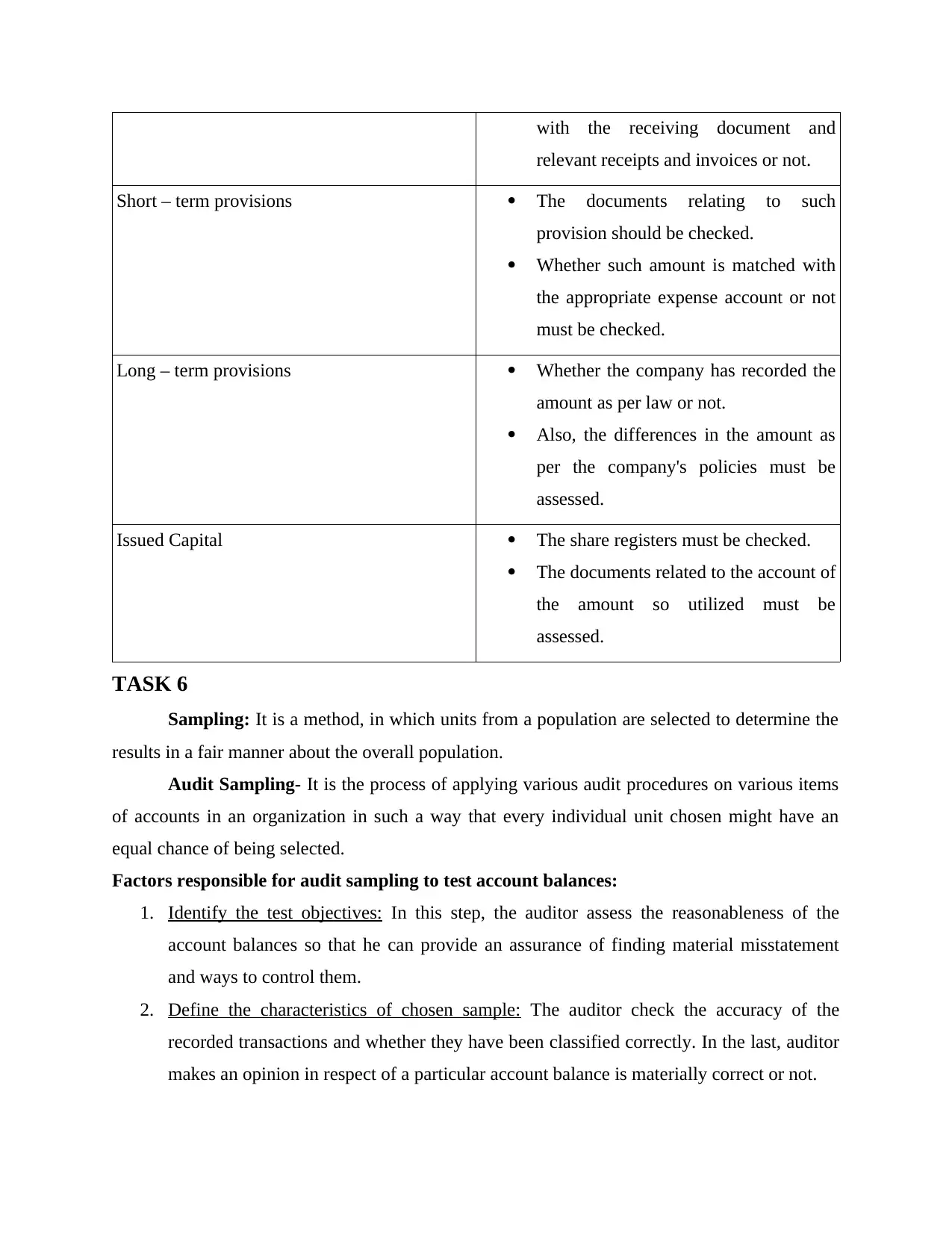

with the receiving document and

relevant receipts and invoices or not.

Short – term provisions The documents relating to such

provision should be checked.

Whether such amount is matched with

the appropriate expense account or not

must be checked.

Long – term provisions Whether the company has recorded the

amount as per law or not.

Also, the differences in the amount as

per the company's policies must be

assessed.

Issued Capital The share registers must be checked.

The documents related to the account of

the amount so utilized must be

assessed.

TASK 6

Sampling: It is a method, in which units from a population are selected to determine the

results in a fair manner about the overall population.

Audit Sampling- It is the process of applying various audit procedures on various items

of accounts in an organization in such a way that every individual unit chosen might have an

equal chance of being selected.

Factors responsible for audit sampling to test account balances:

1. Identify the test objectives: In this step, the auditor assess the reasonableness of the

account balances so that he can provide an assurance of finding material misstatement

and ways to control them.

2. Define the characteristics of chosen sample: The auditor check the accuracy of the

recorded transactions and whether they have been classified correctly. In the last, auditor

makes an opinion in respect of a particular account balance is materially correct or not.

relevant receipts and invoices or not.

Short – term provisions The documents relating to such

provision should be checked.

Whether such amount is matched with

the appropriate expense account or not

must be checked.

Long – term provisions Whether the company has recorded the

amount as per law or not.

Also, the differences in the amount as

per the company's policies must be

assessed.

Issued Capital The share registers must be checked.

The documents related to the account of

the amount so utilized must be

assessed.

TASK 6

Sampling: It is a method, in which units from a population are selected to determine the

results in a fair manner about the overall population.

Audit Sampling- It is the process of applying various audit procedures on various items

of accounts in an organization in such a way that every individual unit chosen might have an

equal chance of being selected.

Factors responsible for audit sampling to test account balances:

1. Identify the test objectives: In this step, the auditor assess the reasonableness of the

account balances so that he can provide an assurance of finding material misstatement

and ways to control them.

2. Define the characteristics of chosen sample: The auditor check the accuracy of the

recorded transactions and whether they have been classified correctly. In the last, auditor

makes an opinion in respect of a particular account balance is materially correct or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.