Auditing and Assurance: Technology's Impact on Audit Quality Report

VerifiedAdded on 2022/08/25

|13

|3484

|21

Report

AI Summary

This report, prepared for BUACC 5935, investigates the evolving landscape of auditing and assurance, focusing on the critical issue of audit quality. It examines concerns raised by regulatory bodies like ASIC and media outlets regarding the effectiveness of audits, especially in light of technological advancements. The report delves into the impact of artificial intelligence and information technology on audit procedures, emphasizing both the benefits of increased efficiency and the potential risks of data security and auditor independence. Ethical considerations, particularly concerning the Restructured Code of Ethics, are analyzed, supported by relevant case studies and examples, including the KPMG Carillion Plc case. The report also explores the role of auditor independence, organizational and operational aspects, and the need for auditor rotation to maintain audit quality, drawing from academic sources. The discussion includes the challenges of maintaining independence and the impact of technological advancements on the auditing profession. The report concludes with an overview of regulatory attempts aimed at improving audit quality.

Running head: AUDITING AND ASSURANCE

AUDITING AND ASSURANCE

Name of the Student

Name of the University

Author Note

AUDITING AND ASSURANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Introduction

The profession of auditing can be understood to be a methodological one which is

essentially focused on the analysis and examination of various auditing clients’ documentations

and financial reporting so that the accounting standards can be maintained and any misstatements

which may exist in the financial statements can be identified (Abc.net.au , 2020). Very often the

managers who are involved in the different accounting operations and related activities tend to

engage in the misstatement and omission of transactions so as to increase their profits or to

increase the incentives which they generally tend to earn (Afr.com ,2020). In line with this, it is

the duty of the auditor to see to it that, the statements are in proper condition and all the

Accounting standards requirements are being fulfilled accordingly. In addition to this, it is

essential that the ethical aspects in concern with the accounting can also be fulfilled accordingly.

However, in the recent years, there has been a considerate and growing issue in relation

to the auditing of services due to the advancement of technology (Arens, Elder & Beasley,

2016). The claim in such a scenario relates to the fact that due to this particular Artificial

intelligence and related technology, the examination and related operations of the auditing firms

has become efficient and there has been a considerable increase in the compliance regarding

independence and information. With consideration to this, it is essential to mention that the

Artificial Intelligence as a technology has provided the Australian Auditing profession a

considerate boost and has added value (Simnett, Carson & Vanstraelen, 2016).

The main reason why the Artificial Intelligence has become popular amongst the

different auditors is because the auditors are being able to attain major opportunities to utilize the

unstructured data and additionally gain advantage from the major technological development. In

Introduction

The profession of auditing can be understood to be a methodological one which is

essentially focused on the analysis and examination of various auditing clients’ documentations

and financial reporting so that the accounting standards can be maintained and any misstatements

which may exist in the financial statements can be identified (Abc.net.au , 2020). Very often the

managers who are involved in the different accounting operations and related activities tend to

engage in the misstatement and omission of transactions so as to increase their profits or to

increase the incentives which they generally tend to earn (Afr.com ,2020). In line with this, it is

the duty of the auditor to see to it that, the statements are in proper condition and all the

Accounting standards requirements are being fulfilled accordingly. In addition to this, it is

essential that the ethical aspects in concern with the accounting can also be fulfilled accordingly.

However, in the recent years, there has been a considerate and growing issue in relation

to the auditing of services due to the advancement of technology (Arens, Elder & Beasley,

2016). The claim in such a scenario relates to the fact that due to this particular Artificial

intelligence and related technology, the examination and related operations of the auditing firms

has become efficient and there has been a considerable increase in the compliance regarding

independence and information. With consideration to this, it is essential to mention that the

Artificial Intelligence as a technology has provided the Australian Auditing profession a

considerate boost and has added value (Simnett, Carson & Vanstraelen, 2016).

The main reason why the Artificial Intelligence has become popular amongst the

different auditors is because the auditors are being able to attain major opportunities to utilize the

unstructured data and additionally gain advantage from the major technological development. In

2AUDITING AND ASSURANCE

addition to this, the artificial technology has also enabled them to gain information from various

sources and prepare the necessary financial statements and auditing sheets accordingly. In

consideration with this, it is important to consider that, the auditing as a profession has been

essentially able to provide the different auditors with a variety of opportunities and give a boost

to the profession of accounting as a whole (Abc.net.au , 2020). Hence, the aim of the essay is to

investigate and examine the particular issue in order to gain a valuable insight.

Therefore, the essay will throw light on three facets of auditing procedure and issues

which have been highlighted due to the advanced technology (Kpmg.au ,2020). The first part of

the essay will focus on the Independence of the auditors and related aspects. The second part will

focus on the accuracy and improvement in the timing which can be undertaken by the auditors

and the last part comprises of the Ethical concerns in regard to the accounting procedure. The

last part of the essay will examine the regulatory attempts which improve the auditing quality of

the different companies along with a summary of the report.

Discussion on concerns

addition to this, the artificial technology has also enabled them to gain information from various

sources and prepare the necessary financial statements and auditing sheets accordingly. In

consideration with this, it is important to consider that, the auditing as a profession has been

essentially able to provide the different auditors with a variety of opportunities and give a boost

to the profession of accounting as a whole (Abc.net.au , 2020). Hence, the aim of the essay is to

investigate and examine the particular issue in order to gain a valuable insight.

Therefore, the essay will throw light on three facets of auditing procedure and issues

which have been highlighted due to the advanced technology (Kpmg.au ,2020). The first part of

the essay will focus on the Independence of the auditors and related aspects. The second part will

focus on the accuracy and improvement in the timing which can be undertaken by the auditors

and the last part comprises of the Ethical concerns in regard to the accounting procedure. The

last part of the essay will examine the regulatory attempts which improve the auditing quality of

the different companies along with a summary of the report.

Discussion on concerns

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

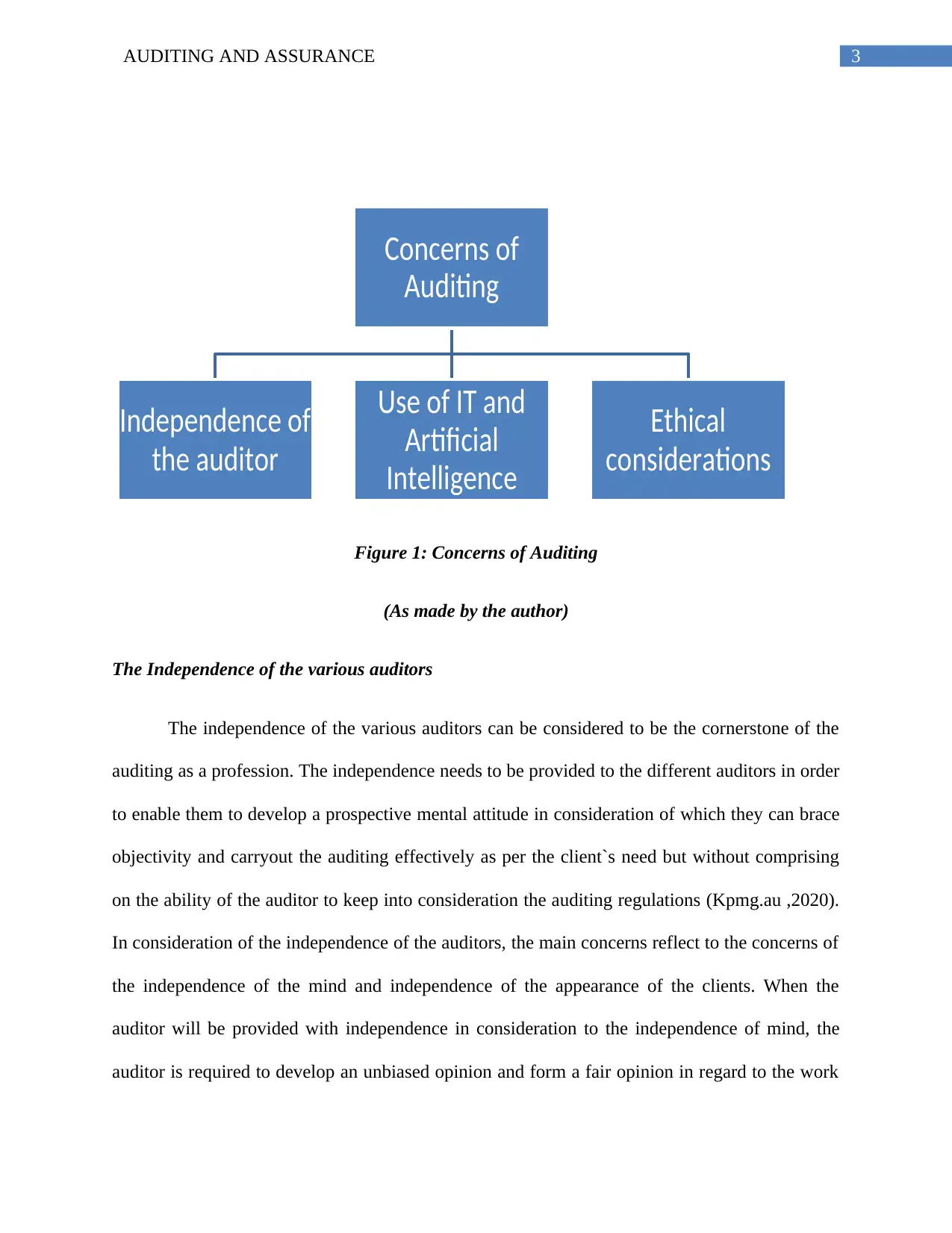

Figure 1: Concerns of Auditing

(As made by the author)

The Independence of the various auditors

The independence of the various auditors can be considered to be the cornerstone of the

auditing as a profession. The independence needs to be provided to the different auditors in order

to enable them to develop a prospective mental attitude in consideration of which they can brace

objectivity and carryout the auditing effectively as per the client`s need but without comprising

on the ability of the auditor to keep into consideration the auditing regulations (Kpmg.au ,2020).

In consideration of the independence of the auditors, the main concerns reflect to the concerns of

the independence of the mind and independence of the appearance of the clients. When the

auditor will be provided with independence in consideration to the independence of mind, the

auditor is required to develop an unbiased opinion and form a fair opinion in regard to the work

Concerns of

Auditing

Independence of

the auditor

Use of IT and

Artificial

Intelligence

Ethical

considerations

Figure 1: Concerns of Auditing

(As made by the author)

The Independence of the various auditors

The independence of the various auditors can be considered to be the cornerstone of the

auditing as a profession. The independence needs to be provided to the different auditors in order

to enable them to develop a prospective mental attitude in consideration of which they can brace

objectivity and carryout the auditing effectively as per the client`s need but without comprising

on the ability of the auditor to keep into consideration the auditing regulations (Kpmg.au ,2020).

In consideration of the independence of the auditors, the main concerns reflect to the concerns of

the independence of the mind and independence of the appearance of the clients. When the

auditor will be provided with independence in consideration to the independence of mind, the

auditor is required to develop an unbiased opinion and form a fair opinion in regard to the work

Concerns of

Auditing

Independence of

the auditor

Use of IT and

Artificial

Intelligence

Ethical

considerations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

which they will undertake. According to Afr.com (2020), the independence of the appearance

refers to the independence in regard to the user perception. With respect to this, it can be

essentially mentioned that there exist a certain level of risk with respect to the independence of

the auditor and this is the aspect which makes the auditor job quite challenging in nature.

This is because, very often the end users who actually view the financial report and

related figures might be under the illusion that the auditor is under the control of the enterprise

and it is due to this reason that the statement is not being able to reflect the true nature of the

enterprise (Kpmg.au , 2020). In addition to this, it also becomes critical to consider that, a similar

barrier to auditor independence occurs when the perception is based on the fact that the auditor

livelihood depends on the company payments and hence they may protect the enterprise at any

cost. However, this is not necessarily the real case and in consideration to this, establishing the

overall authenticity is a key aspect which is required to be considered by the different auditors.

According to the paper by Kelvin Ting Chia on Auditor independence, there exist two

dimensions which were formulated by Michale Power and focus on the independence of the

organization and operations (Simnett, Carson & Vanstraelen, 2016). The organizational

independence revolves around the independence of the mind of the auditor as well as their

overall appearance. On the other hand, the operational independence focuses on the capability of

the auditing as a technique to remain independent and separate of the enterprise activities and be

focused on the collection of the information as well as the factual knowledge (William Jr, Glover

& Prawitt, 2016). In line with this, the author Ting Chia mentioned that even though the

organizational independence may be achieved and successfully attained by the different auditors,

it is difficult for the enterprise to attain operational independence because the data and related

financial information of the enterprise has to be extracted by making use of the data which has to

which they will undertake. According to Afr.com (2020), the independence of the appearance

refers to the independence in regard to the user perception. With respect to this, it can be

essentially mentioned that there exist a certain level of risk with respect to the independence of

the auditor and this is the aspect which makes the auditor job quite challenging in nature.

This is because, very often the end users who actually view the financial report and

related figures might be under the illusion that the auditor is under the control of the enterprise

and it is due to this reason that the statement is not being able to reflect the true nature of the

enterprise (Kpmg.au , 2020). In addition to this, it also becomes critical to consider that, a similar

barrier to auditor independence occurs when the perception is based on the fact that the auditor

livelihood depends on the company payments and hence they may protect the enterprise at any

cost. However, this is not necessarily the real case and in consideration to this, establishing the

overall authenticity is a key aspect which is required to be considered by the different auditors.

According to the paper by Kelvin Ting Chia on Auditor independence, there exist two

dimensions which were formulated by Michale Power and focus on the independence of the

organization and operations (Simnett, Carson & Vanstraelen, 2016). The organizational

independence revolves around the independence of the mind of the auditor as well as their

overall appearance. On the other hand, the operational independence focuses on the capability of

the auditing as a technique to remain independent and separate of the enterprise activities and be

focused on the collection of the information as well as the factual knowledge (William Jr, Glover

& Prawitt, 2016). In line with this, the author Ting Chia mentioned that even though the

organizational independence may be achieved and successfully attained by the different auditors,

it is difficult for the enterprise to attain operational independence because the data and related

financial information of the enterprise has to be extracted by making use of the data which has to

5AUDITING AND ASSURANCE

be provided by the enterprise and may thereby obstruct the overall independence of the auditor

as a whole. Moreover, very often the auditees and the auditing committee which is present within

the enterprise may degrade the quality of the auditing procedure as they control the work

environment of the auditors as well as information and time aspects.

According to William Jr, Glover & Prawitt (2016) , the quality of the audit which takes

place remains at stake as a single auditor generally audits the financial statement of the enterprise

for a longer time frame and in consideration of this, they may get into a close association with

the enterprise and with respect to this, it is important that if the firm intends to maintain the

overall audit quality then in such a scenario, they would be required to rotate the different

auditors who are present and be able to improve the audit quality. When the rotation is being

discussed, the changing of the auditing firms is more critical rather than just changing the

auditors present in the enterprise (Kpmg.au , 2020). In order to prove this case, the example of

the KPMG can be taken who was the contractor of the company Carillion Plc in UK for 19 years.

Hence, several questions were raised in regard to this and there were serious doubts on the

efficiency of the company to conduct high quality audits as it was associated with the company

for a very long period of time. Moreover, the shareholders raised further concerns as the

company had failed to warn the various investors about the inefficiency of the financial stability

of the firm due to which it collapsed later. Hence, the audit quality of the firm can be stated to be

very poor and the enterprise was found guilty of performing poor revenue tests on the audits

(Tspace.gov.au , 2020). Therefore, this case could have been avoided effectively had there been

the rotation of the auditing companies and the liquidation of the enterprise could also be avoided.

Information technology and the Artificial Intelligence

be provided by the enterprise and may thereby obstruct the overall independence of the auditor

as a whole. Moreover, very often the auditees and the auditing committee which is present within

the enterprise may degrade the quality of the auditing procedure as they control the work

environment of the auditors as well as information and time aspects.

According to William Jr, Glover & Prawitt (2016) , the quality of the audit which takes

place remains at stake as a single auditor generally audits the financial statement of the enterprise

for a longer time frame and in consideration of this, they may get into a close association with

the enterprise and with respect to this, it is important that if the firm intends to maintain the

overall audit quality then in such a scenario, they would be required to rotate the different

auditors who are present and be able to improve the audit quality. When the rotation is being

discussed, the changing of the auditing firms is more critical rather than just changing the

auditors present in the enterprise (Kpmg.au , 2020). In order to prove this case, the example of

the KPMG can be taken who was the contractor of the company Carillion Plc in UK for 19 years.

Hence, several questions were raised in regard to this and there were serious doubts on the

efficiency of the company to conduct high quality audits as it was associated with the company

for a very long period of time. Moreover, the shareholders raised further concerns as the

company had failed to warn the various investors about the inefficiency of the financial stability

of the firm due to which it collapsed later. Hence, the audit quality of the firm can be stated to be

very poor and the enterprise was found guilty of performing poor revenue tests on the audits

(Tspace.gov.au , 2020). Therefore, this case could have been avoided effectively had there been

the rotation of the auditing companies and the liquidation of the enterprise could also be avoided.

Information technology and the Artificial Intelligence

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

The second aspect for consideration which has to be considered can be referred as to the

influence of the Artificial Intelligence and the Information technology on the overall behavior of

the auditor. As the behavior of the auditor has an impact on the overall effectiveness and

efficiency of the system, it is considered to be relevant to consider (William Jr, Glover &

Prawitt, 2016). Due to the technological developments, the auditors have boosted their

capabilities and bringing about an improvement of the audit, the effectiveness and efficiency.

The introduction of the Information technology has made the overall auditing procedure quite

easy in nature and has made their overall decisions quite effective and precise in nature.

According to Ey.com (2020), the different auditors have been adopting and embracing the new

technology as it proves to be a good tool to analyze the performance of the firms easily and to

gain a deep insight. In line with this, it is effective to understand that, due to the artificial

intelligence and other IT developments, gathering information from clients has become easier.

According to Simnett, Carson & Vanstraelen (2016), the auditing as an endeavor tends to

involve receiving the information, verifying the information as well as analyzing the information

along with giving an opinion on the enterprise. The evolution of the technology will assist in

ensuring that the data collection is easier and additionally, the software’s are kept up to date and

in order to see to it that the clarity in information can be maintained and in association with this,

the transparency of the information can also be maintained adequately (Forbes.com , 2020). With

consideration to this, it is integral to understand that, although the information technology and

the artificial intelligence generally tends to result in the efficiency of the various operations, a

risk which is associated with it, can be referred to as the risk being related to the unauthorized

access to the data and related information of the company (Sikka, Filling & Liew, 2009). In

association with this, very often there exists considerable access to the data which might be taken

The second aspect for consideration which has to be considered can be referred as to the

influence of the Artificial Intelligence and the Information technology on the overall behavior of

the auditor. As the behavior of the auditor has an impact on the overall effectiveness and

efficiency of the system, it is considered to be relevant to consider (William Jr, Glover &

Prawitt, 2016). Due to the technological developments, the auditors have boosted their

capabilities and bringing about an improvement of the audit, the effectiveness and efficiency.

The introduction of the Information technology has made the overall auditing procedure quite

easy in nature and has made their overall decisions quite effective and precise in nature.

According to Ey.com (2020), the different auditors have been adopting and embracing the new

technology as it proves to be a good tool to analyze the performance of the firms easily and to

gain a deep insight. In line with this, it is effective to understand that, due to the artificial

intelligence and other IT developments, gathering information from clients has become easier.

According to Simnett, Carson & Vanstraelen (2016), the auditing as an endeavor tends to

involve receiving the information, verifying the information as well as analyzing the information

along with giving an opinion on the enterprise. The evolution of the technology will assist in

ensuring that the data collection is easier and additionally, the software’s are kept up to date and

in order to see to it that the clarity in information can be maintained and in association with this,

the transparency of the information can also be maintained adequately (Forbes.com , 2020). With

consideration to this, it is integral to understand that, although the information technology and

the artificial intelligence generally tends to result in the efficiency of the various operations, a

risk which is associated with it, can be referred to as the risk being related to the unauthorized

access to the data and related information of the company (Sikka, Filling & Liew, 2009). In

association with this, very often there exists considerable access to the data which might be taken

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

advantage of by the different members of the enterprise. With respect to this, it becomes

essential to ensure that, the role of the auditor is defined in the rightful manner and that they are

required to identify the various misstatements of the statement and ensure no fraud is being

engaged in. This enables them to be aware of the changes in the technology so that they can

remain updated with the firm`s efforts of maintaining the particular technology and in

consideration of this, allow them to understand how the particular system operates and how the

enterprise is being able to engage in effective relationships with the different stakeholders.

To explain the particular scenario being related to the use of Artificial Intelligence in the

domain of business, the example of the KPMG can be given. This necessarily means that, the

KPMG had adopted the assurance technology which further assisted them to gain a deeper

insight on the information which an organization needs and helped them to go beyond the

traditional filing system (Griffiths, 2016). This has assisted the enterprise to be successful in the

long run. The company culture has improved considerably and with relation to this, it becomes

effective to understand that the risks which are essentially faced by the enterprise can be

calculated with the help of the technology and assists in capturing the interconnectivity in the

risks. With the help of Artificial intelligence, the enterprise has been able to keep a track of the

internet of things, sensor technology and in association with this, work with drones as well

(Simnett, Carson & Vanstraelen, 2016).

Ethical considerations

Another aspect which has to be taken into consideration by the firm can be stated to be

the aspect related to the various ethical considerations which are required to be made by the

auditors while carrying out the auditing system. According to Sikka (2009), the procedure of

advantage of by the different members of the enterprise. With respect to this, it becomes

essential to ensure that, the role of the auditor is defined in the rightful manner and that they are

required to identify the various misstatements of the statement and ensure no fraud is being

engaged in. This enables them to be aware of the changes in the technology so that they can

remain updated with the firm`s efforts of maintaining the particular technology and in

consideration of this, allow them to understand how the particular system operates and how the

enterprise is being able to engage in effective relationships with the different stakeholders.

To explain the particular scenario being related to the use of Artificial Intelligence in the

domain of business, the example of the KPMG can be given. This necessarily means that, the

KPMG had adopted the assurance technology which further assisted them to gain a deeper

insight on the information which an organization needs and helped them to go beyond the

traditional filing system (Griffiths, 2016). This has assisted the enterprise to be successful in the

long run. The company culture has improved considerably and with relation to this, it becomes

effective to understand that the risks which are essentially faced by the enterprise can be

calculated with the help of the technology and assists in capturing the interconnectivity in the

risks. With the help of Artificial intelligence, the enterprise has been able to keep a track of the

internet of things, sensor technology and in association with this, work with drones as well

(Simnett, Carson & Vanstraelen, 2016).

Ethical considerations

Another aspect which has to be taken into consideration by the firm can be stated to be

the aspect related to the various ethical considerations which are required to be made by the

auditors while carrying out the auditing system. According to Sikka (2009), the procedure of

8AUDITING AND ASSURANCE

auditing has a key role to play in determining the overall success of financial reporting and in

consideration of this, it becomes effective to understand that, in general dye to the overall

welfare of the enterprise, it is easy to glorify the accounts and to maintain the economic

positioning of the country (Pwc.com , 2020). With respect to this, it is effective to ensure that,

the auditors are being able to engage in specific analysis and the examination of the same.

According to Groomer and Murthy (2018), when an operating company is functioning, the

auditor as an enterprise would be essentially required to check for ethicality.

Hence, the auditor would be required to maintain the overall compliance laws and other

related norms and procedures accordingly to ensure that, the values illustrated by the Code of

Professional Code of conduct needs to be suitable. These aspects as involved in the Code of

conduct comprise of the integrity, independence, confidentiality, technical as well as professional

standards. In consideration of this, it is essential to ensure that, there have been various issues in

consideration to the ethical aspects such as the Enron, Martha Steward, Lehman and the

Goldman Sachs (Ifac.org , 2020). These companies have not been able to maintain and uplift the

ethicality of the business aspects and in association with this; they have broken the trust of the

shareholders, their honesty and equity contracts. The Enron collapsed back in 2002 whereby they

were held for the ethical violation of the various rules and regulations. In line with this, it

becomes integral to understand that there has been a downfall of the different companies and in

consideration of this, the dues have fallen down to a great extent (Power & Gendron, 2015).

However, when the case of the Enron was highlighted, the legislations also blamed the different

auditing companies. It was mentioned that the auditing enterprises were established for the

welfare of the different members of the enterprises and to protect their stakeholder interest

(Knechel & Salterio , 2016). However, the lack of the bankruptcy should have been identified

auditing has a key role to play in determining the overall success of financial reporting and in

consideration of this, it becomes effective to understand that, in general dye to the overall

welfare of the enterprise, it is easy to glorify the accounts and to maintain the economic

positioning of the country (Pwc.com , 2020). With respect to this, it is effective to ensure that,

the auditors are being able to engage in specific analysis and the examination of the same.

According to Groomer and Murthy (2018), when an operating company is functioning, the

auditor as an enterprise would be essentially required to check for ethicality.

Hence, the auditor would be required to maintain the overall compliance laws and other

related norms and procedures accordingly to ensure that, the values illustrated by the Code of

Professional Code of conduct needs to be suitable. These aspects as involved in the Code of

conduct comprise of the integrity, independence, confidentiality, technical as well as professional

standards. In consideration of this, it is essential to ensure that, there have been various issues in

consideration to the ethical aspects such as the Enron, Martha Steward, Lehman and the

Goldman Sachs (Ifac.org , 2020). These companies have not been able to maintain and uplift the

ethicality of the business aspects and in association with this; they have broken the trust of the

shareholders, their honesty and equity contracts. The Enron collapsed back in 2002 whereby they

were held for the ethical violation of the various rules and regulations. In line with this, it

becomes integral to understand that there has been a downfall of the different companies and in

consideration of this, the dues have fallen down to a great extent (Power & Gendron, 2015).

However, when the case of the Enron was highlighted, the legislations also blamed the different

auditing companies. It was mentioned that the auditing enterprises were established for the

welfare of the different members of the enterprises and to protect their stakeholder interest

(Knechel & Salterio , 2016). However, the lack of the bankruptcy should have been identified

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

by the auditing firm and could have protected the enterprise from aspects like the untruthfulness,

lack of independent management conflict and manipulation of consistent information.

Discussion

Hence, it can be essentially stated that, since these incidents have taken place various

Accounting standards as well as the various laws have been established which have then limited

the overall scandals and unethical aspects, it has to be considered that the International code of

Ethics for Professional accountants was formulated in 2019 (Kpmg.au , 2020). With regard to

this, the code comprises of various amendments and modifications in regard to the rules and the

framework using which the code needs to be applied. Moreover, the ASIC set of standards has

also been updated regularly in order to see to it that the enterprise and accounting balance can be

undertaken accordingly (Leung et al., 2015).

Conclusion

Hence, from the given analysis, it can be mentioned that the quality of auditing can be

understood to be very crucial as the auditing as a body is relied on by various stakeholders of the

firm. It is the primary duty of auditing to ensure that, the book of accounts are prepared in a

manner such that the true positioning of the firm can be identified and in line with this, any risks

which may be faced by the enterprise can be identified effectively. The essay discussed various

aspects and factors which influence the audit quality and comprised of aspects such as the

independence of the auditor, the intrusion of the Information technology and the Artificial

Intelligence and the Ethical considerations. The example of Enron and other examples were

given to imply the importance of auditing quality along with providing a framework using which

the auditing quality can be essentially maintained.

by the auditing firm and could have protected the enterprise from aspects like the untruthfulness,

lack of independent management conflict and manipulation of consistent information.

Discussion

Hence, it can be essentially stated that, since these incidents have taken place various

Accounting standards as well as the various laws have been established which have then limited

the overall scandals and unethical aspects, it has to be considered that the International code of

Ethics for Professional accountants was formulated in 2019 (Kpmg.au , 2020). With regard to

this, the code comprises of various amendments and modifications in regard to the rules and the

framework using which the code needs to be applied. Moreover, the ASIC set of standards has

also been updated regularly in order to see to it that the enterprise and accounting balance can be

undertaken accordingly (Leung et al., 2015).

Conclusion

Hence, from the given analysis, it can be mentioned that the quality of auditing can be

understood to be very crucial as the auditing as a body is relied on by various stakeholders of the

firm. It is the primary duty of auditing to ensure that, the book of accounts are prepared in a

manner such that the true positioning of the firm can be identified and in line with this, any risks

which may be faced by the enterprise can be identified effectively. The essay discussed various

aspects and factors which influence the audit quality and comprised of aspects such as the

independence of the auditor, the intrusion of the Information technology and the Artificial

Intelligence and the Ethical considerations. The example of Enron and other examples were

given to imply the importance of auditing quality along with providing a framework using which

the auditing quality can be essentially maintained.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

Reference

Abc.net.au (2020). Audit firm failure [online]. Available at: https://www.abc.net.au/news/2019-

08-06/audit-firm-failures-could-spark-enron-style-collapse-medcraft/11388164(Retrieved

on: 18 Jan 2020).

Afr.com (2020). Audit Quality [online]. Available at: https://www.afr.com/politics/federal/asic-

to-name-and-shame-big-four-consulting-firms-over-audit-quality-20190806-p52efr

(Retrieved on: 18 Jan 2020).

Arens, A. A., Elder, R. J., & Beasley, M. S. (2016). Auditing and Assurance Services, Global

Edition. Pearson Education Limited.

Ey.com (2020). AI and Audit [online]. Available at: https://www.ey.com/en_gl/assurance/how-

artificial-intelligence-will-transform-the-audit (Retrieved on: 18 Jan 2020).

Forbes.com (2020). Audit Quality [online]. Available at: https://www.forbes.com/sites/insights-

kpmg/2019/03/04/how-advanced-technologies-may-improve-audit-quality/

#511282375632 (Retrieved on: 18 Jan 2020).

Griffiths, P. (2016). Risk-based auditing. Routledge.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp.

105-124). Emerald Publishing Limited.

Ifac.org (2020). Global knowledge gateway [online]. Available at: https://www.ifac.org/global-

knowledge-gateway/ethics/discussion/how-new-ethics-code-will-affect-your-standards

(Retrieved on: 18 Jan 2020).

Reference

Abc.net.au (2020). Audit firm failure [online]. Available at: https://www.abc.net.au/news/2019-

08-06/audit-firm-failures-could-spark-enron-style-collapse-medcraft/11388164(Retrieved

on: 18 Jan 2020).

Afr.com (2020). Audit Quality [online]. Available at: https://www.afr.com/politics/federal/asic-

to-name-and-shame-big-four-consulting-firms-over-audit-quality-20190806-p52efr

(Retrieved on: 18 Jan 2020).

Arens, A. A., Elder, R. J., & Beasley, M. S. (2016). Auditing and Assurance Services, Global

Edition. Pearson Education Limited.

Ey.com (2020). AI and Audit [online]. Available at: https://www.ey.com/en_gl/assurance/how-

artificial-intelligence-will-transform-the-audit (Retrieved on: 18 Jan 2020).

Forbes.com (2020). Audit Quality [online]. Available at: https://www.forbes.com/sites/insights-

kpmg/2019/03/04/how-advanced-technologies-may-improve-audit-quality/

#511282375632 (Retrieved on: 18 Jan 2020).

Griffiths, P. (2016). Risk-based auditing. Routledge.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp.

105-124). Emerald Publishing Limited.

Ifac.org (2020). Global knowledge gateway [online]. Available at: https://www.ifac.org/global-

knowledge-gateway/ethics/discussion/how-new-ethics-code-will-affect-your-standards

(Retrieved on: 18 Jan 2020).

11AUDITING AND ASSURANCE

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Kpmg.au (2020). Audit technology [online]. Available at:

https://home.kpmg/au/en/home/insights/2019/02/audit-technology-future-technology-

audit-quality.html (Retrieved on: 18 Jan 2020).

Leung, P., Coram, P., Cooper, B. J., & Richardson, P. (2015). Modern auditing and assurance

services. John Wiley & Sons.

Power, M. K., & Gendron, Y. (2015). Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), 147-165.

Pwc.com (2020). Balanced score card [online]. Available at: https://www.pwc.com.au/press-

room/2019/pwc-releases-balanced-scorecard.html(Retrieved on: 18 Jan 2020).

Sikka, P. (2009). Financial crisis and the silence of the auditors. Accounting, Organizations and

Society, Vol. 34(6-7), pp. 868-873.

Sikka, P., Filling, S.,Liew, P. (2009) "The audit crunch: reforming auditing", Managerial

Auditing Journal, Vol. 24 No.2, pp.135 – 155.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory, 35(3), 1-32.

Tspace.gov.au (2020). Audit Quality in Australia [online]. Available at:

https://cdn.tspace.gov.au/uploads/sites/21/2019/05/Audit_Qulaity_in_Australia_-

_The_Per.pdf (Retrieved on: 18 Jan 2020).

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Kpmg.au (2020). Audit technology [online]. Available at:

https://home.kpmg/au/en/home/insights/2019/02/audit-technology-future-technology-

audit-quality.html (Retrieved on: 18 Jan 2020).

Leung, P., Coram, P., Cooper, B. J., & Richardson, P. (2015). Modern auditing and assurance

services. John Wiley & Sons.

Power, M. K., & Gendron, Y. (2015). Qualitative research in auditing: A methodological

roadmap. Auditing: A Journal of Practice & Theory, 34(2), 147-165.

Pwc.com (2020). Balanced score card [online]. Available at: https://www.pwc.com.au/press-

room/2019/pwc-releases-balanced-scorecard.html(Retrieved on: 18 Jan 2020).

Sikka, P. (2009). Financial crisis and the silence of the auditors. Accounting, Organizations and

Society, Vol. 34(6-7), pp. 868-873.

Sikka, P., Filling, S.,Liew, P. (2009) "The audit crunch: reforming auditing", Managerial

Auditing Journal, Vol. 24 No.2, pp.135 – 155.

Simnett, R., Carson, E., & Vanstraelen, A. (2016). International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of

Practice & Theory, 35(3), 1-32.

Tspace.gov.au (2020). Audit Quality in Australia [online]. Available at:

https://cdn.tspace.gov.au/uploads/sites/21/2019/05/Audit_Qulaity_in_Australia_-

_The_Per.pdf (Retrieved on: 18 Jan 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.