Auditing Theory and Practice: Analysis of Audit Risks for TCW Company

VerifiedAdded on 2023/06/07

|16

|3697

|54

Report

AI Summary

This report provides a comprehensive analysis of auditing theory and practice, focusing on the identification and assessment of various audit risks. It begins by examining the risks associated with material misstatements, including fraud and error, and emphasizes the importance of ratio analysis in evaluating a company's financial performance. The report uses the TCW Company as a case study, analyzing specific accounts like accounts receivable, investments, marketing expenses, and property assets to identify inherent, control, and detection risks. It also delves into business risks, such as strategic, compliance, financial, operational, and reputational risks, and provides recommendations for mitigating these risks. The report includes an analysis of financial ratios like return on equity, gross margin, and debt-to-equity ratio, offering insights into TCW's financial health and operational efficiency. Overall, the report aims to provide a practical understanding of auditing principles and their application in real-world scenarios, making it a valuable resource for students studying finance and accounting.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the Student:

Name of the University:

Auditing theory and practice

Name of the Student:

Name of the University:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Abstract

The discussion evaluates the various risk attached with the process of audit that involves issues

that is faced by the assessor at the time of the material misstatements recognition. This may take

place due to fraud or error. The approach that is most ideal is the examination the risk of the

business faced during the process of audit by measuring the key financial ratios that would

enable in obtaining fast of the organization performance evaluation. This may help in assisting

the administration to assess the pros and cons from the various initiatives and strategies can be

processed. The TCW Company in the following discussion has been found out. For the firm for

examining the competence and operational effectiveness of the internal control has been focused

upon that also complies with the assurance motives of TCW.

Abstract

The discussion evaluates the various risk attached with the process of audit that involves issues

that is faced by the assessor at the time of the material misstatements recognition. This may take

place due to fraud or error. The approach that is most ideal is the examination the risk of the

business faced during the process of audit by measuring the key financial ratios that would

enable in obtaining fast of the organization performance evaluation. This may help in assisting

the administration to assess the pros and cons from the various initiatives and strategies can be

processed. The TCW Company in the following discussion has been found out. For the firm for

examining the competence and operational effectiveness of the internal control has been focused

upon that also complies with the assurance motives of TCW.

2AUDITING THEORY AND PRACTICE

Table of Contents

Solution to Question 1A..................................................................................................................3

Solution to Question 1B...................................................................................................................6

Solution to Question 2A................................................................................................................11

Solution to Question 2B.................................................................................................................14

List of reference.............................................................................................................................15

Table of Contents

Solution to Question 1A..................................................................................................................3

Solution to Question 1B...................................................................................................................6

Solution to Question 2A................................................................................................................11

Solution to Question 2B.................................................................................................................14

List of reference.............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

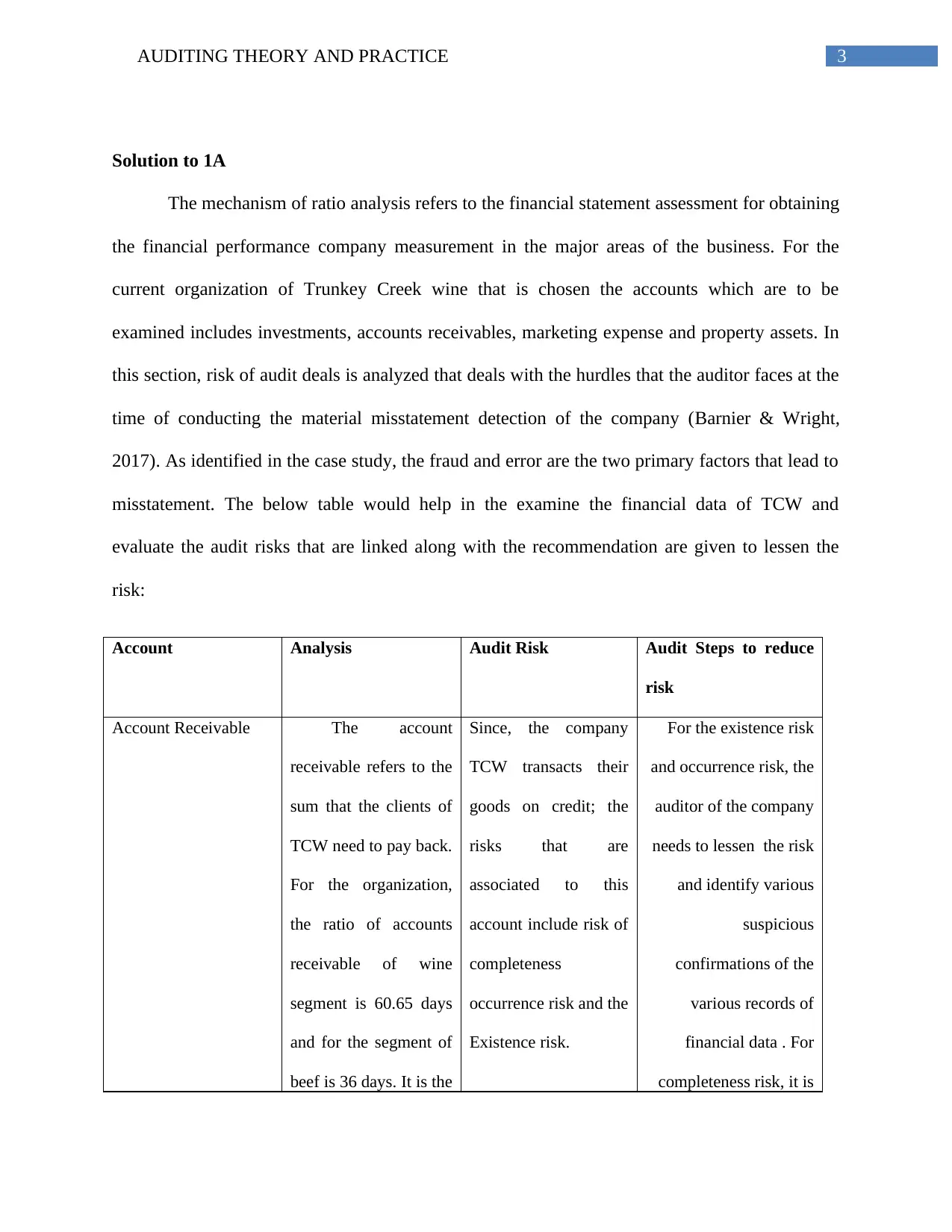

Solution to 1A

The mechanism of ratio analysis refers to the financial statement assessment for obtaining

the financial performance company measurement in the major areas of the business. For the

current organization of Trunkey Creek wine that is chosen the accounts which are to be

examined includes investments, accounts receivables, marketing expense and property assets. In

this section, risk of audit deals is analyzed that deals with the hurdles that the auditor faces at the

time of conducting the material misstatement detection of the company (Barnier & Wright,

2017). As identified in the case study, the fraud and error are the two primary factors that lead to

misstatement. The below table would help in the examine the financial data of TCW and

evaluate the audit risks that are linked along with the recommendation are given to lessen the

risk:

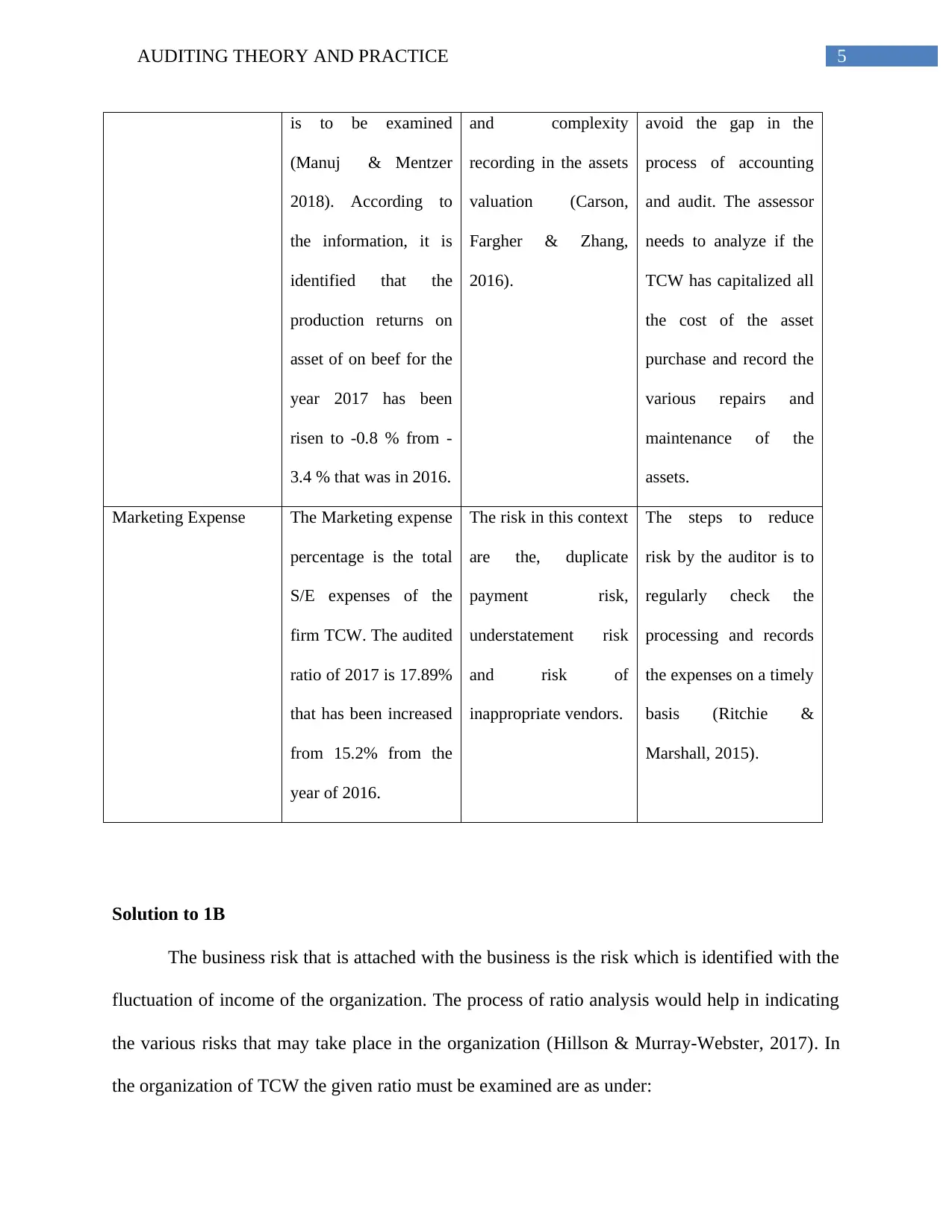

Account Analysis Audit Risk Audit Steps to reduce

risk

Account Receivable The account

receivable refers to the

sum that the clients of

TCW need to pay back.

For the organization,

the ratio of accounts

receivable of wine

segment is 60.65 days

and for the segment of

beef is 36 days. It is the

Since, the company

TCW transacts their

goods on credit; the

risks that are

associated to this

account include risk of

completeness

occurrence risk and the

Existence risk.

For the existence risk

and occurrence risk, the

auditor of the company

needs to lessen the risk

and identify various

suspicious

confirmations of the

various records of

financial data . For

completeness risk, it is

Solution to 1A

The mechanism of ratio analysis refers to the financial statement assessment for obtaining

the financial performance company measurement in the major areas of the business. For the

current organization of Trunkey Creek wine that is chosen the accounts which are to be

examined includes investments, accounts receivables, marketing expense and property assets. In

this section, risk of audit deals is analyzed that deals with the hurdles that the auditor faces at the

time of conducting the material misstatement detection of the company (Barnier & Wright,

2017). As identified in the case study, the fraud and error are the two primary factors that lead to

misstatement. The below table would help in the examine the financial data of TCW and

evaluate the audit risks that are linked along with the recommendation are given to lessen the

risk:

Account Analysis Audit Risk Audit Steps to reduce

risk

Account Receivable The account

receivable refers to the

sum that the clients of

TCW need to pay back.

For the organization,

the ratio of accounts

receivable of wine

segment is 60.65 days

and for the segment of

beef is 36 days. It is the

Since, the company

TCW transacts their

goods on credit; the

risks that are

associated to this

account include risk of

completeness

occurrence risk and the

Existence risk.

For the existence risk

and occurrence risk, the

auditor of the company

needs to lessen the risk

and identify various

suspicious

confirmations of the

various records of

financial data . For

completeness risk, it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

number of days that the

invoice of customers

are outstanding.

the auditor to examine

all the proceeds of sales

and get ability for the

transaction of the

company’s process.

Investment The investment

analysis can be done

by interest earning

ratio. In the company

of TCW in 2016 the

interest earned was

8.10 and for 2017 the

same was 7.51 that

mean that the

investment for the

company has increased

(Bradbury, Raftery &

Scott, 2018).

Additionally, the debt

equity ratio also

represents the

investment risk.

There exists the

inherent risk in the

context of material

misstatement. If risk is

high, there is a liability

to the investors who

needs payments. This

can impact the

working capital.

If auditor obtain

investment data that is

at cost or fair value

which is shown in the

financial statement of.

The auditor must also

analyze the methods for

the determination the

fair value according to

the GAAP.

Property assets The ratio of return on

production assets for

both the segments of

wine and beef of TCW

The associated risk of

the recording of the

property assets is the

correct cost based on

The auditor must reduce

the record complexity

of the assets and make

easy. This would help to

number of days that the

invoice of customers

are outstanding.

the auditor to examine

all the proceeds of sales

and get ability for the

transaction of the

company’s process.

Investment The investment

analysis can be done

by interest earning

ratio. In the company

of TCW in 2016 the

interest earned was

8.10 and for 2017 the

same was 7.51 that

mean that the

investment for the

company has increased

(Bradbury, Raftery &

Scott, 2018).

Additionally, the debt

equity ratio also

represents the

investment risk.

There exists the

inherent risk in the

context of material

misstatement. If risk is

high, there is a liability

to the investors who

needs payments. This

can impact the

working capital.

If auditor obtain

investment data that is

at cost or fair value

which is shown in the

financial statement of.

The auditor must also

analyze the methods for

the determination the

fair value according to

the GAAP.

Property assets The ratio of return on

production assets for

both the segments of

wine and beef of TCW

The associated risk of

the recording of the

property assets is the

correct cost based on

The auditor must reduce

the record complexity

of the assets and make

easy. This would help to

5AUDITING THEORY AND PRACTICE

is to be examined

(Manuj & Mentzer

2018). According to

the information, it is

identified that the

production returns on

asset of on beef for the

year 2017 has been

risen to -0.8 % from -

3.4 % that was in 2016.

and complexity

recording in the assets

valuation (Carson,

Fargher & Zhang,

2016).

avoid the gap in the

process of accounting

and audit. The assessor

needs to analyze if the

TCW has capitalized all

the cost of the asset

purchase and record the

various repairs and

maintenance of the

assets.

Marketing Expense The Marketing expense

percentage is the total

S/E expenses of the

firm TCW. The audited

ratio of 2017 is 17.89%

that has been increased

from 15.2% from the

year of 2016.

The risk in this context

are the, duplicate

payment risk,

understatement risk

and risk of

inappropriate vendors.

The steps to reduce

risk by the auditor is to

regularly check the

processing and records

the expenses on a timely

basis (Ritchie &

Marshall, 2015).

Solution to 1B

The business risk that is attached with the business is the risk which is identified with the

fluctuation of income of the organization. The process of ratio analysis would help in indicating

the various risks that may take place in the organization (Hillson & Murray-Webster, 2017). In

the organization of TCW the given ratio must be examined are as under:

is to be examined

(Manuj & Mentzer

2018). According to

the information, it is

identified that the

production returns on

asset of on beef for the

year 2017 has been

risen to -0.8 % from -

3.4 % that was in 2016.

and complexity

recording in the assets

valuation (Carson,

Fargher & Zhang,

2016).

avoid the gap in the

process of accounting

and audit. The assessor

needs to analyze if the

TCW has capitalized all

the cost of the asset

purchase and record the

various repairs and

maintenance of the

assets.

Marketing Expense The Marketing expense

percentage is the total

S/E expenses of the

firm TCW. The audited

ratio of 2017 is 17.89%

that has been increased

from 15.2% from the

year of 2016.

The risk in this context

are the, duplicate

payment risk,

understatement risk

and risk of

inappropriate vendors.

The steps to reduce

risk by the auditor is to

regularly check the

processing and records

the expenses on a timely

basis (Ritchie &

Marshall, 2015).

Solution to 1B

The business risk that is attached with the business is the risk which is identified with the

fluctuation of income of the organization. The process of ratio analysis would help in indicating

the various risks that may take place in the organization (Hillson & Murray-Webster, 2017). In

the organization of TCW the given ratio must be examined are as under:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

• Return on equity: The return on equity that breaks down the profitability of the

organization of TCW, in 2017 has increased 17.5 from 15.5 in 2016 (Bailey, Collins, & Abbott,

2017). For the year 2018 the expected unaudited records says that it will fall more to 10.80 in the

year 2018.

• Return on production assets of beef: The intensity of production and estimation of

assets with the total assets business is known as the return on assets. In present scenario of TCW,

percentage returns of the beef production. Increased from - 3.45 out of 2016 to 0.82 in 2017.

However, as per the unaudited records the return would rise to 1.67 in 2018.

• Return on grape and wine asset production: The return on grape and wine production

of the TCW in 2016 was 16.2 that reduced to 14.5 in the year 2017. In 2018 the unaudited record

is much less that amounts to 12.2(Bentley-Goode, Newton & Thompson, 2017).

• Gross Margin: The gross margin is the total income of TCW after reducing from the

cost of goods sold by the total sales (Louwers, et al., 2015). If the rate is high, the firm has the

ability to hold the units of sales. In TCWs the gross profit margin in 2016 was 31.76 which fell

to 14.5 in 2017; However, the gross margin decreased to 12.2 out of 2018 as per the unaudited

report.

• Marketing cost over S/A costs: The costs of marketing is the cash level that has been

with the profits from the total of administrative costs considering the end goal for increasing the

sales (Knechel & Salterio, 2016). It is an indirect cost. As per the records of 2017 and 2016 that

are audited, the marketing cost level has reduced from 2016 in 15.2 to 17.89 in 2017. In 2018 the

unaudited record amounted to 23.67.

• Return on equity: The return on equity that breaks down the profitability of the

organization of TCW, in 2017 has increased 17.5 from 15.5 in 2016 (Bailey, Collins, & Abbott,

2017). For the year 2018 the expected unaudited records says that it will fall more to 10.80 in the

year 2018.

• Return on production assets of beef: The intensity of production and estimation of

assets with the total assets business is known as the return on assets. In present scenario of TCW,

percentage returns of the beef production. Increased from - 3.45 out of 2016 to 0.82 in 2017.

However, as per the unaudited records the return would rise to 1.67 in 2018.

• Return on grape and wine asset production: The return on grape and wine production

of the TCW in 2016 was 16.2 that reduced to 14.5 in the year 2017. In 2018 the unaudited record

is much less that amounts to 12.2(Bentley-Goode, Newton & Thompson, 2017).

• Gross Margin: The gross margin is the total income of TCW after reducing from the

cost of goods sold by the total sales (Louwers, et al., 2015). If the rate is high, the firm has the

ability to hold the units of sales. In TCWs the gross profit margin in 2016 was 31.76 which fell

to 14.5 in 2017; However, the gross margin decreased to 12.2 out of 2018 as per the unaudited

report.

• Marketing cost over S/A costs: The costs of marketing is the cash level that has been

with the profits from the total of administrative costs considering the end goal for increasing the

sales (Knechel & Salterio, 2016). It is an indirect cost. As per the records of 2017 and 2016 that

are audited, the marketing cost level has reduced from 2016 in 15.2 to 17.89 in 2017. In 2018 the

unaudited record amounted to 23.67.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

• Times interest earned: The interest earned refers to the coverage ratio that makes the

estimation of the organization capacity of the to meet payment of the debts. In the present case

the coverage ratio is less than one that means that, the firm not getting sufficient cash from the

various operations of the business (Farooq & de Villiers, 2017). The interest that is earned is

reducing in the organization of TCW that represents to that there not much generation of cash. In

2017 the interest earned was 7.51; in 2016 was 8.10 and the expected and unaudited interest for

2018 was 6.67.

• Days in inventory (wine): The days sales are represented by the days for the sale of the

inventories at the determined period. For this case, the inventory refers to the production of the

wine. For wine, the days of inventory for 2016 was 460, in 2017 was 423 and in case of the

unaudited record the number of days is 367.

• Days in accounts receivables (wine): The accounts receivables days is the number of

days that the company of TCW would need to get the installments of their sales. If numbers of

days are more, it reflects a issue in cash generation. In case there is lesser number of days, it

reflects that there is a strict policy of credit that may reduce the revenue (Cohen & Simnett,

2014). Here, the goods is the wine production of TCW. The receivable of days for wine was

53.24 in 2016, 60.65 in the year 2017 and the unaudited record are 50.2.

• Days in accounts receivables (beef): The account receivable days for beef in 2016 was

24, in 2017 was 36 and the unaudited record are 57 in the year 2018.

• Current ratio: The current ratio refers is the liquidity ratio estimates the capacity of the

firm to accommodate both long term and short term liabilities. It can be calculated by division of

the total of liabilities and assets of the organization. In the given case the aggregate assers to both

• Times interest earned: The interest earned refers to the coverage ratio that makes the

estimation of the organization capacity of the to meet payment of the debts. In the present case

the coverage ratio is less than one that means that, the firm not getting sufficient cash from the

various operations of the business (Farooq & de Villiers, 2017). The interest that is earned is

reducing in the organization of TCW that represents to that there not much generation of cash. In

2017 the interest earned was 7.51; in 2016 was 8.10 and the expected and unaudited interest for

2018 was 6.67.

• Days in inventory (wine): The days sales are represented by the days for the sale of the

inventories at the determined period. For this case, the inventory refers to the production of the

wine. For wine, the days of inventory for 2016 was 460, in 2017 was 423 and in case of the

unaudited record the number of days is 367.

• Days in accounts receivables (wine): The accounts receivables days is the number of

days that the company of TCW would need to get the installments of their sales. If numbers of

days are more, it reflects a issue in cash generation. In case there is lesser number of days, it

reflects that there is a strict policy of credit that may reduce the revenue (Cohen & Simnett,

2014). Here, the goods is the wine production of TCW. The receivable of days for wine was

53.24 in 2016, 60.65 in the year 2017 and the unaudited record are 50.2.

• Days in accounts receivables (beef): The account receivable days for beef in 2016 was

24, in 2017 was 36 and the unaudited record are 57 in the year 2018.

• Current ratio: The current ratio refers is the liquidity ratio estimates the capacity of the

firm to accommodate both long term and short term liabilities. It can be calculated by division of

the total of liabilities and assets of the organization. In the given case the aggregate assers to both

8AUDITING THEORY AND PRACTICE

noncurrent and current assets of the current and of TCW. The current ratio is 2.66 for the year

2016, 2.54 in the year 2017 and the unaudited record is 2.80.

• Acid test ratio: The acid -test ratio or quick ratio is the assets that can be converted into

cash without changing the value (Junior, Best & Cotter, 2014). The acid test ratio was 1.20 in

2016, 1.15 in 2017 and the unaudited record is expected to be 1.18.

• Debts to equity ratio: The debt to equity ratio refers to the financial ratio that shows the

financial ratios that demonstrates the extent of shareholders debt and equity to finance the asset

with respect to the equity value (Sadgrove, 2016). Debt to equity ratio was 0.67 in 2016, 0.63 for

the year 2017 and the unaudited record is 0.54.

It can be observed from the above analysis, the various types of risks have been

identified, and Business risk is the probability of not obtaining the investment return. In case of

the company of TCW the identified risks are:

Strategic risks: The strategic risk is the operating risk within a specific industry at a particular

time that can take place from change in technology or clients preference change (Cohen,

Krishnamoorthy & Wright, 2017). For TCW, they deal with both beef and wine; therefore, risk

linked with strategy is much less. Moreover, there has been installation of new IT system that

may give rise to some risk.

Risk of compliance: The risk that are related with compliance to regulations of bureaucratic or

authoritative that the firm may pursue. For the TCW as there is a sound internal control, the

identified compliance risk is less.

noncurrent and current assets of the current and of TCW. The current ratio is 2.66 for the year

2016, 2.54 in the year 2017 and the unaudited record is 2.80.

• Acid test ratio: The acid -test ratio or quick ratio is the assets that can be converted into

cash without changing the value (Junior, Best & Cotter, 2014). The acid test ratio was 1.20 in

2016, 1.15 in 2017 and the unaudited record is expected to be 1.18.

• Debts to equity ratio: The debt to equity ratio refers to the financial ratio that shows the

financial ratios that demonstrates the extent of shareholders debt and equity to finance the asset

with respect to the equity value (Sadgrove, 2016). Debt to equity ratio was 0.67 in 2016, 0.63 for

the year 2017 and the unaudited record is 0.54.

It can be observed from the above analysis, the various types of risks have been

identified, and Business risk is the probability of not obtaining the investment return. In case of

the company of TCW the identified risks are:

Strategic risks: The strategic risk is the operating risk within a specific industry at a particular

time that can take place from change in technology or clients preference change (Cohen,

Krishnamoorthy & Wright, 2017). For TCW, they deal with both beef and wine; therefore, risk

linked with strategy is much less. Moreover, there has been installation of new IT system that

may give rise to some risk.

Risk of compliance: The risk that are related with compliance to regulations of bureaucratic or

authoritative that the firm may pursue. For the TCW as there is a sound internal control, the

identified compliance risk is less.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

Financial risk: It is the monetary risk linked with the loss is known as financial risk. In the

present case of TCW, there is large financial risk because of the implications of new framework

of IT. Apart from the that since there are three of the segments of grapes, wines and beef they

may experience of loss of money.

Operational Risks: The operational risk is the risk that takes place due to the internal

failures that can be a result of the various business activities. The risk may also take place

due to the external events that may takes place suddenly. As in the company TCW operates

in both wine and beef the operational risk is more.

Risk of reputations: The risk of reputation refers to that risk that takes place due to the

anticipation of loss the reputation of the business or negative fame. The risk of reputation is

high in the company of TCW as it works in excess of two sections.

Solution to 2A

The Internal control refers to the objectives confirmation of company in the adequacy and

proficiency in operations. It is a systematic assurance financial reporting arrangement which is to

be consistent with the laws, strategies and controls.

In TCW the Internal control is the process that is impacted by the organization

management are the group of trustees and various people who gives sensible confirmation for

the attainment of the goals of the –

• Compliance with the applicable controls and laws

• The various effectiveness and efficiency of the tasks

Financial risk: It is the monetary risk linked with the loss is known as financial risk. In the

present case of TCW, there is large financial risk because of the implications of new framework

of IT. Apart from the that since there are three of the segments of grapes, wines and beef they

may experience of loss of money.

Operational Risks: The operational risk is the risk that takes place due to the internal

failures that can be a result of the various business activities. The risk may also take place

due to the external events that may takes place suddenly. As in the company TCW operates

in both wine and beef the operational risk is more.

Risk of reputations: The risk of reputation refers to that risk that takes place due to the

anticipation of loss the reputation of the business or negative fame. The risk of reputation is

high in the company of TCW as it works in excess of two sections.

Solution to 2A

The Internal control refers to the objectives confirmation of company in the adequacy and

proficiency in operations. It is a systematic assurance financial reporting arrangement which is to

be consistent with the laws, strategies and controls.

In TCW the Internal control is the process that is impacted by the organization

management are the group of trustees and various people who gives sensible confirmation for

the attainment of the goals of the –

• Compliance with the applicable controls and laws

• The various effectiveness and efficiency of the tasks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

• Financial reporting reliability

In the TCW company the inward control components are taken in hand as per the of the standard

rules, if –

• There is a approval of the appropriate methods has been taken for the costs of capital

• Proper insurance scope has been provided for the assets

• The evaluation of depreciation is conducted efficiently to every period

• The salvage value and useful life have been determined properly

In the enterprise TCW, the organization considers the business profitability not just as

the function of revenue but also for sound resources management. The identified internal

controls are:

Effective control Risk alleviated Test of Control

Controlling environment The identified risks while

control of the TCW

environment is the reputational

risk and the operational risk.

The test of control is the moral

value check, managerial skills,

employees working honesty

and the company direction.

• Financial reporting reliability

In the TCW company the inward control components are taken in hand as per the of the standard

rules, if –

• There is a approval of the appropriate methods has been taken for the costs of capital

• Proper insurance scope has been provided for the assets

• The evaluation of depreciation is conducted efficiently to every period

• The salvage value and useful life have been determined properly

In the enterprise TCW, the organization considers the business profitability not just as

the function of revenue but also for sound resources management. The identified internal

controls are:

Effective control Risk alleviated Test of Control

Controlling environment The identified risks while

control of the TCW

environment is the reputational

risk and the operational risk.

The test of control is the moral

value check, managerial skills,

employees working honesty

and the company direction.

11AUDITING THEORY AND PRACTICE

Risk assessment In this control system, the

risks that have to be examined

are compliance risk and

financial risk. The assessment

risk would help in the

prediction of the risk

beforehand.

The assessment of risk deals

with the setting up of the

effective control over the

various external and internal

control of the risk associated

of the chosen company of

TCW.

Communication and

Information

The risk that is identified the

reputation risk and financial

risk. The effective control of

communication and

information makes the TCW

alert to take decisions in ration

to the stakeholders.

The relevant information that

is and needs to be taken for the

achievement of the

management goals. It is the

verifying process of the data in

relation with stakeholders.

Monitoring The operational risk and

financial risk are identified in

this control test (Simnett,

Carson & Vanstraelen, 2016).

It is the method of compliance

with the various regulations,

rules and laws.

It is the effectiveness control is

to protect the issues that may

take place in future for lack in

the efficient control.

Physical control Internal controls of physical

control faces two types of

risks. The first risk is physical

damage risk, theft of loss and

assets (Arens, Elder, Beasley

The physical control involves

in identification of the fixed

asset and verification of that

whether the administration

reviews periodically the asset

Risk assessment In this control system, the

risks that have to be examined

are compliance risk and

financial risk. The assessment

risk would help in the

prediction of the risk

beforehand.

The assessment of risk deals

with the setting up of the

effective control over the

various external and internal

control of the risk associated

of the chosen company of

TCW.

Communication and

Information

The risk that is identified the

reputation risk and financial

risk. The effective control of

communication and

information makes the TCW

alert to take decisions in ration

to the stakeholders.

The relevant information that

is and needs to be taken for the

achievement of the

management goals. It is the

verifying process of the data in

relation with stakeholders.

Monitoring The operational risk and

financial risk are identified in

this control test (Simnett,

Carson & Vanstraelen, 2016).

It is the method of compliance

with the various regulations,

rules and laws.

It is the effectiveness control is

to protect the issues that may

take place in future for lack in

the efficient control.

Physical control Internal controls of physical

control faces two types of

risks. The first risk is physical

damage risk, theft of loss and

assets (Arens, Elder, Beasley

The physical control involves

in identification of the fixed

asset and verification of that

whether the administration

reviews periodically the asset

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.