Auditing Theory and Practice: Financial Statement Analysis Report

VerifiedAdded on 2020/03/01

|13

|2907

|100

Report

AI Summary

This report analyzes auditing theory and practice, focusing on the financial statements of DIPL. It examines audit planning using analytical methods like ratio analysis and benchmarking to assess financial health and identify trends. The report identifies inherent risks, including employee inexperience, environmental factors, and IT system implementation issues, which can lead to material misstatements. It explores fraud risks such as employee engagement in fraudulent activities and financial reporting manipulation, highlighting the impact of management pressure and business entity characteristics. The analysis also addresses inventory valuation issues and provides recommendations for mitigating identified risks. The report offers a comprehensive overview of auditing principles and their application in a real-world business scenario.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Name of Student:

Name of University:

Author’s Note:

Auditing Theory and Practice

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Table of Contents

Answer to question 1:......................................................................................................................2

Explanation:.................................................................................................................................3

Answer to question 2:......................................................................................................................4

Answer to question 3:......................................................................................................................7

Answer to part A:.........................................................................................................................7

Answer to part B:.........................................................................................................................9

References:....................................................................................................................................10

Table of Contents

Answer to question 1:......................................................................................................................2

Explanation:.................................................................................................................................3

Answer to question 2:......................................................................................................................4

Answer to question 3:......................................................................................................................7

Answer to part A:.........................................................................................................................7

Answer to part B:.........................................................................................................................9

References:....................................................................................................................................10

2AUDITING THEORY AND PRACTICE

Answer to question 1:

The investigative method corresponding to the fiscal information of the DIPL could be

facilitated in the groundwork of the audit plan. Such an arrangement can be done in a specific

way, focussing on the guidelines, which is important to be complied to at the time of undertaking

of the audit. Chiefly, the assessor is enabled to maintain the total amount of the audit at a

significant level which assists in the reduction of the thought processes related to the clients

(Zureigat 2015). The diagnostic approach to the financial statements of the DIPL shows the

information dissemination method from it. Such an evaluative method, is possible to be

conducted by the use of a number of methods and techniques. With the help of the evaluation

analysis method with regard to the financial announcements, several accountants as also

economic analysts can use the financial announcements to understand and evaluate them to

arrive at crucial business decisions (Barr-Pulliam et al. 2017).

The type of the common sizing analytic method allows the fiscal announcements

assessment to a common point of reference. This causes the possible contrast of the fiscal

statements in association to the several items lines stated in the financial report along with the

method of reporting. As an example, it can be said that, the registration of the items like the

assets, liabilities as well as the equity of the owners in the fiscal reporting of the company along

with the investigational digression form the normal scenario (Bayer and Cowell 2016).The

procedure of benchmarking is considered as a fiscal procedure and it should be utilised for the

assessment of the audit plan. The variance of the original financial declaration from the basic

enables the deviation understanding as well as the evaluation of the recognised variance reason.

Along with this, the ratio analysis can be adjudged as a suitable analytical method which can be

Answer to question 1:

The investigative method corresponding to the fiscal information of the DIPL could be

facilitated in the groundwork of the audit plan. Such an arrangement can be done in a specific

way, focussing on the guidelines, which is important to be complied to at the time of undertaking

of the audit. Chiefly, the assessor is enabled to maintain the total amount of the audit at a

significant level which assists in the reduction of the thought processes related to the clients

(Zureigat 2015). The diagnostic approach to the financial statements of the DIPL shows the

information dissemination method from it. Such an evaluative method, is possible to be

conducted by the use of a number of methods and techniques. With the help of the evaluation

analysis method with regard to the financial announcements, several accountants as also

economic analysts can use the financial announcements to understand and evaluate them to

arrive at crucial business decisions (Barr-Pulliam et al. 2017).

The type of the common sizing analytic method allows the fiscal announcements

assessment to a common point of reference. This causes the possible contrast of the fiscal

statements in association to the several items lines stated in the financial report along with the

method of reporting. As an example, it can be said that, the registration of the items like the

assets, liabilities as well as the equity of the owners in the fiscal reporting of the company along

with the investigational digression form the normal scenario (Bayer and Cowell 2016).The

procedure of benchmarking is considered as a fiscal procedure and it should be utilised for the

assessment of the audit plan. The variance of the original financial declaration from the basic

enables the deviation understanding as well as the evaluation of the recognised variance reason.

Along with this, the ratio analysis can be adjudged as a suitable analytical method which can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

used for contrasting the fiscal declarations along with the assessment of the audit plan (Bepari

and Mollik 2015).

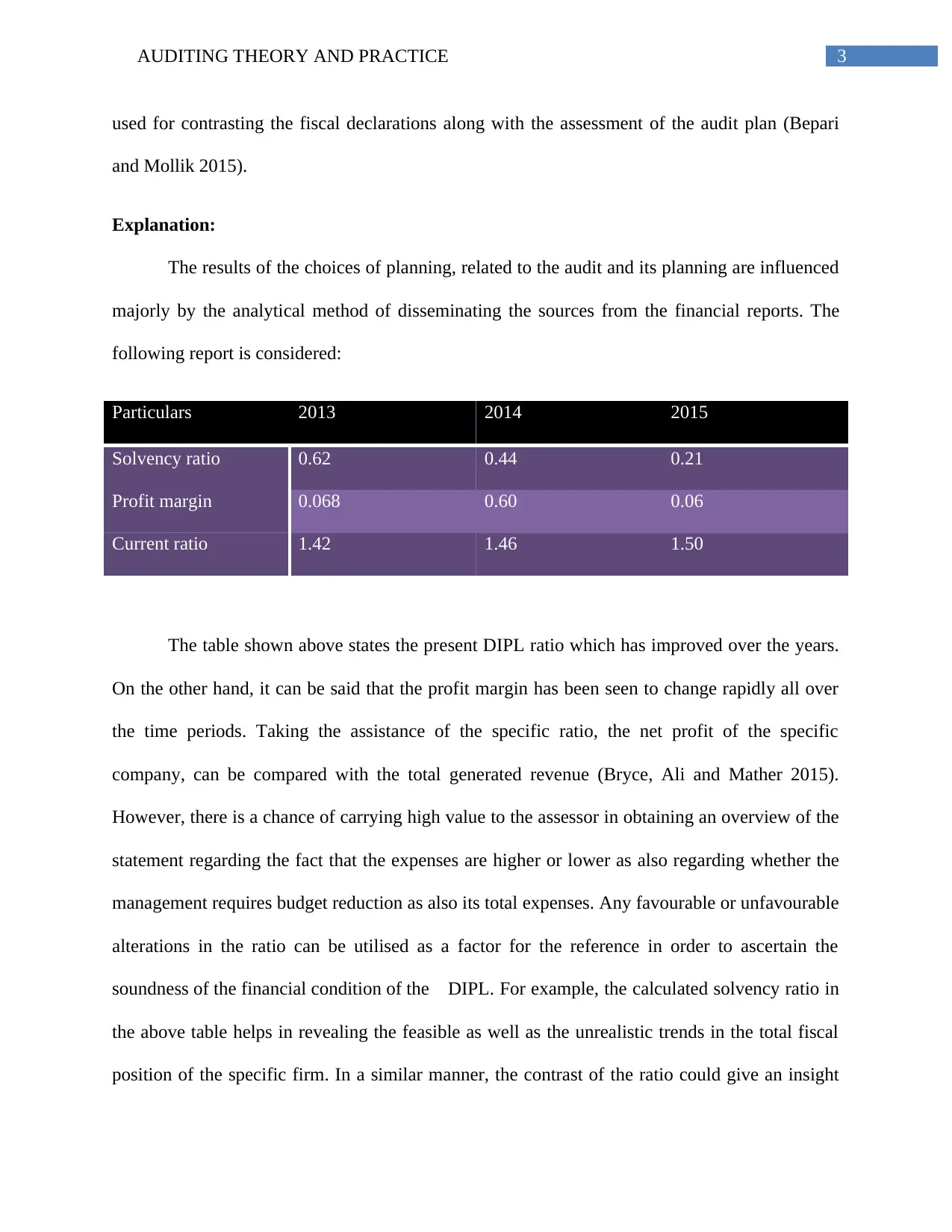

Explanation:

The results of the choices of planning, related to the audit and its planning are influenced

majorly by the analytical method of disseminating the sources from the financial reports. The

following report is considered:

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The table shown above states the present DIPL ratio which has improved over the years.

On the other hand, it can be said that the profit margin has been seen to change rapidly all over

the time periods. Taking the assistance of the specific ratio, the net profit of the specific

company, can be compared with the total generated revenue (Bryce, Ali and Mather 2015).

However, there is a chance of carrying high value to the assessor in obtaining an overview of the

statement regarding the fact that the expenses are higher or lower as also regarding whether the

management requires budget reduction as also its total expenses. Any favourable or unfavourable

alterations in the ratio can be utilised as a factor for the reference in order to ascertain the

soundness of the financial condition of the DIPL. For example, the calculated solvency ratio in

the above table helps in revealing the feasible as well as the unrealistic trends in the total fiscal

position of the specific firm. In a similar manner, the contrast of the ratio could give an insight

used for contrasting the fiscal declarations along with the assessment of the audit plan (Bepari

and Mollik 2015).

Explanation:

The results of the choices of planning, related to the audit and its planning are influenced

majorly by the analytical method of disseminating the sources from the financial reports. The

following report is considered:

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The table shown above states the present DIPL ratio which has improved over the years.

On the other hand, it can be said that the profit margin has been seen to change rapidly all over

the time periods. Taking the assistance of the specific ratio, the net profit of the specific

company, can be compared with the total generated revenue (Bryce, Ali and Mather 2015).

However, there is a chance of carrying high value to the assessor in obtaining an overview of the

statement regarding the fact that the expenses are higher or lower as also regarding whether the

management requires budget reduction as also its total expenses. Any favourable or unfavourable

alterations in the ratio can be utilised as a factor for the reference in order to ascertain the

soundness of the financial condition of the DIPL. For example, the calculated solvency ratio in

the above table helps in revealing the feasible as well as the unrealistic trends in the total fiscal

position of the specific firm. In a similar manner, the contrast of the ratio could give an insight

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

into the long as well as short term business necessities. Thus it is possible for the auditors to gain

an insight into the DIPPL’s relative position over the entire time period along with the evaluation

of the factors which leads to a position of the organisation which is not desirable (Cason, Friesen

and Gangadharan 2016).

Answer to question 2:

Many noteworthy factors are intrinsic in the auditing procedure that comprises the

incident of materialistic misstatements in the monetary declarations of a particular unit. It can

however be said that different natures of both organised as well as unorganised risks highlighting

the method in which the economic misstatements exist in the fiscal announcements of the

organisation. In addition to this the identified risks may be because of the fiscal as well as non-

fiscal factors that can subsequently stop a particular unit from reflecting a view of the financial

announcements. Depending on this information from Devos and Zackrisson (2015), the obtained

risks may be related to many omission risks related to the risks of any unimaginable errors of

particular bookkeepers. Thus it can be stated that it is the business risk for the business functions

of the DIPL.

Apart from this, the workers of the DIPL are not experienced enough and do not have the

required skill that has led to the total inherent organisational risk. In addition to this, such a lack

of experience can cause occurrence of errors or mistakes, increasing the innate risks. This is

because of the fact that the workers contribute a significant part of the company and it is not

practicable for the firm to be sure about its success in the future without the proper amount of

inputs from the employees. Apart from this, the other aspects contributing to the innate risk can

be divided into numerous segments like the external as well as the environmental aspects as also

into the long as well as short term business necessities. Thus it is possible for the auditors to gain

an insight into the DIPPL’s relative position over the entire time period along with the evaluation

of the factors which leads to a position of the organisation which is not desirable (Cason, Friesen

and Gangadharan 2016).

Answer to question 2:

Many noteworthy factors are intrinsic in the auditing procedure that comprises the

incident of materialistic misstatements in the monetary declarations of a particular unit. It can

however be said that different natures of both organised as well as unorganised risks highlighting

the method in which the economic misstatements exist in the fiscal announcements of the

organisation. In addition to this the identified risks may be because of the fiscal as well as non-

fiscal factors that can subsequently stop a particular unit from reflecting a view of the financial

announcements. Depending on this information from Devos and Zackrisson (2015), the obtained

risks may be related to many omission risks related to the risks of any unimaginable errors of

particular bookkeepers. Thus it can be stated that it is the business risk for the business functions

of the DIPL.

Apart from this, the workers of the DIPL are not experienced enough and do not have the

required skill that has led to the total inherent organisational risk. In addition to this, such a lack

of experience can cause occurrence of errors or mistakes, increasing the innate risks. This is

because of the fact that the workers contribute a significant part of the company and it is not

practicable for the firm to be sure about its success in the future without the proper amount of

inputs from the employees. Apart from this, the other aspects contributing to the innate risk can

be divided into numerous segments like the external as well as the environmental aspects as also

5AUDITING THEORY AND PRACTICE

the falsified exercises. The ecological aspects showing the method towards the innate risk

constitutes the speedy alterations where the matters can possibly be connected to the inventory

and its valuation, the immense market competition as also the lack of enough money. Barring

this, there is the possibility of materialistic misstatements which can direct the DIPL towards the

innate risks in the coming years.

The analytic procedure of the existing situation of the DIPL shows the fact that the issues

as well as the complexities relating to the succession of the CEO comprise the innate risks as

well. At heart it can be said that the CEO succession is vastly different as the candidates are

individualistic. Thus the procedural commencement without adhering to the said strategies, delay

in the initiation process as well as the ineffective connection in case of the CEO as well as the

staff may result in an intrinsic risk (Zureigat 2015).

The case analysis which is given implies that the implementation procedure of the IT

system has led to several issues. DIPL has employee shortage for managing the implementation

procedure as also the method of installing the reconciliation and the testing process which should

genuinely be done before the end of the time period (Stephenson et al. 2015). In addition to this,

the previous assessment stated was recorded in a specific manner as viable. Thus it results in the

materialistic misstatements due to the inherent factors where there is a deletion error in a definite

fiscal announcement.

The staff members of the DIPL, are required to follow an appropriate sequence for

registering the receivable accounts as well as the ledgers associated to the receivable accounts.

Along with this, bank reconciliation is necessary to be appropriately recorded as well (Mumford

et al. 2014).

the falsified exercises. The ecological aspects showing the method towards the innate risk

constitutes the speedy alterations where the matters can possibly be connected to the inventory

and its valuation, the immense market competition as also the lack of enough money. Barring

this, there is the possibility of materialistic misstatements which can direct the DIPL towards the

innate risks in the coming years.

The analytic procedure of the existing situation of the DIPL shows the fact that the issues

as well as the complexities relating to the succession of the CEO comprise the innate risks as

well. At heart it can be said that the CEO succession is vastly different as the candidates are

individualistic. Thus the procedural commencement without adhering to the said strategies, delay

in the initiation process as well as the ineffective connection in case of the CEO as well as the

staff may result in an intrinsic risk (Zureigat 2015).

The case analysis which is given implies that the implementation procedure of the IT

system has led to several issues. DIPL has employee shortage for managing the implementation

procedure as also the method of installing the reconciliation and the testing process which should

genuinely be done before the end of the time period (Stephenson et al. 2015). In addition to this,

the previous assessment stated was recorded in a specific manner as viable. Thus it results in the

materialistic misstatements due to the inherent factors where there is a deletion error in a definite

fiscal announcement.

The staff members of the DIPL, are required to follow an appropriate sequence for

registering the receivable accounts as well as the ledgers associated to the receivable accounts.

Along with this, bank reconciliation is necessary to be appropriately recorded as well (Mumford

et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

It can further be said that the registration of revenue found form the e-book as also taking

into account the reprinting of the textbook had a chance of possibly resulting in the inherent risks

due to the intricacies associated with the procedure. Finally, the valuation applicable to the raw

materials at an average cost is very much below the present cost of paper.

The inherent risks can be adjudged as the receptiveness of a specific assertion in

relevance to the material misstatements and are shown precisely as follows:

Increasing employee and management burdens:

It is due to the mounting burden on the DIPL and its staff that it has resulted in the

imprecise bookkeeping. As a result, numerous characteristics have taken place including the

propensity in the cash flow encountering, low level of liquidity as well as the operational results

(Nalewaik and Mills 2016).

Management Integrity as a whole:

Based on the case study, the management procedure of the DIPL does not possess the

right amount of integrity which is wanted for readiness towards any possible loss in the business

community (Milonas et al. 2016).

Excessive pressure on the management:

Sometimes, it might occur that there is the existence of incentives for the management.

As a result, the fiscal announcements have several misstatements.

Nature of Business Entity:

It can further be said that the registration of revenue found form the e-book as also taking

into account the reprinting of the textbook had a chance of possibly resulting in the inherent risks

due to the intricacies associated with the procedure. Finally, the valuation applicable to the raw

materials at an average cost is very much below the present cost of paper.

The inherent risks can be adjudged as the receptiveness of a specific assertion in

relevance to the material misstatements and are shown precisely as follows:

Increasing employee and management burdens:

It is due to the mounting burden on the DIPL and its staff that it has resulted in the

imprecise bookkeeping. As a result, numerous characteristics have taken place including the

propensity in the cash flow encountering, low level of liquidity as well as the operational results

(Nalewaik and Mills 2016).

Management Integrity as a whole:

Based on the case study, the management procedure of the DIPL does not possess the

right amount of integrity which is wanted for readiness towards any possible loss in the business

community (Milonas et al. 2016).

Excessive pressure on the management:

Sometimes, it might occur that there is the existence of incentives for the management.

As a result, the fiscal announcements have several misstatements.

Nature of Business Entity:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

DIPL contributes to the most valuable growth in the financial as well as the situations of

a competitive nature. Furthermore, these factors may have an impact on the inherent risks of the

business units for the method of audit planning evaluation in a significant fashion (Gani,

Wijeweera and Eddie 2017).

Answer to question 3:

Answer to part A:

Based on the findings in Saad (2014), the fraud risks had a possibility of resulting in

extreme losses of the assets due to huge amount of fraudulent activities. The deficiency of

motivation or the drive in the workforce because of the additional pressure of work on the staff,

can have a chance of causing significantly increased risks of fraud. Further, strong amount of

pressure is put on the management of the corporation due to the announcement of the particular

fiscal results in an effort to avoid the generation of the guarantees.

The major types of risks identified in the reference of the DIPL’s business operations

are briefly stated as follows:

Types of risk Identification

Engagement of entire work force in fraudulent

performances

The only risk of fraud that might take place due to

the DIPL’s business operations in the engagement

of the workforce in the activities of a fraudulent

nature because of a better nature and a better

dissatisfaction level of the employees. The case

study of the operations of the DIPL states that the

board has put several amount of pressure on the

DIPL contributes to the most valuable growth in the financial as well as the situations of

a competitive nature. Furthermore, these factors may have an impact on the inherent risks of the

business units for the method of audit planning evaluation in a significant fashion (Gani,

Wijeweera and Eddie 2017).

Answer to question 3:

Answer to part A:

Based on the findings in Saad (2014), the fraud risks had a possibility of resulting in

extreme losses of the assets due to huge amount of fraudulent activities. The deficiency of

motivation or the drive in the workforce because of the additional pressure of work on the staff,

can have a chance of causing significantly increased risks of fraud. Further, strong amount of

pressure is put on the management of the corporation due to the announcement of the particular

fiscal results in an effort to avoid the generation of the guarantees.

The major types of risks identified in the reference of the DIPL’s business operations

are briefly stated as follows:

Types of risk Identification

Engagement of entire work force in fraudulent

performances

The only risk of fraud that might take place due to

the DIPL’s business operations in the engagement

of the workforce in the activities of a fraudulent

nature because of a better nature and a better

dissatisfaction level of the employees. The case

study of the operations of the DIPL states that the

board has put several amount of pressure on the

8AUDITING THEORY AND PRACTICE

company while acquiring an interesting system of

accounting. Such an additional amount of the

pressure on the staff, while doing the installation of

the new information for the accounting might result

in fraud. This implies that the staff may be involved

in actives which are fraudulent in nature. These

activities might involve managing the behaviours

as well as the process of reconciliation in a suitable

fashion along with the materialistic misstatements.

The case provided shows that the ineffective

management of the procedural execution is related

to the implementation of the information

technology and results in incorrect allotment of

various transactions at the end of the period. This

results in severe loss due to the misstatements as

well as the fraudulent risks.

Method corresponding to economic reporting Another fraud risk may confront the business

operations of the DIPL in undertaking the risk

connected to the financial fraud of reporting into

account. At the time of specific situations, it has

been observed that the additional information from

external financers or the management. This method

of expectation is due to achieve the particular

targets of different types of goal performance to

qualify for getting the debt. There is an increased

risk of wrong declarations of an economic nature.

company while acquiring an interesting system of

accounting. Such an additional amount of the

pressure on the staff, while doing the installation of

the new information for the accounting might result

in fraud. This implies that the staff may be involved

in actives which are fraudulent in nature. These

activities might involve managing the behaviours

as well as the process of reconciliation in a suitable

fashion along with the materialistic misstatements.

The case provided shows that the ineffective

management of the procedural execution is related

to the implementation of the information

technology and results in incorrect allotment of

various transactions at the end of the period. This

results in severe loss due to the misstatements as

well as the fraudulent risks.

Method corresponding to economic reporting Another fraud risk may confront the business

operations of the DIPL in undertaking the risk

connected to the financial fraud of reporting into

account. At the time of specific situations, it has

been observed that the additional information from

external financers or the management. This method

of expectation is due to achieve the particular

targets of different types of goal performance to

qualify for getting the debt. There is an increased

risk of wrong declarations of an economic nature.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

Depending on the balance sheet statement of the

DIPL, the net revenue of the organisation

increased. It was because of the organisations’

failure in maintaining standards that it became

ineligible for acquiring the appropriate funds

(Graham 2015).

Answer to part B:

Based on the case study given, it can be said that the method of understanding related to

the inventory valuation of many raw materials at a particular range of average costs is not correct

or appropriate. This is because of the fact that the existing paper cost is higher in comparison to

the average cost (Gray et al. 2016). The associated risk related to the fiscal reporting might have

been recognised by the dissection of the economic statements on the part of the assessors.

Benchmarking is nothing but an analytical procedure which can be utilised for the assessment of

the audit plan. The actual financial declaration from the standard assists in recognising the

deviation and helps in the recognised variance evaluation.

Depending on the balance sheet statement of the

DIPL, the net revenue of the organisation

increased. It was because of the organisations’

failure in maintaining standards that it became

ineligible for acquiring the appropriate funds

(Graham 2015).

Answer to part B:

Based on the case study given, it can be said that the method of understanding related to

the inventory valuation of many raw materials at a particular range of average costs is not correct

or appropriate. This is because of the fact that the existing paper cost is higher in comparison to

the average cost (Gray et al. 2016). The associated risk related to the fiscal reporting might have

been recognised by the dissection of the economic statements on the part of the assessors.

Benchmarking is nothing but an analytical procedure which can be utilised for the assessment of

the audit plan. The actual financial declaration from the standard assists in recognising the

deviation and helps in the recognised variance evaluation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

11AUDITING THEORY AND PRACTICE

Gani, I., Wijeweera, A. and Eddie, I., 2017. Audit Committee Compliance and Company

Performance Nexus: Evidence from ASX Listed Companies. Business and Economic

Research, 7(2), pp.135-145.

Graham, L., 2015. Internal Control Audit and Compliance: Documentation and Testing Under

the New COSO Framework. John Wiley & Sons.

Gray, S.E., Sekendiz, B., Norton, K., Dietrich, J., Keyzer, P., Coyle, I.R. and Finch, C., 2016.

The development and application of an observational audit tool for use in Australian fitness

facilities. Journal of Fitness Research, 5(1), p.29.

Milonas, A., Hutchinson, A., Charlesworth, D., Doric, A., Green, J. and Considine, J., 2016. Post

resuscitation management of cardiac arrest patients in the critical care environment: A

retrospective audit of compliance with evidence based guidelines. Australian Critical Care.

Mumford, V., Greenfield, D., Hogden, A., Debono, D., Gospodarevskaya, E., Forde, K.,

Westbrook, J. and Braithwaite, J., 2014. Disentangling quality and safety indicator data: a

longitudinal, comparative study of hand hygiene compliance and accreditation outcomes in 96

Australian hospitals. BMJ open, 4(9), p.e005284.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Gani, I., Wijeweera, A. and Eddie, I., 2017. Audit Committee Compliance and Company

Performance Nexus: Evidence from ASX Listed Companies. Business and Economic

Research, 7(2), pp.135-145.

Graham, L., 2015. Internal Control Audit and Compliance: Documentation and Testing Under

the New COSO Framework. John Wiley & Sons.

Gray, S.E., Sekendiz, B., Norton, K., Dietrich, J., Keyzer, P., Coyle, I.R. and Finch, C., 2016.

The development and application of an observational audit tool for use in Australian fitness

facilities. Journal of Fitness Research, 5(1), p.29.

Milonas, A., Hutchinson, A., Charlesworth, D., Doric, A., Green, J. and Considine, J., 2016. Post

resuscitation management of cardiac arrest patients in the critical care environment: A

retrospective audit of compliance with evidence based guidelines. Australian Critical Care.

Mumford, V., Greenfield, D., Hogden, A., Debono, D., Gospodarevskaya, E., Forde, K.,

Westbrook, J. and Braithwaite, J., 2014. Disentangling quality and safety indicator data: a

longitudinal, comparative study of hand hygiene compliance and accreditation outcomes in 96

Australian hospitals. BMJ open, 4(9), p.e005284.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.