Auditing Theory and Practice: Enhanced Auditor Reporting in Australia

VerifiedAdded on 2023/06/05

|15

|3175

|450

Report

AI Summary

This report examines the adoption of enhanced auditor reporting in Australia, focusing on ASX-listed companies. It reviews the FY 2017 annual report of Beach Energy Limited, analyzing auditor independence, non-audit services, remuneration, key audit matters, and audit procedures. The report also covers the audit committee's role, the type of audit opinion expressed, management's and auditor's responsibilities, and the absence of material subsequent events. An evaluation of the effectiveness of reported information is provided, along with potential missing information and questions for the AGM. The auditor expressed an unqualified opinion, stating that the financial statements presented a true and fair view of the company's position.

AUDITING THEORY AND PRACTICE 1

AUDITING THEORY AND PRACTICE

By (Name)

Name of the Course

Professor

Name of University

City and State

Date

Word Count: 2600

AUDITING THEORY AND PRACTICE

By (Name)

Name of the Course

Professor

Name of University

City and State

Date

Word Count: 2600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE 2

Executive Summary

This main purpose of this paper is to give research findings on how enhanced reporting of

the auditor has been adopted in Australia. In order to make improvements in the quality of audit

reporting, public companies which are listed have been required to disclose or report on the key

audit matters as a way of improving the material information that is communicated to the users

of financial statements. Plain English must be used in disclosing these matters. These new

disclosure requirements of the auditor started in December 2016. The main aim of this paper is to

review an annual report of a company listed on ASX that is in the S&P/ASX 300 list. For the

purpose of this assignment, Beach Energy Limited is chosen. The annual report of Beach Energy

Limited has been critically reviewed and examined. As per the auditor’s opinion, the financial

reports have been recommended for use by the company’s stakeholders and the general public

(Nigrini 2012, pp. 48). This is because the reports reflect a true and fair financial position as at

June 30, 2017 and financial performance of the company for the financial period then ended

(Beach Energy Ltd 2017, pp. 54-118).

Executive Summary

This main purpose of this paper is to give research findings on how enhanced reporting of

the auditor has been adopted in Australia. In order to make improvements in the quality of audit

reporting, public companies which are listed have been required to disclose or report on the key

audit matters as a way of improving the material information that is communicated to the users

of financial statements. Plain English must be used in disclosing these matters. These new

disclosure requirements of the auditor started in December 2016. The main aim of this paper is to

review an annual report of a company listed on ASX that is in the S&P/ASX 300 list. For the

purpose of this assignment, Beach Energy Limited is chosen. The annual report of Beach Energy

Limited has been critically reviewed and examined. As per the auditor’s opinion, the financial

reports have been recommended for use by the company’s stakeholders and the general public

(Nigrini 2012, pp. 48). This is because the reports reflect a true and fair financial position as at

June 30, 2017 and financial performance of the company for the financial period then ended

(Beach Energy Ltd 2017, pp. 54-118).

AUDITING THEORY AND PRACTICE 3

TABLE OF CONTENTS

CONTENT PAGE

Introduction.................................................................................................................................................4

Auditor’s independence...............................................................................................................................4

Nature of Non-audit services provided...................................................................................................…...5

Remuneration of the Auditor and the Reasons for the changes…………………………………………….7

Key audit matters and procedures performed...............................................................................................7

Audit committee........................................................................................................................................10

Type of audit opinion expressed.........................................................................................................….....10

Director’s and managements’ responsibilities and those of the auditor…..................................................11

Material subsequent events………………………………………………………………………………..11

Evaluation of the Effectiveness of Material Information Reported by the Auditor……………………...12

Material Information Which Could Be Missing..............................................................................…........12

Questions for Follow-up during the AGM…………………………………...……………………………13

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

TABLE OF CONTENTS

CONTENT PAGE

Introduction.................................................................................................................................................4

Auditor’s independence...............................................................................................................................4

Nature of Non-audit services provided...................................................................................................…...5

Remuneration of the Auditor and the Reasons for the changes…………………………………………….7

Key audit matters and procedures performed...............................................................................................7

Audit committee........................................................................................................................................10

Type of audit opinion expressed.........................................................................................................….....10

Director’s and managements’ responsibilities and those of the auditor…..................................................11

Material subsequent events………………………………………………………………………………..11

Evaluation of the Effectiveness of Material Information Reported by the Auditor……………………...12

Material Information Which Could Be Missing..............................................................................…........12

Questions for Follow-up during the AGM…………………………………...……………………………13

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING THEORY AND PRACTICE 4

Introduction

Beach Energy Limited is a public company which is listed on ASX and operates in the

energy sector dealing mainly with oil and gas, exploration as well as production. The head office

of the company is located in Adelaide, South Australia (Moeller 2009, pp. 36). The company

supplies its products mainly to the gas market in the east coast of Australia. The FY 2017 annual

report of the company has been analyzed and reviewed (Beach Energy Ltd 2017, pp. 54-118). A

summary of the research findings has been given in the various sections below.

Auditor’s Independence

Auditor’s independence mostly refers to the ability of an auditor to carry out the financial

audit in a free and objective manner, without being subjective. According to the FY 2017 annual

report, the lead auditor has made a declaration the audit has been carried out as per the provisions

of Section 307C of the Corporations Act of 2001. This declaration has been made to the

company’s directors (Messier, Glover and Prawitt 2008, pp. 58). The auditor has mentioned that

to the best of his knowledge, relating to the FY 2017 financial audit, his independence

requirements have not been contravened as required by the Corporations Act of 2001 relating to

the audit, and that the code of professional conduct which are applicable have not been

contravened in any way by the auditor (Singleton and Singleton 2010, pp. 45).

The Nature of the Non-Audit Services Provided

The company, Beach Energy limited, may choose to engage the auditor for services not

related to its financial audit where it is considered that such business engagement between Beach

and the auditor would be necessary and beneficial, due to the experience and expertise required

in particular cases. The position of the non-audit services provided has been considered by the

Introduction

Beach Energy Limited is a public company which is listed on ASX and operates in the

energy sector dealing mainly with oil and gas, exploration as well as production. The head office

of the company is located in Adelaide, South Australia (Moeller 2009, pp. 36). The company

supplies its products mainly to the gas market in the east coast of Australia. The FY 2017 annual

report of the company has been analyzed and reviewed (Beach Energy Ltd 2017, pp. 54-118). A

summary of the research findings has been given in the various sections below.

Auditor’s Independence

Auditor’s independence mostly refers to the ability of an auditor to carry out the financial

audit in a free and objective manner, without being subjective. According to the FY 2017 annual

report, the lead auditor has made a declaration the audit has been carried out as per the provisions

of Section 307C of the Corporations Act of 2001. This declaration has been made to the

company’s directors (Messier, Glover and Prawitt 2008, pp. 58). The auditor has mentioned that

to the best of his knowledge, relating to the FY 2017 financial audit, his independence

requirements have not been contravened as required by the Corporations Act of 2001 relating to

the audit, and that the code of professional conduct which are applicable have not been

contravened in any way by the auditor (Singleton and Singleton 2010, pp. 45).

The Nature of the Non-Audit Services Provided

The company, Beach Energy limited, may choose to engage the auditor for services not

related to its financial audit where it is considered that such business engagement between Beach

and the auditor would be necessary and beneficial, due to the experience and expertise required

in particular cases. The position of the non-audit services provided has been considered by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE 5

board and it has been confirmed that they are compatible with the general requirements of the

independence of the auditor, as set out by the Corporations Act of 2001 (Knechel and Salterio

2016, pp. 46). By providing the non-audit services to the company, the independence of the

auditor was not compromised at all (Beach Energy Ltd 2017, pp. 118). The non-audit services

offered by the auditor to the audit client relate to legal matters such as:

a. IT services

b. Tax services in Australia

c. Tax and other services for subsidiaries in overseas

d. Transaction services for Drillserach merger

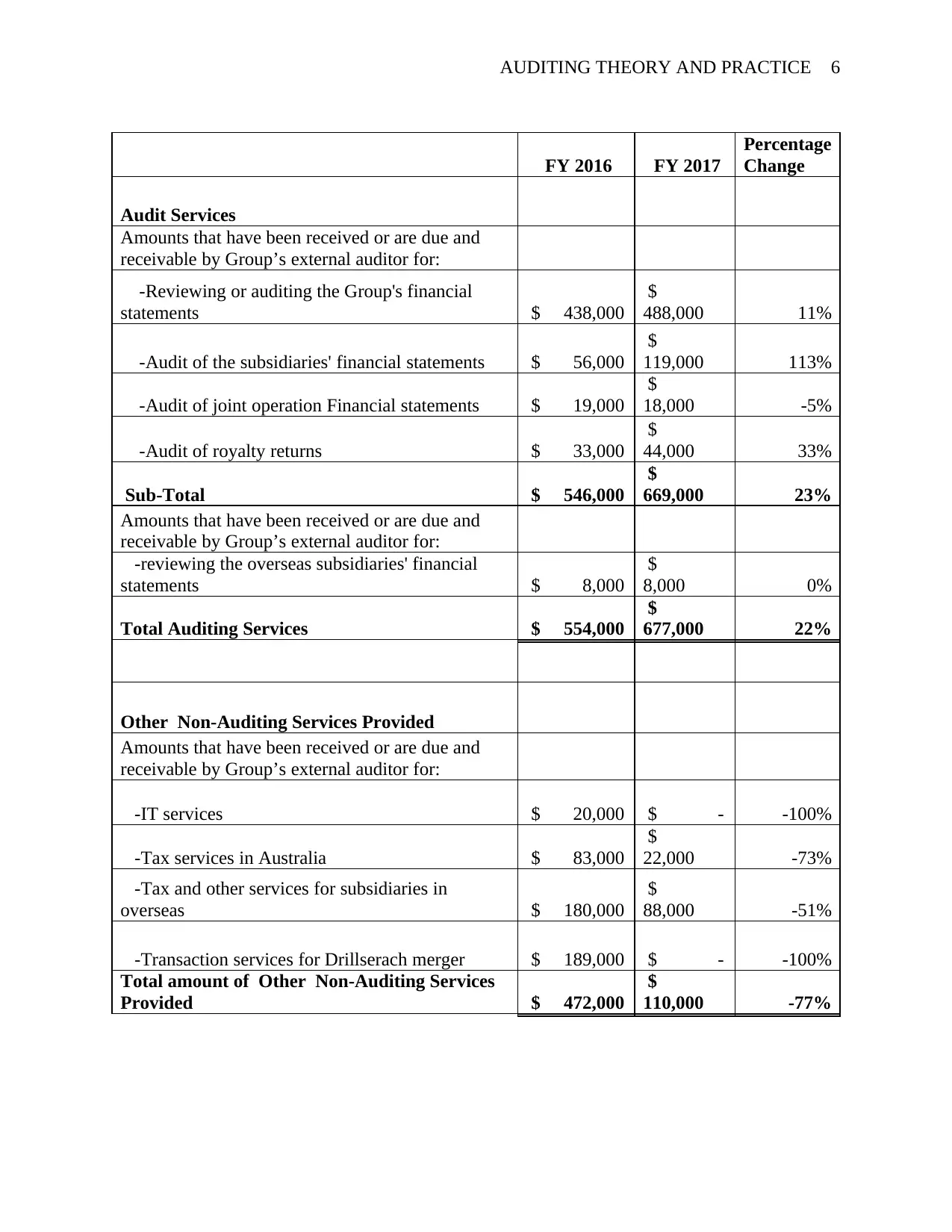

Remuneration of the Auditor and the Reasons for the changes

The remuneration of the auditor for Beach Energy Limited has been summarized in the

table below for the prior financial years.

board and it has been confirmed that they are compatible with the general requirements of the

independence of the auditor, as set out by the Corporations Act of 2001 (Knechel and Salterio

2016, pp. 46). By providing the non-audit services to the company, the independence of the

auditor was not compromised at all (Beach Energy Ltd 2017, pp. 118). The non-audit services

offered by the auditor to the audit client relate to legal matters such as:

a. IT services

b. Tax services in Australia

c. Tax and other services for subsidiaries in overseas

d. Transaction services for Drillserach merger

Remuneration of the Auditor and the Reasons for the changes

The remuneration of the auditor for Beach Energy Limited has been summarized in the

table below for the prior financial years.

AUDITING THEORY AND PRACTICE 6

FY 2016 FY 2017

Percentage

Change

Audit Services

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-Reviewing or auditing the Group's financial

statements $ 438,000

$

488,000 11%

-Audit of the subsidiaries' financial statements $ 56,000

$

119,000 113%

-Audit of joint operation Financial statements $ 19,000

$

18,000 -5%

-Audit of royalty returns $ 33,000

$

44,000 33%

Sub-Total $ 546,000

$

669,000 23%

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-reviewing the overseas subsidiaries' financial

statements $ 8,000

$

8,000 0%

Total Auditing Services $ 554,000

$

677,000 22%

Other Non-Auditing Services Provided

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-IT services $ 20,000 $ - -100%

-Tax services in Australia $ 83,000

$

22,000 -73%

-Tax and other services for subsidiaries in

overseas $ 180,000

$

88,000 -51%

-Transaction services for Drillserach merger $ 189,000 $ - -100%

Total amount of Other Non-Auditing Services

Provided $ 472,000

$

110,000 -77%

FY 2016 FY 2017

Percentage

Change

Audit Services

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-Reviewing or auditing the Group's financial

statements $ 438,000

$

488,000 11%

-Audit of the subsidiaries' financial statements $ 56,000

$

119,000 113%

-Audit of joint operation Financial statements $ 19,000

$

18,000 -5%

-Audit of royalty returns $ 33,000

$

44,000 33%

Sub-Total $ 546,000

$

669,000 23%

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-reviewing the overseas subsidiaries' financial

statements $ 8,000

$

8,000 0%

Total Auditing Services $ 554,000

$

677,000 22%

Other Non-Auditing Services Provided

Amounts that have been received or are due and

receivable by Group’s external auditor for:

-IT services $ 20,000 $ - -100%

-Tax services in Australia $ 83,000

$

22,000 -73%

-Tax and other services for subsidiaries in

overseas $ 180,000

$

88,000 -51%

-Transaction services for Drillserach merger $ 189,000 $ - -100%

Total amount of Other Non-Auditing Services

Provided $ 472,000

$

110,000 -77%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING THEORY AND PRACTICE 7

As observed in the above analysis, the remuneration of the auditor for other non-audit

services dropped significantly in the FY 2017 by a total of 77%. This decrease can be attributed

to the lack of the need for Beach Energy Limited to acquire other non-audit professional services

from the auditor, thus causing the fundamental reductions in the remuneration of the auditor

(Beach Energy Ltd 2017, pp. 118). With regard to the services related to the audit of the group

and its subsidiaries both local and overseas, there was an overall increase of 22% in the

remuneration paid to the auditor. This increase was most probably due to the additional mergers

and acquisitions made by the firm during the financial year ended June 30, 2017. For instance,

there was an increase of the remuneration paid to the auditor of 113% relating to audit and

review of the subsidiaries' financial statements (Hopwood, Leiner and Young 2011, pp. 98).

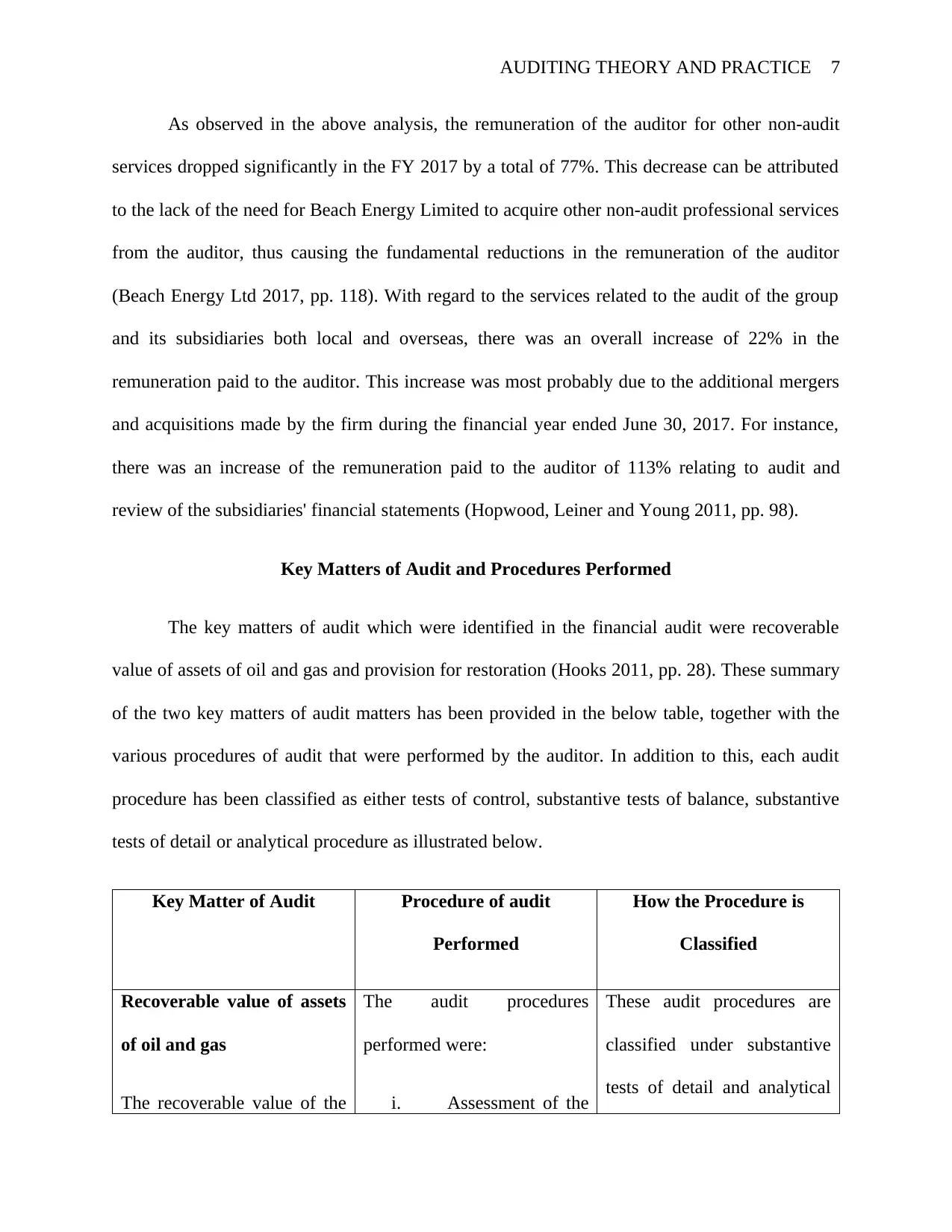

Key Matters of Audit and Procedures Performed

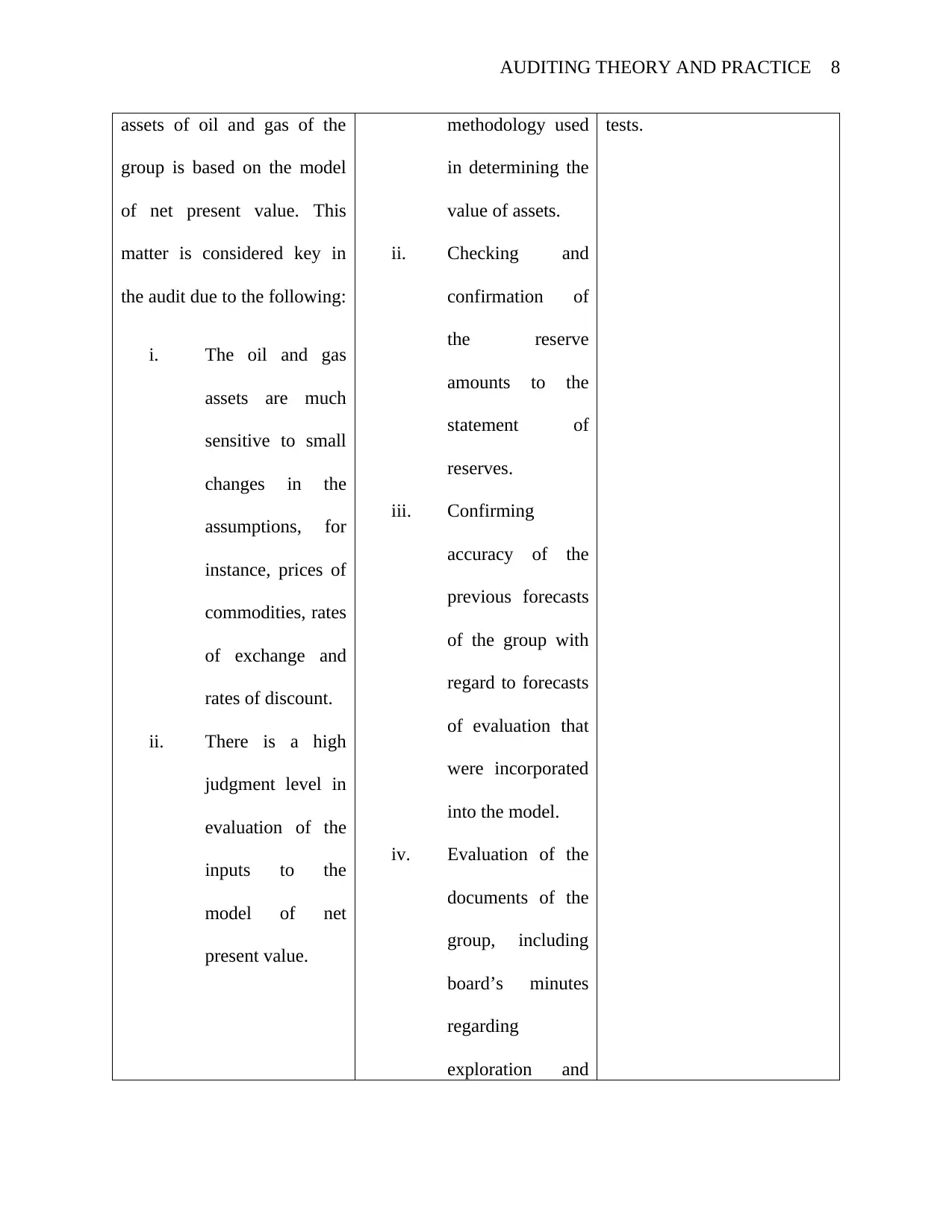

The key matters of audit which were identified in the financial audit were recoverable

value of assets of oil and gas and provision for restoration (Hooks 2011, pp. 28). These summary

of the two key matters of audit matters has been provided in the below table, together with the

various procedures of audit that were performed by the auditor. In addition to this, each audit

procedure has been classified as either tests of control, substantive tests of balance, substantive

tests of detail or analytical procedure as illustrated below.

Key Matter of Audit Procedure of audit

Performed

How the Procedure is

Classified

Recoverable value of assets

of oil and gas

The recoverable value of the

The audit procedures

performed were:

i. Assessment of the

These audit procedures are

classified under substantive

tests of detail and analytical

As observed in the above analysis, the remuneration of the auditor for other non-audit

services dropped significantly in the FY 2017 by a total of 77%. This decrease can be attributed

to the lack of the need for Beach Energy Limited to acquire other non-audit professional services

from the auditor, thus causing the fundamental reductions in the remuneration of the auditor

(Beach Energy Ltd 2017, pp. 118). With regard to the services related to the audit of the group

and its subsidiaries both local and overseas, there was an overall increase of 22% in the

remuneration paid to the auditor. This increase was most probably due to the additional mergers

and acquisitions made by the firm during the financial year ended June 30, 2017. For instance,

there was an increase of the remuneration paid to the auditor of 113% relating to audit and

review of the subsidiaries' financial statements (Hopwood, Leiner and Young 2011, pp. 98).

Key Matters of Audit and Procedures Performed

The key matters of audit which were identified in the financial audit were recoverable

value of assets of oil and gas and provision for restoration (Hooks 2011, pp. 28). These summary

of the two key matters of audit matters has been provided in the below table, together with the

various procedures of audit that were performed by the auditor. In addition to this, each audit

procedure has been classified as either tests of control, substantive tests of balance, substantive

tests of detail or analytical procedure as illustrated below.

Key Matter of Audit Procedure of audit

Performed

How the Procedure is

Classified

Recoverable value of assets

of oil and gas

The recoverable value of the

The audit procedures

performed were:

i. Assessment of the

These audit procedures are

classified under substantive

tests of detail and analytical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE 8

assets of oil and gas of the

group is based on the model

of net present value. This

matter is considered key in

the audit due to the following:

i. The oil and gas

assets are much

sensitive to small

changes in the

assumptions, for

instance, prices of

commodities, rates

of exchange and

rates of discount.

ii. There is a high

judgment level in

evaluation of the

inputs to the

model of net

present value.

methodology used

in determining the

value of assets.

ii. Checking and

confirmation of

the reserve

amounts to the

statement of

reserves.

iii. Confirming

accuracy of the

previous forecasts

of the group with

regard to forecasts

of evaluation that

were incorporated

into the model.

iv. Evaluation of the

documents of the

group, including

board’s minutes

regarding

exploration and

tests.

assets of oil and gas of the

group is based on the model

of net present value. This

matter is considered key in

the audit due to the following:

i. The oil and gas

assets are much

sensitive to small

changes in the

assumptions, for

instance, prices of

commodities, rates

of exchange and

rates of discount.

ii. There is a high

judgment level in

evaluation of the

inputs to the

model of net

present value.

methodology used

in determining the

value of assets.

ii. Checking and

confirmation of

the reserve

amounts to the

statement of

reserves.

iii. Confirming

accuracy of the

previous forecasts

of the group with

regard to forecasts

of evaluation that

were incorporated

into the model.

iv. Evaluation of the

documents of the

group, including

board’s minutes

regarding

exploration and

tests.

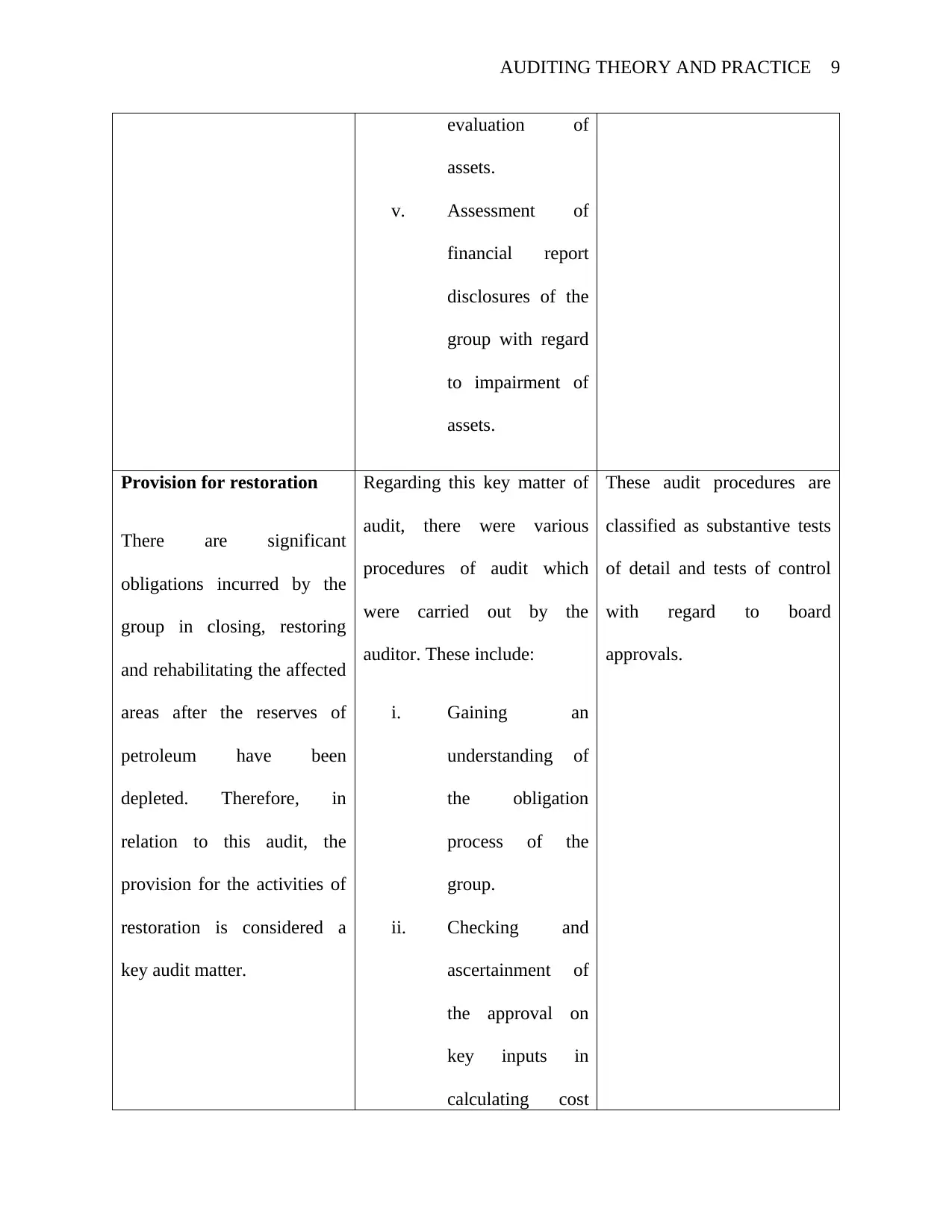

AUDITING THEORY AND PRACTICE 9

evaluation of

assets.

v. Assessment of

financial report

disclosures of the

group with regard

to impairment of

assets.

Provision for restoration

There are significant

obligations incurred by the

group in closing, restoring

and rehabilitating the affected

areas after the reserves of

petroleum have been

depleted. Therefore, in

relation to this audit, the

provision for the activities of

restoration is considered a

key audit matter.

Regarding this key matter of

audit, there were various

procedures of audit which

were carried out by the

auditor. These include:

i. Gaining an

understanding of

the obligation

process of the

group.

ii. Checking and

ascertainment of

the approval on

key inputs in

calculating cost

These audit procedures are

classified as substantive tests

of detail and tests of control

with regard to board

approvals.

evaluation of

assets.

v. Assessment of

financial report

disclosures of the

group with regard

to impairment of

assets.

Provision for restoration

There are significant

obligations incurred by the

group in closing, restoring

and rehabilitating the affected

areas after the reserves of

petroleum have been

depleted. Therefore, in

relation to this audit, the

provision for the activities of

restoration is considered a

key audit matter.

Regarding this key matter of

audit, there were various

procedures of audit which

were carried out by the

auditor. These include:

i. Gaining an

understanding of

the obligation

process of the

group.

ii. Checking and

ascertainment of

the approval on

key inputs in

calculating cost

These audit procedures are

classified as substantive tests

of detail and tests of control

with regard to board

approvals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING THEORY AND PRACTICE 10

estimates.

iii. Checking samples

of future cost

estimates.

Committee of Audit

Beach Energy Ltd has an established committee of audit that is made up of executive

directors and non-executive directors as well. For instance, the company appointed Joycelyn

Morton, a non-executive director, into its audit committee in order to comply with the

requirements of the Listing rule 12.7. The audit committee of Beach Energy Ltd performs the

following functions and responsibilities (Beach Energy Ltd 2017, pp. 121).

i. Reviewing annually the adequacy of the policies and obtaining approval of the board

on any necessary revisions on the policies.

ii. Reviewing the significant accounting policies of the organization as well as its

principles of financial reporting

iii. Reviewing the extent and scope of the general audit of the external auditor.

iv. Reviewing the annual engagement letter of the external auditor.

v. Facilitating a link of communication between directors and the external auditor.

Type of Auditor’s Opinion Expressed

With regard to the audit of the financial reports of Beach Energy Limited for FY 2017,

the auditor expressed an unqualified audit opinion (Beach Energy Ltd 2017, pp. 122). The

estimates.

iii. Checking samples

of future cost

estimates.

Committee of Audit

Beach Energy Ltd has an established committee of audit that is made up of executive

directors and non-executive directors as well. For instance, the company appointed Joycelyn

Morton, a non-executive director, into its audit committee in order to comply with the

requirements of the Listing rule 12.7. The audit committee of Beach Energy Ltd performs the

following functions and responsibilities (Beach Energy Ltd 2017, pp. 121).

i. Reviewing annually the adequacy of the policies and obtaining approval of the board

on any necessary revisions on the policies.

ii. Reviewing the significant accounting policies of the organization as well as its

principles of financial reporting

iii. Reviewing the extent and scope of the general audit of the external auditor.

iv. Reviewing the annual engagement letter of the external auditor.

v. Facilitating a link of communication between directors and the external auditor.

Type of Auditor’s Opinion Expressed

With regard to the audit of the financial reports of Beach Energy Limited for FY 2017,

the auditor expressed an unqualified audit opinion (Beach Energy Ltd 2017, pp. 122). The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING THEORY AND PRACTICE 11

auditor stated that, in their opinion, the financial statements of the company have been prepared

according to the Corporations Act of 2001. The financial reports give a true and fair financial

position of the company as at June 30, 20187 as well as its financial performance for the year

then ended (Eilifsen, Messier, Glover and Prawitt 2013, pp. 49).

Directors’ and Management’s Responsibilities and Those of the Auditor

According to the FY2017 annual report, the management of Beach Energy Ltd had the

following responsibilities regarding the financial reports (Elder, Beasley and Arens 2011, pp.

231).

a. Preparing and presenting the financial reports which give a true and fair presentation

of the financial position and performance of the entire group.

b. Implementation of internal controls necessary for enhancing and enabling preparation

of financial reports of the company that gives a true and fair view.

c. Assessment of the ability of the group to continue as a going concern entity. This

involves disclosure of applicable matters which relate to the going concern of the

company (Louwers, Ramsay, Sinason, Strawser and Thibodeau 2015, pp. 27).

However, the responsibilities of the auditor in the financial reports were:

a. Obtaining a reasonable and verifiable assurance regarding the whole financial report of

the company and analyzing if it is free from material financial information misstatements.

b. Issuing an auditor’s report expressing their opinion with regard to the company’s

financial reports (Cosserat and Rodda 2009, pp. 23).

Material Subsequent Events

auditor stated that, in their opinion, the financial statements of the company have been prepared

according to the Corporations Act of 2001. The financial reports give a true and fair financial

position of the company as at June 30, 20187 as well as its financial performance for the year

then ended (Eilifsen, Messier, Glover and Prawitt 2013, pp. 49).

Directors’ and Management’s Responsibilities and Those of the Auditor

According to the FY2017 annual report, the management of Beach Energy Ltd had the

following responsibilities regarding the financial reports (Elder, Beasley and Arens 2011, pp.

231).

a. Preparing and presenting the financial reports which give a true and fair presentation

of the financial position and performance of the entire group.

b. Implementation of internal controls necessary for enhancing and enabling preparation

of financial reports of the company that gives a true and fair view.

c. Assessment of the ability of the group to continue as a going concern entity. This

involves disclosure of applicable matters which relate to the going concern of the

company (Louwers, Ramsay, Sinason, Strawser and Thibodeau 2015, pp. 27).

However, the responsibilities of the auditor in the financial reports were:

a. Obtaining a reasonable and verifiable assurance regarding the whole financial report of

the company and analyzing if it is free from material financial information misstatements.

b. Issuing an auditor’s report expressing their opinion with regard to the company’s

financial reports (Cosserat and Rodda 2009, pp. 23).

Material Subsequent Events

AUDITING THEORY AND PRACTICE 12

According to the auditor’s report, it has been stated that there are no material subsequent

events which have arisen in the time interval between June 3,, 2017 and June 30, 2017 (Beach

Energy Ltd 2017, pp. 119).

Assessment of the Effectiveness of Material Information Reported by the Auditor

According to the report of the independent auditor regarding the financial audit of Beach

energy Ltd, the auditor has considered almost all material information which is considered

significant for use by external users of financial reports of the company. He has performed all

necessary procedures for ascertaining that the financial statements are free from any material

misstatement and that they are truly and fairly reflective of the financial position and financial

performance of the company (Carson 2009, pp. 78).

Material Information Which Could Be Under-Reported or Missing

Although the independent auditor has given an unqualified opinion in the report of his

audit, there are a few areas which have been under-reported. For instance, regarding business

combinations, full details have not been adequately explained in the financial reports. The

acquisition of 100% interests in the shares of Territory Oil and Gas by Beach Energy Ltd has not

been explained adequately regarding the terms of the transaction, which according to the FY

2017 annual report, remain confidential and undisclosed (Arens, Elder and Beasley 2013, pp.

45). There is more that needs to be disclosed with regard to this acquisition since it is considered

a key matter that may impact the financial decision made by intended users of the financial

statement of the company.

Questions for Follow-Up during the Annual General Meeting of the Company

According to the auditor’s report, it has been stated that there are no material subsequent

events which have arisen in the time interval between June 3,, 2017 and June 30, 2017 (Beach

Energy Ltd 2017, pp. 119).

Assessment of the Effectiveness of Material Information Reported by the Auditor

According to the report of the independent auditor regarding the financial audit of Beach

energy Ltd, the auditor has considered almost all material information which is considered

significant for use by external users of financial reports of the company. He has performed all

necessary procedures for ascertaining that the financial statements are free from any material

misstatement and that they are truly and fairly reflective of the financial position and financial

performance of the company (Carson 2009, pp. 78).

Material Information Which Could Be Under-Reported or Missing

Although the independent auditor has given an unqualified opinion in the report of his

audit, there are a few areas which have been under-reported. For instance, regarding business

combinations, full details have not been adequately explained in the financial reports. The

acquisition of 100% interests in the shares of Territory Oil and Gas by Beach Energy Ltd has not

been explained adequately regarding the terms of the transaction, which according to the FY

2017 annual report, remain confidential and undisclosed (Arens, Elder and Beasley 2013, pp.

45). There is more that needs to be disclosed with regard to this acquisition since it is considered

a key matter that may impact the financial decision made by intended users of the financial

statement of the company.

Questions for Follow-Up during the Annual General Meeting of the Company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.