HA3032 - Auditing TPG Telecom: Risk, Procedure & Analysis

VerifiedAdded on 2023/06/04

|20

|4469

|147

Report

AI Summary

This report provides an in-depth analysis of the auditing process at TPG Telecom Limited, an Australian telecommunications company. It begins by outlining the importance of auditing in identifying financial statement issues and ensuring operational effectiveness. Key business risks, including development, regulatory, competition, and cyber-attack risks, are identified and their significance in the audit process is emphasized. The application of the audit risk model, including control risk, inherent risk, and detection risk, is discussed, along with analytical procedures using financial ratios like return on assets and equity. The report also details audit procedures using a substantive approach for material account balances and concludes with a proposed sampling plan for completing the audit. Desklib offers a wide range of solved assignments and past papers for students.

Auditing 1

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 2

Executive summary

The term is auditing is considered as an essential function that is carried out by the organizations

to identify the issues in financial statements and operational activities to ensure the functioning,

effectiveness and efficiency of the operational activities. Audit can be conducted in two forms

namely internal audit and external audit. The internal audit is carried out by the management and

external audit is carried out by appointing eternal party to analyze the financial operational

performance of the organization. In this report, TPG telecom limited is used to understand the

audit process and its role in analyzing the organizational performance. During the audit

procedure, it is analyzed that there are several business risks both in internal and external

environment that can influence the financial performance of an organization. It is essential for

the auditor to identify these risks and suggest an appropriate way to overcome these risks for

better performance. In addition, the auditors must follow a systematic audit procedure with

analyzing entire material accounts to identify the errors and fraud in the financial records. In this

concern, the auditors are recommended to have proper focus both on internal and external factors

that are influencing to business operations to attain the objectives of audit in professional

manner.

Executive summary

The term is auditing is considered as an essential function that is carried out by the organizations

to identify the issues in financial statements and operational activities to ensure the functioning,

effectiveness and efficiency of the operational activities. Audit can be conducted in two forms

namely internal audit and external audit. The internal audit is carried out by the management and

external audit is carried out by appointing eternal party to analyze the financial operational

performance of the organization. In this report, TPG telecom limited is used to understand the

audit process and its role in analyzing the organizational performance. During the audit

procedure, it is analyzed that there are several business risks both in internal and external

environment that can influence the financial performance of an organization. It is essential for

the auditor to identify these risks and suggest an appropriate way to overcome these risks for

better performance. In addition, the auditors must follow a systematic audit procedure with

analyzing entire material accounts to identify the errors and fraud in the financial records. In this

concern, the auditors are recommended to have proper focus both on internal and external factors

that are influencing to business operations to attain the objectives of audit in professional

manner.

Auditing 3

Table of Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

About TPG telecom limited.........................................................................................................................5

Key business risks for TPG telecom limited................................................................................................5

Application of Audit Risk Model................................................................................................................7

Analytical procedure...................................................................................................................................9

Different material account balances of TPG telecom limited....................................................................12

Audit procedure using substantive approach.............................................................................................13

Sampling plan............................................................................................................................................16

Conclusion.................................................................................................................................................18

References.................................................................................................................................................19

Table of Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

About TPG telecom limited.........................................................................................................................5

Key business risks for TPG telecom limited................................................................................................5

Application of Audit Risk Model................................................................................................................7

Analytical procedure...................................................................................................................................9

Different material account balances of TPG telecom limited....................................................................12

Audit procedure using substantive approach.............................................................................................13

Sampling plan............................................................................................................................................16

Conclusion.................................................................................................................................................18

References.................................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 4

Introduction

Auditing is an essential process for the organizations to analyze the financial performance and

effective business decisions. The successful organizations are using auditing as an exclusive

process of identifying the issues and misstatement in the financial records. The aim of this report

is to outline the role of auditing in an organization. In this concern, the report is describing

different audit steps and key business risks for an organization. TPG telecom limited is

considering to make understanding the about the concept of auditing in practical manner. TPG

telecom limited is a listed in ASX and forcing the telecommunication industry of Australia. In

addition, the report is also determining substantial tests of balances of different assets and

liabilities of the company with use of substantive approach of auditing. The report is also

analyzing the materiality items and carrying out the analytical procedures of TPG telecom

limited with considering different ratios and metrics. Auditing process is also plays and essential

role in attaining the outcomes of auditing in professional manner so that the report is also

discussing auditing process for TPG telecom limited in effective manner. Finally, the report is

describing a sampling plan to complete the audit process in successful manner.

Introduction

Auditing is an essential process for the organizations to analyze the financial performance and

effective business decisions. The successful organizations are using auditing as an exclusive

process of identifying the issues and misstatement in the financial records. The aim of this report

is to outline the role of auditing in an organization. In this concern, the report is describing

different audit steps and key business risks for an organization. TPG telecom limited is

considering to make understanding the about the concept of auditing in practical manner. TPG

telecom limited is a listed in ASX and forcing the telecommunication industry of Australia. In

addition, the report is also determining substantial tests of balances of different assets and

liabilities of the company with use of substantive approach of auditing. The report is also

analyzing the materiality items and carrying out the analytical procedures of TPG telecom

limited with considering different ratios and metrics. Auditing process is also plays and essential

role in attaining the outcomes of auditing in professional manner so that the report is also

discussing auditing process for TPG telecom limited in effective manner. Finally, the report is

describing a sampling plan to complete the audit process in successful manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 5

About TPG telecom limited

In Australian telecommunication industry, TPG is a well known company. The company is

providing communication services in the country. TPG (Total Peripherals Group) was found in

1986 with a reserve conquest of SP Telemedia Limited by TPG. The products, services, people,

innovation and network assets enabled the company to provide reliable, cost effective and fast

telecommunication services. The company provides a wide range of communication products

and services to government, residential users, enterprises and wholesale consumers (TPG, 2018).

The company provides countrywide NBN, ADSL2+, Ethernet broadband, Fiber Optics, IPTV,

telephony services and different business network solutions. TPG has its own network

infrastructure in the country.

Key business risks for TPG telecom limited

In an organization, the business risks are considered as factors that can influence to the ability of

the organization to attain the goals and objectives in desired manner. From last decade,

unexpected changes have been seen in political, economic and business environment, which are

influencing the communication organizations in different ways. These risks may be cause of

business failure if not managed on time (Smith, 2018). In this concern, it is essential for the

management to identify these business risks and take immediate actions to overcome them in

professional manner. The key business risks for TPG telecom limited are discussed as below:

Development risks:

About TPG telecom limited

In Australian telecommunication industry, TPG is a well known company. The company is

providing communication services in the country. TPG (Total Peripherals Group) was found in

1986 with a reserve conquest of SP Telemedia Limited by TPG. The products, services, people,

innovation and network assets enabled the company to provide reliable, cost effective and fast

telecommunication services. The company provides a wide range of communication products

and services to government, residential users, enterprises and wholesale consumers (TPG, 2018).

The company provides countrywide NBN, ADSL2+, Ethernet broadband, Fiber Optics, IPTV,

telephony services and different business network solutions. TPG has its own network

infrastructure in the country.

Key business risks for TPG telecom limited

In an organization, the business risks are considered as factors that can influence to the ability of

the organization to attain the goals and objectives in desired manner. From last decade,

unexpected changes have been seen in political, economic and business environment, which are

influencing the communication organizations in different ways. These risks may be cause of

business failure if not managed on time (Smith, 2018). In this concern, it is essential for the

management to identify these business risks and take immediate actions to overcome them in

professional manner. The key business risks for TPG telecom limited are discussed as below:

Development risks:

Auditing 6

The changing political and economic environment is generating the issues in the developing the

telecommunication operations across the world. In the changing circumstances and unpredictable

environment, the organizations cannot make proper planning for further development. As well

as, the management can also face the financial risks in developing its business operations in the

fluctuated economic environment (Sohal, 2013). In this concern, it is analyzed that there are

several development risks for TPG telecom limited that can hamper its development activities in

big manner.

Risks related to regulatory burden:

Over last year the telecommunication organizations are facing the issue of regulatory burden in

big manner. The government is changing the regulatory rules and regulations and making stricter

for the telecommunication to follow these rules and regulations. The instability in political and

economical in certain global markets increased the regulatory burden for the company in

operating the telecommunication services in the country (BDO, 2017). Thus, there are several

regulatory risks for TPG telecom limited that can generate business risks and hinder the

operational activities in big manner.

Risk of competition:

There are different global telecommunication organizations that are increasing their business

operations across the world and providing competitive services to attract the customers. It is a

big risk for TPG telecom limited as Australia is a better place for the telecommunication

companies to expand their business in effective manner (Smith, 2018). In this concern, TPG is

also facing the risk of high competition in Australia.

Risk of cyber attack:

The changing political and economic environment is generating the issues in the developing the

telecommunication operations across the world. In the changing circumstances and unpredictable

environment, the organizations cannot make proper planning for further development. As well

as, the management can also face the financial risks in developing its business operations in the

fluctuated economic environment (Sohal, 2013). In this concern, it is analyzed that there are

several development risks for TPG telecom limited that can hamper its development activities in

big manner.

Risks related to regulatory burden:

Over last year the telecommunication organizations are facing the issue of regulatory burden in

big manner. The government is changing the regulatory rules and regulations and making stricter

for the telecommunication to follow these rules and regulations. The instability in political and

economical in certain global markets increased the regulatory burden for the company in

operating the telecommunication services in the country (BDO, 2017). Thus, there are several

regulatory risks for TPG telecom limited that can generate business risks and hinder the

operational activities in big manner.

Risk of competition:

There are different global telecommunication organizations that are increasing their business

operations across the world and providing competitive services to attract the customers. It is a

big risk for TPG telecom limited as Australia is a better place for the telecommunication

companies to expand their business in effective manner (Smith, 2018). In this concern, TPG is

also facing the risk of high competition in Australia.

Risk of cyber attack:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 7

It is analyzed that the technology is continuously increasing and generating different cyber attack

risks for the telecommunication services. There are several hackers that can steal authentic

information, financial data and customer data of the telecommunication (BDO, 2017). Therefore,

TPG telecom limited may also face the risk of cyber attack.

Importance of identifying the business risks in audit process:

The International Accounting Standard (ISA) 315 determines that the auditors have need to gain

proper understanding about the internal and external environment that are influencing to

operational activities to complete the audit process in effective manner. The auditors can identify

misstatement in the financial records in better manner through analyzing the possible business

risks. In this concern, the determination of business risks has importance for TPG to make

successful the audit procedure.

Application of Audit Risk Model

In audit process, the audit risk model is used to determine overall risks associated to audit and

explain that how these risks can be managed. In other words, audit model is a process of

identifying total risks associated to audit. As per this model, the audit risk contains three

components that are used to calculate the audit risk (Botez, 2015). These components are

inherent risk, control risk and detection risk.

Audit risk = Control risk * Inherent risk * Detection risk

Control risk: In financial statements, the control risk is considered as a risk in material

misstatement, which arises due to failure or nonappearance in operation of significant control of

the individual. It is essential for an organization to have enough internal control to avert

It is analyzed that the technology is continuously increasing and generating different cyber attack

risks for the telecommunication services. There are several hackers that can steal authentic

information, financial data and customer data of the telecommunication (BDO, 2017). Therefore,

TPG telecom limited may also face the risk of cyber attack.

Importance of identifying the business risks in audit process:

The International Accounting Standard (ISA) 315 determines that the auditors have need to gain

proper understanding about the internal and external environment that are influencing to

operational activities to complete the audit process in effective manner. The auditors can identify

misstatement in the financial records in better manner through analyzing the possible business

risks. In this concern, the determination of business risks has importance for TPG to make

successful the audit procedure.

Application of Audit Risk Model

In audit process, the audit risk model is used to determine overall risks associated to audit and

explain that how these risks can be managed. In other words, audit model is a process of

identifying total risks associated to audit. As per this model, the audit risk contains three

components that are used to calculate the audit risk (Botez, 2015). These components are

inherent risk, control risk and detection risk.

Audit risk = Control risk * Inherent risk * Detection risk

Control risk: In financial statements, the control risk is considered as a risk in material

misstatement, which arises due to failure or nonappearance in operation of significant control of

the individual. It is essential for an organization to have enough internal control to avert

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 8

occurrence of error and fraud in the financial records (Contessotto and Moroney, 2014). For

instance, if an organization has not experienced accounting staff, than there may be probability

of misstatement. The inexperienced employees cannot prevent or detect the misstatements from

the financial records. The unskilled staff thinks that they can eliminate the potential

misstatements, which is not possible in critical transactions. I

Inherent risk: In financial statements, the inherent risks generate due to omission or error in

financial records. The inherent risks will be higher highly complex financial transactions. For

instance, a recently formed financial institution which contains significant exposures and trades

in multifaceted derivative mechanism may be measured highly critical as compared to audit of

manufacturing organizations in a stable environment.

Detection risk: The auditors use audit risk model to manage entire risks that are engaged with

audit. The auditors continue by inspecting the control and inherent risks related to audit

engagement while understanding the environment of an entity. Detection risk indicates to

inability of an auditor of identifying the errors in the financial statements that are not still

detained by the internal control.

If, the inherent risk is .80, control risk is .60 and audit risk is .05 that the detection risk will be

calculated as below:

Audit risk = Control risk * Inherent risk * Detection risk

.05 = .60 * .80 * Detection risk

Detection risk = 0.5/ (.60*.80)

Detection risk = 0.10

occurrence of error and fraud in the financial records (Contessotto and Moroney, 2014). For

instance, if an organization has not experienced accounting staff, than there may be probability

of misstatement. The inexperienced employees cannot prevent or detect the misstatements from

the financial records. The unskilled staff thinks that they can eliminate the potential

misstatements, which is not possible in critical transactions. I

Inherent risk: In financial statements, the inherent risks generate due to omission or error in

financial records. The inherent risks will be higher highly complex financial transactions. For

instance, a recently formed financial institution which contains significant exposures and trades

in multifaceted derivative mechanism may be measured highly critical as compared to audit of

manufacturing organizations in a stable environment.

Detection risk: The auditors use audit risk model to manage entire risks that are engaged with

audit. The auditors continue by inspecting the control and inherent risks related to audit

engagement while understanding the environment of an entity. Detection risk indicates to

inability of an auditor of identifying the errors in the financial statements that are not still

detained by the internal control.

If, the inherent risk is .80, control risk is .60 and audit risk is .05 that the detection risk will be

calculated as below:

Audit risk = Control risk * Inherent risk * Detection risk

.05 = .60 * .80 * Detection risk

Detection risk = 0.5/ (.60*.80)

Detection risk = 0.10

Auditing 9

Analysis: After the calculation of audit risk model with considering the inherent risk and control

risks, the obtained value of detection risk is 0.10. The equation is determining that detection risk

in audit is at minimum level while the inherent risk at maximum level and control risk is at

medium level for TPG telecom limited. Higher rate of inherent risk in determining that the

accounting transactions might be exposed both by internal and external environmental factors.

The external factors are economic, legal and political factors. The changes in these factors have

influenced on the operational activities of the organization. As well as, the areas of deception are

as below which are arisen due to weak control on internal activities of the organization:

Payroll fraud

Third party fraud

Cash & other valuable assets

Banking transactions

In this concern, it is essential for the auditor to review these risks while carrying out the audit

process. The analysis of these risks identifies the areas which are influencing the financial and

operational activities of the organization. Auditors require an appropriate policy and approach to

analyze the impact of errors and fraud on financial statements of the organization. Thus, the

analysis of different audit risks is essential for the auditors to accomplish the audit process in

more professional and reliable manner.

Analytical procedure

According the International Accounting Standards, it is required for the auditors to perform an

analytical procedure while auditing. The analytical procedure will be helpful in analyzing the

financial performance of the associated organization in professional manner (Jans et al., 2014). In

Analysis: After the calculation of audit risk model with considering the inherent risk and control

risks, the obtained value of detection risk is 0.10. The equation is determining that detection risk

in audit is at minimum level while the inherent risk at maximum level and control risk is at

medium level for TPG telecom limited. Higher rate of inherent risk in determining that the

accounting transactions might be exposed both by internal and external environmental factors.

The external factors are economic, legal and political factors. The changes in these factors have

influenced on the operational activities of the organization. As well as, the areas of deception are

as below which are arisen due to weak control on internal activities of the organization:

Payroll fraud

Third party fraud

Cash & other valuable assets

Banking transactions

In this concern, it is essential for the auditor to review these risks while carrying out the audit

process. The analysis of these risks identifies the areas which are influencing the financial and

operational activities of the organization. Auditors require an appropriate policy and approach to

analyze the impact of errors and fraud on financial statements of the organization. Thus, the

analysis of different audit risks is essential for the auditors to accomplish the audit process in

more professional and reliable manner.

Analytical procedure

According the International Accounting Standards, it is required for the auditors to perform an

analytical procedure while auditing. The analytical procedure will be helpful in analyzing the

financial performance of the associated organization in professional manner (Jans et al., 2014). In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 10

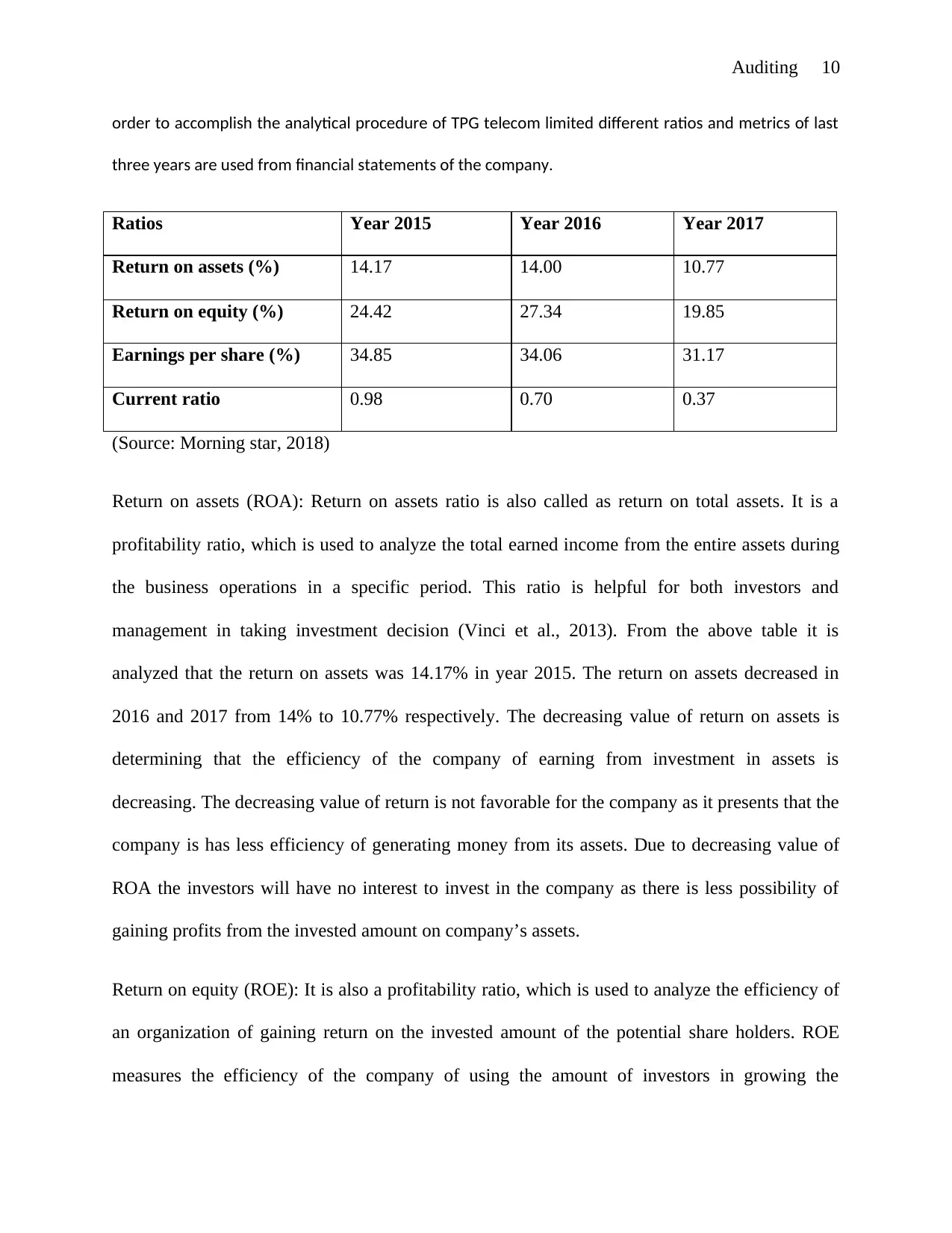

order to accomplish the analytical procedure of TPG telecom limited different ratios and metrics of last

three years are used from financial statements of the company.

Ratios Year 2015 Year 2016 Year 2017

Return on assets (%) 14.17 14.00 10.77

Return on equity (%) 24.42 27.34 19.85

Earnings per share (%) 34.85 34.06 31.17

Current ratio 0.98 0.70 0.37

(Source: Morning star, 2018)

Return on assets (ROA): Return on assets ratio is also called as return on total assets. It is a

profitability ratio, which is used to analyze the total earned income from the entire assets during

the business operations in a specific period. This ratio is helpful for both investors and

management in taking investment decision (Vinci et al., 2013). From the above table it is

analyzed that the return on assets was 14.17% in year 2015. The return on assets decreased in

2016 and 2017 from 14% to 10.77% respectively. The decreasing value of return on assets is

determining that the efficiency of the company of earning from investment in assets is

decreasing. The decreasing value of return is not favorable for the company as it presents that the

company is has less efficiency of generating money from its assets. Due to decreasing value of

ROA the investors will have no interest to invest in the company as there is less possibility of

gaining profits from the invested amount on company’s assets.

Return on equity (ROE): It is also a profitability ratio, which is used to analyze the efficiency of

an organization of gaining return on the invested amount of the potential share holders. ROE

measures the efficiency of the company of using the amount of investors in growing the

order to accomplish the analytical procedure of TPG telecom limited different ratios and metrics of last

three years are used from financial statements of the company.

Ratios Year 2015 Year 2016 Year 2017

Return on assets (%) 14.17 14.00 10.77

Return on equity (%) 24.42 27.34 19.85

Earnings per share (%) 34.85 34.06 31.17

Current ratio 0.98 0.70 0.37

(Source: Morning star, 2018)

Return on assets (ROA): Return on assets ratio is also called as return on total assets. It is a

profitability ratio, which is used to analyze the total earned income from the entire assets during

the business operations in a specific period. This ratio is helpful for both investors and

management in taking investment decision (Vinci et al., 2013). From the above table it is

analyzed that the return on assets was 14.17% in year 2015. The return on assets decreased in

2016 and 2017 from 14% to 10.77% respectively. The decreasing value of return on assets is

determining that the efficiency of the company of earning from investment in assets is

decreasing. The decreasing value of return is not favorable for the company as it presents that the

company is has less efficiency of generating money from its assets. Due to decreasing value of

ROA the investors will have no interest to invest in the company as there is less possibility of

gaining profits from the invested amount on company’s assets.

Return on equity (ROE): It is also a profitability ratio, which is used to analyze the efficiency of

an organization of gaining return on the invested amount of the potential share holders. ROE

measures the efficiency of the company of using the amount of investors in growing the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 11

company (Al Karim and Alam, 2013). The investors have intention to gain high return on their

investment from the company. Return on equity of TPG was 24.42 in 2015, 27.34 in 2016 and

19.85 in 2017. There is not stability on in return on equity of the company. In this concern, there

may be confusion among the investors to invest in the company as they have intention to gain

constant return on their investment.

Earnings per share (EPS): EPS is also known as net income on per share. Higher earnings per

share remain better for the company to attract the investors and improve the market image of the

company. As well as, higher EPS determined that the company has good profits to issue its

shareholders on outstanding shares (Omar et al., 2014). The EPS of TPG was 34.58 in 2015,

34.06 in 2016 and 31.17 in 2017. The decreasing EPS of the company is indicating that the

company has lower profits to distribute its share holders, which is not good for the company.

Due to the decreasing EPS the investors will have less intention to invest in equity of the

company.

Current ratio: The term current ratio is used to analyze the capability of an organization of using

its current to pay current liabilities. Current ratio is helpful for the creditors and investors to

analyze the liquidity position of an organization and the ability of paying current liabilities with

use of current assets. Higher current ratio remains favorable for the company as it indicates that

the organization has good ability to pay its short-term liabilities or current debts. The current

ration of TPG telecom limited was 0.98, 0.70 and 0.37 in 2015, 2016 and 2017 respectively. The

decreasing current ratio is determining that the company has lower ability of paying debts from

its current assets, which is not favorable for the company.

company (Al Karim and Alam, 2013). The investors have intention to gain high return on their

investment from the company. Return on equity of TPG was 24.42 in 2015, 27.34 in 2016 and

19.85 in 2017. There is not stability on in return on equity of the company. In this concern, there

may be confusion among the investors to invest in the company as they have intention to gain

constant return on their investment.

Earnings per share (EPS): EPS is also known as net income on per share. Higher earnings per

share remain better for the company to attract the investors and improve the market image of the

company. As well as, higher EPS determined that the company has good profits to issue its

shareholders on outstanding shares (Omar et al., 2014). The EPS of TPG was 34.58 in 2015,

34.06 in 2016 and 31.17 in 2017. The decreasing EPS of the company is indicating that the

company has lower profits to distribute its share holders, which is not good for the company.

Due to the decreasing EPS the investors will have less intention to invest in equity of the

company.

Current ratio: The term current ratio is used to analyze the capability of an organization of using

its current to pay current liabilities. Current ratio is helpful for the creditors and investors to

analyze the liquidity position of an organization and the ability of paying current liabilities with

use of current assets. Higher current ratio remains favorable for the company as it indicates that

the organization has good ability to pay its short-term liabilities or current debts. The current

ration of TPG telecom limited was 0.98, 0.70 and 0.37 in 2015, 2016 and 2017 respectively. The

decreasing current ratio is determining that the company has lower ability of paying debts from

its current assets, which is not favorable for the company.

Auditing 12

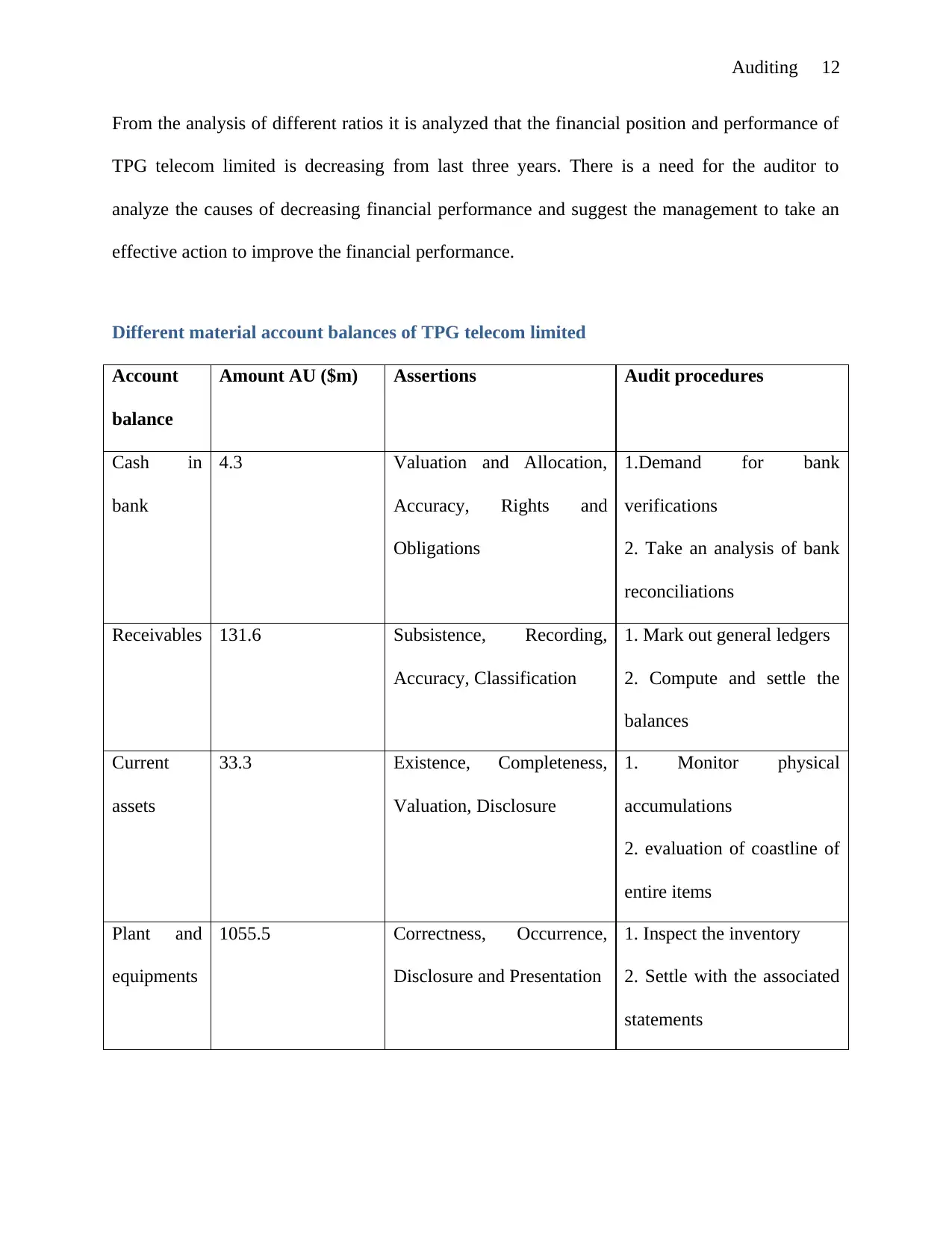

From the analysis of different ratios it is analyzed that the financial position and performance of

TPG telecom limited is decreasing from last three years. There is a need for the auditor to

analyze the causes of decreasing financial performance and suggest the management to take an

effective action to improve the financial performance.

Different material account balances of TPG telecom limited

Account

balance

Amount AU ($m) Assertions Audit procedures

Cash in

bank

4.3 Valuation and Allocation,

Accuracy, Rights and

Obligations

1.Demand for bank

verifications

2. Take an analysis of bank

reconciliations

Receivables 131.6 Subsistence, Recording,

Accuracy, Classification

1. Mark out general ledgers

2. Compute and settle the

balances

Current

assets

33.3 Existence, Completeness,

Valuation, Disclosure

1. Monitor physical

accumulations

2. evaluation of coastline of

entire items

Plant and

equipments

1055.5 Correctness, Occurrence,

Disclosure and Presentation

1. Inspect the inventory

2. Settle with the associated

statements

From the analysis of different ratios it is analyzed that the financial position and performance of

TPG telecom limited is decreasing from last three years. There is a need for the auditor to

analyze the causes of decreasing financial performance and suggest the management to take an

effective action to improve the financial performance.

Different material account balances of TPG telecom limited

Account

balance

Amount AU ($m) Assertions Audit procedures

Cash in

bank

4.3 Valuation and Allocation,

Accuracy, Rights and

Obligations

1.Demand for bank

verifications

2. Take an analysis of bank

reconciliations

Receivables 131.6 Subsistence, Recording,

Accuracy, Classification

1. Mark out general ledgers

2. Compute and settle the

balances

Current

assets

33.3 Existence, Completeness,

Valuation, Disclosure

1. Monitor physical

accumulations

2. evaluation of coastline of

entire items

Plant and

equipments

1055.5 Correctness, Occurrence,

Disclosure and Presentation

1. Inspect the inventory

2. Settle with the associated

statements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.