Auditing and Assurance Services Report: Deficiencies Analysis

VerifiedAdded on 2019/11/12

|6

|996

|434

Report

AI Summary

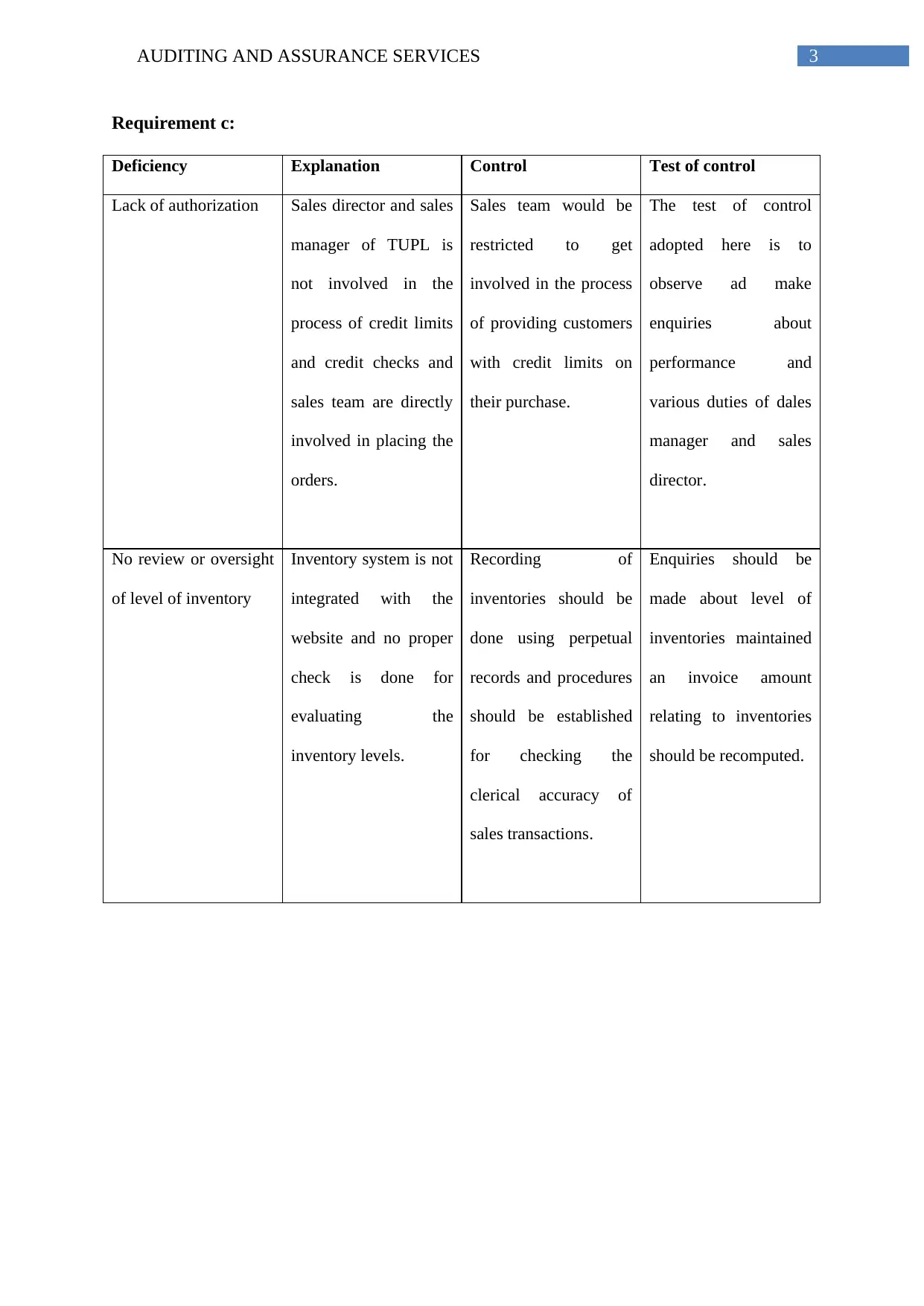

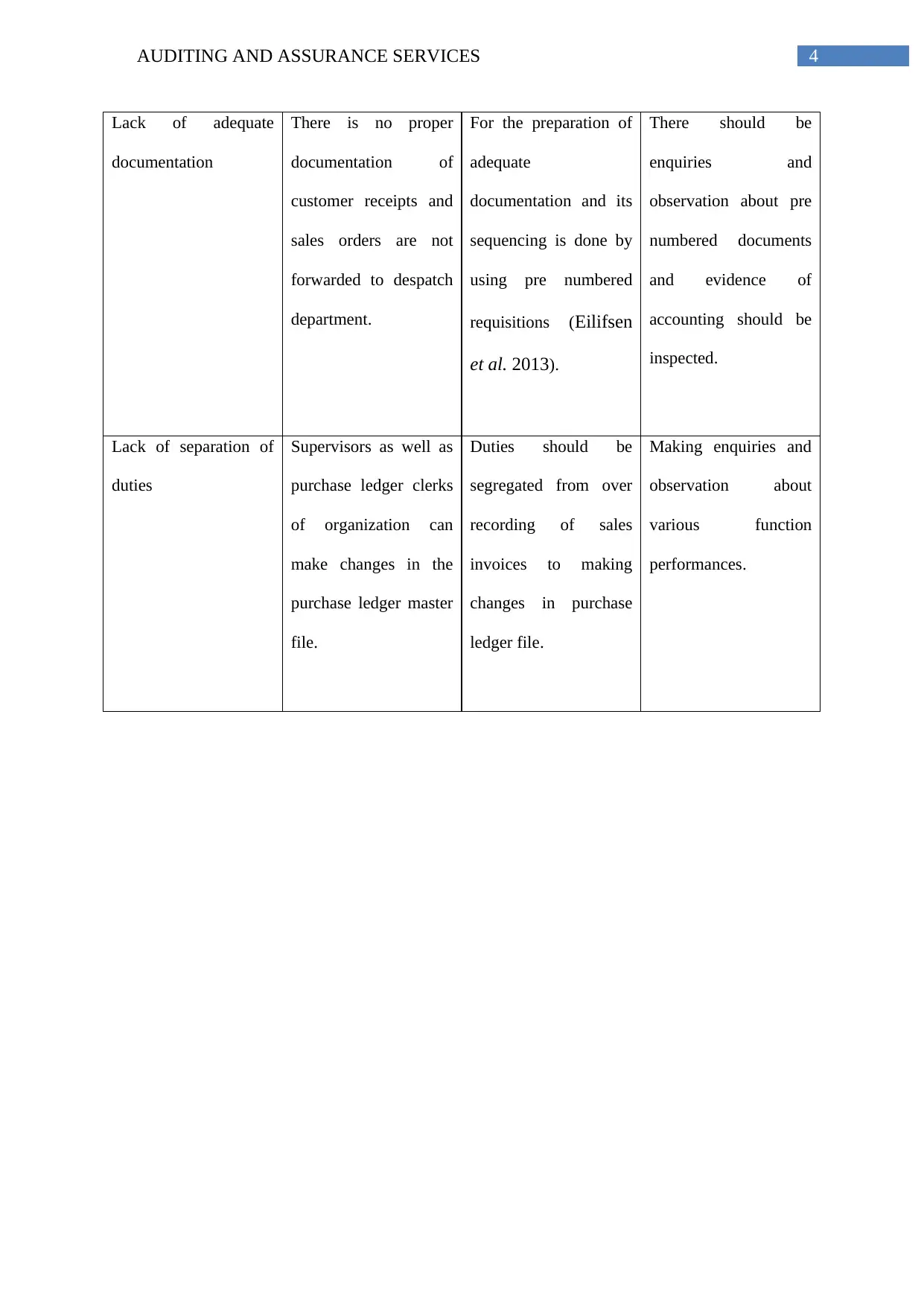

This report provides an analysis of auditing and assurance services, specifically focusing on the internal control deficiencies identified within Toy Universe Pty Limited (TUPL). The report highlights five key deficiencies: lack of adequate documentation, lack of authorization, lack of separation of duties, inadequate control over the safeguarding of assets, and no review or oversight of inventory levels. Each deficiency is explained in detail, outlining its potential impact on the reliability of financial statements. The report also proposes control tests and actions that can be implemented to mitigate the risks associated with each deficiency. The discussion covers the segregation of duties, authorization protocols, inventory management, and documentation procedures. The analysis is supported by references to relevant auditing and assurance services literature.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.