ACCT20075: Auditing and Ethics Report - Company Analysis and Review

VerifiedAdded on 2023/06/08

|15

|2949

|483

Report

AI Summary

This report provides a comprehensive analysis of the auditing procedures applied to Woodside Petroleum Limited (WPL). It begins by examining materiality determination, considering both qualitative and quantitative aspects, and calculating planning materiality based on WPL's 2017 financial data. The report then reviews draft notes and disclosures, highlighting significant items like leases, contingent liabilities, and dividends. A detailed financial statement analytical review follows, assessing liquidity, profitability, asset management, leverage, and valuation ratios from 2014 to 2017. The analysis includes an examination of cash flow, focusing on operating, investing activities, and non-cash transactions. Finally, the report assesses going concern risk, considering WPL's financial performance and potential impact on its ability to continue as a viable business. The report concludes with a review of the auditor's report.

Running head: AUDITING AND ETHICS

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Auditing and Ethics

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality Determination and Audit Scope................................................................................2

Draft Notes and Disclosure Review............................................................................................4

Section 2..........................................................................................................................................5

Financial Statement Analytical Review.......................................................................................5

Section 3..........................................................................................................................................9

Review of Cash Flow...................................................................................................................9

Going Concern Risk Assessment...............................................................................................10

Review of Auditor’s Report.......................................................................................................10

References......................................................................................................................................12

Table of Contents

Section 1..........................................................................................................................................2

Materiality Determination and Audit Scope................................................................................2

Draft Notes and Disclosure Review............................................................................................4

Section 2..........................................................................................................................................5

Financial Statement Analytical Review.......................................................................................5

Section 3..........................................................................................................................................9

Review of Cash Flow...................................................................................................................9

Going Concern Risk Assessment...............................................................................................10

Review of Auditor’s Report.......................................................................................................10

References......................................................................................................................................12

2AUDITING AND ETHICS

Section 1

Materiality Determination and Audit Scope

The main aim of this assignment is to gain understanding about the audit procedures of

Woodside Petroleum Limited (WPL) in order to review the materiality that the auditors are

needed to consider in the detection of material misstatements in the financial reports. Materiality

is a crucial concept for audit scope and helps the auditors in considering the fact that which

misstatements are major and which misstatements are minor as they can have significant effects

on the company financials (Legoria, Melendrez & Reynolds, 2013). The auditors judge the

significant missstements based on the level of materiality and the process as well as level of

impact of these aspects on the decision-making process of the investors and others users of the

financial reports. WPL is one of the leading energy companies having operation in the Australian

regions (Woodside.com.au, 2018).

Materiality is a major fundamental concept of auditing as it is needed for the auditors to

take into account the material aspects and whether the managements of the companies have

correctly reported them or not. In order to set the materiality level of business, the auditors are

needed to apply their materiality judgment. The auditors of the companies consider both the

qualitative and quantitative characteristics as the basis for determining materiality (Christensen,

Glover & Wood, 2013). Under the qualitative dimension of materiality, the auditors consider the

factor like business inventory, net profit, changes in the accounting methods along with major

accounting policies. Under the dimension of quantitative aspect of materiality, the auditors take

into consideration the estimated percentage that needs to be charged at appropriate basis for the

determination of level of materiality for financial items of the annual reports of the companies. It

Section 1

Materiality Determination and Audit Scope

The main aim of this assignment is to gain understanding about the audit procedures of

Woodside Petroleum Limited (WPL) in order to review the materiality that the auditors are

needed to consider in the detection of material misstatements in the financial reports. Materiality

is a crucial concept for audit scope and helps the auditors in considering the fact that which

misstatements are major and which misstatements are minor as they can have significant effects

on the company financials (Legoria, Melendrez & Reynolds, 2013). The auditors judge the

significant missstements based on the level of materiality and the process as well as level of

impact of these aspects on the decision-making process of the investors and others users of the

financial reports. WPL is one of the leading energy companies having operation in the Australian

regions (Woodside.com.au, 2018).

Materiality is a major fundamental concept of auditing as it is needed for the auditors to

take into account the material aspects and whether the managements of the companies have

correctly reported them or not. In order to set the materiality level of business, the auditors are

needed to apply their materiality judgment. The auditors of the companies consider both the

qualitative and quantitative characteristics as the basis for determining materiality (Christensen,

Glover & Wood, 2013). Under the qualitative dimension of materiality, the auditors consider the

factor like business inventory, net profit, changes in the accounting methods along with major

accounting policies. Under the dimension of quantitative aspect of materiality, the auditors take

into consideration the estimated percentage that needs to be charged at appropriate basis for the

determination of level of materiality for financial items of the annual reports of the companies. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICS

depends on the judgment of the auditors to consider the percentage that needs to be charged for

the determination of materiality level; and the auditors are needed to consider the size as well as

nature of the business organizations. In the initial stage of audit planning, the auditors consider

the computation of materiality; after that, the auditors consider the computation of materiality of

different financial items after the materiality determination in the initial stage (Eilifsen &

Messier Jr, 2014). Thus, the above discussion indicates towards the importance of materiality

computation in the auditing process.

Under the estimation of materiality in quantitative basis, the auditors need to consider

different materiality base for the planning of materiality and the materiality of business

performance. At the time to consider different bases for materiality, the auditors are needed to

take into consideration significant items from the Profit or Loss statement as well as balance

sheet of the entities (Ruhnke & Schmidt, 2014). According to the Profit or Loss statement, the

considered bases for materiality determination are net profit before tax, total revenue and total

sales or revenue. In the balance sheet, the considered base for materiality is total assets of the

businesses (Ruhnke, Pronobis & Michel, 2014).

The 2017 Annual Report of WPL is taken into consideration in order to estimate the

materiality level of the business for the year of 2017. It can be seen from the 2017 Annual Report

of WPL that there has been major drop in the operating revenue of the company. At the time of

the determination of the level of materiality, the common practice is to consider the highest value

as the base for the determination of materiality (Edgley, 2014). In case of WPL, the total asset of

the company is considered as the base of materiality determination and the value of total asset in

2017 Consolidated Statement of Financial Position is $25,401 million (Woodside.com.au, 2018).

depends on the judgment of the auditors to consider the percentage that needs to be charged for

the determination of materiality level; and the auditors are needed to consider the size as well as

nature of the business organizations. In the initial stage of audit planning, the auditors consider

the computation of materiality; after that, the auditors consider the computation of materiality of

different financial items after the materiality determination in the initial stage (Eilifsen &

Messier Jr, 2014). Thus, the above discussion indicates towards the importance of materiality

computation in the auditing process.

Under the estimation of materiality in quantitative basis, the auditors need to consider

different materiality base for the planning of materiality and the materiality of business

performance. At the time to consider different bases for materiality, the auditors are needed to

take into consideration significant items from the Profit or Loss statement as well as balance

sheet of the entities (Ruhnke & Schmidt, 2014). According to the Profit or Loss statement, the

considered bases for materiality determination are net profit before tax, total revenue and total

sales or revenue. In the balance sheet, the considered base for materiality is total assets of the

businesses (Ruhnke, Pronobis & Michel, 2014).

The 2017 Annual Report of WPL is taken into consideration in order to estimate the

materiality level of the business for the year of 2017. It can be seen from the 2017 Annual Report

of WPL that there has been major drop in the operating revenue of the company. At the time of

the determination of the level of materiality, the common practice is to consider the highest value

as the base for the determination of materiality (Edgley, 2014). In case of WPL, the total asset of

the company is considered as the base of materiality determination and the value of total asset in

2017 Consolidated Statement of Financial Position is $25,401 million (Woodside.com.au, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICS

After that, 5% is considered as he percentage that needs to be charged for the purpose of

materiality determination. The computation can be seen in below:

Planning Materiality = 5% of the Total Assets

= 5% of $25,401 million = $ 1,270.05 million

Draft Notes and Disclosure Review

The draft notes and the disclosures in the 2017 Annual Report of WPL have major

importance in the audit procedures of the company as it includes certain accounting treatments

along with explanations of some crucial aspects of the financial statements. The following are

some significant items in the drafts that can have impact on the audit process of WPL:

Leases: It can be seen from the notes of leases that the company has segregated their leases

between finance leases and operating leases as per the regulation of AASB 117 Leases.

However, from the year 2018, the companies are needed to comply with the new lease standers

AASB 16 Leases that will eliminate the segregation of leases as operating and finance leases.

For this reason, the auditors can check lease balances of WPL for finding any manipulation

(Woodside.com.au, 2018).

Contingent Liabilities: Contingent liability is a part of the financial activities of WPL that is

full of uncertainty; and there is not any accounting base for the determination of the contingent

liabilities. 2017 Annual Report of WPL states that US$66 million is the amount of contingent

liabilities of WPL in 2017. Due to uncertainty, the auditors can look into this matter to get the

confirmation (Woodside.com.au, 2018).

After that, 5% is considered as he percentage that needs to be charged for the purpose of

materiality determination. The computation can be seen in below:

Planning Materiality = 5% of the Total Assets

= 5% of $25,401 million = $ 1,270.05 million

Draft Notes and Disclosure Review

The draft notes and the disclosures in the 2017 Annual Report of WPL have major

importance in the audit procedures of the company as it includes certain accounting treatments

along with explanations of some crucial aspects of the financial statements. The following are

some significant items in the drafts that can have impact on the audit process of WPL:

Leases: It can be seen from the notes of leases that the company has segregated their leases

between finance leases and operating leases as per the regulation of AASB 117 Leases.

However, from the year 2018, the companies are needed to comply with the new lease standers

AASB 16 Leases that will eliminate the segregation of leases as operating and finance leases.

For this reason, the auditors can check lease balances of WPL for finding any manipulation

(Woodside.com.au, 2018).

Contingent Liabilities: Contingent liability is a part of the financial activities of WPL that is

full of uncertainty; and there is not any accounting base for the determination of the contingent

liabilities. 2017 Annual Report of WPL states that US$66 million is the amount of contingent

liabilities of WPL in 2017. Due to uncertainty, the auditors can look into this matter to get the

confirmation (Woodside.com.au, 2018).

5AUDITING AND ETHICS

Dividend: WPL has provide the break-up of the payment of dividend for the year 2017 and the

company declares dividend based on their business profitability. This particular aspect creates

scope for the presence of manipulation or fraud in the dividend payment and declaration. For this

reason, the auditors of WPL can consider reviewing the dividend payment of WPL

(Woodside.com.au, 2018).

Section 2

Financial Statement Analytical Review

At the time to conduct the audit operations, the auditors adopt the technique of analytical

review that includes the computation as well as analysis of major financial ratios from different

business dimensions, In case of WPL, the considered rations cover the areas like liquidity,

profitability, asset management, leverage and valuation. The following discussion shows the

analysis of the ratios of WPL for four years from 2014 to 2017:

Liquidity Ratios

Dividend: WPL has provide the break-up of the payment of dividend for the year 2017 and the

company declares dividend based on their business profitability. This particular aspect creates

scope for the presence of manipulation or fraud in the dividend payment and declaration. For this

reason, the auditors of WPL can consider reviewing the dividend payment of WPL

(Woodside.com.au, 2018).

Section 2

Financial Statement Analytical Review

At the time to conduct the audit operations, the auditors adopt the technique of analytical

review that includes the computation as well as analysis of major financial ratios from different

business dimensions, In case of WPL, the considered rations cover the areas like liquidity,

profitability, asset management, leverage and valuation. The following discussion shows the

analysis of the ratios of WPL for four years from 2014 to 2017:

Liquidity Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICS

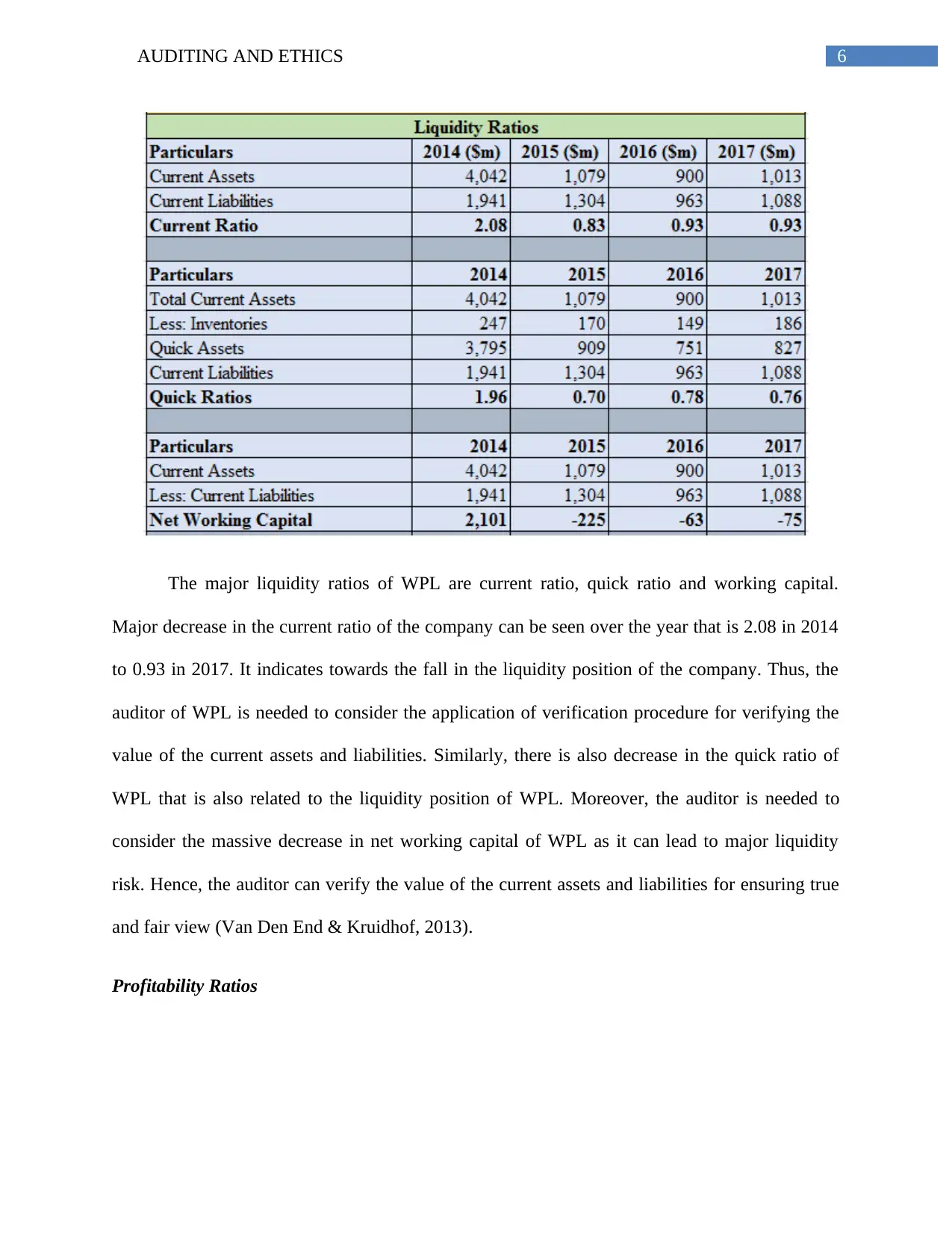

The major liquidity ratios of WPL are current ratio, quick ratio and working capital.

Major decrease in the current ratio of the company can be seen over the year that is 2.08 in 2014

to 0.93 in 2017. It indicates towards the fall in the liquidity position of the company. Thus, the

auditor of WPL is needed to consider the application of verification procedure for verifying the

value of the current assets and liabilities. Similarly, there is also decrease in the quick ratio of

WPL that is also related to the liquidity position of WPL. Moreover, the auditor is needed to

consider the massive decrease in net working capital of WPL as it can lead to major liquidity

risk. Hence, the auditor can verify the value of the current assets and liabilities for ensuring true

and fair view (Van Den End & Kruidhof, 2013).

Profitability Ratios

The major liquidity ratios of WPL are current ratio, quick ratio and working capital.

Major decrease in the current ratio of the company can be seen over the year that is 2.08 in 2014

to 0.93 in 2017. It indicates towards the fall in the liquidity position of the company. Thus, the

auditor of WPL is needed to consider the application of verification procedure for verifying the

value of the current assets and liabilities. Similarly, there is also decrease in the quick ratio of

WPL that is also related to the liquidity position of WPL. Moreover, the auditor is needed to

consider the massive decrease in net working capital of WPL as it can lead to major liquidity

risk. Hence, the auditor can verify the value of the current assets and liabilities for ensuring true

and fair view (Van Den End & Kruidhof, 2013).

Profitability Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICS

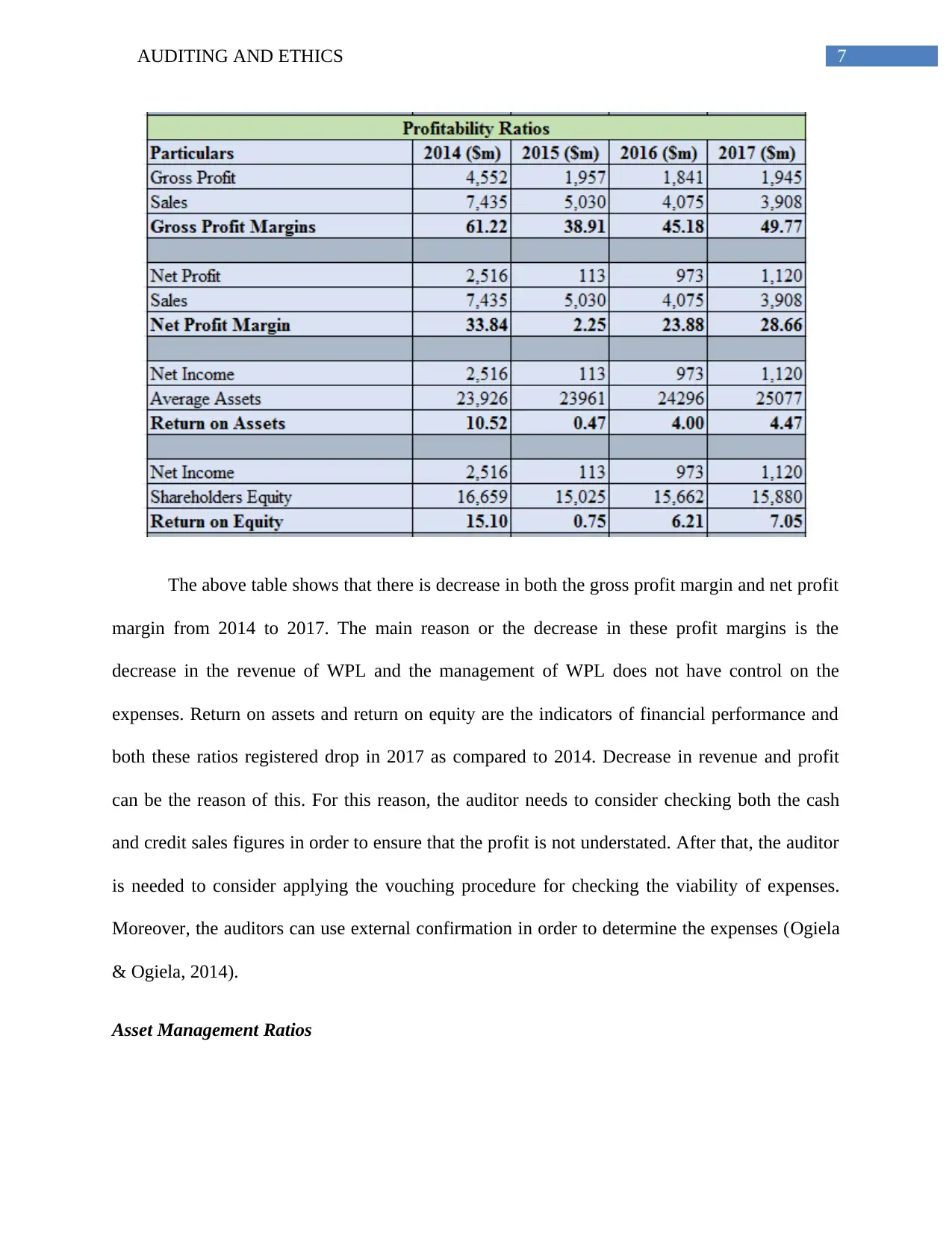

The above table shows that there is decrease in both the gross profit margin and net profit

margin from 2014 to 2017. The main reason or the decrease in these profit margins is the

decrease in the revenue of WPL and the management of WPL does not have control on the

expenses. Return on assets and return on equity are the indicators of financial performance and

both these ratios registered drop in 2017 as compared to 2014. Decrease in revenue and profit

can be the reason of this. For this reason, the auditor needs to consider checking both the cash

and credit sales figures in order to ensure that the profit is not understated. After that, the auditor

is needed to consider applying the vouching procedure for checking the viability of expenses.

Moreover, the auditors can use external confirmation in order to determine the expenses (Ogiela

& Ogiela, 2014).

Asset Management Ratios

The above table shows that there is decrease in both the gross profit margin and net profit

margin from 2014 to 2017. The main reason or the decrease in these profit margins is the

decrease in the revenue of WPL and the management of WPL does not have control on the

expenses. Return on assets and return on equity are the indicators of financial performance and

both these ratios registered drop in 2017 as compared to 2014. Decrease in revenue and profit

can be the reason of this. For this reason, the auditor needs to consider checking both the cash

and credit sales figures in order to ensure that the profit is not understated. After that, the auditor

is needed to consider applying the vouching procedure for checking the viability of expenses.

Moreover, the auditors can use external confirmation in order to determine the expenses (Ogiela

& Ogiela, 2014).

Asset Management Ratios

8AUDITING AND ETHICS

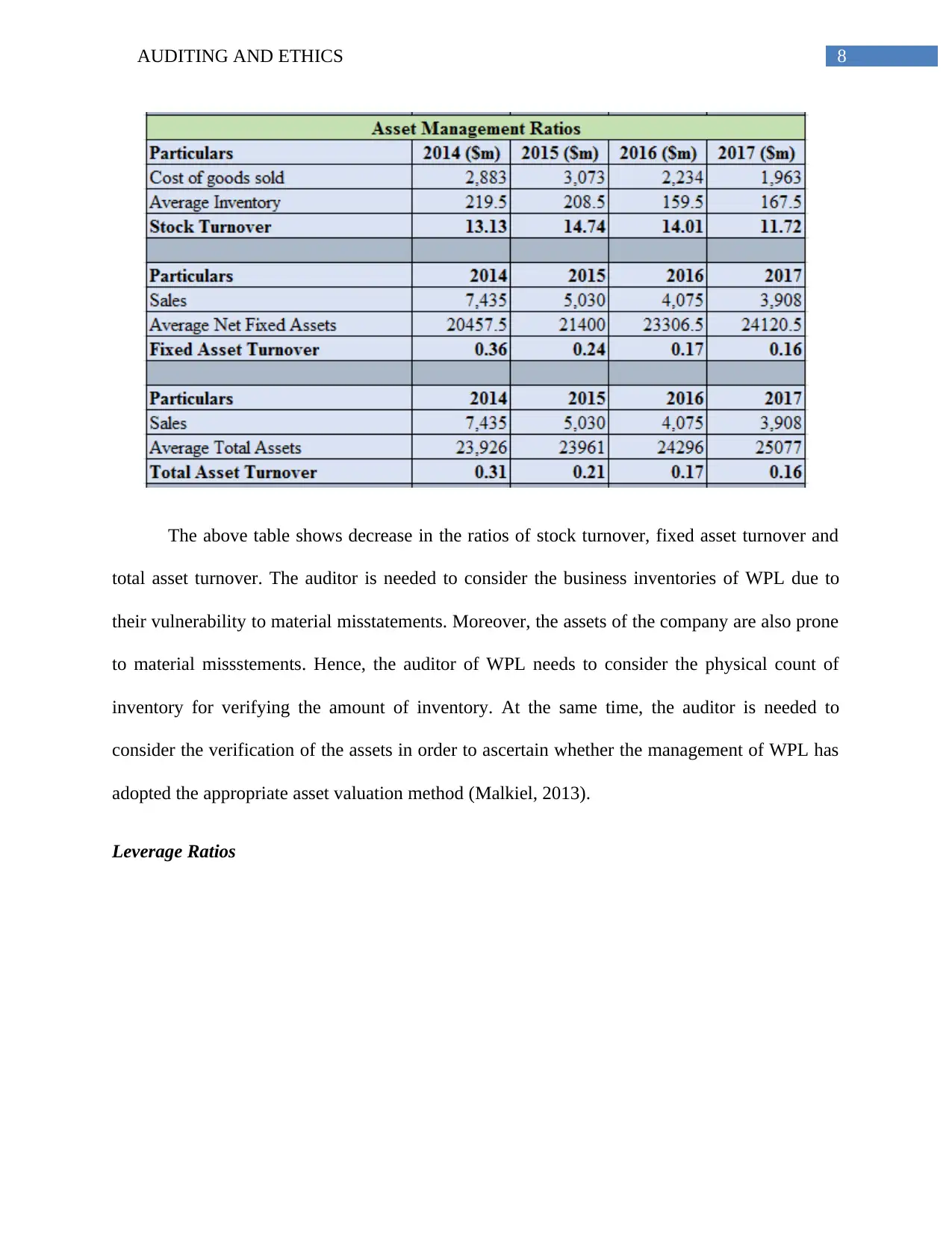

The above table shows decrease in the ratios of stock turnover, fixed asset turnover and

total asset turnover. The auditor is needed to consider the business inventories of WPL due to

their vulnerability to material misstatements. Moreover, the assets of the company are also prone

to material missstements. Hence, the auditor of WPL needs to consider the physical count of

inventory for verifying the amount of inventory. At the same time, the auditor is needed to

consider the verification of the assets in order to ascertain whether the management of WPL has

adopted the appropriate asset valuation method (Malkiel, 2013).

Leverage Ratios

The above table shows decrease in the ratios of stock turnover, fixed asset turnover and

total asset turnover. The auditor is needed to consider the business inventories of WPL due to

their vulnerability to material misstatements. Moreover, the assets of the company are also prone

to material missstements. Hence, the auditor of WPL needs to consider the physical count of

inventory for verifying the amount of inventory. At the same time, the auditor is needed to

consider the verification of the assets in order to ascertain whether the management of WPL has

adopted the appropriate asset valuation method (Malkiel, 2013).

Leverage Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICS

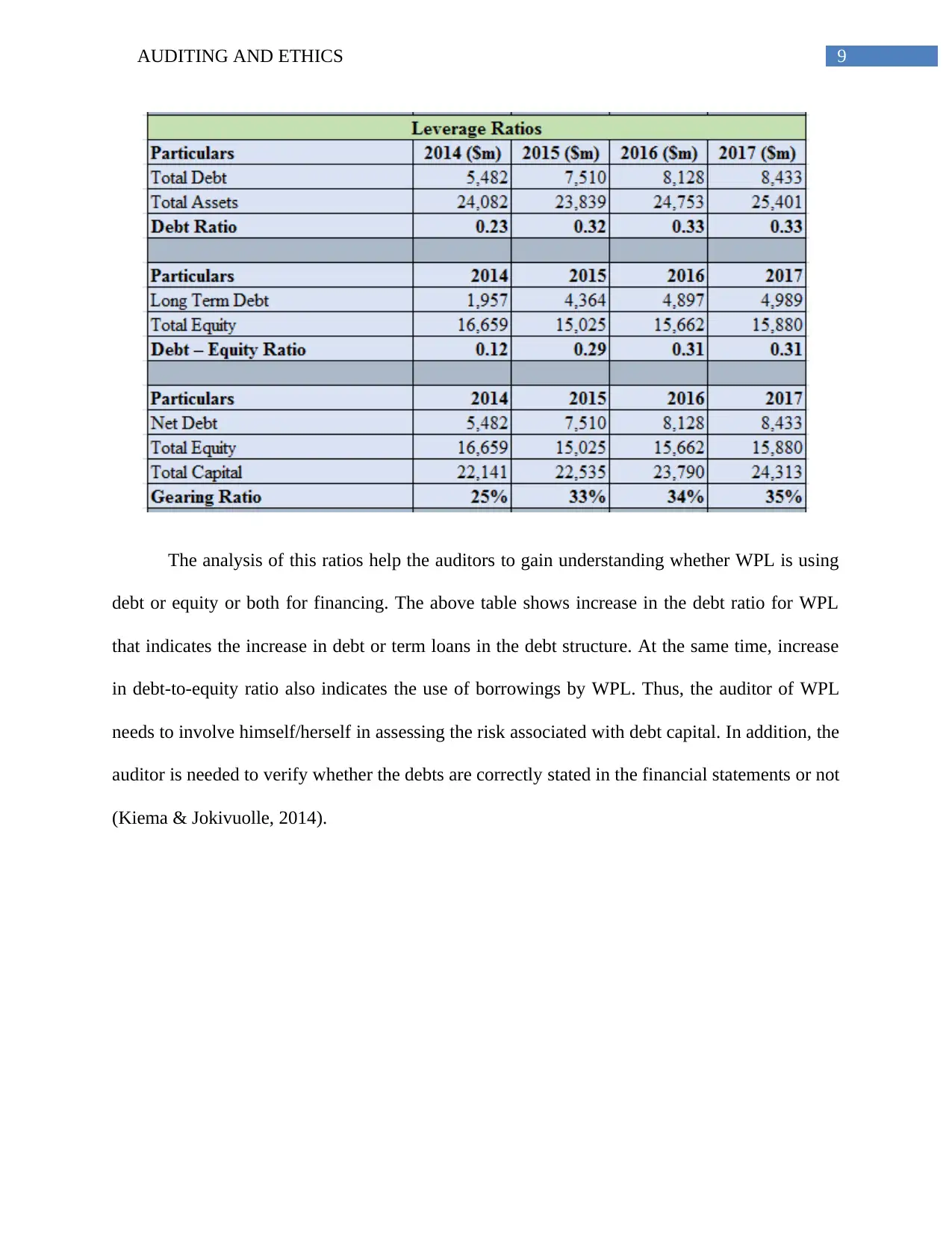

The analysis of this ratios help the auditors to gain understanding whether WPL is using

debt or equity or both for financing. The above table shows increase in the debt ratio for WPL

that indicates the increase in debt or term loans in the debt structure. At the same time, increase

in debt-to-equity ratio also indicates the use of borrowings by WPL. Thus, the auditor of WPL

needs to involve himself/herself in assessing the risk associated with debt capital. In addition, the

auditor is needed to verify whether the debts are correctly stated in the financial statements or not

(Kiema & Jokivuolle, 2014).

The analysis of this ratios help the auditors to gain understanding whether WPL is using

debt or equity or both for financing. The above table shows increase in the debt ratio for WPL

that indicates the increase in debt or term loans in the debt structure. At the same time, increase

in debt-to-equity ratio also indicates the use of borrowings by WPL. Thus, the auditor of WPL

needs to involve himself/herself in assessing the risk associated with debt capital. In addition, the

auditor is needed to verify whether the debts are correctly stated in the financial statements or not

(Kiema & Jokivuolle, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICS

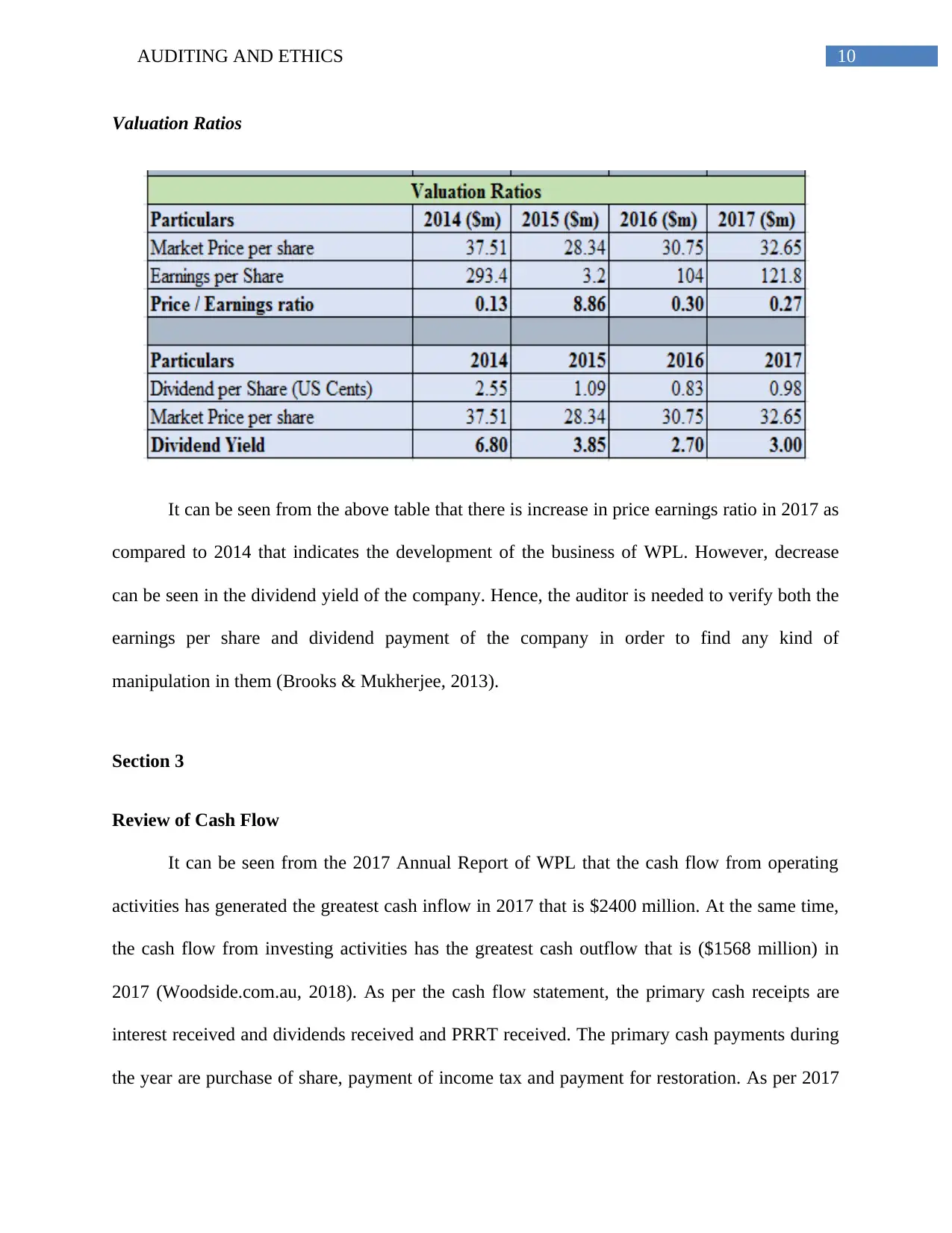

Valuation Ratios

It can be seen from the above table that there is increase in price earnings ratio in 2017 as

compared to 2014 that indicates the development of the business of WPL. However, decrease

can be seen in the dividend yield of the company. Hence, the auditor is needed to verify both the

earnings per share and dividend payment of the company in order to find any kind of

manipulation in them (Brooks & Mukherjee, 2013).

Section 3

Review of Cash Flow

It can be seen from the 2017 Annual Report of WPL that the cash flow from operating

activities has generated the greatest cash inflow in 2017 that is $2400 million. At the same time,

the cash flow from investing activities has the greatest cash outflow that is ($1568 million) in

2017 (Woodside.com.au, 2018). As per the cash flow statement, the primary cash receipts are

interest received and dividends received and PRRT received. The primary cash payments during

the year are purchase of share, payment of income tax and payment for restoration. As per 2017

Valuation Ratios

It can be seen from the above table that there is increase in price earnings ratio in 2017 as

compared to 2014 that indicates the development of the business of WPL. However, decrease

can be seen in the dividend yield of the company. Hence, the auditor is needed to verify both the

earnings per share and dividend payment of the company in order to find any kind of

manipulation in them (Brooks & Mukherjee, 2013).

Section 3

Review of Cash Flow

It can be seen from the 2017 Annual Report of WPL that the cash flow from operating

activities has generated the greatest cash inflow in 2017 that is $2400 million. At the same time,

the cash flow from investing activities has the greatest cash outflow that is ($1568 million) in

2017 (Woodside.com.au, 2018). As per the cash flow statement, the primary cash receipts are

interest received and dividends received and PRRT received. The primary cash payments during

the year are purchase of share, payment of income tax and payment for restoration. As per 2017

11AUDITING AND ETHICS

Annual Report of WPL, the main non-cash financial and investing activities are payment for

capital and exploration expenditures, borrowing costs, proceeds from borrowings, repayment of

borrowings, payment of dividend, contributions to non-controlling interest and others

(Woodside.com.au, 2018).

Going Concern Risk Assessment

The going concern assumption is considered as a fundamental principle for the businesses

and it is needed for the auditor of WPL to report any factor that can affect the going concern

status of the business of WPL. The analysis of the liquidity position of WPL states that there is

major decrease in the liquidity rations of WPL and it is a negative sign for the company (Blay &

Geiger, 2013). Moreover, there is fall in the level of profit of the company along with the

increase in the operating expenses. At the same time, there is increase in the debt risk of WPL

due to the increase in debt capital in the capital structure. All these negative aspects indicates

towards the fact that the going concern status of WPL can be in danger due to drop in some of

the major financial parameters. For this reason, it is needed for the auditor of WPL to provide the

company with the advices for bringing improvements in the liquidity and profitability position

and to put more reliance on the equity share capital in the debt structure (Sundgren & Svanström,

2014).

Review of Auditor’s Report

It can be seen from the 2017 Annual Report of WPL that Ernst & Young (EY) was the

audit partner of WPL for the year 2017. After the examination of the financial statements of

WPL, EY has provided the opinion that the financial statements of the company provided the

true and fair view of the financial position of their business. Moreover, EY has also provided the

opinion that WPL has conducted their accounting operations by complying with the principles of

Annual Report of WPL, the main non-cash financial and investing activities are payment for

capital and exploration expenditures, borrowing costs, proceeds from borrowings, repayment of

borrowings, payment of dividend, contributions to non-controlling interest and others

(Woodside.com.au, 2018).

Going Concern Risk Assessment

The going concern assumption is considered as a fundamental principle for the businesses

and it is needed for the auditor of WPL to report any factor that can affect the going concern

status of the business of WPL. The analysis of the liquidity position of WPL states that there is

major decrease in the liquidity rations of WPL and it is a negative sign for the company (Blay &

Geiger, 2013). Moreover, there is fall in the level of profit of the company along with the

increase in the operating expenses. At the same time, there is increase in the debt risk of WPL

due to the increase in debt capital in the capital structure. All these negative aspects indicates

towards the fact that the going concern status of WPL can be in danger due to drop in some of

the major financial parameters. For this reason, it is needed for the auditor of WPL to provide the

company with the advices for bringing improvements in the liquidity and profitability position

and to put more reliance on the equity share capital in the debt structure (Sundgren & Svanström,

2014).

Review of Auditor’s Report

It can be seen from the 2017 Annual Report of WPL that Ernst & Young (EY) was the

audit partner of WPL for the year 2017. After the examination of the financial statements of

WPL, EY has provided the opinion that the financial statements of the company provided the

true and fair view of the financial position of their business. Moreover, EY has also provided the

opinion that WPL has conducted their accounting operations by complying with the principles of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.