ACC211 Report: ACC211 Project Evaluation for Auditizz Electronics

VerifiedAdded on 2022/12/30

|10

|1894

|99

Report

AI Summary

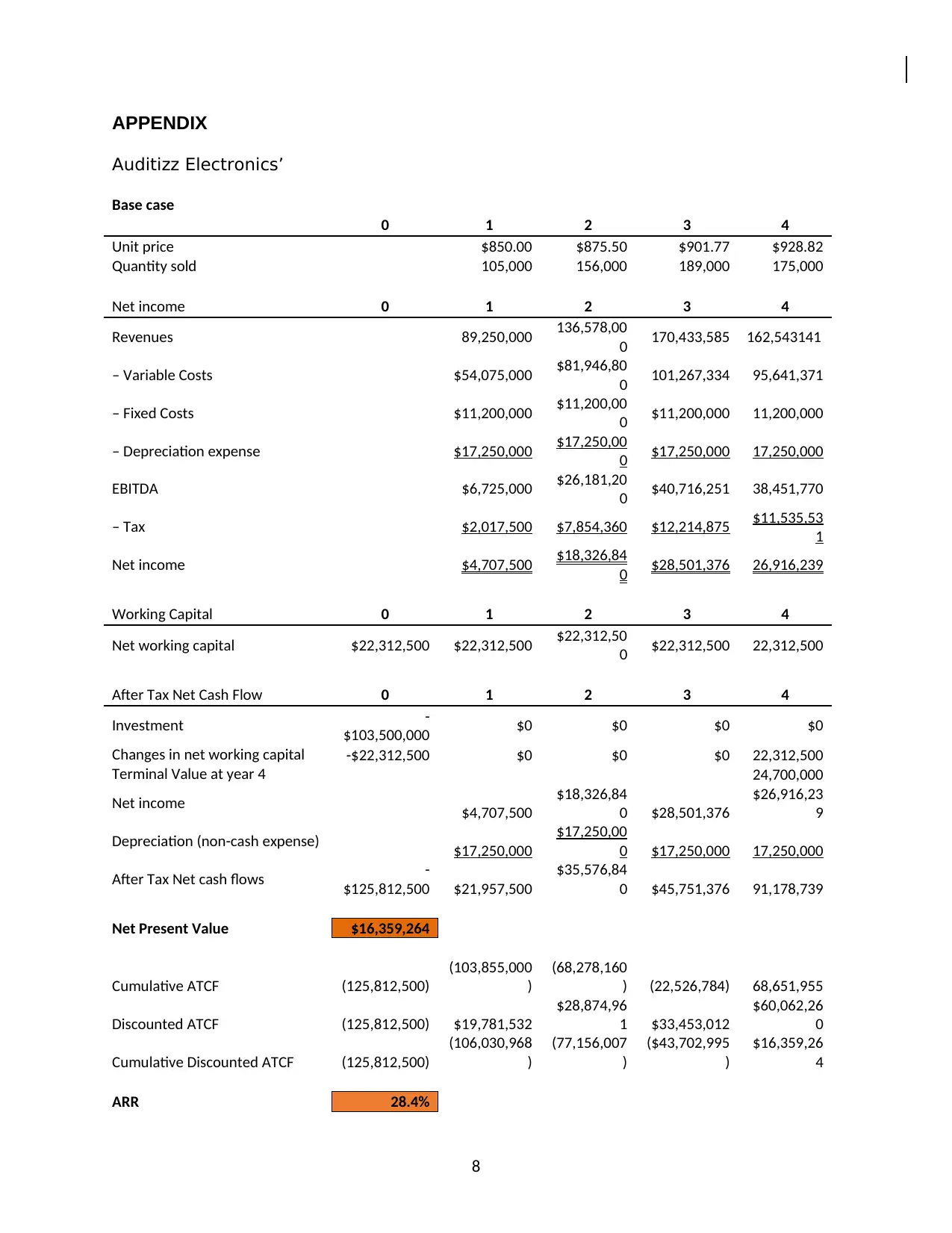

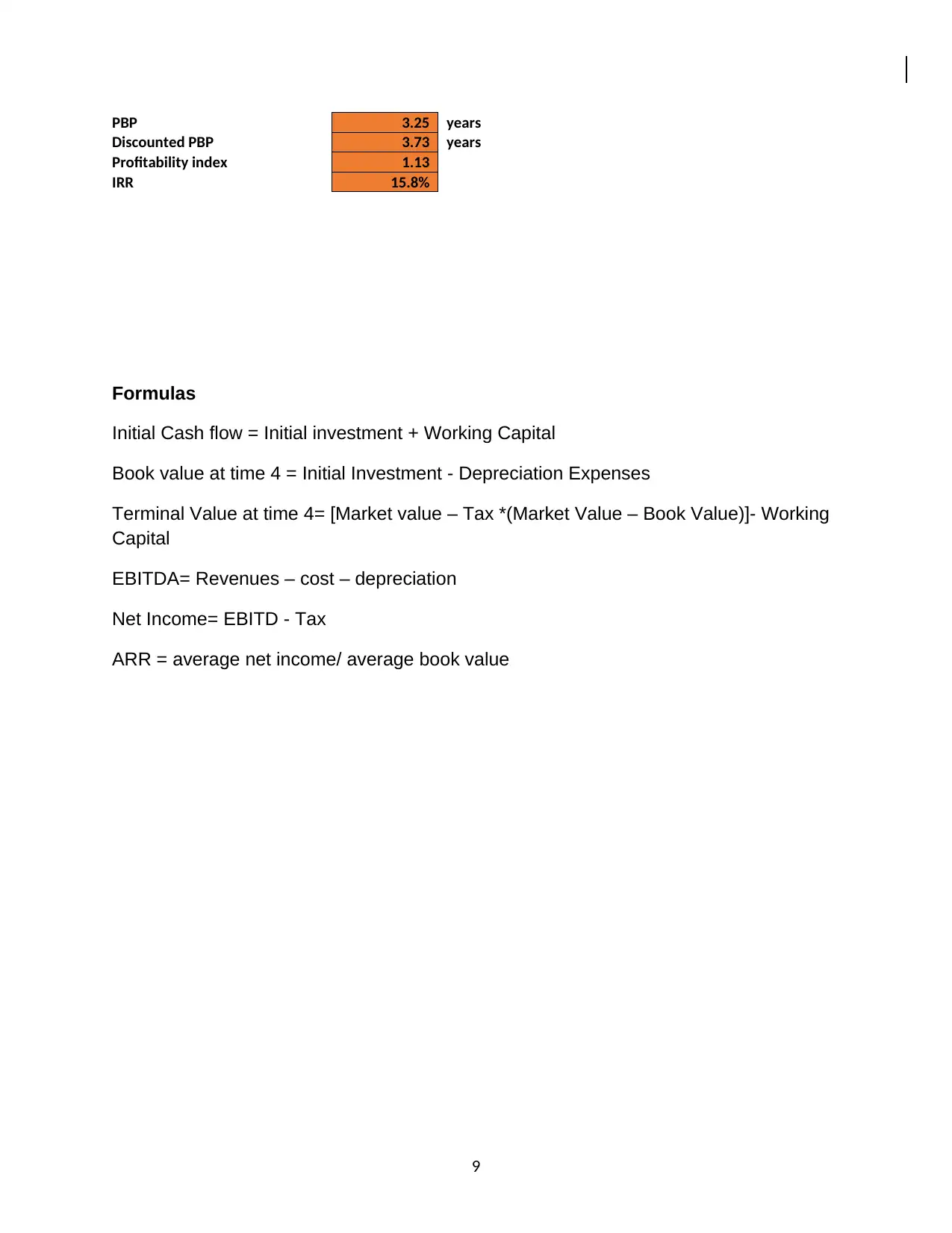

This report provides a comprehensive evaluation of Auditizz Electronics' potential investment in the production of real-time translators (RTT). The analysis employs both discounted and non-discounted cash flow methods to assess the project's viability. The report calculates the payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). Sensitivity analyses are conducted to assess the impact of changes in unit price and sales quantity on the project's profitability. Forecasting risk and its implications are discussed. The report concludes with recommendations on whether Auditizz Electronics should proceed with the investment, considering the project's financial metrics, sensitivity to key assumptions, and overall forecasting risk. The efficient market hypothesis and the relationship between NPV and market value are also briefly addressed.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.