Auditor's Compliance Report: Double Ink Printers Limited Analysis

VerifiedAdded on 2020/03/07

|12

|2539

|44

Report

AI Summary

This report examines the compliances an auditor must undertake when auditing Double Ink Printers Limited (DIPL). It begins with an executive summary and introduction, outlining the report's purpose and structure, which is to understand the auditor's role in presenting financial results to stakeholders. The report then delves into analytical procedures at the planning stage, highlighting the importance of understanding the business and identifying potential risks. Key areas of focus include non-operating expenses, current ratios, debt ratios, and changes in accounting policies. The report also assesses risk factors, such as inventory valuation and the acquisition of Nuclear Publishing Limited, and fraud factors, including external pressures and deviations from accounting standards. The conclusion emphasizes the importance of accurate financial reporting and the auditor's role in ensuring that financial information does not mislead users. The report recommends that auditors perform thorough risk assessment procedures to draw correct opinions from the financial results of the company.

COMPLIANCES TO BE DONE BY AUDITOR IN

CASE OF DOUBLE INK PRINTERS LIMITED

August 20

2017

Student Name

Student ID

CASE OF DOUBLE INK PRINTERS LIMITED

August 20

2017

Student Name

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report has been framed with the title - Compliances to be done by Auditor in case of Double

Ink Printers Limited. The main purpose of doing this report is to understand the role of auditor in

presentation of financial result of company to different stakeholders of that company so that

decisions can be taken by them. This report identifies the three different aspects which an auditor

should consider while planning the audit of Double Ink Printers Limited and conducting audit

thereon. This report helps the auditor to perform analytical procedures and assessment of risk

procedures at the planning stage to identifies the factors which are out of the control of

management and can affect the results presented by the management of company. Through this

report another purpose which can be achieved is ascertainment of fraud factors in company

which results in manipulation of Financial Reporting to attract the different users in positive

manner towards the company.

2

The report has been framed with the title - Compliances to be done by Auditor in case of Double

Ink Printers Limited. The main purpose of doing this report is to understand the role of auditor in

presentation of financial result of company to different stakeholders of that company so that

decisions can be taken by them. This report identifies the three different aspects which an auditor

should consider while planning the audit of Double Ink Printers Limited and conducting audit

thereon. This report helps the auditor to perform analytical procedures and assessment of risk

procedures at the planning stage to identifies the factors which are out of the control of

management and can affect the results presented by the management of company. Through this

report another purpose which can be achieved is ascertainment of fraud factors in company

which results in manipulation of Financial Reporting to attract the different users in positive

manner towards the company.

2

Table of Contents

Executive Summary 2

Introduction 4

Analytical Procedures at Planning Stage 5

Assessment of Risk factors in Planning Stage 7

Assessment of Fraud Factors in conduct of Audit 8

Conclusion and Recommendation 9

References 10

Appendix 11

3

Executive Summary 2

Introduction 4

Analytical Procedures at Planning Stage 5

Assessment of Risk factors in Planning Stage 7

Assessment of Fraud Factors in conduct of Audit 8

Conclusion and Recommendation 9

References 10

Appendix 11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Auditing is the important aspect of every company working anywhere in world. By doing audit

of Financial Results present by the company, the auditor authenticate the results of company

which has be used by third party present in internal and external environment in their decision

making about the affairs of the company. It shows that role of audit and auditor is important for

everyone for management of the company who is presenting the information and for users who

uses the information presented by the company.

This report has been prepared to assess the compliances which the auditor should do at the

planning stage of the audit or at the actual working stage of the audit in conducting audit. The

report has been divided in different parts so that the purpose of the report can be easily

communicated. The report has started with executive summary and introduction containing the

purpose and structure of the report. The next part dealt with the analytical procedures which an

auditor should adopt while doing planning the audit based on the past years results of the

company. The other part explain what are key risk factors which an auditor should think over at

the planning of the audit of company and the chances of in the financial results of the company

with the presence of these factors. The next part of the report what can be fraud factors which are

present in the company which can lead to manipulation of results in the company and how the

auditor should taken care of these factors in conduct of audit of that company. The report has

been ended with proper conclusions and recommendation about the auditor’s role in Double Ink

Printers Limited. The report has been framed using information and facts present on secondary

data sources available online.

4

Auditing is the important aspect of every company working anywhere in world. By doing audit

of Financial Results present by the company, the auditor authenticate the results of company

which has be used by third party present in internal and external environment in their decision

making about the affairs of the company. It shows that role of audit and auditor is important for

everyone for management of the company who is presenting the information and for users who

uses the information presented by the company.

This report has been prepared to assess the compliances which the auditor should do at the

planning stage of the audit or at the actual working stage of the audit in conducting audit. The

report has been divided in different parts so that the purpose of the report can be easily

communicated. The report has started with executive summary and introduction containing the

purpose and structure of the report. The next part dealt with the analytical procedures which an

auditor should adopt while doing planning the audit based on the past years results of the

company. The other part explain what are key risk factors which an auditor should think over at

the planning of the audit of company and the chances of in the financial results of the company

with the presence of these factors. The next part of the report what can be fraud factors which are

present in the company which can lead to manipulation of results in the company and how the

auditor should taken care of these factors in conduct of audit of that company. The report has

been ended with proper conclusions and recommendation about the auditor’s role in Double Ink

Printers Limited. The report has been framed using information and facts present on secondary

data sources available online.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ANALYTICAL PROCEDURES AT PLANNING STAGE

An audit procedure at planning stage contains Analytical procedures which are of two types

Primary Analytical Procedure and Substantive Analytical procedures. Analytical procedures at

the planning stage of audit helps in the auditor to understand the business nature of the Company

for which the audit has to be done by auditor. Auditor can understand different changes that

happened in the business in the period under consideration of the audit and what are key risk

factors that can affect the financial results of the company. These factors help the auditor in

planning stage to identify the areas that can be taken care in depth (ACCA, 2016).

Double Ink Printers Limited is the company for which the analytical procedures has to done by

auditor to understand the way the audit can be planned so that all the key areas containing high

element of risk can be covered during audit. For doing analytical procedures first requirement is

to understand the business nature of the company. The company DIPL is engaged in printing

business of different books and articles for different users. The company is providing the

services of printing to different book publisher, magazines owners and different advertisement

company. The company is taking raw material from home countries and foreign countries on

50% basis so that quality of printing can be maintained. The company has maintained e portal of

different material which can be print by company so that person can identify the material online

and place the order of printing.

Analytical procedures as per ISA 300 at the time of planning stage defines the procedures that

can used by the auditor to identify the potential risk situations by analyzing trends and ratios

which can be calculated from past years financial data. In the case of DIPL, the following trends

and ratios helps the auditor to plan the audit and influenced the planning decisions for the year

the ending 30th June 2015:-

a. Non operating Expense – Foreign Exchange Loss – The auditor has taken into

consideration that 50 % purchases of raw material are from foreign countries having

5

An audit procedure at planning stage contains Analytical procedures which are of two types

Primary Analytical Procedure and Substantive Analytical procedures. Analytical procedures at

the planning stage of audit helps in the auditor to understand the business nature of the Company

for which the audit has to be done by auditor. Auditor can understand different changes that

happened in the business in the period under consideration of the audit and what are key risk

factors that can affect the financial results of the company. These factors help the auditor in

planning stage to identify the areas that can be taken care in depth (ACCA, 2016).

Double Ink Printers Limited is the company for which the analytical procedures has to done by

auditor to understand the way the audit can be planned so that all the key areas containing high

element of risk can be covered during audit. For doing analytical procedures first requirement is

to understand the business nature of the company. The company DIPL is engaged in printing

business of different books and articles for different users. The company is providing the

services of printing to different book publisher, magazines owners and different advertisement

company. The company is taking raw material from home countries and foreign countries on

50% basis so that quality of printing can be maintained. The company has maintained e portal of

different material which can be print by company so that person can identify the material online

and place the order of printing.

Analytical procedures as per ISA 300 at the time of planning stage defines the procedures that

can used by the auditor to identify the potential risk situations by analyzing trends and ratios

which can be calculated from past years financial data. In the case of DIPL, the following trends

and ratios helps the auditor to plan the audit and influenced the planning decisions for the year

the ending 30th June 2015:-

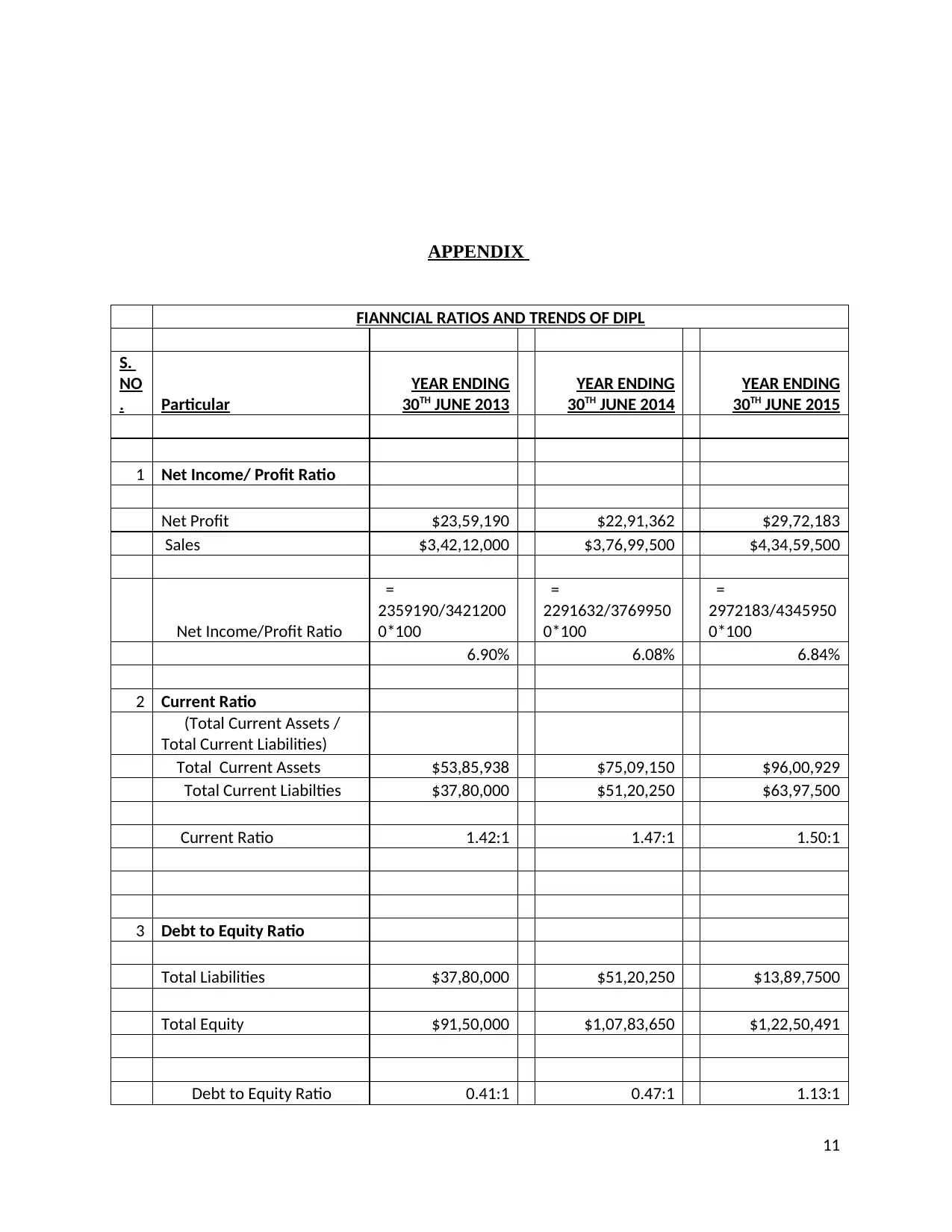

a. Non operating Expense – Foreign Exchange Loss – The auditor has taken into

consideration that 50 % purchases of raw material are from foreign countries having

5

currency different from home country currency. So there is possibility of foreign

exchange gain or loss every year. DIPL has record $ 38,500 in 2013 and $ 49,750 in 2014

as Foreign Exchange Loss but in 2015 the management of company reported zero loss or

gain on foreign transaction which should consider by auditor in planning stage.

b. Current Ratio in relation to Loan: - The Company has Current ratio 1.42: 1 in 2013 and

1.47 in 2014 in relation 1.50:1 in 2015 as calculated in Appendix. The company has taken

a loan of $ 7.5 million in 2015 on a condition that the company should maintain the

current ratio of 1.5: 1 which creates alarming situation for auditor at the planning stage to

think and plan the audit accordingly (Anastasia, 2015).

c. Debt Ratio and Net Profit Ratio :- The DIPL report Debt to Equity ratio 1.13:1 in 2015 as

compared to 0.41:1 in 2013 as shown in Appendix. Showing that the debt has been

increased by the company and more funds are ploughed in the business to earn high

profits but Net profit ratio was 6.90% in 2013 and 6.84% in 2015 showing the adverse

effect of funds on the company profitability. The audit should consider this point while

identifying the procedures for audit (Weiss, 2014).

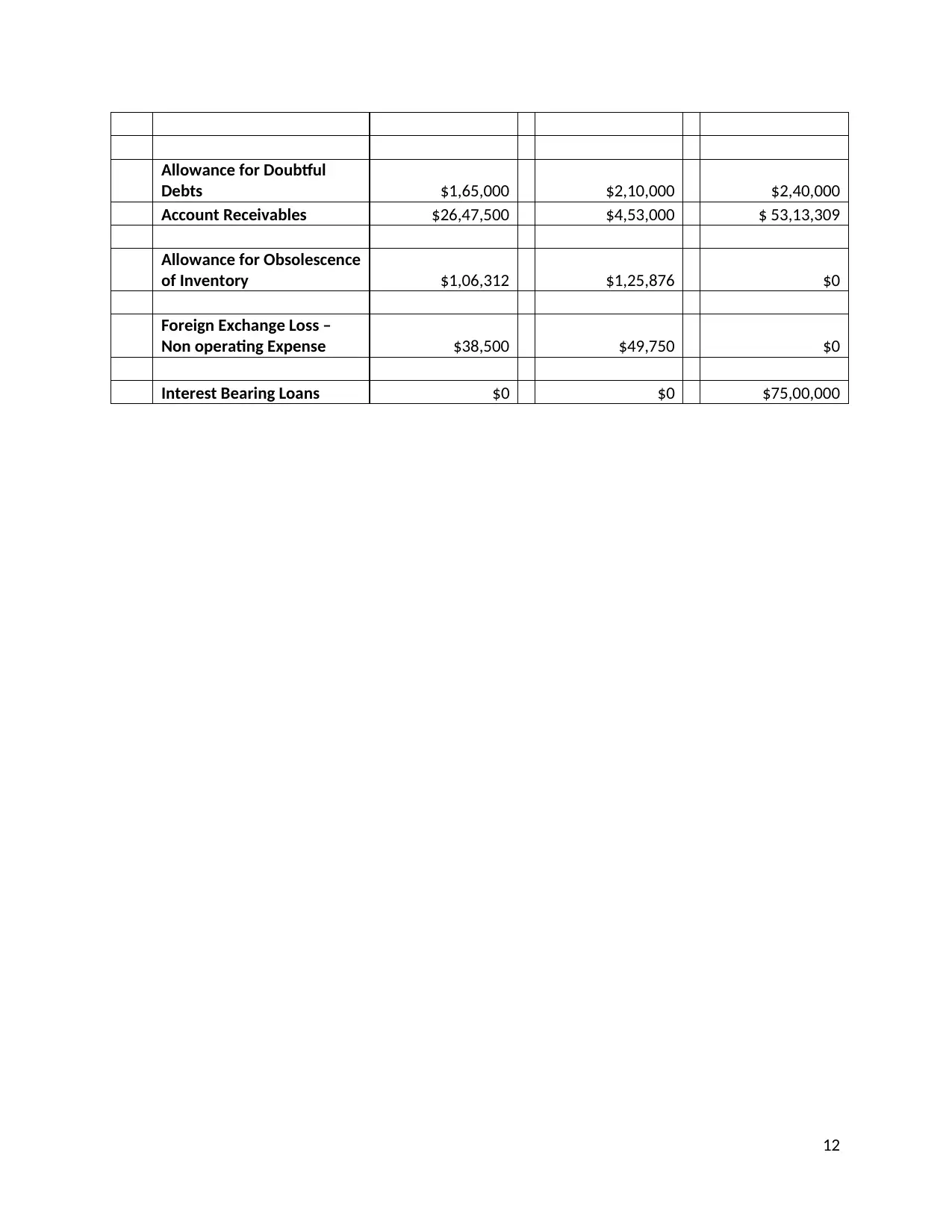

d. Allowance of Doubtful Debts and Account Receivables:-DIPL has reported $ 2, 40,000

as doubtful debts provision in relation to debtor of $ 53, 13,309 in 2015 as compared to $

210,000 as doubtful debts on $ 4, 53,000 debtors in 2014. It shows high variation in

provision for debtor to have errors chances in taking accounting estimate with regards to

debtors.

e. Change in Accounting Policy: - DIPL management has changed the policy in relation to

provision for obsolesce of inventory. The auditor should consider this fact at the time

planning stage that the company is assuming no normal wastage at all from 2015 (Cooper

, 2015).

From the above, it can be clearly understand that the Financial results presented in Financial

Reporting by company management can highly influenced the decisions of the auditor and audit

team at the planning stage.

6

exchange gain or loss every year. DIPL has record $ 38,500 in 2013 and $ 49,750 in 2014

as Foreign Exchange Loss but in 2015 the management of company reported zero loss or

gain on foreign transaction which should consider by auditor in planning stage.

b. Current Ratio in relation to Loan: - The Company has Current ratio 1.42: 1 in 2013 and

1.47 in 2014 in relation 1.50:1 in 2015 as calculated in Appendix. The company has taken

a loan of $ 7.5 million in 2015 on a condition that the company should maintain the

current ratio of 1.5: 1 which creates alarming situation for auditor at the planning stage to

think and plan the audit accordingly (Anastasia, 2015).

c. Debt Ratio and Net Profit Ratio :- The DIPL report Debt to Equity ratio 1.13:1 in 2015 as

compared to 0.41:1 in 2013 as shown in Appendix. Showing that the debt has been

increased by the company and more funds are ploughed in the business to earn high

profits but Net profit ratio was 6.90% in 2013 and 6.84% in 2015 showing the adverse

effect of funds on the company profitability. The audit should consider this point while

identifying the procedures for audit (Weiss, 2014).

d. Allowance of Doubtful Debts and Account Receivables:-DIPL has reported $ 2, 40,000

as doubtful debts provision in relation to debtor of $ 53, 13,309 in 2015 as compared to $

210,000 as doubtful debts on $ 4, 53,000 debtors in 2014. It shows high variation in

provision for debtor to have errors chances in taking accounting estimate with regards to

debtors.

e. Change in Accounting Policy: - DIPL management has changed the policy in relation to

provision for obsolesce of inventory. The auditor should consider this fact at the time

planning stage that the company is assuming no normal wastage at all from 2015 (Cooper

, 2015).

From the above, it can be clearly understand that the Financial results presented in Financial

Reporting by company management can highly influenced the decisions of the auditor and audit

team at the planning stage.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ASSESSMENT OF RISK FACTORS IN PLANNING STAGE

Risk Assessment is the major procedures which have been performed by Auditor to have

reasonable reasons for material misstatement in the financial results presented by the

management of company so that further audit procedures can be framed by analyzing the impact

of risk factors on the business operations and its results. The following are two inherent risk

factors are presented in the DIPL business operations along with their influence and impact on

the material errors in Financial reports of DIPL:-

a. Valuation of Inventory of Raw Material and Finished Goods :- The DIPL has major

portion of its business operations in form of inventory and the company is valuing

inventory on the Average Cost basis resulting the value of inventory of Raw material and

Finished Goods at price lower than the current market value. The risk factor in this

inventory is not valuing at current prices and valuation of inventory at the end of

particular period is less as compared to actual prices. The chances of having high material

misstatement can be there as management can manipulate the financial performance from

business operations by valuing the inventory at fewer prices (Bedard and Graham, 2002).

b. Acquisition of Nuclear Publishing Limited (NPL):- The DIPL has acquired the business

operations of NPL in September 2014 by giving the payment on the basis of net assets of

NPL with the motive to earn high profits margins on sale of medical books of NPL. But

in 2015 there are chances that the books of NPL will become outdated and no one will

buy them in near future because of changes in medical industry. This is considered as

major risk factor on DIPL as the company has done huge investment in taking NPL

operations which is in danger situation. This risk factor can create chances of

misstatement in the financial results by the management of the company in future as the

company may face the shortage funds of lower profits (Gary, 2017).

7

Risk Assessment is the major procedures which have been performed by Auditor to have

reasonable reasons for material misstatement in the financial results presented by the

management of company so that further audit procedures can be framed by analyzing the impact

of risk factors on the business operations and its results. The following are two inherent risk

factors are presented in the DIPL business operations along with their influence and impact on

the material errors in Financial reports of DIPL:-

a. Valuation of Inventory of Raw Material and Finished Goods :- The DIPL has major

portion of its business operations in form of inventory and the company is valuing

inventory on the Average Cost basis resulting the value of inventory of Raw material and

Finished Goods at price lower than the current market value. The risk factor in this

inventory is not valuing at current prices and valuation of inventory at the end of

particular period is less as compared to actual prices. The chances of having high material

misstatement can be there as management can manipulate the financial performance from

business operations by valuing the inventory at fewer prices (Bedard and Graham, 2002).

b. Acquisition of Nuclear Publishing Limited (NPL):- The DIPL has acquired the business

operations of NPL in September 2014 by giving the payment on the basis of net assets of

NPL with the motive to earn high profits margins on sale of medical books of NPL. But

in 2015 there are chances that the books of NPL will become outdated and no one will

buy them in near future because of changes in medical industry. This is considered as

major risk factor on DIPL as the company has done huge investment in taking NPL

operations which is in danger situation. This risk factor can create chances of

misstatement in the financial results by the management of the company in future as the

company may face the shortage funds of lower profits (Gary, 2017).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASSESSMENT OF FRAUD FACTORS IN CONDUCT OF AUDIT

Fraud Risk factors are the dangers situation which shows that chances of frauds in relation to

financial results are there in the company. In DIPL, business operations understandability helps

the auditor to identify the fraud risk factors to which the DIPL and its working are affected. The

following are two key fraud risk factors which relate of false financial reporting by the company

and their impact on the conduct of audit of auditor:-

a. External pressure on the DIPL management: - The company has taken a loan of work $

7.5 million from BDO Finance Company for expansion of business operations. The loan

has been taken on two conditions that the current ratio of DIPL will always be more 1.5:1

and Debt to Equity Ratio will always be less than 1:1 otherwise the loan amount will

repaid by the DIPL management. The management has external pressure from BDO

Finance and this will enhances the chances of material misstatement in the company

financials and will influenced the management to value the current assets on higher side

and this can be shown from allowances of doubtful debtors which has been decreased

drastically in comparison to debtor balances in 2015.

b. Deviation from Accounting Treatment defined in AASB:-The AASB basic requirement

to record income and expense are on accrual basis not on receipt basis. But DIPL are

recording the storage fees on receipt basis and does not booking the accrual income as the

fees are received in advance for whole of the year. This is creating the situation of risk or

frauds on the part of Income to be disclosed in particular year as revenue in DIPL

(Zimbelman, 1997).

From the above two factors which shows the susceptibility of frauds in Financial Reporting of

DIPL will affect the conduct of audit. The auditor has to do substantive audit procedures in

relation to above factors so that the option can be framed easily in effective and corrective

manner.

8

Fraud Risk factors are the dangers situation which shows that chances of frauds in relation to

financial results are there in the company. In DIPL, business operations understandability helps

the auditor to identify the fraud risk factors to which the DIPL and its working are affected. The

following are two key fraud risk factors which relate of false financial reporting by the company

and their impact on the conduct of audit of auditor:-

a. External pressure on the DIPL management: - The company has taken a loan of work $

7.5 million from BDO Finance Company for expansion of business operations. The loan

has been taken on two conditions that the current ratio of DIPL will always be more 1.5:1

and Debt to Equity Ratio will always be less than 1:1 otherwise the loan amount will

repaid by the DIPL management. The management has external pressure from BDO

Finance and this will enhances the chances of material misstatement in the company

financials and will influenced the management to value the current assets on higher side

and this can be shown from allowances of doubtful debtors which has been decreased

drastically in comparison to debtor balances in 2015.

b. Deviation from Accounting Treatment defined in AASB:-The AASB basic requirement

to record income and expense are on accrual basis not on receipt basis. But DIPL are

recording the storage fees on receipt basis and does not booking the accrual income as the

fees are received in advance for whole of the year. This is creating the situation of risk or

frauds on the part of Income to be disclosed in particular year as revenue in DIPL

(Zimbelman, 1997).

From the above two factors which shows the susceptibility of frauds in Financial Reporting of

DIPL will affect the conduct of audit. The auditor has to do substantive audit procedures in

relation to above factors so that the option can be framed easily in effective and corrective

manner.

8

CONCLUSION AND RECOMMENDATION

The financial reporting of every company plays a vital role in the decisions about that company.

The financial reporting done by the management should such that the information present in the

financial reports does not mislead the users of the company. The auditor has to perform different

risk assessment procedures as compliance procedures before planning the audit of any company.

In the case of Double Ink Printer the compliances in relation to analytical procedures, inherent

risk factor and fraud risk factors helps the auditor to understand the nature of business of

company and plan the audit accordingly so that correct opinion can be drawn from the financial

results of the company.

It is recommended from the report that the auditor should performed details analysis before the

start of the audit by considering all the facts present in the company so that the risks can mitigate

for material misstatement in financial reports and audit can be conducted in unbiased manner.

9

The financial reporting of every company plays a vital role in the decisions about that company.

The financial reporting done by the management should such that the information present in the

financial reports does not mislead the users of the company. The auditor has to perform different

risk assessment procedures as compliance procedures before planning the audit of any company.

In the case of Double Ink Printer the compliances in relation to analytical procedures, inherent

risk factor and fraud risk factors helps the auditor to understand the nature of business of

company and plan the audit accordingly so that correct opinion can be drawn from the financial

results of the company.

It is recommended from the report that the auditor should performed details analysis before the

start of the audit by considering all the facts present in the company so that the risks can mitigate

for material misstatement in financial reports and audit can be conducted in unbiased manner.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-

exams-study-resources/p7/technical-articles/analytical-procedures.html accessed

on 20-08-2017

Anastasia, (2015), “Financial Statement Analysis: An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/

accessed

on 20-08-2017.

Bedard, J.C. and Graham, L.E, (2002) “The effects of decision aid orientation on risk

factor identification and audit test planning. Auditing: A Journal of

Practice &

Theory, 21(2), pp.39-56

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor

-resources/Investor-perspectives-2/Documents/Prudence_Investor

-Perspective_Conceptual-FW.PDF accessed on 20-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation

%20Octobe

r%202014.pdf accessed on 20-08-2017

Zimbelman, M.F.,( 1997) ,”The effects of SAS No. 82 on auditors' attention to fraud risk

factors and audit planning decisions- Journal of Accounting Research, 35,

pp.75 -97

10

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-

exams-study-resources/p7/technical-articles/analytical-procedures.html accessed

on 20-08-2017

Anastasia, (2015), “Financial Statement Analysis: An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/

accessed

on 20-08-2017.

Bedard, J.C. and Graham, L.E, (2002) “The effects of decision aid orientation on risk

factor identification and audit test planning. Auditing: A Journal of

Practice &

Theory, 21(2), pp.39-56

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor

-resources/Investor-perspectives-2/Documents/Prudence_Investor

-Perspective_Conceptual-FW.PDF accessed on 20-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation

%20Octobe

r%202014.pdf accessed on 20-08-2017

Zimbelman, M.F.,( 1997) ,”The effects of SAS No. 82 on auditors' attention to fraud risk

factors and audit planning decisions- Journal of Accounting Research, 35,

pp.75 -97

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

FIANNCIAL RATIOS AND TRENDS OF DIPL

S.

NO

. Particular

YEAR ENDING

30TH JUNE 2013

YEAR ENDING

30TH JUNE 2014

YEAR ENDING

30TH JUNE 2015

1 Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

2 Current Ratio

(Total Current Assets /

Total Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilties $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

3 Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

11

FIANNCIAL RATIOS AND TRENDS OF DIPL

S.

NO

. Particular

YEAR ENDING

30TH JUNE 2013

YEAR ENDING

30TH JUNE 2014

YEAR ENDING

30TH JUNE 2015

1 Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

2 Current Ratio

(Total Current Assets /

Total Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilties $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

3 Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

11

Allowance for Doubtful

Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence

of Inventory $1,06,312 $1,25,876 $0

Foreign Exchange Loss –

Non operating Expense $38,500 $49,750 $0

Interest Bearing Loans $0 $0 $75,00,000

12

Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence

of Inventory $1,06,312 $1,25,876 $0

Foreign Exchange Loss –

Non operating Expense $38,500 $49,750 $0

Interest Bearing Loans $0 $0 $75,00,000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.