Auditing Report: Governance, Ethics, and Auditor Liability

VerifiedAdded on 2021/04/19

|13

|2919

|452

Report

AI Summary

This report provides a detailed analysis of auditing practices, focusing on the responsibilities of auditors in reviewing the governance of audit clients. It explores the requirements outlined in auditing standard ASA 135, emphasizing the importance of understanding internal controls and assessing risks. The report also examines governance issues at Commonwealth Bank and the recommendations made by ASIC. Furthermore, it applies the AAA ethical decision-making model to a scenario involving ethical dilemmas within an auditing firm. Finally, the report addresses the role of auditors, the statutory cap on liability, and the implications for audit firms. The report covers various aspects of auditing, including auditor responsibilities, ethical decision-making, governance issues, and the limitations of auditor liability in the context of Australian regulations.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author Note

Auditing

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Answer to Question 1:.....................................................................................................................2

Auditor’s responsibility in reviewing the governance of an audit client:........................................2

Answer to Question 2:.....................................................................................................................2

Application of AAA ethical model for ethical issues identification:..............................................2

Answer to Question 3:.....................................................................................................................3

Explanation of role of auditors and statutory cap on liability of auditors:......................................3

Conclusion:......................................................................................................................................3

Table of Contents

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Answer to Question 1:.....................................................................................................................2

Auditor’s responsibility in reviewing the governance of an audit client:........................................2

Answer to Question 2:.....................................................................................................................2

Application of AAA ethical model for ethical issues identification:..............................................2

Answer to Question 3:.....................................................................................................................3

Explanation of role of auditors and statutory cap on liability of auditors:......................................3

Conclusion:......................................................................................................................................3

2AUDITING

Introduction:

The report is prepared for analyzing the given case study on an Australian accounting

firm, Miller Yates Howarth which has various audit clients in the sector of mining, agriculture,

property and manufacturing industries. In this regard, it is required to demonstrate the

responsibility of auditors to review the governance of audit clients. In addition to this, the issues

relating to the governance of Common wealth bank has been identified and the recommendation

made by ASIC (Australian securities and investment commission) have been explained. The

application of AAA ethical decision making model has been done to the given situation where

senior working manager at MYH is faced with situation where his team member is acting in an

irresponsible way. The later part of report deals with explanation of role of statutory cap on

liability of auditors and incorporation of auditors on limitations of auditor’s liability. It

demonstrates the examination of limitation of liability of auditors in light of statutory cap and

corporation.

Discussion:

Answer to Question 1:

Auditor’s responsibility in reviewing the governance of an audit client:

An auditor as per the auditing standard ASA 135 is required to obtain an understanding

of the environment and internal control of reporting entities by performing the procedures of risk

assessment. Any susceptibility in the financial report of entity regarding the material

misstatements either due to fraud or errors should be discussed with the engagement team. The

assessment of governance also require to understand the internal function of entity that would

helps in determination of function that is relevant to the process of auditing. Determination of

Introduction:

The report is prepared for analyzing the given case study on an Australian accounting

firm, Miller Yates Howarth which has various audit clients in the sector of mining, agriculture,

property and manufacturing industries. In this regard, it is required to demonstrate the

responsibility of auditors to review the governance of audit clients. In addition to this, the issues

relating to the governance of Common wealth bank has been identified and the recommendation

made by ASIC (Australian securities and investment commission) have been explained. The

application of AAA ethical decision making model has been done to the given situation where

senior working manager at MYH is faced with situation where his team member is acting in an

irresponsible way. The later part of report deals with explanation of role of statutory cap on

liability of auditors and incorporation of auditors on limitations of auditor’s liability. It

demonstrates the examination of limitation of liability of auditors in light of statutory cap and

corporation.

Discussion:

Answer to Question 1:

Auditor’s responsibility in reviewing the governance of an audit client:

An auditor as per the auditing standard ASA 135 is required to obtain an understanding

of the environment and internal control of reporting entities by performing the procedures of risk

assessment. Any susceptibility in the financial report of entity regarding the material

misstatements either due to fraud or errors should be discussed with the engagement team. The

assessment of governance also require to understand the internal function of entity that would

helps in determination of function that is relevant to the process of auditing. Determination of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

risks that are considered significant should be determined by using professional judgment. Any

assertion level and risk of material misstatements in the financial report should be assessed and

identified by auditors. Furthermore, auditors are required to obtain an understanding of the

internal control of entity and whether the risks sought from material misstatement is significant

and whether the sufficient appropriate audit evidence is provided by substantive procedures

(Furnham & Gunter, 2015).

Another responsibility of auditor is to maintain and establish an internal control and

appropriate modifications should be made as per the changes. Activities regarding the

management of control within the organization include verifying the review of management

regarding the preparation of bank reconciliation on timely basis, evaluation of compliance of

sales personnel’s with the policies of reporting entity. However, it is not required by auditors to

make the assessment and identification of all business risk as it is not necessary that all business

risks would give rise to material misstatement. Auditors should have detailed understanding of

internal control that would assist them in identification of different types of factors that would

affect the material misstatement and how the timing, nature and extent of procedures of audit are

impacted. Auditors should have complete focus on audit of internal controls and financial

statements for analyzing the objectives impacting their materiality (Louwer et al., 2014). An

understanding of relevant internal control should be obtained by auditors by determining the

extent, nature and timing of audit test and the identification of material misstatements. For

ensuring that there is adequate governance, auditors are required to ascertain whether there is

proper maintenance and implementation of control for evaluating control design. External

auditors as per IAS 135 are required to conduct enquiries on functions of internal audit for

assessing and identifying the material risks. The processing of entity to identify the business

risks that are considered significant should be determined by using professional judgment. Any

assertion level and risk of material misstatements in the financial report should be assessed and

identified by auditors. Furthermore, auditors are required to obtain an understanding of the

internal control of entity and whether the risks sought from material misstatement is significant

and whether the sufficient appropriate audit evidence is provided by substantive procedures

(Furnham & Gunter, 2015).

Another responsibility of auditor is to maintain and establish an internal control and

appropriate modifications should be made as per the changes. Activities regarding the

management of control within the organization include verifying the review of management

regarding the preparation of bank reconciliation on timely basis, evaluation of compliance of

sales personnel’s with the policies of reporting entity. However, it is not required by auditors to

make the assessment and identification of all business risk as it is not necessary that all business

risks would give rise to material misstatement. Auditors should have detailed understanding of

internal control that would assist them in identification of different types of factors that would

affect the material misstatement and how the timing, nature and extent of procedures of audit are

impacted. Auditors should have complete focus on audit of internal controls and financial

statements for analyzing the objectives impacting their materiality (Louwer et al., 2014). An

understanding of relevant internal control should be obtained by auditors by determining the

extent, nature and timing of audit test and the identification of material misstatements. For

ensuring that there is adequate governance, auditors are required to ascertain whether there is

proper maintenance and implementation of control for evaluating control design. External

auditors as per IAS 135 are required to conduct enquiries on functions of internal audit for

assessing and identifying the material risks. The processing of entity to identify the business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

risks relevant to objectives of financial reporting should be assessed by auditors. Therefore, the

responsibility of auditors for reviewing the audit client’s governance requires them to have better

understanding of risk and control of organization.

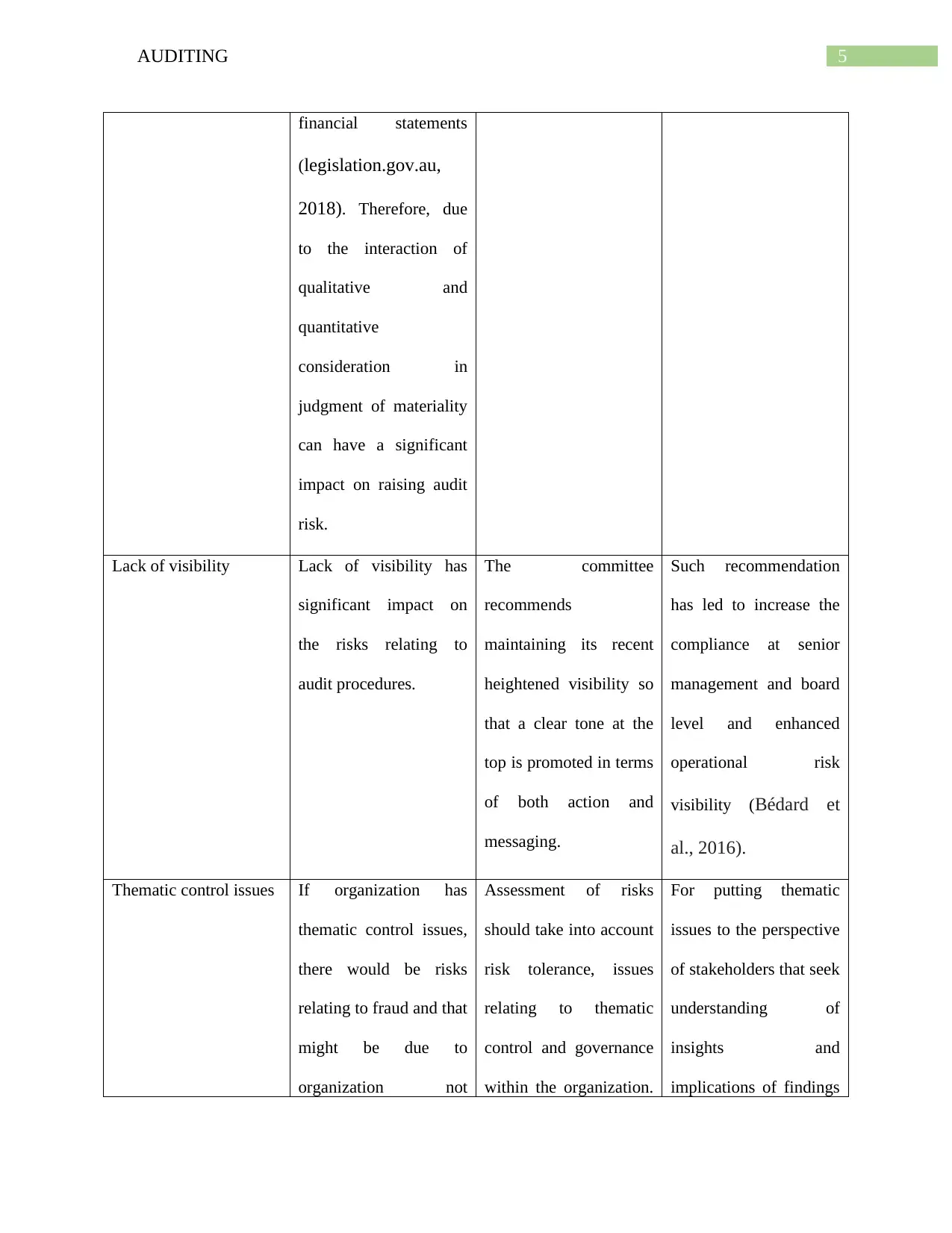

Identification of Commonwealth bank governance issues and ASIC recommendations:

Issue Impact on raising

audit risk

Recommendation Reduction in audit

risk because of the

recommendation

Material issues Materiality concept is

considered important for

fair presentation of

financial statements.

Materiality is

considered to be one of

the important factors in

influencing the audit

risk (Philipsen, 2014).

Consideration of

materiality by auditors

is regarded as matter of

professional judgment

which influences the

perception of the

reasonable person

requirements relying on

It is recommended by

ASIC to embed and

accept collective

accountability and

ensure that executive

committee understand,

discuss and take actions

for mitigating impact of

such risk on business

unit.

The committee of

business unit level risk

should advise

organization on relevant

on material risks so that

the delegated authorities

undertake such

decisions.

risks relevant to objectives of financial reporting should be assessed by auditors. Therefore, the

responsibility of auditors for reviewing the audit client’s governance requires them to have better

understanding of risk and control of organization.

Identification of Commonwealth bank governance issues and ASIC recommendations:

Issue Impact on raising

audit risk

Recommendation Reduction in audit

risk because of the

recommendation

Material issues Materiality concept is

considered important for

fair presentation of

financial statements.

Materiality is

considered to be one of

the important factors in

influencing the audit

risk (Philipsen, 2014).

Consideration of

materiality by auditors

is regarded as matter of

professional judgment

which influences the

perception of the

reasonable person

requirements relying on

It is recommended by

ASIC to embed and

accept collective

accountability and

ensure that executive

committee understand,

discuss and take actions

for mitigating impact of

such risk on business

unit.

The committee of

business unit level risk

should advise

organization on relevant

on material risks so that

the delegated authorities

undertake such

decisions.

5AUDITING

financial statements

(legislation.gov.au,

2018). Therefore, due

to the interaction of

qualitative and

quantitative

consideration in

judgment of materiality

can have a significant

impact on raising audit

risk.

Lack of visibility Lack of visibility has

significant impact on

the risks relating to

audit procedures.

The committee

recommends

maintaining its recent

heightened visibility so

that a clear tone at the

top is promoted in terms

of both action and

messaging.

Such recommendation

has led to increase the

compliance at senior

management and board

level and enhanced

operational risk

visibility (Bédard et

al., 2016).

Thematic control issues If organization has

thematic control issues,

there would be risks

relating to fraud and that

might be due to

organization not

Assessment of risks

should take into account

risk tolerance, issues

relating to thematic

control and governance

within the organization.

For putting thematic

issues to the perspective

of stakeholders that seek

understanding of

insights and

implications of findings

financial statements

(legislation.gov.au,

2018). Therefore, due

to the interaction of

qualitative and

quantitative

consideration in

judgment of materiality

can have a significant

impact on raising audit

risk.

Lack of visibility Lack of visibility has

significant impact on

the risks relating to

audit procedures.

The committee

recommends

maintaining its recent

heightened visibility so

that a clear tone at the

top is promoted in terms

of both action and

messaging.

Such recommendation

has led to increase the

compliance at senior

management and board

level and enhanced

operational risk

visibility (Bédard et

al., 2016).

Thematic control issues If organization has

thematic control issues,

there would be risks

relating to fraud and that

might be due to

organization not

Assessment of risks

should take into account

risk tolerance, issues

relating to thematic

control and governance

within the organization.

For putting thematic

issues to the perspective

of stakeholders that seek

understanding of

insights and

implications of findings

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

complying with the

regulations and laws by

audited entities.

In addition to this, there

should be thematic

review of provision of

audit which would help

in identifying any

deficiencies in

effectiveness of

operations.

generated from audit

(Niemi et al., 2016).

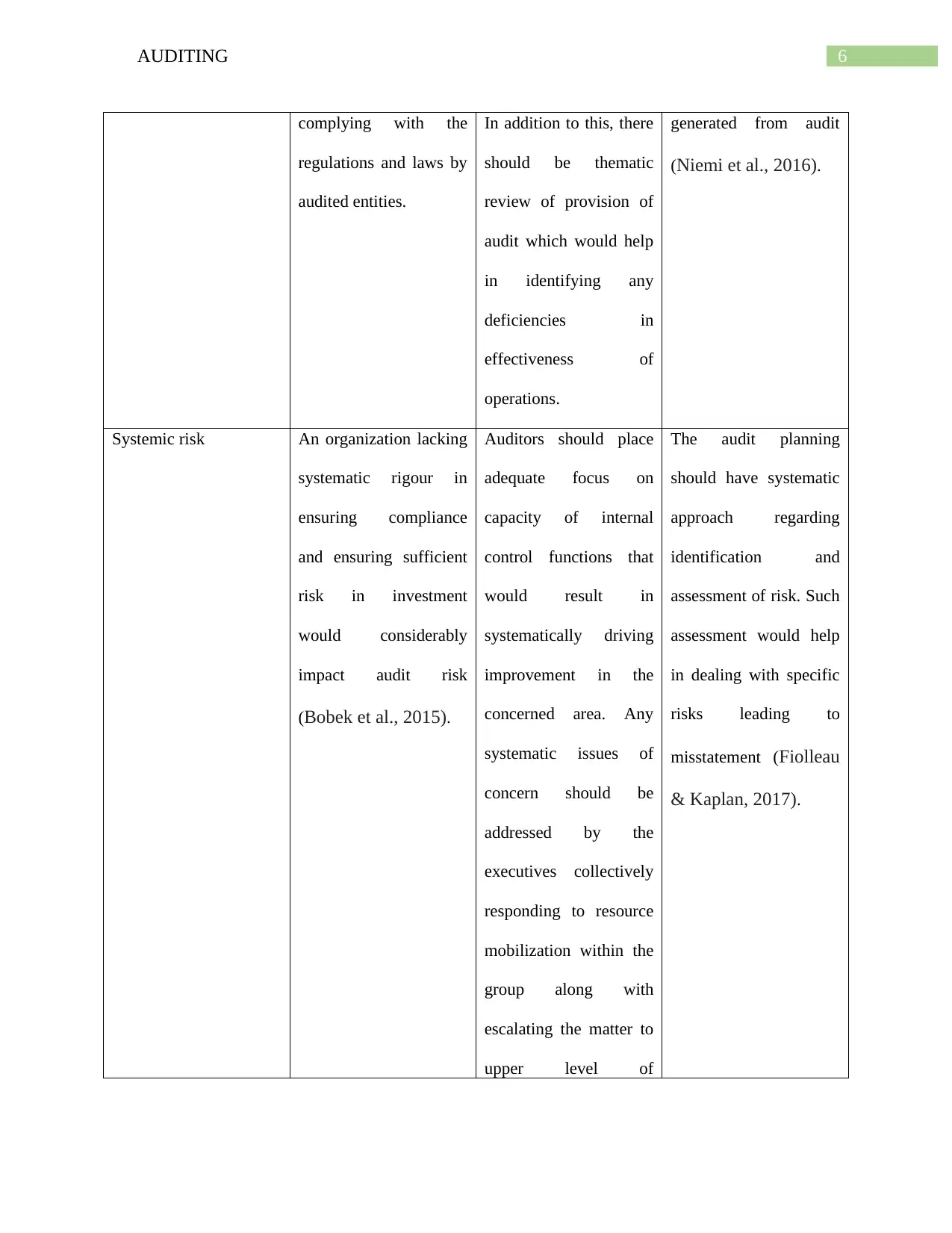

Systemic risk An organization lacking

systematic rigour in

ensuring compliance

and ensuring sufficient

risk in investment

would considerably

impact audit risk

(Bobek et al., 2015).

Auditors should place

adequate focus on

capacity of internal

control functions that

would result in

systematically driving

improvement in the

concerned area. Any

systematic issues of

concern should be

addressed by the

executives collectively

responding to resource

mobilization within the

group along with

escalating the matter to

upper level of

The audit planning

should have systematic

approach regarding

identification and

assessment of risk. Such

assessment would help

in dealing with specific

risks leading to

misstatement (Fiolleau

& Kaplan, 2017).

complying with the

regulations and laws by

audited entities.

In addition to this, there

should be thematic

review of provision of

audit which would help

in identifying any

deficiencies in

effectiveness of

operations.

generated from audit

(Niemi et al., 2016).

Systemic risk An organization lacking

systematic rigour in

ensuring compliance

and ensuring sufficient

risk in investment

would considerably

impact audit risk

(Bobek et al., 2015).

Auditors should place

adequate focus on

capacity of internal

control functions that

would result in

systematically driving

improvement in the

concerned area. Any

systematic issues of

concern should be

addressed by the

executives collectively

responding to resource

mobilization within the

group along with

escalating the matter to

upper level of

The audit planning

should have systematic

approach regarding

identification and

assessment of risk. Such

assessment would help

in dealing with specific

risks leading to

misstatement (Fiolleau

& Kaplan, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

management (Bratten

et al., 2017).

Answer to Question 2:

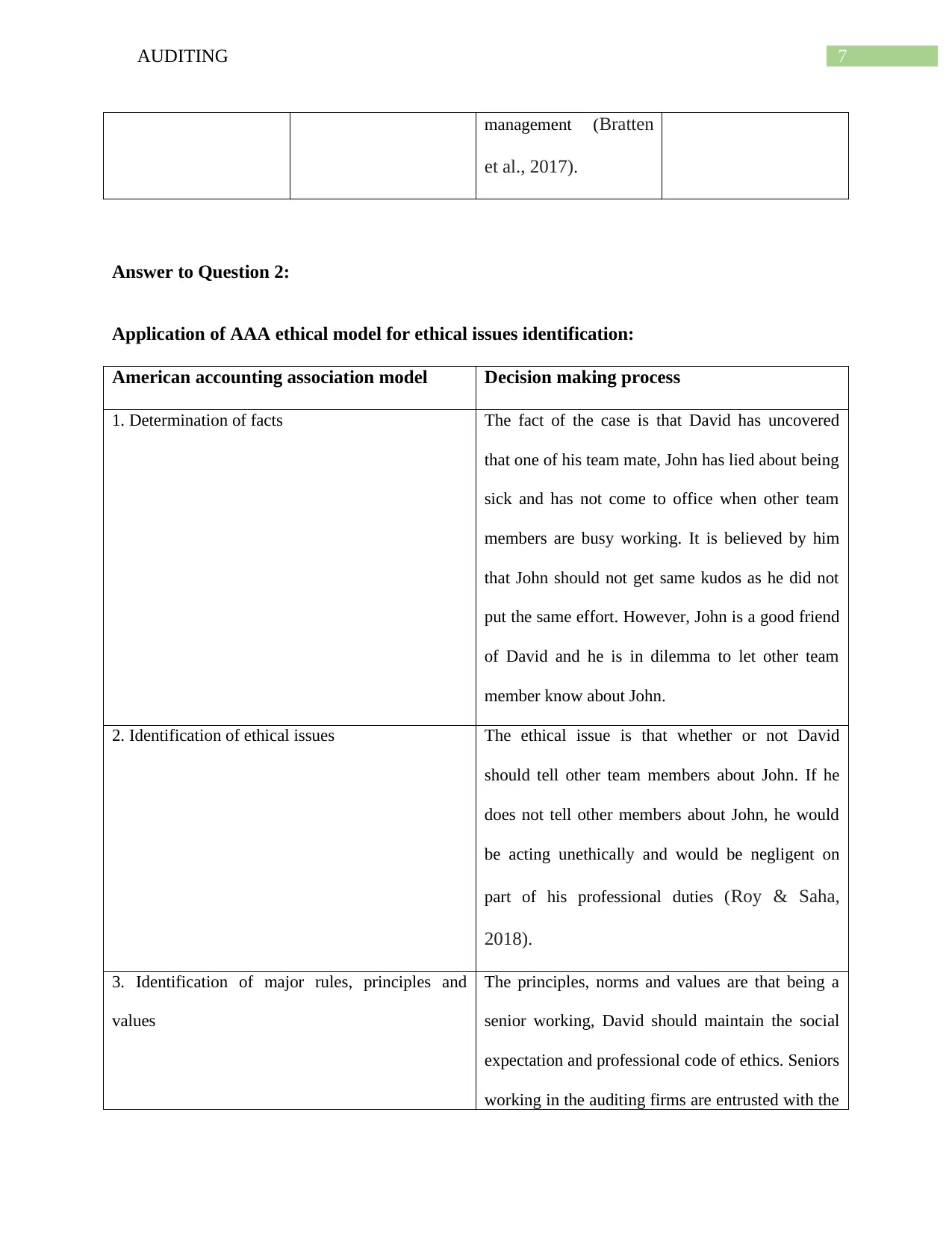

Application of AAA ethical model for ethical issues identification:

American accounting association model Decision making process

1. Determination of facts The fact of the case is that David has uncovered

that one of his team mate, John has lied about being

sick and has not come to office when other team

members are busy working. It is believed by him

that John should not get same kudos as he did not

put the same effort. However, John is a good friend

of David and he is in dilemma to let other team

member know about John.

2. Identification of ethical issues The ethical issue is that whether or not David

should tell other team members about John. If he

does not tell other members about John, he would

be acting unethically and would be negligent on

part of his professional duties (Roy & Saha,

2018).

3. Identification of major rules, principles and

values

The principles, norms and values are that being a

senior working, David should maintain the social

expectation and professional code of ethics. Seniors

working in the auditing firms are entrusted with the

management (Bratten

et al., 2017).

Answer to Question 2:

Application of AAA ethical model for ethical issues identification:

American accounting association model Decision making process

1. Determination of facts The fact of the case is that David has uncovered

that one of his team mate, John has lied about being

sick and has not come to office when other team

members are busy working. It is believed by him

that John should not get same kudos as he did not

put the same effort. However, John is a good friend

of David and he is in dilemma to let other team

member know about John.

2. Identification of ethical issues The ethical issue is that whether or not David

should tell other team members about John. If he

does not tell other members about John, he would

be acting unethically and would be negligent on

part of his professional duties (Roy & Saha,

2018).

3. Identification of major rules, principles and

values

The principles, norms and values are that being a

senior working, David should maintain the social

expectation and professional code of ethics. Seniors

working in the auditing firms are entrusted with the

8AUDITING

task of preventing any thing that interrupts with the

objectivity leading to failure of senior professional

responsibility in the organization.

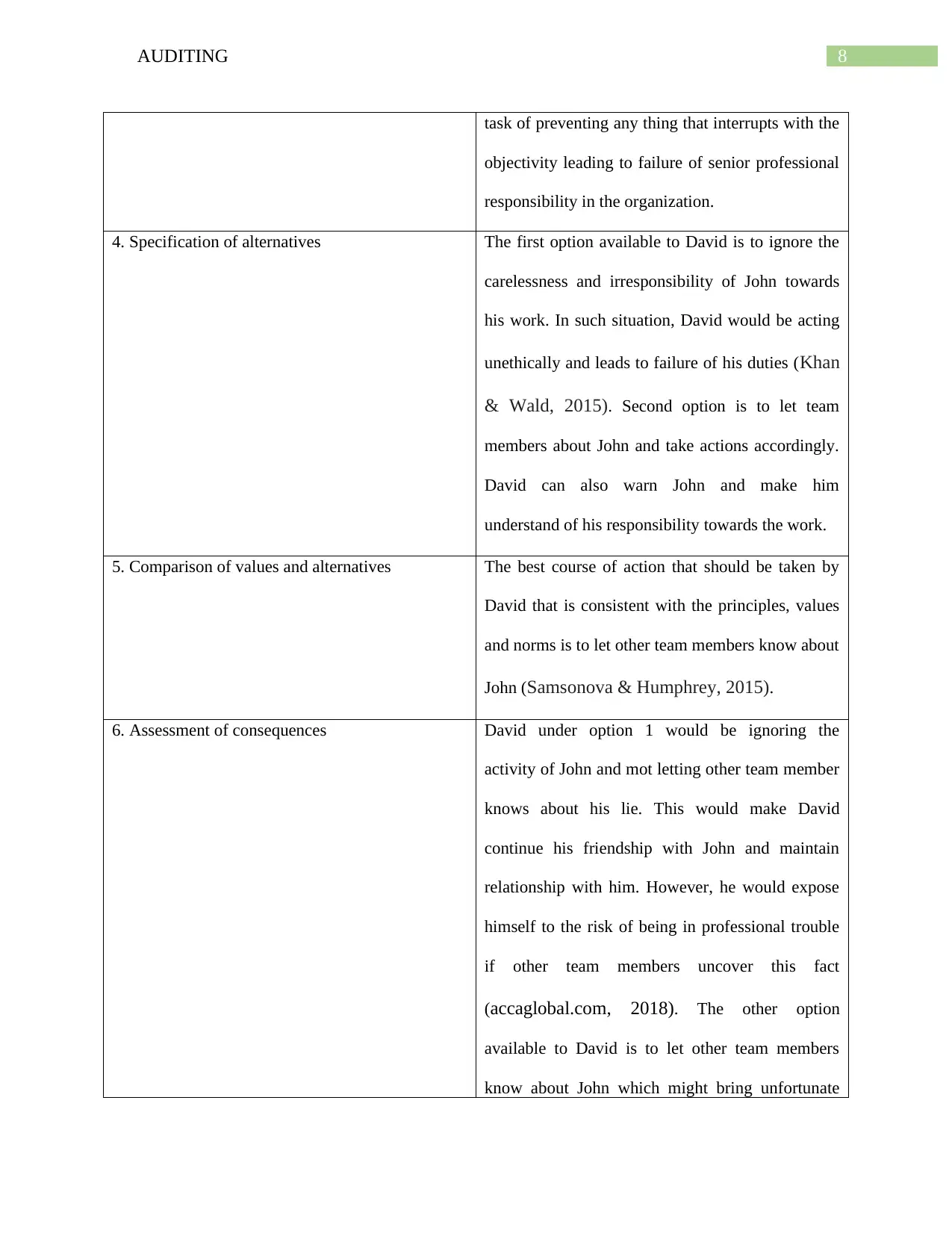

4. Specification of alternatives The first option available to David is to ignore the

carelessness and irresponsibility of John towards

his work. In such situation, David would be acting

unethically and leads to failure of his duties (Khan

& Wald, 2015). Second option is to let team

members about John and take actions accordingly.

David can also warn John and make him

understand of his responsibility towards the work.

5. Comparison of values and alternatives The best course of action that should be taken by

David that is consistent with the principles, values

and norms is to let other team members know about

John (Samsonova & Humphrey, 2015).

6. Assessment of consequences David under option 1 would be ignoring the

activity of John and mot letting other team member

knows about his lie. This would make David

continue his friendship with John and maintain

relationship with him. However, he would expose

himself to the risk of being in professional trouble

if other team members uncover this fact

(accaglobal.com, 2018). The other option

available to David is to let other team members

know about John which might bring unfortunate

task of preventing any thing that interrupts with the

objectivity leading to failure of senior professional

responsibility in the organization.

4. Specification of alternatives The first option available to David is to ignore the

carelessness and irresponsibility of John towards

his work. In such situation, David would be acting

unethically and leads to failure of his duties (Khan

& Wald, 2015). Second option is to let team

members about John and take actions accordingly.

David can also warn John and make him

understand of his responsibility towards the work.

5. Comparison of values and alternatives The best course of action that should be taken by

David that is consistent with the principles, values

and norms is to let other team members know about

John (Samsonova & Humphrey, 2015).

6. Assessment of consequences David under option 1 would be ignoring the

activity of John and mot letting other team member

knows about his lie. This would make David

continue his friendship with John and maintain

relationship with him. However, he would expose

himself to the risk of being in professional trouble

if other team members uncover this fact

(accaglobal.com, 2018). The other option

available to David is to let other team members

know about John which might bring unfortunate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

consequences on part of their friendship.

Nevertheless, it would help in enhancing social

standard of David.

7. Decision making The ethical decision making by David would be

option 2 that is letting team members know about

John’s lie.

Answer to Question 3:

Explanation of role of auditors and statutory cap on liability of auditors:

Liability of auditors has become a matter of increasing concern in recent years.

Regarding the discharge of the statutory functions, there are several heads of potential liability

which the auditors are subjected to. For professional default, auditors are currently exposed to

unlimited liability. The negligence of auditors for statutory audits results in implementation of

statutory cap on liability (Doxey et al., 2015). In Australia, the consequence of the interaction of

statutory regime comes from system of liability for auditors that help in regulating the financial

information disclosure. A set of absolute statutory duties is attributable to the underlying

problem that is associated with auditor’s liability. Audit firms are provided with wider

organizational options by the replacement of several and joint liability with proportional liability.

Statutory requirements are enacted by way of reducing the professional responsibilities of

auditors to third parties, liability of auditors in case of negligence to third parties, tightening

statue limitations and strengthening standards of privity (Bigus, 2015).

Statutory capping involves the imposition of statutory of a limit to liability quantum foe

which liability is held by specific party. Such mechanism involves computation of equity amount

consequences on part of their friendship.

Nevertheless, it would help in enhancing social

standard of David.

7. Decision making The ethical decision making by David would be

option 2 that is letting team members know about

John’s lie.

Answer to Question 3:

Explanation of role of auditors and statutory cap on liability of auditors:

Liability of auditors has become a matter of increasing concern in recent years.

Regarding the discharge of the statutory functions, there are several heads of potential liability

which the auditors are subjected to. For professional default, auditors are currently exposed to

unlimited liability. The negligence of auditors for statutory audits results in implementation of

statutory cap on liability (Doxey et al., 2015). In Australia, the consequence of the interaction of

statutory regime comes from system of liability for auditors that help in regulating the financial

information disclosure. A set of absolute statutory duties is attributable to the underlying

problem that is associated with auditor’s liability. Audit firms are provided with wider

organizational options by the replacement of several and joint liability with proportional liability.

Statutory requirements are enacted by way of reducing the professional responsibilities of

auditors to third parties, liability of auditors in case of negligence to third parties, tightening

statue limitations and strengthening standards of privity (Bigus, 2015).

Statutory capping involves the imposition of statutory of a limit to liability quantum foe

which liability is held by specific party. Such mechanism involves computation of equity amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

in partnership, multiple audit fees and amount of professional indemnity covering the assets. It is

required to have nexus between worth of task performed and extent of liability by making the

assumption of charging multiple of fees. The companies and securities law committee in 1986 in

Australia is responsible for entertaining the possible solutions of statutory cap on liability of

auditors. It is argued that the credibility of audit report would be undermined and there would not

be significant reduction in cost by the imposition of statutory cap and it brings about excessive

damage problems (Cianci et al., 2014).

Conclusion:

From the analysis of responsibility of auditors in reviewing the governance of companies,

it has been found that auditors are required to have adequate understanding of the risks and

control of expertise and organization. The auditing standard 135 depicts the proposed

requirements for making enquiries into the internal functioning of audit. Such enquiries would

help in enhancing the effectiveness of audit engagements. The proposed requirements as per

standard are expected to increase the work of auditors. Various common wealth governance

issues that have been identified include lack of visibility, thematic issues, material issue and

systematic risk. Furthermore, the application of AAA ethical decision making model has helped

senior working professional at MYH to arrive at ethical decision and undertaking decision that is

best in the interest of individual employee and organization as a whole. It has been found in

regard to liability of auditors that limiting their liability is reasonable and fair by proposing a

fixed statutory cap. However, such limitation should not be applicable in event of breaching of

their duties such as negligent behavior and committing fraud by way of collusive behavior.

in partnership, multiple audit fees and amount of professional indemnity covering the assets. It is

required to have nexus between worth of task performed and extent of liability by making the

assumption of charging multiple of fees. The companies and securities law committee in 1986 in

Australia is responsible for entertaining the possible solutions of statutory cap on liability of

auditors. It is argued that the credibility of audit report would be undermined and there would not

be significant reduction in cost by the imposition of statutory cap and it brings about excessive

damage problems (Cianci et al., 2014).

Conclusion:

From the analysis of responsibility of auditors in reviewing the governance of companies,

it has been found that auditors are required to have adequate understanding of the risks and

control of expertise and organization. The auditing standard 135 depicts the proposed

requirements for making enquiries into the internal functioning of audit. Such enquiries would

help in enhancing the effectiveness of audit engagements. The proposed requirements as per

standard are expected to increase the work of auditors. Various common wealth governance

issues that have been identified include lack of visibility, thematic issues, material issue and

systematic risk. Furthermore, the application of AAA ethical decision making model has helped

senior working professional at MYH to arrive at ethical decision and undertaking decision that is

best in the interest of individual employee and organization as a whole. It has been found in

regard to liability of auditors that limiting their liability is reasonable and fair by proposing a

fixed statutory cap. However, such limitation should not be applicable in event of breaching of

their duties such as negligent behavior and committing fraud by way of collusive behavior.

11AUDITING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.