Auditing and Fraud: Auditors' Responsibility and the Fraud Triangle

VerifiedAdded on 2023/05/28

|15

|711

|175

Report

AI Summary

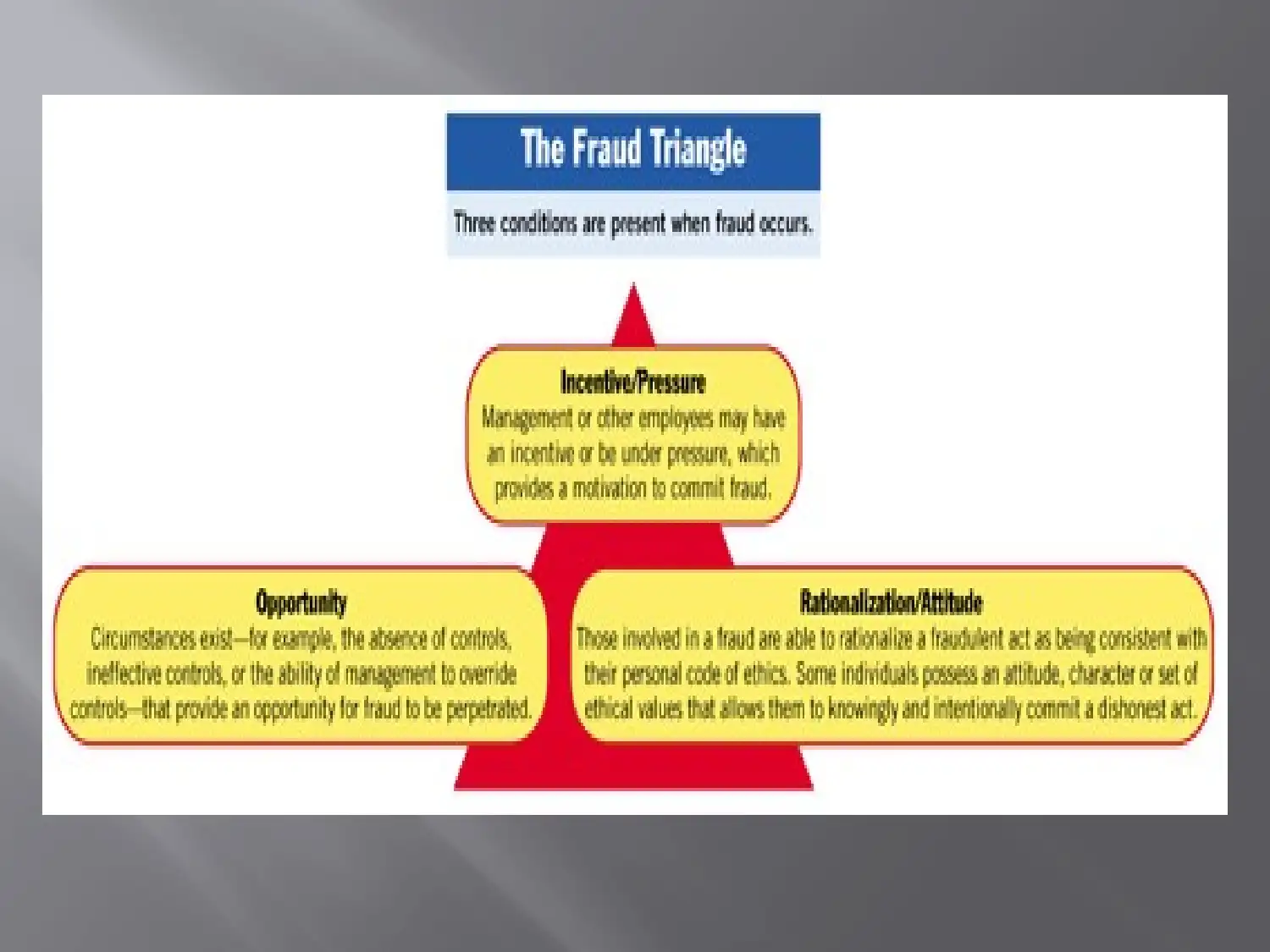

This report delves into the critical responsibility of auditors in detecting fraud within financial statements. It emphasizes that auditors must assess financial statements based on relevant rules, regulations, and standards. The report highlights the importance of internal control evaluations and the use of sampling procedures to form opinions on financial statement quality. A key component of the report is the discussion of the 'Fraud Triangle,' which includes incentive, opportunity, and attitude as indicators of potential fraudulent activities. Auditors are encouraged to be professionally skeptical and to adjust audit procedures based on the presence of these elements to identify and communicate potential fraud to management. The report references relevant auditing standards and provides context through sources like the Brumell Group and the Journal of Accountancy.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.