Australian Taxation Law: Case Studies and Applications

VerifiedAdded on 2020/04/01

|10

|1329

|35

AI Summary

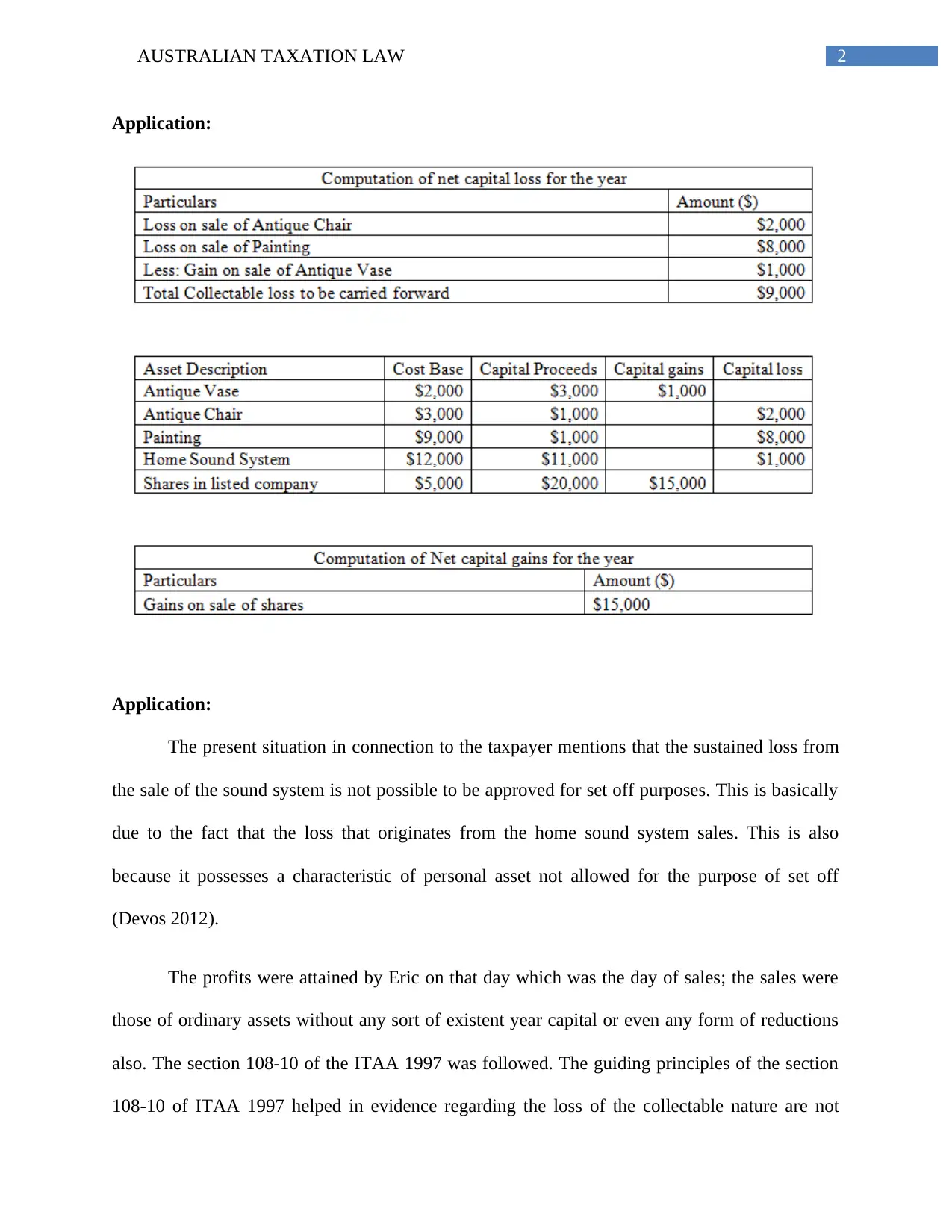

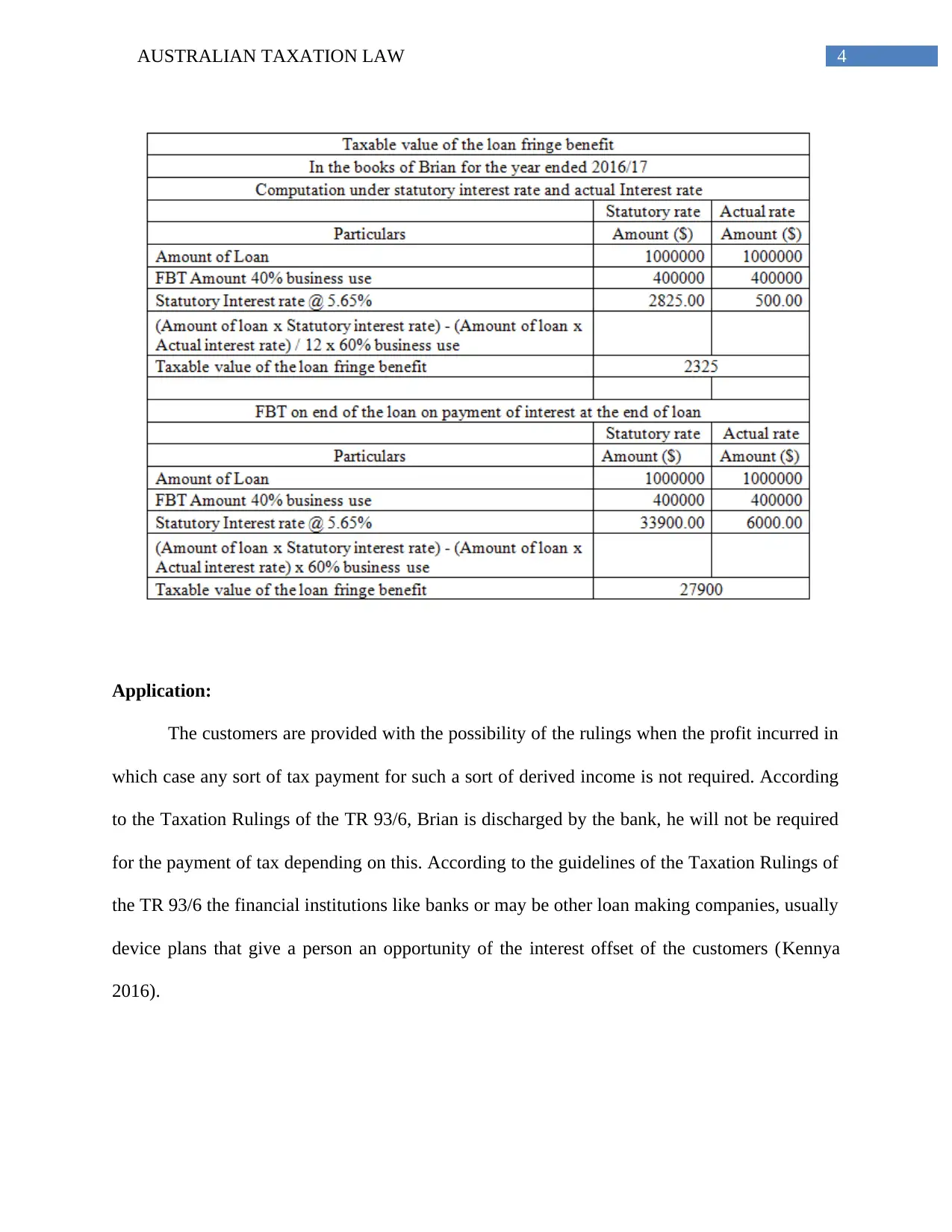

The assignment examines several aspects of Australian Taxation Law as outlined in the Income Tax Assessment Act (ITAA) 1997. It begins by exploring whether a taxpayer can set off capital losses against ordinary income, referencing sections 108-10 and 108-20 ITAA 1997, concluding that such losses are non-set-off due to their personal asset nature. The next question discusses the Fringe Benefit Tax (FBT) calculation under the Fringe Benefits Tax Act 1986 and TR 93/6, explaining scenarios where tax payment is not required for certain interest offsets. The third issue addresses income loss distribution in joint property ownership, using cases like FC of T v McDonald to clarify that such ownership isn't treated as a partnership for tax purposes. In discussing legal tax avoidance, the assignment refers to IRC v Duke Westminster (1936), emphasizing individual rights to arrange tax affairs legally. Finally, it evaluates timber cutting taxation under subsection 6(1) ITAA 1997, determining that income from felled timber is taxable, and considering alternative lump-sum payments as royalties. Each case study provides a practical application of specific sections of Australian Taxation Law.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.