Financial Analysis: Aussie Ltd's Tax Implications in Australia

VerifiedAdded on 2020/04/01

|11

|3299

|467

Report

AI Summary

This report provides a comprehensive analysis of the tax implications for Aussie Ltd., a subsidiary of Meranti Ltd. operating in Australia. The report examines the impact of import duties, GST, income tax, and capital gains tax on the company's financial performance. It delves into the specifics of Australian taxation laws, including the treatment of residents and non-residents, company tax rates, and the application of the nexus test. The analysis covers various aspects, such as advertising expenses, redundancy payments, and the implications of the company's structure. The report also includes a case study of an individual, James, and the tax implications related to his property investments, including renovation expenses and rental income. The document concludes by discussing the key considerations for Aussie Ltd. to minimize its tax liabilities and optimize its financial strategies within the framework of Australian tax regulations.

Running head: ASSESSMENT ITEM 2

ASSESSMENT ITEM 2

ASSESSMENT ITEM 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

ASSESSMENT ITEM 2

Table of contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................7

Reference list.................................................................................................................................10

ASSESSMENT ITEM 2

Table of contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................7

Reference list.................................................................................................................................10

3

ASSESSMENT ITEM 2

Question 1

Aussie ltd is a subsidiary company of Meranti Ltd in Australia. Meranti Ltd. Manufactures high

quality furniture in low cost and exports it to Aussie Ltd. People of Australia can enjoy the low

cost and high quality furniture from Aussie Ltd and for this reason, the sales volume of Aussies

Ltd is high that affects other furniture manufacturers in Australia and threat the local

employment market. In current income year, government of Australia imposed high import duty

to the annual sales of the imported furniture of Aussie Ltd. Aussie Ltd. spent $2 million in

advertising campaign in the Australian media to repeal this duty. The company also wanted the

petition from Australian public in the parliament for this. The advertising amount for this was the

eight times of normal advertising budget. Aussie Ltd. had to pay $1 million redundancy payment

to their 50 employees.

In Australia, the taxation law of Australia is different for residents and non-residents. Residents

need to provide tax for their all the source of income. Income tax regulation 1936 listed some

countries emphasis the tax treatment. The tax might be lower if Meranti Ltd is operated in those

listed countries. If not, then Aussie Ltd. needs to provide high amount of tax for it because,

Aussie Ltd. import furniture from Meranti Ltd.

However, non-residents need to provide tax only sourced in Australia. For the small business the

company tax rate is 27.5% from July, 2016 for the businesses that earn less than $10 million

yearly. For the companies, there is no tax-free threshold. However, for a business, the tax rate is

lower than highest tax of an individual (Tran‐Nam & Evans, 2014). Aussie Ltd. generates high

income by selling furniture in Australian market in low price. For the lower price, Aussie Ltd.

needs to provide lower tax for each of their furniture. However, for higher sales, revenue

generation of Aussie Ltd. is high and for this reason, Aussie Ltd. needs to provide high income

tax.

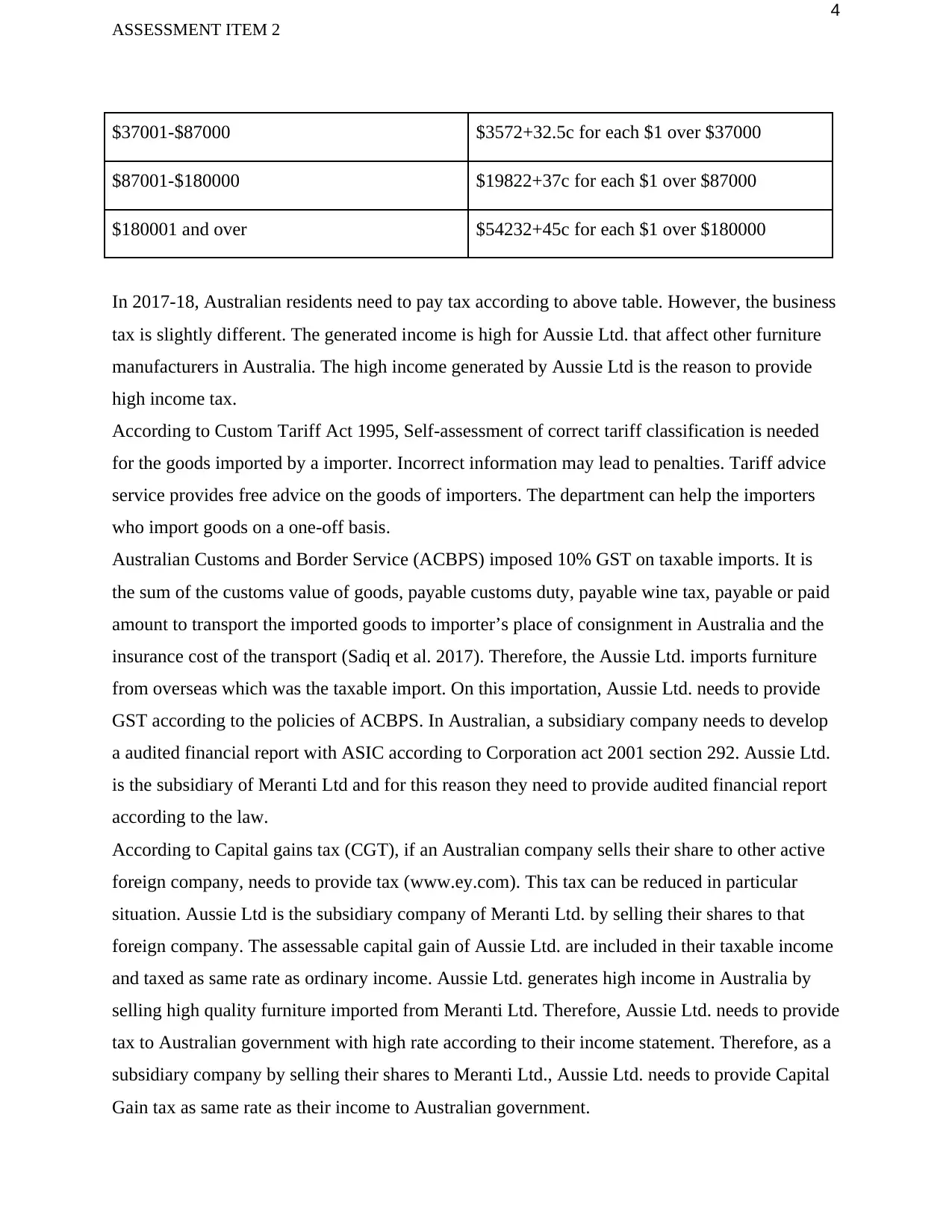

Australian resident tax rate 2017-18

Income Tax

$0- $18200 Nil

$18201- $37000 19c for each $1 over $18200

ASSESSMENT ITEM 2

Question 1

Aussie ltd is a subsidiary company of Meranti Ltd in Australia. Meranti Ltd. Manufactures high

quality furniture in low cost and exports it to Aussie Ltd. People of Australia can enjoy the low

cost and high quality furniture from Aussie Ltd and for this reason, the sales volume of Aussies

Ltd is high that affects other furniture manufacturers in Australia and threat the local

employment market. In current income year, government of Australia imposed high import duty

to the annual sales of the imported furniture of Aussie Ltd. Aussie Ltd. spent $2 million in

advertising campaign in the Australian media to repeal this duty. The company also wanted the

petition from Australian public in the parliament for this. The advertising amount for this was the

eight times of normal advertising budget. Aussie Ltd. had to pay $1 million redundancy payment

to their 50 employees.

In Australia, the taxation law of Australia is different for residents and non-residents. Residents

need to provide tax for their all the source of income. Income tax regulation 1936 listed some

countries emphasis the tax treatment. The tax might be lower if Meranti Ltd is operated in those

listed countries. If not, then Aussie Ltd. needs to provide high amount of tax for it because,

Aussie Ltd. import furniture from Meranti Ltd.

However, non-residents need to provide tax only sourced in Australia. For the small business the

company tax rate is 27.5% from July, 2016 for the businesses that earn less than $10 million

yearly. For the companies, there is no tax-free threshold. However, for a business, the tax rate is

lower than highest tax of an individual (Tran‐Nam & Evans, 2014). Aussie Ltd. generates high

income by selling furniture in Australian market in low price. For the lower price, Aussie Ltd.

needs to provide lower tax for each of their furniture. However, for higher sales, revenue

generation of Aussie Ltd. is high and for this reason, Aussie Ltd. needs to provide high income

tax.

Australian resident tax rate 2017-18

Income Tax

$0- $18200 Nil

$18201- $37000 19c for each $1 over $18200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ASSESSMENT ITEM 2

$37001-$87000 $3572+32.5c for each $1 over $37000

$87001-$180000 $19822+37c for each $1 over $87000

$180001 and over $54232+45c for each $1 over $180000

In 2017-18, Australian residents need to pay tax according to above table. However, the business

tax is slightly different. The generated income is high for Aussie Ltd. that affect other furniture

manufacturers in Australia. The high income generated by Aussie Ltd is the reason to provide

high income tax.

According to Custom Tariff Act 1995, Self-assessment of correct tariff classification is needed

for the goods imported by a importer. Incorrect information may lead to penalties. Tariff advice

service provides free advice on the goods of importers. The department can help the importers

who import goods on a one-off basis.

Australian Customs and Border Service (ACBPS) imposed 10% GST on taxable imports. It is

the sum of the customs value of goods, payable customs duty, payable wine tax, payable or paid

amount to transport the imported goods to importer’s place of consignment in Australia and the

insurance cost of the transport (Sadiq et al. 2017). Therefore, the Aussie Ltd. imports furniture

from overseas which was the taxable import. On this importation, Aussie Ltd. needs to provide

GST according to the policies of ACBPS. In Australian, a subsidiary company needs to develop

a audited financial report with ASIC according to Corporation act 2001 section 292. Aussie Ltd.

is the subsidiary of Meranti Ltd and for this reason they need to provide audited financial report

according to the law.

According to Capital gains tax (CGT), if an Australian company sells their share to other active

foreign company, needs to provide tax (www.ey.com). This tax can be reduced in particular

situation. Aussie Ltd is the subsidiary company of Meranti Ltd. by selling their shares to that

foreign company. The assessable capital gain of Aussie Ltd. are included in their taxable income

and taxed as same rate as ordinary income. Aussie Ltd. generates high income in Australia by

selling high quality furniture imported from Meranti Ltd. Therefore, Aussie Ltd. needs to provide

tax to Australian government with high rate according to their income statement. Therefore, as a

subsidiary company by selling their shares to Meranti Ltd., Aussie Ltd. needs to provide Capital

Gain tax as same rate as their income to Australian government.

ASSESSMENT ITEM 2

$37001-$87000 $3572+32.5c for each $1 over $37000

$87001-$180000 $19822+37c for each $1 over $87000

$180001 and over $54232+45c for each $1 over $180000

In 2017-18, Australian residents need to pay tax according to above table. However, the business

tax is slightly different. The generated income is high for Aussie Ltd. that affect other furniture

manufacturers in Australia. The high income generated by Aussie Ltd is the reason to provide

high income tax.

According to Custom Tariff Act 1995, Self-assessment of correct tariff classification is needed

for the goods imported by a importer. Incorrect information may lead to penalties. Tariff advice

service provides free advice on the goods of importers. The department can help the importers

who import goods on a one-off basis.

Australian Customs and Border Service (ACBPS) imposed 10% GST on taxable imports. It is

the sum of the customs value of goods, payable customs duty, payable wine tax, payable or paid

amount to transport the imported goods to importer’s place of consignment in Australia and the

insurance cost of the transport (Sadiq et al. 2017). Therefore, the Aussie Ltd. imports furniture

from overseas which was the taxable import. On this importation, Aussie Ltd. needs to provide

GST according to the policies of ACBPS. In Australian, a subsidiary company needs to develop

a audited financial report with ASIC according to Corporation act 2001 section 292. Aussie Ltd.

is the subsidiary of Meranti Ltd and for this reason they need to provide audited financial report

according to the law.

According to Capital gains tax (CGT), if an Australian company sells their share to other active

foreign company, needs to provide tax (www.ey.com). This tax can be reduced in particular

situation. Aussie Ltd is the subsidiary company of Meranti Ltd. by selling their shares to that

foreign company. The assessable capital gain of Aussie Ltd. are included in their taxable income

and taxed as same rate as ordinary income. Aussie Ltd. generates high income in Australia by

selling high quality furniture imported from Meranti Ltd. Therefore, Aussie Ltd. needs to provide

tax to Australian government with high rate according to their income statement. Therefore, as a

subsidiary company by selling their shares to Meranti Ltd., Aussie Ltd. needs to provide Capital

Gain tax as same rate as their income to Australian government.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

ASSESSMENT ITEM 2

According to the business structures, Aussie Ltd. can be categorised as Company. A company

needs to be registered for GST if it’s annual turnover $75000 or over (Tang, 2016). They must

lodge annual company tax return and pays tax according to company’s tax rate. Aussie Ltd.

generates revenue by own expertise and skills. Therefore, Personal Services Income (PSI) rule

will be applied on Aussie Ltd. According to PSI, the income generated by Aussie Ltd. can be

treated as their individual income and that affect their claimed deduction.

In order to claim tax deduction, Aussie Ltd. needs to spend money to generate revenue. Aussie

Ltd. needs to show the expanse of their company is used to generate revenue. The expenditure

needs cannot be domestic or private in nature and the expenditure must not be outgoing of capital

(Braithwaite, 2017). The main expenditure of Aussie Ltd. consists of salaries of the employees,

import of the furniture from Meranti Ltd. Therefore, to claim deduction on the imposed tax,

Aussie Ltd. needs to maintain all these conditions.

Aussie Ltd. generates their income by selling furniture mainly to the people of Australia. From

this income, Aussie Ltd. makes their budget, provide salaries to their employees, import furniture

from Meranti Ltd. Aussie Ltd. can claim tax deduction to their income by showing their

expenditure according to Australian law.

According to Income Tax Assessment Act 1997, Aussie Ltd. can claim their deduction on their

income. Section 8-1(1) includes, People can claim deduction if they experience loss in their

income generation and that loss needs to be production related ("Legal Database", 2017).

However, Aussie Ltd. did not experience loss in their business by selling large number furniture

to the people of Australia in lower price. There is also no loss in production system of Aussie

Ltd. Therefore, according to section 8-1(1), Aussie Ltd. cannot claim deduction in their tax.

According to 8-1(2), people cannot deduct a loss or outgoing under this section if it is loss of

capital, loss of domestic or private nature, to gain or producing ones exempt income or non-

assess ("Legal Database", 2017). Aussie Ltd. did not experience any loss in their capital or

domestic or private nature. For this reason, Aussie Ltd. cannot claim any kind off of tax

deduction according to Income Tax Assessment Act 1997 (Residency requirements for

companies, corporate limited partnerships and trusts. 2017). Therefore Aussie Ltd needs to

follow various types of policies. Nexus text is one of the best policies for solving this tax

implication problem. Aussie Ltd should apply this policy to get relief from this new tax

implication.

ASSESSMENT ITEM 2

According to the business structures, Aussie Ltd. can be categorised as Company. A company

needs to be registered for GST if it’s annual turnover $75000 or over (Tang, 2016). They must

lodge annual company tax return and pays tax according to company’s tax rate. Aussie Ltd.

generates revenue by own expertise and skills. Therefore, Personal Services Income (PSI) rule

will be applied on Aussie Ltd. According to PSI, the income generated by Aussie Ltd. can be

treated as their individual income and that affect their claimed deduction.

In order to claim tax deduction, Aussie Ltd. needs to spend money to generate revenue. Aussie

Ltd. needs to show the expanse of their company is used to generate revenue. The expenditure

needs cannot be domestic or private in nature and the expenditure must not be outgoing of capital

(Braithwaite, 2017). The main expenditure of Aussie Ltd. consists of salaries of the employees,

import of the furniture from Meranti Ltd. Therefore, to claim deduction on the imposed tax,

Aussie Ltd. needs to maintain all these conditions.

Aussie Ltd. generates their income by selling furniture mainly to the people of Australia. From

this income, Aussie Ltd. makes their budget, provide salaries to their employees, import furniture

from Meranti Ltd. Aussie Ltd. can claim tax deduction to their income by showing their

expenditure according to Australian law.

According to Income Tax Assessment Act 1997, Aussie Ltd. can claim their deduction on their

income. Section 8-1(1) includes, People can claim deduction if they experience loss in their

income generation and that loss needs to be production related ("Legal Database", 2017).

However, Aussie Ltd. did not experience loss in their business by selling large number furniture

to the people of Australia in lower price. There is also no loss in production system of Aussie

Ltd. Therefore, according to section 8-1(1), Aussie Ltd. cannot claim deduction in their tax.

According to 8-1(2), people cannot deduct a loss or outgoing under this section if it is loss of

capital, loss of domestic or private nature, to gain or producing ones exempt income or non-

assess ("Legal Database", 2017). Aussie Ltd. did not experience any loss in their capital or

domestic or private nature. For this reason, Aussie Ltd. cannot claim any kind off of tax

deduction according to Income Tax Assessment Act 1997 (Residency requirements for

companies, corporate limited partnerships and trusts. 2017). Therefore Aussie Ltd needs to

follow various types of policies. Nexus text is one of the best policies for solving this tax

implication problem. Aussie Ltd should apply this policy to get relief from this new tax

implication.

6

ASSESSMENT ITEM 2

According to nexus test, it is referred to pursuit undertaken by an individual or a private

company in regarding with governmental entity or State. This test basically is used for solving

any dispute between Government and individual persons. This nexus test is required in tax

determination in which this test will help to determination of taxability and deductibility.

According to this case, company needs to appeal against government order and discussion on the

legality of governmental restriction (Residency tests. 2017). Aussie Ltd is also incurred many

expenses about their advertisement against Australian government's policy and now Aussie Ltd

wants to avail tax benefit for recovering their business growth. The company also blame against

government that Government is trying to interference in normal business affairs. Therefore,

Aussie Ltd wants to get relief from Government’s policy by taking some advantages through

taxes by applying this Nexus model.

ASSESSMENT ITEM 2

According to nexus test, it is referred to pursuit undertaken by an individual or a private

company in regarding with governmental entity or State. This test basically is used for solving

any dispute between Government and individual persons. This nexus test is required in tax

determination in which this test will help to determination of taxability and deductibility.

According to this case, company needs to appeal against government order and discussion on the

legality of governmental restriction (Residency tests. 2017). Aussie Ltd is also incurred many

expenses about their advertisement against Australian government's policy and now Aussie Ltd

wants to avail tax benefit for recovering their business growth. The company also blame against

government that Government is trying to interference in normal business affairs. Therefore,

Aussie Ltd wants to get relief from Government’s policy by taking some advantages through

taxes by applying this Nexus model.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

ASSESSMENT ITEM 2

Question 2

James decided to buy a block of five flats which he intended to rent to tenants in the future to

earn a fixed amount. Prior to buying the property, he contacted a building inspector and asked for

his advice about the expenses that he would incur to upgrade and renovate the properties. He was

advised by the inspector that it would cost him around $20,000 for renovating the roof, for

plumbing and to paint the rooms.

James bought the property on the 1st of September 2016 and the plumbing, painting and the

roofing works were all completed and the first tenant came in on the 1st of October 2016. Within

a short period of time after the tenants moved in, a part of the upstairs collapsed and James was

informed that the property was infested with termites and he has to spend around $50,000 to

repair and renovate the ceiling and the flooring. For future benefit James decided to use steel and

good quality timber to make sure there are no further complications. The renovation works were

completed on the 1st of February 2017 and James further paid $2000 to the pest control company

to check the termite infested areas of the property and take measures against them.

Residential homes are generally exempted from taxes in Australia. But if the house or the flat is

used for renovating for profit or running a business, only then they will be capital gains tax

(CGT), income tax and goods and services tax (GST) incurred (Sadiq et al. 2017). Basically, if

the property is used for income only then the owner of the property should include that income in

the income statement and has to pay tax as per the taxable income slab set by the government of

Australia.

In this project since the person named James is purchasing a block of five flats for using it for

earning money, so in this scenario James has to include his income earned from rent in his

income statement as he is taxable according to the government of Australia. In this case, James

has to maintain all the records of all expenses made by him so that he can claim as deductions

and include all the costs in his income statement to make his financial statement more

transparent. In relation to this scenario as well, in case if James decides to sell his properties,

then the amount of money he will get during the sale of the properties will lead him to pay

capital gains tax (CGT). As stated by MacLaran (2014) in some cases if James decides to rent

out the home he has been living then in those cases capital gains tax is not applicable.

ASSESSMENT ITEM 2

Question 2

James decided to buy a block of five flats which he intended to rent to tenants in the future to

earn a fixed amount. Prior to buying the property, he contacted a building inspector and asked for

his advice about the expenses that he would incur to upgrade and renovate the properties. He was

advised by the inspector that it would cost him around $20,000 for renovating the roof, for

plumbing and to paint the rooms.

James bought the property on the 1st of September 2016 and the plumbing, painting and the

roofing works were all completed and the first tenant came in on the 1st of October 2016. Within

a short period of time after the tenants moved in, a part of the upstairs collapsed and James was

informed that the property was infested with termites and he has to spend around $50,000 to

repair and renovate the ceiling and the flooring. For future benefit James decided to use steel and

good quality timber to make sure there are no further complications. The renovation works were

completed on the 1st of February 2017 and James further paid $2000 to the pest control company

to check the termite infested areas of the property and take measures against them.

Residential homes are generally exempted from taxes in Australia. But if the house or the flat is

used for renovating for profit or running a business, only then they will be capital gains tax

(CGT), income tax and goods and services tax (GST) incurred (Sadiq et al. 2017). Basically, if

the property is used for income only then the owner of the property should include that income in

the income statement and has to pay tax as per the taxable income slab set by the government of

Australia.

In this project since the person named James is purchasing a block of five flats for using it for

earning money, so in this scenario James has to include his income earned from rent in his

income statement as he is taxable according to the government of Australia. In this case, James

has to maintain all the records of all expenses made by him so that he can claim as deductions

and include all the costs in his income statement to make his financial statement more

transparent. In relation to this scenario as well, in case if James decides to sell his properties,

then the amount of money he will get during the sale of the properties will lead him to pay

capital gains tax (CGT). As stated by MacLaran (2014) in some cases if James decides to rent

out the home he has been living then in those cases capital gains tax is not applicable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ASSESSMENT ITEM 2

But in case James has a property which he does not intend to rent out to people then the property

would be subject to capital gains tax same as in case of renting a property but income tax cannot

be claimed for owning the property as it does not generate any rental income. As stated by Jones

(2016) the cost of ownership of the property can be included in the base price of the property

which would eventually reduce the capital gains tax during the time of sale. As stated by Wood,

Ong & Cigdem (2016) the amount of tax levied when the property is owned or when the

property is getting sold then the amount of tax depends on whether the property was used for

business or commercial purpose or for residential purpose (Legal Database. 2017). Vacant land

is considered to be capital asset and it is taxable under the capital gains tax laws. However, in

case of property being sold, the amount is considered to be ordinary income and is considered

under goods and services tax (GST) on the amount received from selling the property.

There are various situations regarding the taxation system like if a person is renovating one or

more property, then tax will be levied determining whether the person is a person property

investor or renovating a property for business or commercial purpose with an aim to earn profit.

In reference to this as opined by Tang (2016) if the person is investing in order to earn profit then

the amount will be considered to be taxable under the government rules. Furthermore, if

construction is done for new residential purpose, then the builders are liable to goods and

services tax (GST) on the selling price and the builders can claim the credit amount for the

construction costs and the price related to purchases during construction. Construction businesses

should always report to the ATO every year regarding the total amount of money paid to the

contractors and suppliers of the construction materials and goods.

In cases where a property is leased or rented for business purpose whether it is commercial or a

personal home then the amount of money earned should be included in the statement of tax

return and the owner of the property can also claim income tax deductions for certain expenses to

the property. As stated by Kelly, Hunter, Harrison and Donegan (2013) the owner of the property

will also be liable for capital gains tax on any sale of assets and the owner can have goods and

services tax entitlements and obligations when the property is leased or rented for business

purpose. Furthermore, if the owner of the property deals with a one-off transaction like leasing or

renovating and buying or selling then the owner will be considered to be owning an enterprise

and if the profit earned from the transactions exceeds the goods and services tax registration limit

then the owner has to register for goods and services tax (Legal Database. 2017).

ASSESSMENT ITEM 2

But in case James has a property which he does not intend to rent out to people then the property

would be subject to capital gains tax same as in case of renting a property but income tax cannot

be claimed for owning the property as it does not generate any rental income. As stated by Jones

(2016) the cost of ownership of the property can be included in the base price of the property

which would eventually reduce the capital gains tax during the time of sale. As stated by Wood,

Ong & Cigdem (2016) the amount of tax levied when the property is owned or when the

property is getting sold then the amount of tax depends on whether the property was used for

business or commercial purpose or for residential purpose (Legal Database. 2017). Vacant land

is considered to be capital asset and it is taxable under the capital gains tax laws. However, in

case of property being sold, the amount is considered to be ordinary income and is considered

under goods and services tax (GST) on the amount received from selling the property.

There are various situations regarding the taxation system like if a person is renovating one or

more property, then tax will be levied determining whether the person is a person property

investor or renovating a property for business or commercial purpose with an aim to earn profit.

In reference to this as opined by Tang (2016) if the person is investing in order to earn profit then

the amount will be considered to be taxable under the government rules. Furthermore, if

construction is done for new residential purpose, then the builders are liable to goods and

services tax (GST) on the selling price and the builders can claim the credit amount for the

construction costs and the price related to purchases during construction. Construction businesses

should always report to the ATO every year regarding the total amount of money paid to the

contractors and suppliers of the construction materials and goods.

In cases where a property is leased or rented for business purpose whether it is commercial or a

personal home then the amount of money earned should be included in the statement of tax

return and the owner of the property can also claim income tax deductions for certain expenses to

the property. As stated by Kelly, Hunter, Harrison and Donegan (2013) the owner of the property

will also be liable for capital gains tax on any sale of assets and the owner can have goods and

services tax entitlements and obligations when the property is leased or rented for business

purpose. Furthermore, if the owner of the property deals with a one-off transaction like leasing or

renovating and buying or selling then the owner will be considered to be owning an enterprise

and if the profit earned from the transactions exceeds the goods and services tax registration limit

then the owner has to register for goods and services tax (Legal Database. 2017).

9

ASSESSMENT ITEM 2

In this project since the main focus is on a single person, so after discussing the scenarios when

and where can a person be charged for tax, now it should be determined whether the amount

earned and the amount spent by James on the property to purchase as well as to renovate would

be taxable or not. After studying all the cases when a person can be taxed and in what situations,

it can be concluded that James would be chargeable for the entire amount spent by him. First, he

will be charged for the expenses for developing and renovating the properties that he had bought.

Secondly, he is liable to pay tax as the amount of money earned from leasing the property for

rent will earn revenues which will be source of income for him. So, since the building is

becoming a commercial one, so he will have to pay tax for the amount of money he is earning.

Another aspect that James can use to his benefit is that he can claim deductions in tax for the

amount of money he spent on purchasing, renovating and developing the property and by this he

can reclaim the amount of money he spent on the property before leasing it for rent. Now,

considering the amount of money James is earning in a year on that basis he will be charged for

tax for the financial years. Depending on the amount of revenue James is earning on yearly basis,

the income tax inspectors will be checking the tax slabs and charge James accordingly.

ASSESSMENT ITEM 2

In this project since the main focus is on a single person, so after discussing the scenarios when

and where can a person be charged for tax, now it should be determined whether the amount

earned and the amount spent by James on the property to purchase as well as to renovate would

be taxable or not. After studying all the cases when a person can be taxed and in what situations,

it can be concluded that James would be chargeable for the entire amount spent by him. First, he

will be charged for the expenses for developing and renovating the properties that he had bought.

Secondly, he is liable to pay tax as the amount of money earned from leasing the property for

rent will earn revenues which will be source of income for him. So, since the building is

becoming a commercial one, so he will have to pay tax for the amount of money he is earning.

Another aspect that James can use to his benefit is that he can claim deductions in tax for the

amount of money he spent on purchasing, renovating and developing the property and by this he

can reclaim the amount of money he spent on the property before leasing it for rent. Now,

considering the amount of money James is earning in a year on that basis he will be charged for

tax for the financial years. Depending on the amount of revenue James is earning on yearly basis,

the income tax inspectors will be checking the tax slabs and charge James accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

ASSESSMENT ITEM 2

Reference list

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Jones, D. (2016). Capital gains tax: The rise of market value?. Taxation in Australia, 51(2), 67.

Kelly, J. F., Hunter, J., Harrison, C., & Donegan, P. (2013). Renovating housing policy (p. 1).

Melbourne: Grattan Institute.

Legal Database. (2017). Ato.gov.au. Retrieved 16 September 2017, from

https://www.ato.gov.au/law/view/document?docid=PAC/19970038/8-1

MacLaran, A. (2014). Making space: property development and urban planning. Routledge.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., ... Ting, A. K. F.

(2017). Principles of Taxation Law 2017. (10 ed.) Sydney: Thomson Reuters.

Tang, C. (2016). Australian GST update—2015. World Journal of VAT/GST Law, 5(1), 32-41.

Tang, C. (2016). Australian GST update—2015. World Journal of VAT/GST Law, 5(1), 32-41.

Tran‐Nam, B., & Evans, C. (2014). Towards the development of a tax system complexity index.

Fiscal Studies, 35(3), 341-370.

Wood, G., Ong, R., & Cigdem, M. (2016). Housing tax reform: Is there a way

forward?. Economic Papers: A journal of applied economics and policy, 35(4), 332-346.

Legal Database. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/law/#Law

Legal Database. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/law/view/document?Mode=type&TOC=

%2204%3ACases%3AAdministrative%20Appeals%20Tribunal

%3A2017%3ADeputy%20Commissioner%20of%20Taxation%20v.%20Pedley

%20(No%202)%20-%20(17%20August%202017)%3B%22&DOCID=%22JUD

%2F*2017*wadc107%2F00001%22

Residency tests. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-

your-tax-residency/Residency-tests/

Residency requirements for companies, corporate limited partnerships and trusts.

(2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/Business/International-tax-for-business/In-detail/

ASSESSMENT ITEM 2

Reference list

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Jones, D. (2016). Capital gains tax: The rise of market value?. Taxation in Australia, 51(2), 67.

Kelly, J. F., Hunter, J., Harrison, C., & Donegan, P. (2013). Renovating housing policy (p. 1).

Melbourne: Grattan Institute.

Legal Database. (2017). Ato.gov.au. Retrieved 16 September 2017, from

https://www.ato.gov.au/law/view/document?docid=PAC/19970038/8-1

MacLaran, A. (2014). Making space: property development and urban planning. Routledge.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., ... Ting, A. K. F.

(2017). Principles of Taxation Law 2017. (10 ed.) Sydney: Thomson Reuters.

Tang, C. (2016). Australian GST update—2015. World Journal of VAT/GST Law, 5(1), 32-41.

Tang, C. (2016). Australian GST update—2015. World Journal of VAT/GST Law, 5(1), 32-41.

Tran‐Nam, B., & Evans, C. (2014). Towards the development of a tax system complexity index.

Fiscal Studies, 35(3), 341-370.

Wood, G., Ong, R., & Cigdem, M. (2016). Housing tax reform: Is there a way

forward?. Economic Papers: A journal of applied economics and policy, 35(4), 332-346.

Legal Database. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/law/#Law

Legal Database. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/law/view/document?Mode=type&TOC=

%2204%3ACases%3AAdministrative%20Appeals%20Tribunal

%3A2017%3ADeputy%20Commissioner%20of%20Taxation%20v.%20Pedley

%20(No%202)%20-%20(17%20August%202017)%3B%22&DOCID=%22JUD

%2F*2017*wadc107%2F00001%22

Residency tests. (2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-

your-tax-residency/Residency-tests/

Residency requirements for companies, corporate limited partnerships and trusts.

(2017). Ato.gov.au. Retrieved 17 September 2017, from

https://www.ato.gov.au/Business/International-tax-for-business/In-detail/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ASSESSMENT ITEM 2

residency/residency-requirements-for-companies,-corporate-limited-partnerships-

and-trusts/

ASSESSMENT ITEM 2

residency/residency-requirements-for-companies,-corporate-limited-partnerships-

and-trusts/

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.