ACC6030: Analysis of Austal Ltd Audit Report and Auditor Opinion

VerifiedAdded on 2023/06/03

|18

|5352

|70

Case Study

AI Summary

This case study provides a comprehensive analysis of the audit report for Austal Ltd, a high-profile international company. The report employs a risk-based auditing approach to evaluate the "true and fair" status of the company's financial statements and critiques the opinion presented in the independent audit report. The analysis delves into key areas such as corporate governance, internal controls, auditor reporting obligations, and potential auditor negligence, relating these elements to relevant provisions and regulations. The methodology employed is descriptive research, assessing compliance with standards and regulations to determine the appropriateness of the auditor's opinion. Findings reveal compliance with provisions to a significant extent. The study incorporates figures illustrating success rates in safety measures and different types of audit procedures. The report concludes with recommendations concerning compliance and substantive procedures that auditors should apply when forming an opinion on financial reports, providing a valuable resource for understanding auditing and assurance services.

qwertyuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbnmqwe

rtyuiopasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwehjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbnmqwe

AUDITING AND ASSURANCE SERVICES

iopasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbnmqwe

rtyuiopasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwehjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbnmqwe

AUDITING AND ASSURANCE SERVICES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

A risk-based audit can be defined as an approach whose main concentration is on the intrinsic

risk present in activities or system and provide assurance that risk is being managed by the

administration within the defined risk administration function of an organisation by giving

assurance related to risk mitigation. Further, RBA enables the auditor to assert assurance to

the board of members that risk management processes are supervising risk efficiently,

corresponding to the risk appetite. Present report revolves around detail assessment of

auditor’s opinion of Austal Ltd. The report initiates with the description research

methodology which has been applied in the present result to attain an appropriate conclusion.

A further finding of important areas in order to comment on the opinion of the auditor, i.e.

corporate governance, internal control, auditor reporting obligation and auditor negligence

and contributory negligence have been explained. The same has been related to specific

provision and regulation in order to judge compliance of same in case of Austal Ltd. The

implication of provision in case of Austal Ltd. represents that the company has complied with

all required provision to a significant extent. Eventually recommendation have been provides

which explain compliance and substantive procedure which should be applied by the auditor

in order to provide opinion on financial report.

A risk-based audit can be defined as an approach whose main concentration is on the intrinsic

risk present in activities or system and provide assurance that risk is being managed by the

administration within the defined risk administration function of an organisation by giving

assurance related to risk mitigation. Further, RBA enables the auditor to assert assurance to

the board of members that risk management processes are supervising risk efficiently,

corresponding to the risk appetite. Present report revolves around detail assessment of

auditor’s opinion of Austal Ltd. The report initiates with the description research

methodology which has been applied in the present result to attain an appropriate conclusion.

A further finding of important areas in order to comment on the opinion of the auditor, i.e.

corporate governance, internal control, auditor reporting obligation and auditor negligence

and contributory negligence have been explained. The same has been related to specific

provision and regulation in order to judge compliance of same in case of Austal Ltd. The

implication of provision in case of Austal Ltd. represents that the company has complied with

all required provision to a significant extent. Eventually recommendation have been provides

which explain compliance and substantive procedure which should be applied by the auditor

in order to provide opinion on financial report.

Table of Contents

Introduction................................................................................................................................5

Methodology..............................................................................................................................5

Findings......................................................................................................................................6

Implication of findings...............................................................................................................9

Conclusion and recommendation.............................................................................................15

References................................................................................................................................17

Introduction................................................................................................................................5

Methodology..............................................................................................................................5

Findings......................................................................................................................................6

Implication of findings...............................................................................................................9

Conclusion and recommendation.............................................................................................15

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List of figures

Figure 1: Graph representing frequency rate of attainment of success in safety measures fro

employees.................................................................................................................................10

Figure 2: Type of Audit procedures.........................................................................................13

Figure 3: Directions in which assertion of an auditor are made..............................................14

Figure 1: Graph representing frequency rate of attainment of success in safety measures fro

employees.................................................................................................................................10

Figure 2: Type of Audit procedures.........................................................................................13

Figure 3: Directions in which assertion of an auditor are made..............................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Australian Auditing Standards provides requirements and specification relating to

responsibilities of an auditor relating to the audit of financial report as well as complete set of

books of accounts. As per assertions of Abu-Ras, (2015), it acts as a guidance tool for auditor

in conducting an audit of any company or organization. It establishes requirement and

explanation relating to the obligations of an auditor and the assurance practitioner while

performing audit, assurance or similar service engagements. In the present report analysis of

the annual report of Austal Ltd has been done through the application of the descriptive

methodology. The company is the world’s biggest aluminium shipbuilder, leading the global

market for high-speed craft (Austal Limited Annual Report 2017). Further, the significant

variants related to the risk audit procedure, i.e. corporate governance, internal control, auditor

negligence and reporting obligations have been discussed in detail in order to report on the

true and fair status of financial statements of Austal Ltd (Austal Limited Corporate

Governance Report 2017). Initially, provisions which are required to be followed by

management, as well as auditor, have been discussed. Further, with the assistance of

descriptive methodology findings relating to same of Austal Ltd have been ascertained. The

report concludes with the opinion that the audit has appropriately complied with required

provisions and after attainment of sufficient appropriate evidence had specified his opinion

relating to the financial report.

METHODOLOGY

The methodology applied in the present study is a descriptive research method which not fits

efficiently into the definition of quantitative and qualitative research methodologies.

Although it could use constituents of both, often within the same study. Further, Kemp, Hort

and Hollowood, (2018), assert that descriptive research consists of assembling of data which

explains the data collection. Since the mind of a human being cannot remove full import of a

large mass of raw data, descriptive statistics are extremely significant in decreasing the data

to an understandable manner. In addition to this, description emerges following creative

examination and serves up to organize the findings to fit them with explanations and then test

or certify those explanations (Larcker and Tayan, 2015). The explanation often elucidates

knowledge that may not otherwise be observed or even encounter. Furthermore, the same

method has been applied for the assessment of the financial report of Austal Ltd. In order to

Australian Auditing Standards provides requirements and specification relating to

responsibilities of an auditor relating to the audit of financial report as well as complete set of

books of accounts. As per assertions of Abu-Ras, (2015), it acts as a guidance tool for auditor

in conducting an audit of any company or organization. It establishes requirement and

explanation relating to the obligations of an auditor and the assurance practitioner while

performing audit, assurance or similar service engagements. In the present report analysis of

the annual report of Austal Ltd has been done through the application of the descriptive

methodology. The company is the world’s biggest aluminium shipbuilder, leading the global

market for high-speed craft (Austal Limited Annual Report 2017). Further, the significant

variants related to the risk audit procedure, i.e. corporate governance, internal control, auditor

negligence and reporting obligations have been discussed in detail in order to report on the

true and fair status of financial statements of Austal Ltd (Austal Limited Corporate

Governance Report 2017). Initially, provisions which are required to be followed by

management, as well as auditor, have been discussed. Further, with the assistance of

descriptive methodology findings relating to same of Austal Ltd have been ascertained. The

report concludes with the opinion that the audit has appropriately complied with required

provisions and after attainment of sufficient appropriate evidence had specified his opinion

relating to the financial report.

METHODOLOGY

The methodology applied in the present study is a descriptive research method which not fits

efficiently into the definition of quantitative and qualitative research methodologies.

Although it could use constituents of both, often within the same study. Further, Kemp, Hort

and Hollowood, (2018), assert that descriptive research consists of assembling of data which

explains the data collection. Since the mind of a human being cannot remove full import of a

large mass of raw data, descriptive statistics are extremely significant in decreasing the data

to an understandable manner. In addition to this, description emerges following creative

examination and serves up to organize the findings to fit them with explanations and then test

or certify those explanations (Larcker and Tayan, 2015). The explanation often elucidates

knowledge that may not otherwise be observed or even encounter. Furthermore, the same

method has been applied for the assessment of the financial report of Austal Ltd. In order to

assess whether Austal Ltd has complied with specified provision and regulation or not, the

core of related provision will be ascertained. Further, in case compliance with the same has

been made it will be assumed that auditor has made an appropriate opinion. As an application

of descriptive research methodology leads to provide a result on the case to case basis. Thus,

the same method will be applied for evaluating assessment of corporate governance, internal

control, auditor regulatory obligation, auditor negligence and contributory negligence and

independence of auditor on an individual basis. If compliance has been made for each of the

above-specified variants than valid assertion can be made relating to the truthfulness of

opinion of auditor relating to financial report of Austal Ltd.

FINDINGS

Ethics and Culture: Accounting Professional and Ethical Standards Board (APES) 110 had

issued the code of principles for professional accountants, signifies that associates of the

company are expected to work with the courage and the regulations. In accordance with the

study of Duska, Duska, and Kury (2018) code of ethics provides that ethics are an attitude of

mind on primary basis rather than compliance with written rules of conduct. It also sets out

key ethical statements concerning the responsibility of an audit (Hay, Knehcel and Willekens,

2014). It is necessary that auditors must operate with the relevant ethical obligations.

Moreover, APES 110 comprises three segments, and they are:

General Application of code

Associates in public practice

Members in organisation

The five fundamental principles which are required to be followed by all the members are

integrity, objectivity, confidentiality, professional behaviour and professional competence

and due care. Thus, an audit is to be conducted on the basis of specified variants.

Corporate governance: It can be specified as a system through with companies are managed

as well as directed. It comprises a relationship between management, shareholders and board

and obligations of the board of directors. There are some principles which are described

under the council of ASX related to the corporate governance, and same are required to be

followed by the companies in developing their corporate governance structure:

core of related provision will be ascertained. Further, in case compliance with the same has

been made it will be assumed that auditor has made an appropriate opinion. As an application

of descriptive research methodology leads to provide a result on the case to case basis. Thus,

the same method will be applied for evaluating assessment of corporate governance, internal

control, auditor regulatory obligation, auditor negligence and contributory negligence and

independence of auditor on an individual basis. If compliance has been made for each of the

above-specified variants than valid assertion can be made relating to the truthfulness of

opinion of auditor relating to financial report of Austal Ltd.

FINDINGS

Ethics and Culture: Accounting Professional and Ethical Standards Board (APES) 110 had

issued the code of principles for professional accountants, signifies that associates of the

company are expected to work with the courage and the regulations. In accordance with the

study of Duska, Duska, and Kury (2018) code of ethics provides that ethics are an attitude of

mind on primary basis rather than compliance with written rules of conduct. It also sets out

key ethical statements concerning the responsibility of an audit (Hay, Knehcel and Willekens,

2014). It is necessary that auditors must operate with the relevant ethical obligations.

Moreover, APES 110 comprises three segments, and they are:

General Application of code

Associates in public practice

Members in organisation

The five fundamental principles which are required to be followed by all the members are

integrity, objectivity, confidentiality, professional behaviour and professional competence

and due care. Thus, an audit is to be conducted on the basis of specified variants.

Corporate governance: It can be specified as a system through with companies are managed

as well as directed. It comprises a relationship between management, shareholders and board

and obligations of the board of directors. There are some principles which are described

under the council of ASX related to the corporate governance, and same are required to be

followed by the companies in developing their corporate governance structure:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The first principle of the corporate governance states that lay a solid basis for administration

and supervision. As per assertions of Husnin, Nawawi and Puteh Salin (2016), it specifies

that the organisational structure should be prepared in such a way so that it creates value for

the organization. Further, this principle states that the company should encourage fair and

responsible decision making (Armstrong, Blouin, Jagolinzer and Larcker, 2015). According

to the fourth principle of corporate governance, it is necessary that the company must make

safeguards reliability in the financial reports. According to Tricker and Tricker (2015), there

should be timely and fair disclosure of the financial reports. In accordance with the principles

of corporate governance, the rights of shareholders should be esteemed. Moreover, the risk

which is to be availed by the stakeholders should be identified and managed also. Lastly,

employees of the company should be compensated in a reasonable and responsible manner.

Internal Control: In accordance with provision specified in ASA 315, auditors are obliged to

have an understanding of internal control related to the audit. Thus, at the financial statement

level, the auditor’s assessment of the risk of material misstatement is influenced by their

understanding of the control environment. Further, as per study of Di Pietr, Ay, Art and

Ronen (2014), at the assertion level, it is necessary to evaluate the control risk while

analyzing the related to the risk of material misstatement that is to consider equity’s, i.e.

control risk. As per the study of Camfferman and Zeff (2015), in order to provide audit

evidence relating to internal controls relating to the risk of material misstatement at assertion

level, the auditor should assemble audit evidence about the existence, efficacy and stability of

controls. Proof of availability of controls is usually gained when the auditor is evaluating

control risk. Further, internal controls exist and are properly designed to prevent, identify and

correct the material misstatement. In accordance with ASA 330 eventually, a test of controls

are applied in their efficacy and to assess whether IC has functioned effectively during the

relevant period or not (Brasel, Doxey, Grenier and Reffett, 2016).

Perry and Nöelke, (2015), asserted that the main aspect of internal control for evidence is

effectiveness that is whether the control is functioning in an effective manner or not. The

same implies that does the control prevent or identify the misstatements that it is established

to prevent or detect. As per assertions of DeZoort and Harrison, (2018) effectiveness is

assessed as the constituent of a test of controls. The process for testing of internal control

includes re-considering of control such as examining the price, quantities , maths on the

invoice and detecting documents to perceive that controls were compiled with, for instance,

examining that a voucher consists supporting documentation (Euchner and Ganguly, 2014).

and supervision. As per assertions of Husnin, Nawawi and Puteh Salin (2016), it specifies

that the organisational structure should be prepared in such a way so that it creates value for

the organization. Further, this principle states that the company should encourage fair and

responsible decision making (Armstrong, Blouin, Jagolinzer and Larcker, 2015). According

to the fourth principle of corporate governance, it is necessary that the company must make

safeguards reliability in the financial reports. According to Tricker and Tricker (2015), there

should be timely and fair disclosure of the financial reports. In accordance with the principles

of corporate governance, the rights of shareholders should be esteemed. Moreover, the risk

which is to be availed by the stakeholders should be identified and managed also. Lastly,

employees of the company should be compensated in a reasonable and responsible manner.

Internal Control: In accordance with provision specified in ASA 315, auditors are obliged to

have an understanding of internal control related to the audit. Thus, at the financial statement

level, the auditor’s assessment of the risk of material misstatement is influenced by their

understanding of the control environment. Further, as per study of Di Pietr, Ay, Art and

Ronen (2014), at the assertion level, it is necessary to evaluate the control risk while

analyzing the related to the risk of material misstatement that is to consider equity’s, i.e.

control risk. As per the study of Camfferman and Zeff (2015), in order to provide audit

evidence relating to internal controls relating to the risk of material misstatement at assertion

level, the auditor should assemble audit evidence about the existence, efficacy and stability of

controls. Proof of availability of controls is usually gained when the auditor is evaluating

control risk. Further, internal controls exist and are properly designed to prevent, identify and

correct the material misstatement. In accordance with ASA 330 eventually, a test of controls

are applied in their efficacy and to assess whether IC has functioned effectively during the

relevant period or not (Brasel, Doxey, Grenier and Reffett, 2016).

Perry and Nöelke, (2015), asserted that the main aspect of internal control for evidence is

effectiveness that is whether the control is functioning in an effective manner or not. The

same implies that does the control prevent or identify the misstatements that it is established

to prevent or detect. As per assertions of DeZoort and Harrison, (2018) effectiveness is

assessed as the constituent of a test of controls. The process for testing of internal control

includes re-considering of control such as examining the price, quantities , maths on the

invoice and detecting documents to perceive that controls were compiled with, for instance,

examining that a voucher consists supporting documentation (Euchner and Ganguly, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In case the control is programmed for example examining authorisation codes, run

unauthorised business transaction by the program to ensure they are recognised appropriately

and excluded.

Reporting obligation of auditor: According to ASA 200, the main goal of an audit of the

financial statement is to acquire reasonable assurance regarding whether the financial report

which is used use as a whole is without material misstatement thus facilitating the auditor to

express a view as to whether the financial statement is produced in all material respects in

according with an appropriate financial framework (Ghosh and Tang, 2015). It is required

that the inspection of financial reports is conducted according to the regulated Australian

auditing standards (Barth, Landsman and Lang, 2018).

Section 308 of Corporate Act 2001 specifies that the audit report should state the auditor’s

opinion regarding compliance with accounting standard and true and fair view. Further,

section 308 (3 (b) specifies that auditor is obliged to form a view on the issues noted during

the audit. Along with this, Martinov-Bennie and Mladenovic, (2015), asserts that it is

required to include the same points in the reports of the auditor if there is a shortage, failure

or deficiency regarding any those of those specified issues.

Auditor negligence and contributory negligence – A successful negligence claim entails only

in case the plaintiff are in a position to prove various issues (Chartered Accountants Australia

and New Zealand (CAANZ), 2015). Firstly, the defendant should owe the plaintiff a

responsibility of care, based upon the valid foreseeability of the defendant’s act or oversight

causing plaintiff loss and physical, casual or incidental proximity between the two. Further,

As per assertion of Hentati-Klila, Dammak-Barkallah and Affes, (2017), the defendant’s

behaviour may not succeed to reach a dispassionately determined of the care. In addition to

this, the defendant’s failure to attain the standard of care must cause the plaintiff’s loss, and

finally, the loss occurred should be reasonably predictable. Moreover, according to Bamber

and McMeeking (2016), the auditor who provides his statement to the organisation in the

usual manner could not be accountable till his objective or one of his goals, in preparing the

reports that are to induce the plaintiff or a class which comprises the plaintiff.

Further, in accordance with division 2A section 331AA, of Corporation Law 2001, a

published audit report increases the reliability of the published financial reports which it

escorts for the advantages of the individuals, those who have no other reasonable way of

acquiring this information. The main objective of this division is to substantiate the right of

unauthorised business transaction by the program to ensure they are recognised appropriately

and excluded.

Reporting obligation of auditor: According to ASA 200, the main goal of an audit of the

financial statement is to acquire reasonable assurance regarding whether the financial report

which is used use as a whole is without material misstatement thus facilitating the auditor to

express a view as to whether the financial statement is produced in all material respects in

according with an appropriate financial framework (Ghosh and Tang, 2015). It is required

that the inspection of financial reports is conducted according to the regulated Australian

auditing standards (Barth, Landsman and Lang, 2018).

Section 308 of Corporate Act 2001 specifies that the audit report should state the auditor’s

opinion regarding compliance with accounting standard and true and fair view. Further,

section 308 (3 (b) specifies that auditor is obliged to form a view on the issues noted during

the audit. Along with this, Martinov-Bennie and Mladenovic, (2015), asserts that it is

required to include the same points in the reports of the auditor if there is a shortage, failure

or deficiency regarding any those of those specified issues.

Auditor negligence and contributory negligence – A successful negligence claim entails only

in case the plaintiff are in a position to prove various issues (Chartered Accountants Australia

and New Zealand (CAANZ), 2015). Firstly, the defendant should owe the plaintiff a

responsibility of care, based upon the valid foreseeability of the defendant’s act or oversight

causing plaintiff loss and physical, casual or incidental proximity between the two. Further,

As per assertion of Hentati-Klila, Dammak-Barkallah and Affes, (2017), the defendant’s

behaviour may not succeed to reach a dispassionately determined of the care. In addition to

this, the defendant’s failure to attain the standard of care must cause the plaintiff’s loss, and

finally, the loss occurred should be reasonably predictable. Moreover, according to Bamber

and McMeeking (2016), the auditor who provides his statement to the organisation in the

usual manner could not be accountable till his objective or one of his goals, in preparing the

reports that are to induce the plaintiff or a class which comprises the plaintiff.

Further, in accordance with division 2A section 331AA, of Corporation Law 2001, a

published audit report increases the reliability of the published financial reports which it

escorts for the advantages of the individuals, those who have no other reasonable way of

acquiring this information. The main objective of this division is to substantiate the right of

the individual to take action in opposition to an auditor where the auditor’s conduct in

preparing an audit statement has caused the person reasonably predictable loss. In addition to

this, as per study of Griffiths (2016), it is the responsibility of an auditor to make sure that

company is not publishing the financial reports of the company of the year which is deceptive

or unreliable. Moreover, as per specification provided in section 331AC of Corporations Act

2001 individual suffering loss or damage because of reasonable dependence on the conduct

of an auditor’s breach with provision of section 331 AB might recuperate the sum of that loss

or damage by action against the auditor or any other individual involved in the contravention

(Barth, Landsman and Lang, 2018). It has been specified in section 331AD that the court

might have regard to the following matters in ascertaining whether it is reasonable for an

individual to depend on the audit opinion and same are:

The accessibility of other sources of information in order to provide reliability to the

organisation’s financial reports.

The capability of an individual to search for other sources of information.

Any other issue which courts considers fit.

IMPLICATION OF FINDINGS

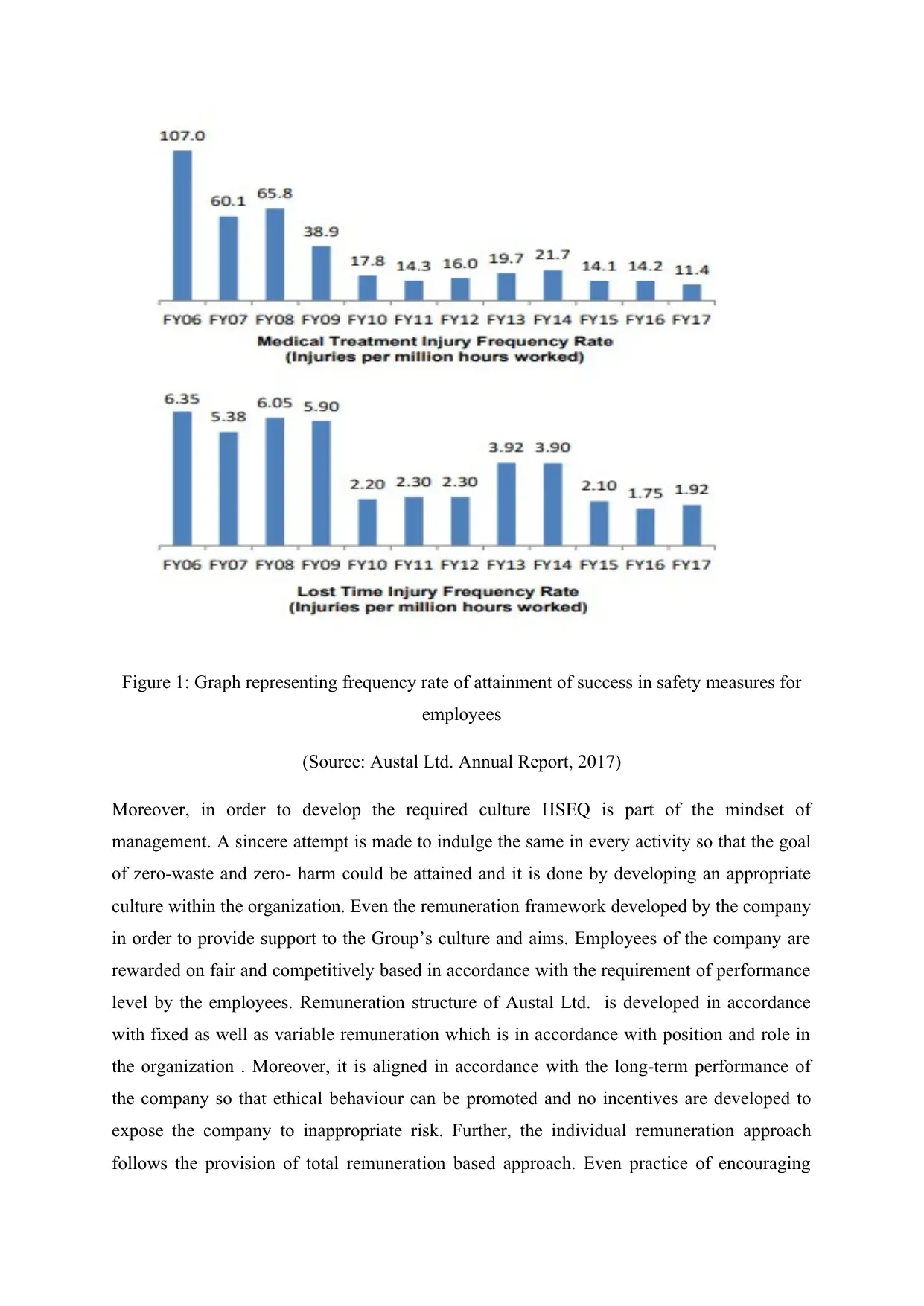

Policies followed by Austal Ltd. specifies that the company attempts to develop positive and

healthy culture. It can be accessed through its main approach named as ‘Zero Harm’

underscoring Austal’s commitment with its customers, employees, regulators and other

organizations with which it works. The success in same can be evaluated by the

achievements of the company as it made a significant reduction in frequency rate of injury,

i.e. 15% in five consecutive years (Austal Limited Annual Report 2017). The company

believes that the safety of employees, customer and another significant stakeholder

importance for the company. In order to attain the same, the company focuses on (Health,

Safety, Environment and Quality) HSEQ, which is more than a metric for Austal Ltd.

preparing an audit statement has caused the person reasonably predictable loss. In addition to

this, as per study of Griffiths (2016), it is the responsibility of an auditor to make sure that

company is not publishing the financial reports of the company of the year which is deceptive

or unreliable. Moreover, as per specification provided in section 331AC of Corporations Act

2001 individual suffering loss or damage because of reasonable dependence on the conduct

of an auditor’s breach with provision of section 331 AB might recuperate the sum of that loss

or damage by action against the auditor or any other individual involved in the contravention

(Barth, Landsman and Lang, 2018). It has been specified in section 331AD that the court

might have regard to the following matters in ascertaining whether it is reasonable for an

individual to depend on the audit opinion and same are:

The accessibility of other sources of information in order to provide reliability to the

organisation’s financial reports.

The capability of an individual to search for other sources of information.

Any other issue which courts considers fit.

IMPLICATION OF FINDINGS

Policies followed by Austal Ltd. specifies that the company attempts to develop positive and

healthy culture. It can be accessed through its main approach named as ‘Zero Harm’

underscoring Austal’s commitment with its customers, employees, regulators and other

organizations with which it works. The success in same can be evaluated by the

achievements of the company as it made a significant reduction in frequency rate of injury,

i.e. 15% in five consecutive years (Austal Limited Annual Report 2017). The company

believes that the safety of employees, customer and another significant stakeholder

importance for the company. In order to attain the same, the company focuses on (Health,

Safety, Environment and Quality) HSEQ, which is more than a metric for Austal Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1: Graph representing frequency rate of attainment of success in safety measures for

employees

(Source: Austal Ltd. Annual Report, 2017)

Moreover, in order to develop the required culture HSEQ is part of the mindset of

management. A sincere attempt is made to indulge the same in every activity so that the goal

of zero-waste and zero- harm could be attained and it is done by developing an appropriate

culture within the organization. Even the remuneration framework developed by the company

in order to provide support to the Group’s culture and aims. Employees of the company are

rewarded on fair and competitively based in accordance with the requirement of performance

level by the employees. Remuneration structure of Austal Ltd. is developed in accordance

with fixed as well as variable remuneration which is in accordance with position and role in

the organization . Moreover, it is aligned in accordance with the long-term performance of

the company so that ethical behaviour can be promoted and no incentives are developed to

expose the company to inappropriate risk. Further, the individual remuneration approach

follows the provision of total remuneration based approach. Even practice of encouraging

employees

(Source: Austal Ltd. Annual Report, 2017)

Moreover, in order to develop the required culture HSEQ is part of the mindset of

management. A sincere attempt is made to indulge the same in every activity so that the goal

of zero-waste and zero- harm could be attained and it is done by developing an appropriate

culture within the organization. Even the remuneration framework developed by the company

in order to provide support to the Group’s culture and aims. Employees of the company are

rewarded on fair and competitively based in accordance with the requirement of performance

level by the employees. Remuneration structure of Austal Ltd. is developed in accordance

with fixed as well as variable remuneration which is in accordance with position and role in

the organization . Moreover, it is aligned in accordance with the long-term performance of

the company so that ethical behaviour can be promoted and no incentives are developed to

expose the company to inappropriate risk. Further, the individual remuneration approach

follows the provision of total remuneration based approach. Even practice of encouraging

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

meritocracy is being followed by the company for the ascertainment of individual

performance with focusing on contribution, ethics and safety. Thus, it can be concluded that

the company has followed provisions relating to ethics and culture in an appropriate manner

which are necessary for an organization in order to comply with the specified provision.

Corporate governance statement of the company asserts that Board of Director and senior

executives of the company are committed to the best practices of corporate governance, risk

management and ethical standards (Austal Limited Corporate Governance Report, 2017).

However, the company has provided its corporate governance statement at its website rather

than annual report. Board of the company is made responsible for assisting and assessing the

consolidated entity on behalf of shareholders. Further, the structure of corporate governance

has been developed in accordance with ASX Corporate Governance so that both the

structures could be aligned. It can be accessed from the corporate governance statement of

the company that the company has followed the majority of the provision of ASX corporate

governance Austal Limited Corporate Governance Report, 2017). A few of provision which

has been partially complied have been appropriately discussed in the related report in order to

provide justification behind same. Ethical standards which are followed by Board of

directors comprise the specified variants:

Behave honestly and in good faith.

Implement due care and diligence in order to accomplish obligation relating to the

organization.

Application of their powers to act in best interest of Austan Ltd.

Ignorance of conflict and provide full disclosure relating to possible conflict of

interest

Compliance with the provision of law

Taking independent judgements in order to assure the soundness of Board decision.

The existence of the above variants represents that appropriate corporate governance

structure is developed as well as complied in Austal Ltd.

Board Management is responsible for developing as well as maintaining internal control, and

the auditor is responsible for the assessment of the existence of internal control through

understanding the business environment. In the present case of Austal Ltd. Board has shaped

as well as reviewed the risk appetite along with the internal process and procedure in order to

performance with focusing on contribution, ethics and safety. Thus, it can be concluded that

the company has followed provisions relating to ethics and culture in an appropriate manner

which are necessary for an organization in order to comply with the specified provision.

Corporate governance statement of the company asserts that Board of Director and senior

executives of the company are committed to the best practices of corporate governance, risk

management and ethical standards (Austal Limited Corporate Governance Report, 2017).

However, the company has provided its corporate governance statement at its website rather

than annual report. Board of the company is made responsible for assisting and assessing the

consolidated entity on behalf of shareholders. Further, the structure of corporate governance

has been developed in accordance with ASX Corporate Governance so that both the

structures could be aligned. It can be accessed from the corporate governance statement of

the company that the company has followed the majority of the provision of ASX corporate

governance Austal Limited Corporate Governance Report, 2017). A few of provision which

has been partially complied have been appropriately discussed in the related report in order to

provide justification behind same. Ethical standards which are followed by Board of

directors comprise the specified variants:

Behave honestly and in good faith.

Implement due care and diligence in order to accomplish obligation relating to the

organization.

Application of their powers to act in best interest of Austan Ltd.

Ignorance of conflict and provide full disclosure relating to possible conflict of

interest

Compliance with the provision of law

Taking independent judgements in order to assure the soundness of Board decision.

The existence of the above variants represents that appropriate corporate governance

structure is developed as well as complied in Austal Ltd.

Board Management is responsible for developing as well as maintaining internal control, and

the auditor is responsible for the assessment of the existence of internal control through

understanding the business environment. In the present case of Austal Ltd. Board has shaped

as well as reviewed the risk appetite along with the internal process and procedure in order to

assure that management has succeeded in development and implementation of risk

management and internal control (Austal Limited Annual Report 2017). Even the Audit and

Risk Committee has specified that they are responsible for assuring the appropriateness of

system and procedure relating to internal control. Moreover, they are also liable for internal

control programs and policies which are to be aligned by management relating to the

company’s reporting system. Thus the above specifications specify that the company has

developed and implemented an appropriate structure in order to monitor the existence of

internal control. It has been provided in the annual report of Austal Ltd that no contravention

has been made relating to auditor independence requirement as per Corporations Act 2001

and applicability of code of professional conduct relating to audit (Adelopo, 2016). As the

opinion has been formed after compliance with provisions of APES 110 code of ethics for

professional accountant and corporation act 2001. Thus, it can be analysed that all the

provision relating to reporting obligation and auditor negligence and contributory negligence

have been compiled by the auditor. Further, provision of Corporation Act 2001 has been

followed in order to develop a report and conclude audit procedure in accordance with the

same. It has also been stated that audit evidence which has been obtained by the auditor are

sufficient and appropriate in accordance with their opinion (Austal Limited Annual Report

2017). Moreover, they have also fulfilled the obligations specified in Auditor’s

Responsibilities for the Audit of Financial Report section relating to the audit report.

Even the audit procedures have been developed in such a manner that they are able to assess

the risk of material misstatement relating to the financial report. Further, Key Audit matters

have also been specified by the auditor along with the manner in which same have been dealt

with. Above specified facts represent that auditor has accomplished their duties in an

appropriate manner and a sincere effort has been made to assure compliance with related

provision and regulations. The audit of Austal Ltd has been conducted in accordance with

Australian Auditing Standard. The auditors have ascertained and analyzed the risk of material

misstatement in the financial report relating to fraud or error (Austal Limited Annual Report

2017).

management and internal control (Austal Limited Annual Report 2017). Even the Audit and

Risk Committee has specified that they are responsible for assuring the appropriateness of

system and procedure relating to internal control. Moreover, they are also liable for internal

control programs and policies which are to be aligned by management relating to the

company’s reporting system. Thus the above specifications specify that the company has

developed and implemented an appropriate structure in order to monitor the existence of

internal control. It has been provided in the annual report of Austal Ltd that no contravention

has been made relating to auditor independence requirement as per Corporations Act 2001

and applicability of code of professional conduct relating to audit (Adelopo, 2016). As the

opinion has been formed after compliance with provisions of APES 110 code of ethics for

professional accountant and corporation act 2001. Thus, it can be analysed that all the

provision relating to reporting obligation and auditor negligence and contributory negligence

have been compiled by the auditor. Further, provision of Corporation Act 2001 has been

followed in order to develop a report and conclude audit procedure in accordance with the

same. It has also been stated that audit evidence which has been obtained by the auditor are

sufficient and appropriate in accordance with their opinion (Austal Limited Annual Report

2017). Moreover, they have also fulfilled the obligations specified in Auditor’s

Responsibilities for the Audit of Financial Report section relating to the audit report.

Even the audit procedures have been developed in such a manner that they are able to assess

the risk of material misstatement relating to the financial report. Further, Key Audit matters

have also been specified by the auditor along with the manner in which same have been dealt

with. Above specified facts represent that auditor has accomplished their duties in an

appropriate manner and a sincere effort has been made to assure compliance with related

provision and regulations. The audit of Austal Ltd has been conducted in accordance with

Australian Auditing Standard. The auditors have ascertained and analyzed the risk of material

misstatement in the financial report relating to fraud or error (Austal Limited Annual Report

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.